- 4Q18’s volatility was disproportionately large relative to the strength in US fundamentals.

- Profits growth will likely slow in 2019, but growth rates should remain positive. We do not see a profits recession until 2020 or later.

- Liquidity is starting to be withdrawn from the global economy, but this is a normal late-cycle development.

- The stock market reflects behavior in the real economy. Investors and, more importantly, corporations have been very skittish. Those fears have limited irrational behavior throughout the cycle.

- Stock market volatility, therefore, does not appear to be primarily attributable to traditional fundamental variables. Rather, a highly capricious political environment is making corporate and household planning nearly impossible.

- Investors must keep their wits, ignore short-term noise, and invest based on longer-term fundamentals.

2018 ended with an emotional “run” on the equity market during which fear played a larger role than did fundamentals. 2019 is likely to be more fundamentally based and our portfolios are positioned for the opportunities we see, but investors should be wary of powerful late-cycle rallies that might occur despite slowing or deteriorating fundamentals.

Our portfolios are currently structured with a bias toward China, stable growth, and short-term Treasuries.

China is the only major economy attempting to stimulate

China’s stock market was one of the worst performers during 2018. The combination of a trade war and slowing global growth was not a good one for such an export dependent economy. However, the weakness in external demand for Chinese goods led the government to stimulate the domestic economy with significant monetary and fiscal programs. In fact, China is the only major economy that is attempting to incrementally stimulate their economy.

One of the reasons we were so bullish on the US economy earlier in the decade was our belief that monetary and fiscal stimulus would work. Many pundits suggested the US economy would have an “L” shaped recovery, meaning that the economy would basically never recover from the “Great Recession”, and that the business cycle was effectively dead. The US economy did, of course, recover and there was a significant bull market.

There are similarly negative statements made today regarding the future of the Chinese economy, and how their monetary and fiscal efforts will prove impotent.

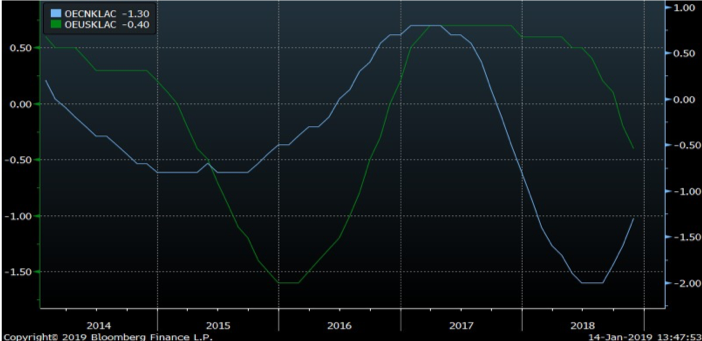

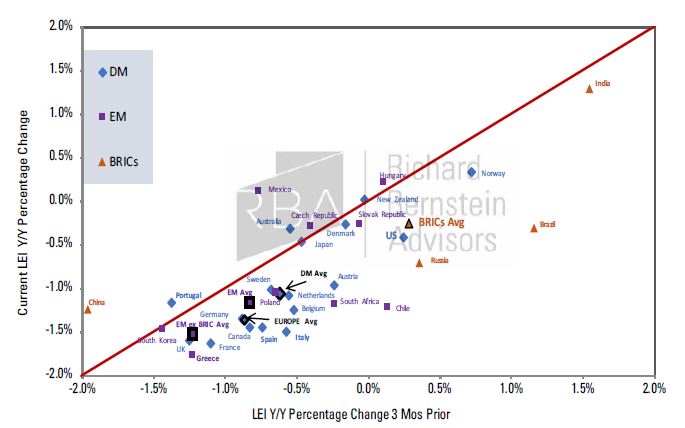

Chart 1 shows that there may be hope for the Chinese economy because of those stimulative measures. The chart compares the OECD Leading Economic Indicator for China versus that of the US, and the two indicators have been moving in opposite directions. Whereas the US indicator (green line) is increasingly suggesting an economic slowdown, the Chinese indicator (blue line) is beginning to improve. The China Leading Indicator’s recent improvement is quite unique. Chart 2 highlights that China is one of only two major economies with improving leading economic indicators (Australia is the other).

Admittedly, Chinese corporate profits have yet to improve, but evidence is starting to build that they might accelerate in 2019. China is our primary overweight outside the US.

CHART 1:

China vs. US: OECD Leading Indicators

Source: Richard Bernstein Advisors LLC, OECD, Bloomberg Finance L.P.

CHART 2:

LEI Momentum

Based on 1/14/19 OECD

Release

Source: Richard Bernstein Advisors LLC, OECD

Stable growth may be more important than Value vs. Growth

Consensus seems to favor value stocks over growth stocks for 2019, but that dichotomy may be the wrong way to frame the issue. Rather than value versus growth, we think a better comparison is stable growth versus cyclical growth.

Value traditionally outperformed growth when profits cycles accelerated because value stocks historically tend to be more cyclical than are growth stocks. However, growth outperformed value during 2018 as the profits cycle accelerated largely because growth stocks were more cyclical than value stocks. Chart 3 points out that growth stocks within the S&P 500® outperformed value stocks by about 900 basis points during 2018.

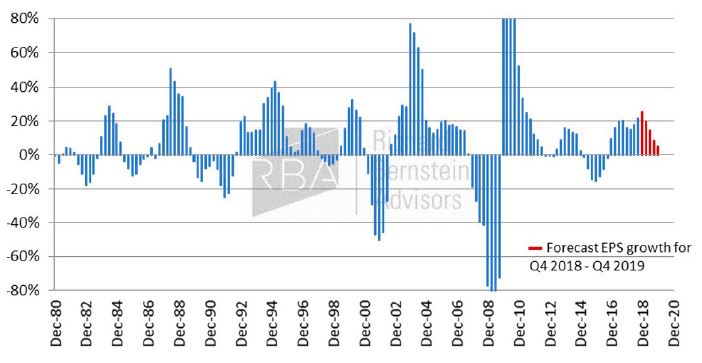

Chart 4 includes our forecast for S&P 500® reported earnings growth for 2019, and we expect the profits cycle to slow as the year progresses. We do not anticipate a full-blown profits recession, but we see profits growth slowing from roughly 25% in 4Q18 to roughly 5-7% in 4Q19. Historically that would argue growth might outperform.

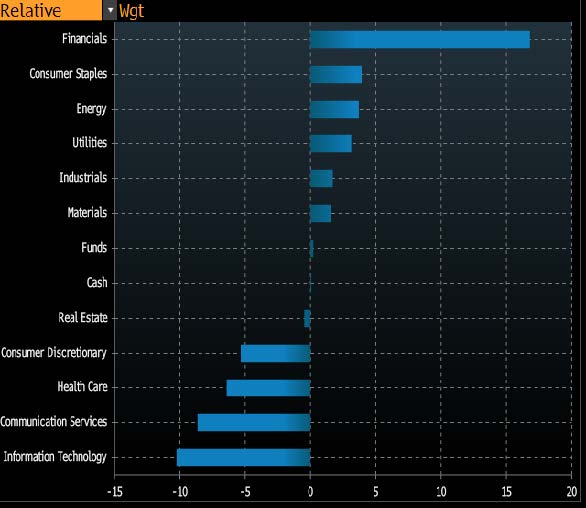

The problem with the traditional growth and value comparison is that both market segments are currently comprised of cyclical stocks. Chart 5 shows that value universes are presently dominated by financials, whereas growth universes are dominated by technology. The earning streams of both financials and technology are highly cyclical, so the argument today regarding growth versus value is simply one of cyclicals versus cyclicals.

CHART 3:

S&P 500® Growth vs. Value 2018

Performance

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

CHART 4:

S&P 500® Reported Y/Y Trailing GAAP EPS

Growth from Dec. 1980 -Sep. 2018

Source: Richard Bernstein Advisors LLC, Standard & Poor’s

CHART 5:

Relative Sector Weights:

S&P 500® Value Index vs. S&P 500® Growth

Index

Source: Bloomberg Finance L.P.

Stable growth is typically a critical characteristic when profits cycles decelerate. After all, cycles are determined by cyclicals, and if the profits cycle is indeed going to decelerate in 2019, then accordingly one should underweight cyclicals and overweight stable growth.

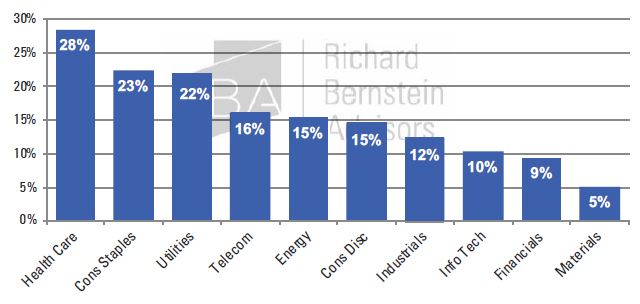

Overweighting stable growth has been considerably more important when the profits cycle decelerated than has worrying about growth or value. Chart 6 shows the performance of S&P 500® sectors when the profits cycle decelerates. Technology and Financials have historically been the 2nd and 3rd worst performing sectors when profits decelerated.

CHART 6:

Average Performance when Profits Decelerate: S&P 500®

Sectors

(Sep. 1989 - Dec. 2015*)

*Last profits cycle trough

Source: Richard Bernstein Advisors LLC, Standard and Poor's, Bloomberg Finance L.P.

Still little incentive to take duration risk

RBA avoided duration risk during 2018, and that proved to be prudent. Chart 7 shows the 2018 total return of various fixed-income indices, and shorter-duration bonds uniformly outperformed longer-duration ones. For example, the Bloomberg Barclays 1-3 Year Treasury Index was up roughly 2% for the year, whereas 20+ year Treasuries returned-2% with substantially more volatility.

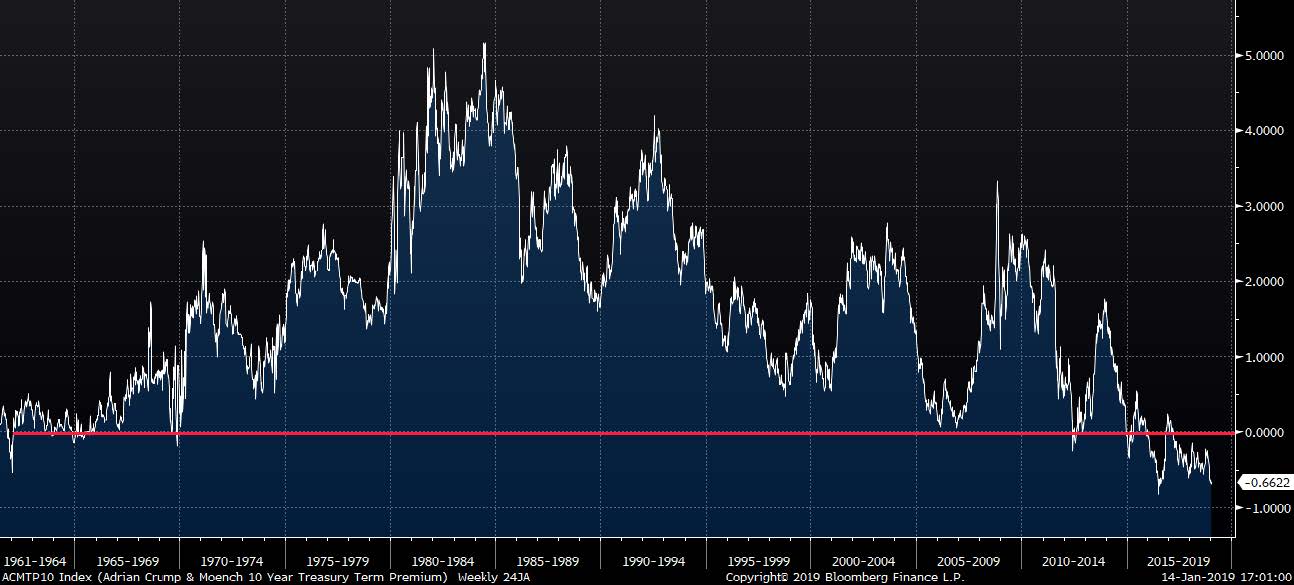

We continue to see little incentive to take duration risk within our portfolios. Chart 8 shows the term premium through time for the 10-year T-note. The term premium simply suggests whether it is better to buy one 10-year note or better to roll over 10 one-year notes. The recent term premium has been historically negative. A negative term premium suggests that investors are underpricing duration risk and that shorter- term notes will probably outperform longer-dated ones.

A negative term premium is a relatively rare occurrence (limited primarily to the current period and the early-1960s), but shorter-term notes have outperformed longer-term ones during most 12-month periods in which the term premium was negative. More importantly, RBA’s research shows that there is a strong correlation between the term premium and the probability and magnitude of longer-term notes out/ underperforming over subsequent 12-month periods.

CHART 7:

Fixed Income Indices 2018 Total Returns

Source: Bloomberg Finance L.P.

CHART 8:

10-Year Treasury Term

Premium

(Jun. 16, 1961 – Jan. 14, 2019)

Source: Bloomberg Finance L.P.

2019’s potential risk

Investors and companies are typically the most bullish at a market’s peak. Instead of reducing risk as market peak nears, investors and companies add cyclicality and ignore the business cycle because they believe “this time is different”. The resulting buildup of operating and financial leverage exacerbates cyclicality, and the businesses and the stock market become most sensitive to the economy right at the peak of a cycle.

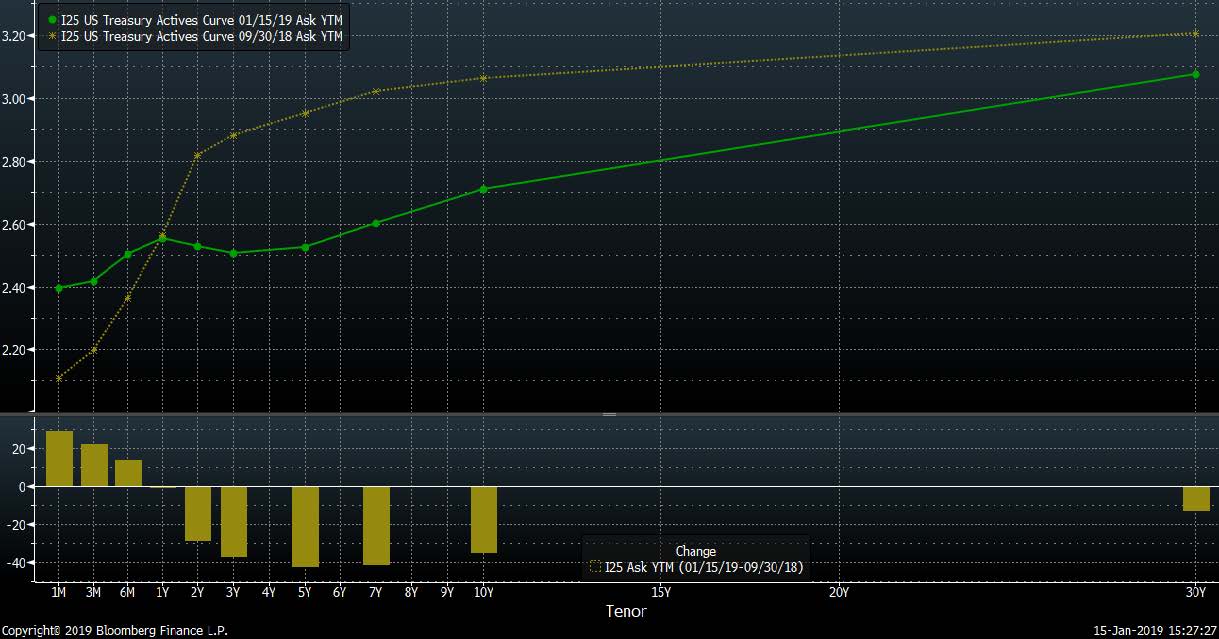

The fourth quarter’s emotional “run” on the market might be setting up such late-stage over-optimism. Although there is limited evidence that the corporate sector is accentuating cyclicality, some stock market investors are claiming that a new market cycle has begun despite that the yield curve has continued to flatten since market volatility rose (see Chart 9) and slowing earnings growth rate forecasts. Investors should be wary of a strong market rally during 2019 if that rally is coupled with waning profitability and an inverted yield curve. Increasing investor optimism amid deteriorating profits and liquidity has rarely, if ever, ended well.

CHART 9:

Slope of the US Treasuries Yield Curve:

Sep. 30, 2018 vs. Jan. 15, 2019

Source: Bloomberg Finance L.P.

Initial 2019 positioning

Although RBA’s various portfolios differ by risk characteristics and asset categories, the following general themes are embedded in our portfolios as we begin 2019:

We remain overweight equities, but not by nearly as much as we had been for the past several years. This reflects our view that profits growth will slow, but no profits recession is yet on the horizon.

We prefer to accentuate stable growth rather than either traditional growth or value. The growth and value universes are both presently dominated by cyclical industries that tend to underperform when profits decelerate.

Chinese stocks might present opportunities in 2019. Although our profit indicators have yet to turn (which would remove our uncertainty), China is the only major economy actively stimulating via monetary and fiscal policy. In addition, China is one of only two major economies in which leading indicators are accelerating. Profits remain a sizeable question mark.

The term premium is historically negative, and our fixed-income holdings are primarily short-maturity Treasuries. A negative term premium suggests that investors are underpricing the risks of longer-duration bonds. A decelerating profits cycle suggests quality over credit.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results.Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

S&P 500® Value Index: The S&P 500® Value Index is a free-float- adjusted, market-capitalization-weighted index. All the stocks in the underlying parent index are allocated into value or growth. Stocks that do not have pure value or pure growth characteristics have their market caps distributed between the value & growth indices.

S&P 500® Growth Index: The S&P 500® Growth Index is a free-float- adjusted, market-capitalization-weighted index. All the stocks in the underlying parent index are allocated into value or growth. Stocks that do not have pure value or pure growth characteristics have their market caps distributed between the value & growth indices.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

Fixed Income Indices:

Bloomberg Barclays US Aggregate Total Return: The Bloomberg Barclays US Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government- related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

Bloomberg Barclays U.S. Treasury: 20+ Year Total Return Index: The Bloomberg Barclays US Treasury Index measures US dollar- denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

Bloomberg Barclays U.S. Treasury: 7-10 Year Total Return Index: The Bloomberg Barclays US Treasury Index measures US dollar- denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

Bloomberg Barclays U.S. Treasury: 3-7 Year Total Return Index: The Bloomberg Barclays US Treasury Index measures US dollar- denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

Bloomberg Barclays U.S. Treasury: 1-3 Year Total Return Index: The Bloomberg Barclays US Treasury Index measures US dollar- denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

RBA Investment Process:

➜ Q uantitative indicators and macro-economic analysis are used to establish views on major secular and cyclical trends in the market.

➜ I nvestment themes focus on disparities between

fundamentals and sentiment.

➜ Market mis-pricings are identified relative to changes in the global economy, geopolitics and corporate profits.

© Copyright 2019 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors