Graham Allison published a controversial book in 2017 in which he argued that the probability for a major war increases when an established hegemon faces an emerging power that threatens the hegemon’s position. He used Thucydides, the Greek historian who wrote a history of the war between Sparta and Athens, as his model for superpower competition.1

Over the past few years, we have noted steady changes in American views toward China, and vice versa, that will likely lead to superpower competition and the potential for conflict. In Part I of this report, we will discuss the American and Chinese viewpoints. In Part II, we will summarize the two positions and examine the potential for war using the historical examples of British policy toward the U.S. and Germany, offering our take on which analogy best fits. There will be a discussion of current American views on hegemony as well. As always, we will conclude with market ramifications.

The American View

During the period of active American hegemony, the U.S. has faced only one serious competitor, the Soviet Union. When the Berlin Wall fell and the Soviet Union eventually collapsed, American foreign policy leadership tended to view this outcome as the victory of a superior system over the doomed totalitarian system of communism. After all, one of the primary architects of the Cold War, George Kennan, argued that the U.S. could outlast the Soviets because democracy and capitalism were superior.2 This position was reiterated by Francis Fukuyama in his argument that the fall of communism proved, once and for all, that the culmination of government and policy was capitalism and democracy, and that there was no other alternative available.3

When studying history it is important to understand how mankind has progressed and adapted to conditions over the years. However, it is not a science. Proving something using the scientific method requires the ability to create experiments and apply controls to prove that one thing causes another. In history, and in many of the social sciences, experimentation is impossible. Something happens—a war, market crash, epidemic, etc.—and we search for conditions that preceded the event and actions taken during the event to determine lessons. History and social sciences that try to examine human events that progress through time are vulnerable to the post hoc ergo propter hoc4 fallacy. Just because some event preceded an outcome doesn’t necessarily prove that it caused the specific outcome.

Unfortunately, much of the “stuff” of history does not lend itself to experimentation and decision makers still have to take action. Therefore, if they want to rely on history to improve the odds of success, what lessons from history do they draw? In the absence of experiments, we generally rely on narratives that weave a tale of how one thing in history caused another. Historians and social scientists then argue over which narrative is the best explanation.

Sadly, being human, the narrative that usually wins out is the one that puts a group in the best light. Arguing that the U.S. won the Cold War because its system was superior is going to be an attractive narrative. Suggesting that the U.S. won because of Russian geography was much less flattering. There is no doubt that capitalist economies fared better than communist economies, but it is also true that throughout Russian history the country has tended to expand (to force invaders to extend supply lines and rely on the Russian winter to destroy forces) and collapse (when the cost of empire became unsustainable). Thus, it is quite possible that the Soviet Union fell apart due less to its economic system and more due to its unfortunate geography that has no natural barriers to invasion.

For the most part, the lessons American policymakers took from winning the Cold War were that the systems of democracy and capitalism were superior and that all nations were destined to move toward these systems. This idea is known as the “Washington Consensus.”

U.S. policy toward China has been affected by this consensus. If the movement to democracy and capitalism was inevitable, then it was worth allowing Beijing to create conditions where foreign direct investment required the transfer of technical knowledge and letting China into the WTO on favorable terms. After all, eventually, China was going to be “just like us.”

There was some evidence to support this notion. The economic reforms under Deng Xiaoping moved China away from a Stalinist economy to a more market-driven one. China engaged with the global economy and Western companies flocked to place part of their supply chains into China. U.S. companies found a nearly infinite supply of low-cost workers. Rapid technology improvements allowed Western firms to shift an increasing amount of sophisticated processes abroad.5 However, extending supply chains to China did carry costs; China insisted on majority Chinese ownership and forced technology transfers. And, China purposely kept its currency undervalued, contributing to a massive trade surplus that reduced American jobs in manufacturing. Still, as long as China eventually became democratic, these costs were worth bearing.

The Chinese View

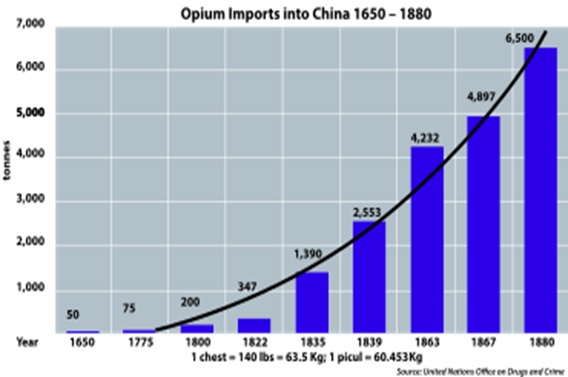

Although it is always difficult to determine key events in a nation’s history, we will argue that modern China was most affected by the Opium Wars.6 During the 17th and 18th centuries, Europeans discovered Chinese silk and tea. In the late 1600s, Chinese silk and tea represented just over 8% of the British East India company sales to Europe. By the middle of the 18th century, these two items represented almost 38% of sales.7 By the early 19th century, Britain was running a large trade deficit with China.8 By 1820, China had the largest economy in the world. This large and growing trade deficit led to constant outflows of silver to China. Under Hume’s Price/Specie theory, the rise of silver stocks should have led to inflation in China and an eventual reversal in trade flows. However, the emperor confiscated the silver from exporters, which kept prices from rising.9 Europe needed a product that China wanted in order to reverse the silver flow. And, it found it with opium.

(Source: U.N.)

As criminal syndicates and drug companies have discovered, opiates are ideal products because they turn their consumers into addicts. Economic theory argues that addictive substances have highly inelastic demand, meaning the demand curve is nearly vertical and therefore small supply constraints can bring soaring prices.

The Qing dynasty began to notice this problem and banned opium imports and domestic production in 1800. As observed in the U.S. “War on Drugs,” the results were less than impressive; the British and their local Chinese counterparts were able to smuggle opium into China unabated. In 1813, the emperor issued an edict making it illegal to smoke the drug. Again, no effect. Finally, in 1838, the emperor appointed a special commissioner, Lin Zexu, to end the trade for good. The commissioner, apparently zealous, arrested British opium dealers and confiscated 2.7 mm pounds (in weight) of opium. The British saw the arrests as an infringement on the crown and sent warships. The Chinese, who had been isolated from the rest of the world, had inferior military technology and suffered a stinging defeat in what became known as the First Opium War in 1842. The resolution of that war became the Treaty of Nanking. Essentially, the British could operate with impunity in China and also gained the port of Hong Kong in this treaty. Still, that didn’t seem enough which led to the Second Opium War, which ran from 1856 to 1860. This war essentially turned China into a vassal state. After the British gained access to China, various European nations, the U.S. and Japan all demanded access as well and the Qing emperor was powerless to halt the incursions. The Taiping Rebellion and the Boxer Rebellion, along with the persistent expansion of foreign holdings in China, led to the eventual collapse of the Qing dynasty in 1912.

China views the Opium Wars as a humiliating defeat at the hands of foreign powers. The lessons learned from the debacle were that foreigners have designs on China and the only way to prevent another humiliation is through unity. Disunity was a key factor that allowed foreign powers to gain control of China. Some Chinese citizens, especially on the outward-looking coast, cooperated with foreigners for profit. In the interior, a weak central government led to the rise of warlords. Part of the support for the Communist Party of China (CPC) comes from the fact that Mao was able to oust the Kuomintang led by Chiang Kai-shek and unify China (with the exception of Taiwan, still considered a province of the mainland). Mao did this by closing off China from the world and consolidating power. Accordingly, China became unified but very poor. Deng concluded that China, under CPC leadership, was unified enough to venture out into the world to improve the economy.

Part II

Next week, we will conclude this report with a summary of these two positions, examine the potential for war using the historical examples of British policy toward the U.S. and Germany, and offer our take on which analogy best fits. We will also discuss current American views on hegemony and conclude with market ramifications.

Bill O’Grady

January 28, 2019

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

[1] Allison, G. (2017). Destined for War: Can America and China Escape Thucydides’s Trap? New York, NY: Houghton Mifflin Harcourt Publishing Company.

See also: the Confluence Reading List.

[2]https://www.trumanlibrary.org/whistlestop/study_collections/coldwar/documents/pdf/6-6.pdf

[3] https://www.jstor.org/stable/24027184?read-now=1&seq=1#page_scan_tab_contents ; It should be noted that Fukuyama has attempted to “walk back” his argument, suggesting it was shorn of its nuance. Although that may be true, it did capture the essence of the era and became one of the tenets of U.S. policy in the post-Cold War era.

[4] “After this, therefore because of this.”

[5] The wave of globalization that developed in the 1990s was critically dependent on technology. See: Baldwin, R. (2016). The Great Convergence: Information Technology and the New Globalization. Cambridge, MA: Harvard University Press.

[6] This section borrows heavily from https://geopoliticalfutures.com/third-opium-war/ (paywall)

[7] Findlay, R. and O’Rourke, K. (2007). Power and Plenty: Trade, War, and the World Economy in the Second Millennium. Princeton, NJ: Princeton University Press.

[8] Esteban, J. C. (February 2001). The British balance of payments, 1772‐1820: India transfers and war finance. The Economic History Review, 54: pp. 58-86.

[9] This should sound familiar; this is how China was able to prevent the CNY from appreciating in the last decade when China was running a large trade surplus.

© Confluence Investment Management

Read more commentaries by Confluence Investment Management