Introductory economics classes discuss monetary policy’s inconsistent lead times. Many observers have described monetary policy as a blunt tool with which to steer the economy because of the unpredictability of both the timing and magnitude of effects associated with the easing or tightening of monetary policy.

A primary cause for that unpredictability is that the Federal Reserve cannot force banks to lend or not lend. The Fed might prefer a certain monetary policy track, but there is no guarantee that the private sector banking system will abide by the Fed’s desires. At the trough of a cycle, banks perceive lending to be so risky that their risk aversion can overwhelm the Fed’s desire for the banks to increase lending. That in turn forces the Fed to further ease monetary policy. Such risk aversion was so prevalent during the last recession that even 0% interest rates did not spur lending. We coined the phrase at that time, “you can lead a horse to water, but you can’t make it lend”.

At the peak of a cycle, however, banks’ lending profits can be so large that the thirst to lend more overwhelms the Fed’s desire for the banks to calm down. That in turn forces the Fed to further tighten policy. In most cycles, the Fed eventually tightens too much, and a recession subsequently occurs.

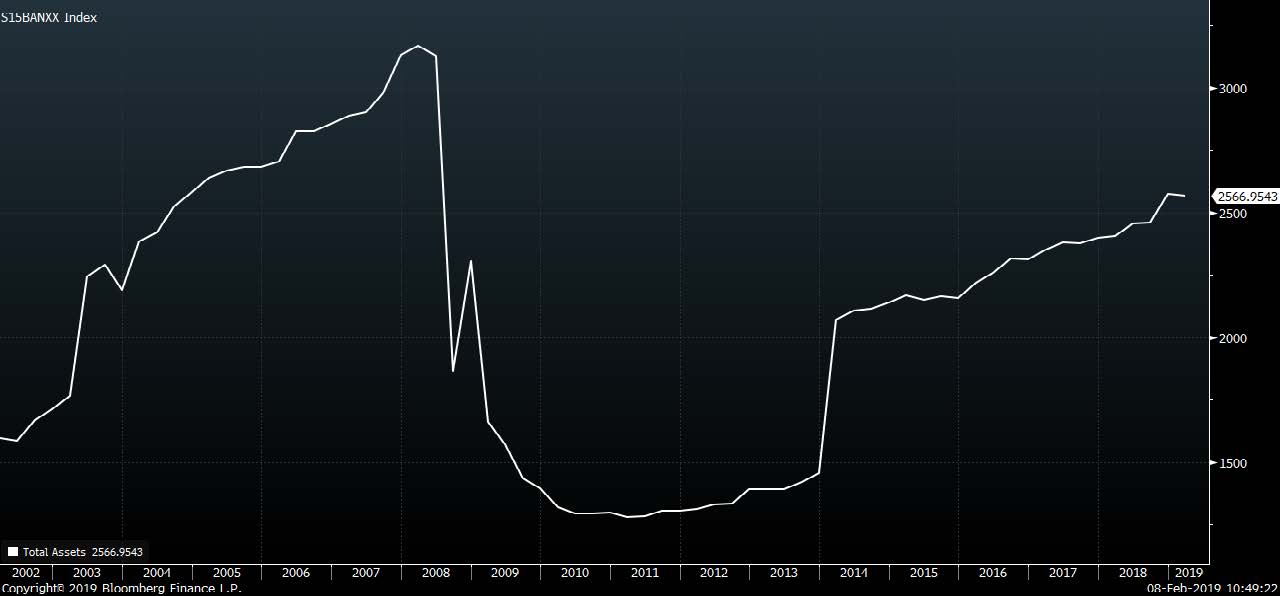

Chart 1 shows the total assets of the S&P 1500® Supercomposite Bank Index. Bank assets grew at a rapid pace in 2006/7 despite lending risk increasing significantly and the Fed raising rates. Bank assets then fell precipitously after 2008’s recession and it took years for banks to again expand their balance sheets. There are, of course, many reasons why bank balance sheets might change in size other than monetary policy. One should also examine accounting changes, regulatory changes, and the like. Nonetheless, bank balance sheets during the past 20 years reflect the long-standing problems associated with the lags associated with monetary policy.

CHART 1:

S&P 1500® Supercomposite Banks Index: Total

Assets (Mar. 2002 – Jan. 2019)

Source: Bloomberg Finance L.P. For Index descriptors, see “Index Descriptions” at end of document.

Source: Bloomberg Finance L.P. For Index descriptors, see “Index Descriptions” at end of document.

Once again, this cycle is more normal than investors believe

The current economic cycle remains remarkably normal despite claims that the cycle is unique or unprecedented. Similarly, the relationship between the Fed’s desire to set monetary policy and the banks’ business decisions have been somewhat out of step. As in previous cycles, the Fed raised rates before banks began to tighten credit.

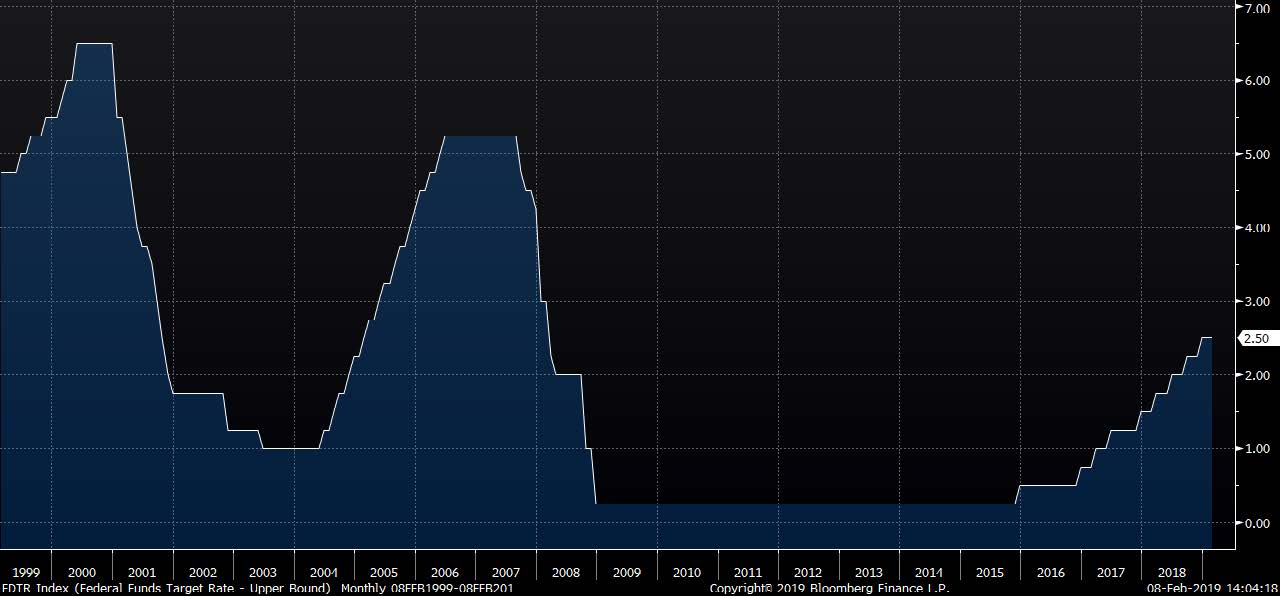

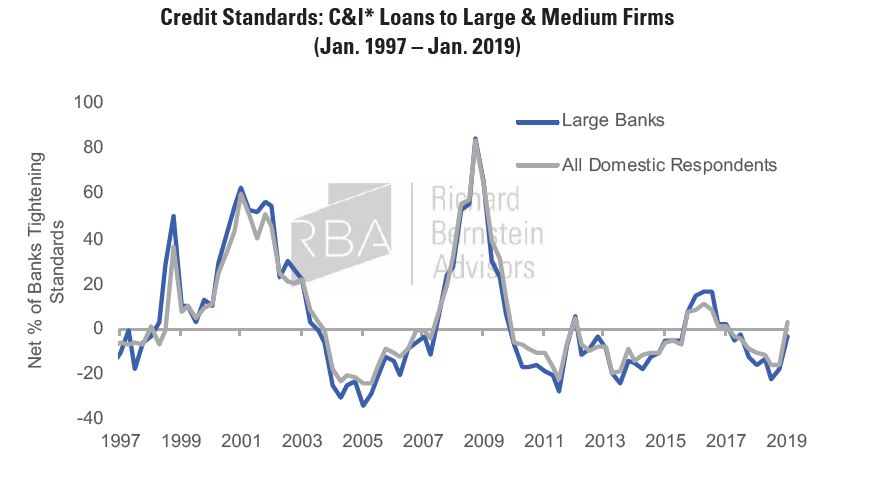

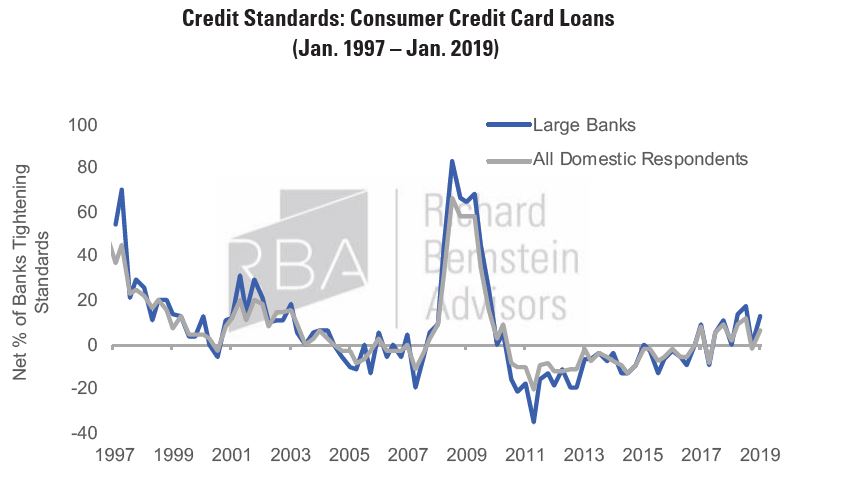

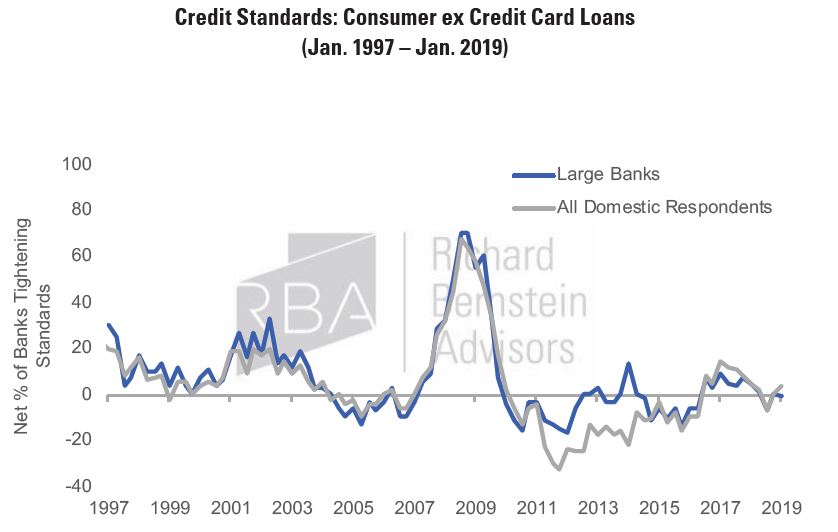

Chart 2 shows the Fed’s target rate for Fed Funds, and the Fed started raising rates (i.e., tightening policy) in December 2015. However, Charts 3-5 highlight that banks have only recently begun to tighten credit policies. These charts come from the Fed’s Senior Loan Officer Opinion Survey, and rising lines suggest a tightening of credit conditions. In some cases, such as Commercial and Industrial (C&I) Loans, banks were easing credit conditions during 2016 and 2017 despite that the Fed was tightening monetary policy.

The Fed has recently seemed squeamish about continuing to tighten monetary policy considering increased equity market volatility. However, the Fed’s survey of loan officers suggests that loan officers are tightening lending standards. Should this trend continue, banks would seem to be moving in the opposite direction of the Fed.

CHART 2:

Fed Funds Target

Rate (Jan. 1999 – Jan. 2019)

Source: Bloomberg Finance L.P.

CHART 3:

Source: Richard Bernstein Advisors LLC. FRB. *Commercial and Industrial. For Index descriptors, see “Index Descriptions” at end of document.

CHART 4:

Source: Richard Bernstein Advisors LLC. FRB. For Index descriptors, see “Index Descriptions” at end of document.

CHART 5:

Source: Richard Bernstein Advisors LLC. FRB. For Index descriptors, see “Index Descriptions” at end of document.

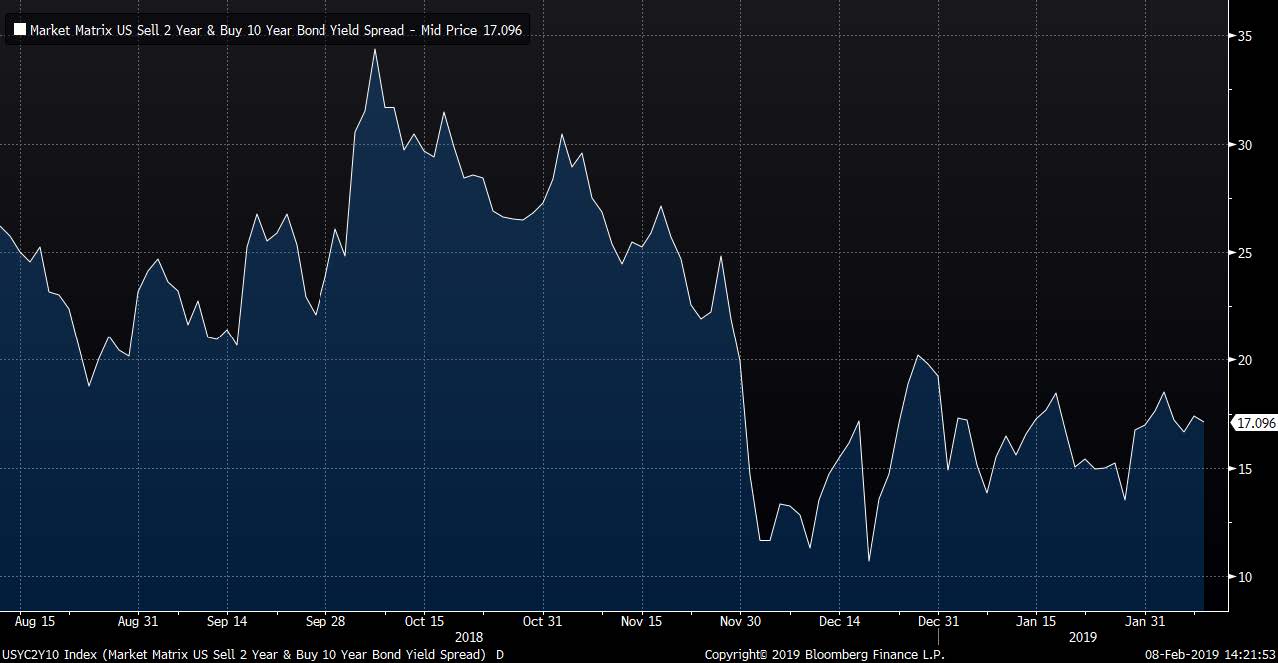

Market implication: watch banks not the Fed

The Fed has recently indicated that the equity market’s volatility has influenced the path of monetary policy, and many investors have suggested that a swift and sudden decline in equity prices would cause the Fed to ease. The markets, however, seem skeptical.

The slope of the yield curve, a reliable leading indicator of the economy, has continued to flatten. The yield spread between the 10-year t-note and the 2-year t-note was about 35 basis points before the fourth quarter’s financial market volatility. It is currently about 17 basis points, or roughly half as steep as it was before the recent period of increased volatility and concern. (See Chart 6.)

CHART 6:

Slope of the Yield Curve: 10-Yr Treasury – 2-Yr Treasury

(Aug. 2018 – Jan. 2019)

Source: Bloomberg Finance L.P.

A flat, but not inverted, yield curve has not historically been a warning signal. However, we find it curious that investors were very worried about the flattening yield curve when the 10-2 spread was twice what it is today, but today seem relatively unconcerned. The curve seems to be paying more attention to actual lending conditions (i.e., the loan officers) than to the Fed’s rhetoric.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results.Indices are not actively managed and investors cannot invest directly in the indices.

S&P 1500® Supercomposite Bank Index: Standard & Poor’s (S&P) 1500® Composite Bank Index: The S&P 1500® Composite Bank Index is an unmanaged, capitalization-weighted index designed to measure the performance of companies included in the S&P 1500® that are classified as members of the GICS® Level 2 Banks industry group.

Credit Standards: Measures the net percentage of respondents tightening based on the Federal Reserve’s Senior Loan Officer Opinion Survey on Bank Lending Practices. The Senior Loan Officer Opinion Survey includes up to eighty large domestic banks and twenty-four U.S. branches and agencies of foreign banks. Questions cover changes in the standards and terms of the banks’ lending and the state of business and household demand for loans. Note due to changes in the FRB’s categories, the Consumer Loans ex Credit Cards data is compiled as the “Consumer loans excluding credit cards” category prior to 2011 Q2, and is the sum of the “New and used autos” and the “Consumer loans excluding credit cards and autos” categories for the period 2011 Q2 through present.

© Copyright 2019 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors

Source: Bloomberg Finance L.P. For Index descriptors, see “Index Descriptions” at end of document.

Source: Bloomberg Finance L.P. For Index descriptors, see “Index Descriptions” at end of document. Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.