Emerging market equities were off to a strong start overall in 2019, rebounding from a 2018 downturn. Manraj Sekhon, CIO of Franklin Templeton Emerging Markets Equity, and Chetan Sehgal, senior managing director and director of portfolio management, outline what drove market moves in January and why they and the team think confidence in emerging markets should continue to improve.

Three Things We’re Thinking About Today

-

- As widely expected, the US Federal Reserve (Fed) left its key interest rate unchanged at its January meeting. A change in the Fed’s language and tone from its December meeting, indicating patience, signaled a likely pause or even halt in rate hikes. Flexibility in balance sheet normalization was also indicated. Market participants now widely expect one rate hike for 2019, down from two last month, leading market sentiment toward emerging-market (EM) equities and currencies to improve further. Portfolio flows into EMs have also turned positive in recent months, driven by renewed optimism in the asset class. EMs as a whole continue to demonstrate strong economic potential, with floating foreign exchange regimes, current account surpluses and more favorable debt levels than their developed-market (DM) peers.

- Progress in US-China trade talks, a stronger Chinese renminbi, implementation of supportive policies on the monetary and fiscal fronts as well as stimulus policies aimed at boosting consumption and tourism drove sentiment in Chinese equities in January. While gross domestic product (GDP) growth in China has eased recently, we do not expect a hard landing as long as the government maintains adequate liquidity and close control over the capital account. The economy continued to grow at a robust rate of over 6%, making the country one of the fastest growing major economies in the world. Meanwhile, a shift toward innovation, technology and consumption as primary drivers of growth could support sustainability over the long term. In the interim, however, we maintain a cautious view as a prolonged trade US-China trade dispute could lead to significant volatility. We will continue to monitor the situation and look for attractive investment opportunities in sectors related to health care, consumption and manufacturing upgrades, which over the long term, are less directly impacted by tariff regime changes.

Outlook

Investor sentiment in emerging markets continued to improve in January, supported by a dovish Fed and hopes for the United States and China to reach a trade deal by March, when higher US tariffs on Chinese goods are poised to set in.

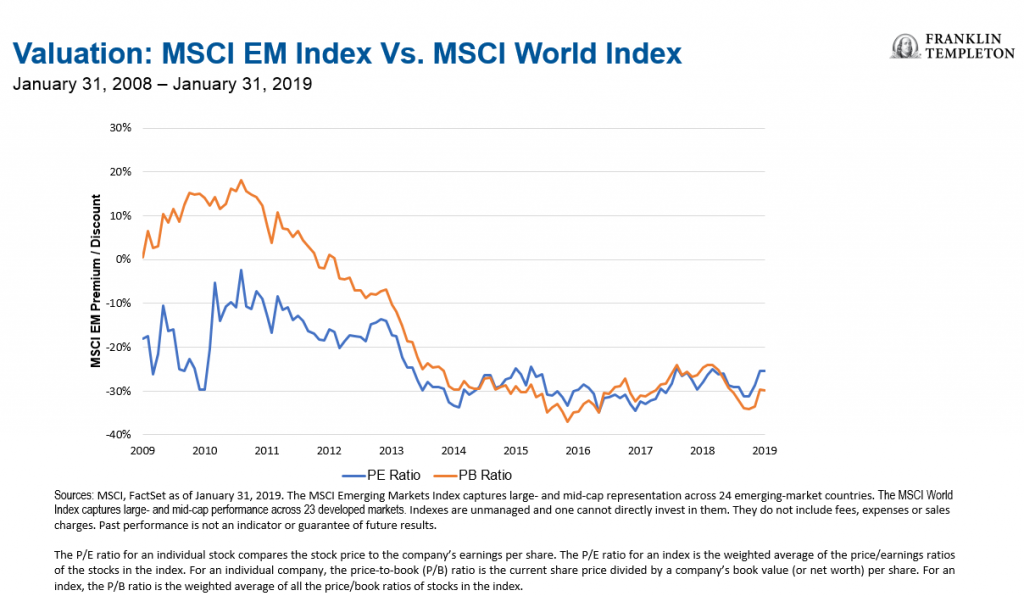

We believe that confidence in EMs could strengthen further based on several factors: economic growth differentials between EMs and DMs are widening in the former’s favor, EM currencies appear undervalued despite balance of payment surpluses in many markets, ongoing reforms, a robust EM earnings outlook and undemanding valuations.

Emerging markets are currently trading at a significant discount to developed markets (DMs), providing long-term investors with an attractive investment opportunity. As of end-January, the MSCI EM Index traded at a forward price-to-earnings (P/E) ratio of 11.4x and a price-to-book value (P/BV) of 1.6x, while DMs, as represented by the MSCI World Index had a forward P/E of 14.5 and P/BV of 2.3x1.

We are particularly upbeat about growth prospects for the information technology and consumer-related sectors. The growing adoption of technology and growth of digital platforms have helped create new goods and services for consumers across EMs, and at the same time creating growth opportunities for many EM companies and investors. Additionally, with most young people (those under the age of 30) in the world living in EMs, we believe there are tremendous opportunities for businesses that can effectively capture and serve this target market.

Emerging Markets Key Trends and Developments

Global stock markets began 2019 on a strong note, driven by optimism around US-China trade negotiations and hopes for a prolonged pause in US interest rate hikes. EM equities benefited from domestic currency strength and robust portfolio inflows to finish January ahead of their DM counterparts. The MSCI Emerging Markets Index rose 8.8% over the month, compared with a 7.8% return in the MSCI World Index, both in US dollars.

The Most Important Moves in Emerging Markets This Month

- Asian equities rebounded, aided by strong returns in Pakistan, China and South Korea. China’s stock market rallied, thanks to signs of progress in US-China trade talks and fresh policies to counter slower economic growth. South Korea’s benchmark index rose as technology heavyweights surged on the back of improved investor sentiment. Conversely, stocks in India declined. Expectations of increased government spending ahead of a general election this year raised concerns over the country’s fiscal deficit.

- In Latin America, Brazil, Colombia and Chile were among the leading performers, ending January with double-digit gains on the back of higher commodity prices and stronger domestic currencies. Positive expectations from the new administration further supported returns in Brazil. Peru and Mexico, while recording positive returns, lagged their regional peers. Concerns that severe fuel shortages, resulting from the government’s efforts to combat fuel and gasoline theft, could impact business operations weighed on sentiment in Mexican equities.

- Equity markets in emerging Europe also gained ground with Turkey and Russia leading the way. Higher oil prices and appreciation in the Russian ruble drove returns in that market. The Czech Republic, Hungary and Poland also posted solid gains but lagged their regional counterparts. The South African rand was among the best-performing EM currencies in January, driving equity gains in US-dollar terms. Higher metal prices drove returns in steel and platinum companies, while weaker-than-expected Christmas sales data and profit warnings from a number of companies weighed on retailers in South Africa.

- Frontier markets ended the month with positive returns, but fared worse than their global counterparts. Argentina and Kenya led returns, although Vietnam and Kuwait also recorded gains. Romania and Nigeria, however, recorded declines. Appreciation in the Argentine peso and easing inflation supported sentiment in its stock market. Concerns surrounding the upcoming presidential elections in Nigeria weighed on investor confidence, while the government’s decision to implement a levy on the financial sector in Romania worried investors.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The comments, opinions and analyses expressed herein are solely the views of the author(s), are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

_________________________________

1. Sources: MSCI, FactSet as of January 31, 2019. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. The P/E ratio for an individual stock compares the stock price to the company’s earnings per share. The P/E ratio for an index is the weighted average of the price/earnings ratios of the stocks in the index. For an individual company, the price-to-book (P/B) ratio is the current share price divided by a company’s book value (or net worth) per share. For an index, the P/B ratio is the weighted average of all the price/book ratios of stocks in the index.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments