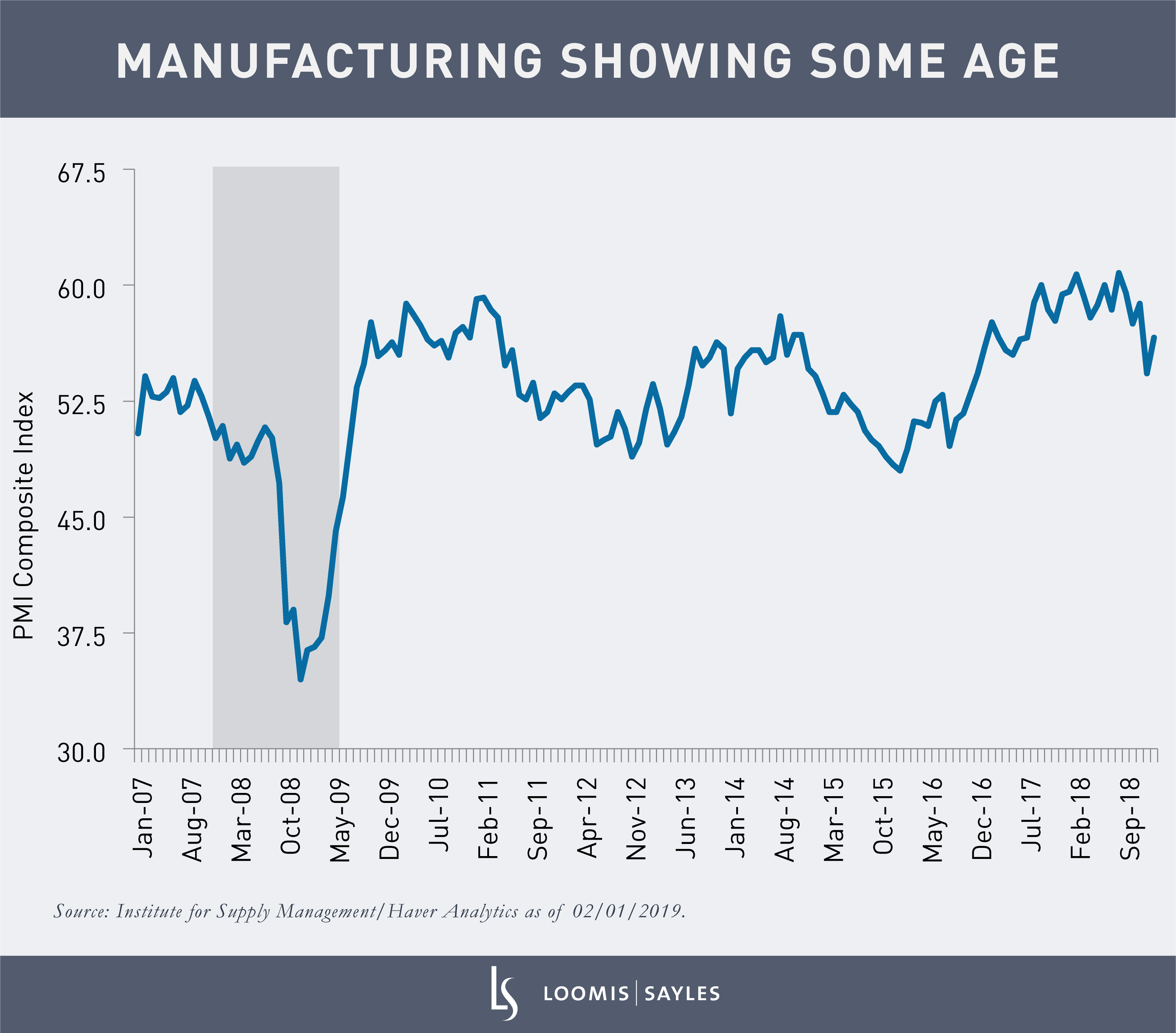

The ISM’s1 US manufacturing surveys are widely recognized gauges of economic health. They’ve taken us on a ride in recent months.

It started in December, when the Manufacturing Index fell a large 4.5 percentage points to 54.3. The drop coincided with a volatile month in the markets and seemed to confirm fears about slower growth.

Then January brought good news. The index reading was solidly expansionary, rebounding to 56.6. Market consensus had expected a further decline, so the surprise gain was welcome.

But January also brought bad news. Despite the bounce, the January reading was the lowest in the past 17 months (except for December 2018). Manufacturing is showing some age. Fed rate hikes, oil price fluctuations, weakness in major trading partners, and protectionism have taken a toll. The month-long federal shutdown didn't help.

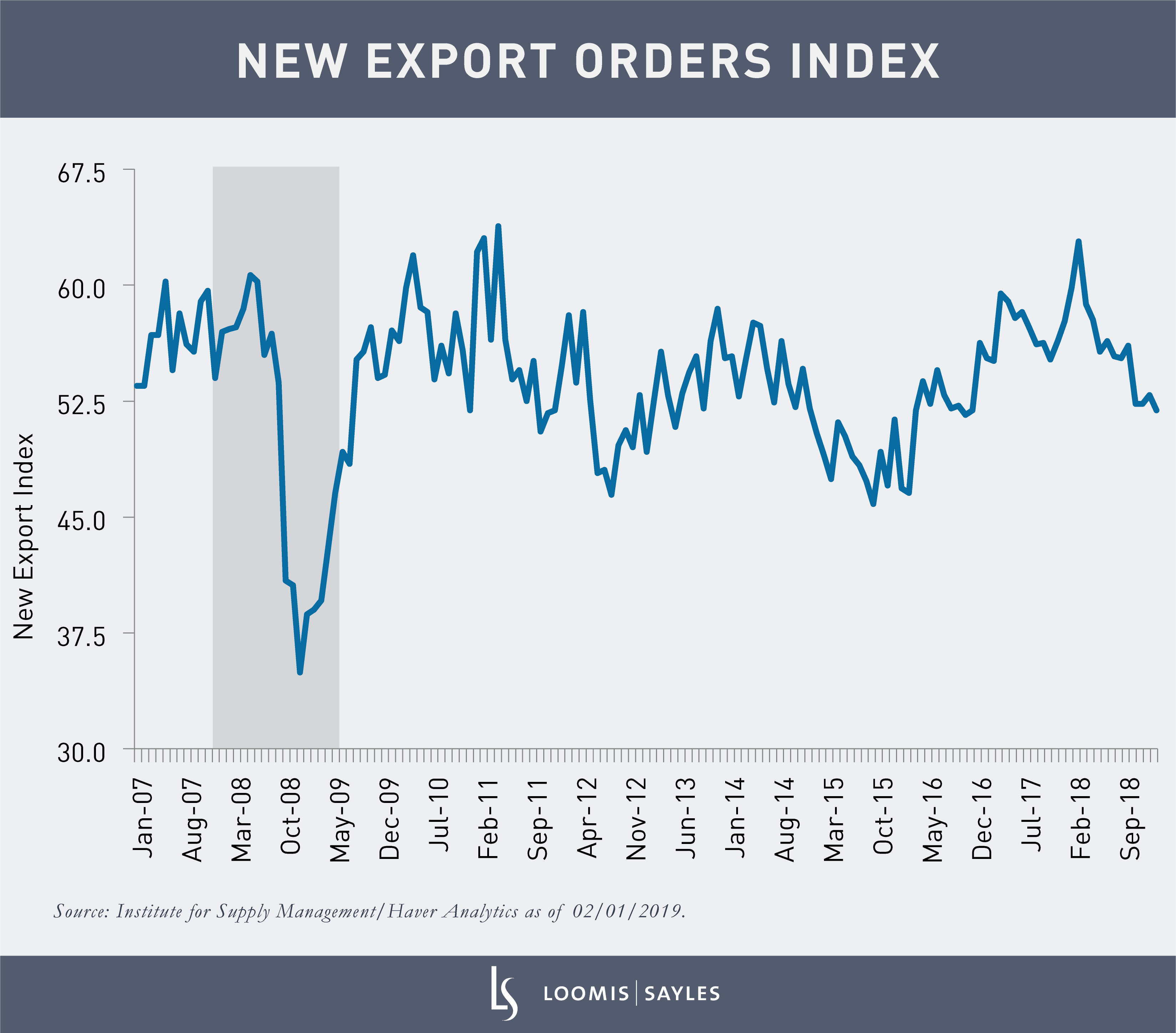

As for the ugly, that came courtesy of a separate index—the New Export Orders Index. It worries me that New Export Orders fell from 52.8 to 51.9 in January, a two-year low and just barely expansionary. It is no news that major trading partners are shaky, and the US dollar is relatively strong. Exports got hit.

It would help a lot if the US weren't doing so much of the heavy lifting in keeping the world economy afloat. It is hard to be optimistic about the trade deficit.

MALR023105

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

1 Institute for Supply Management