Asian Credit: High Yield Anticipated to Offer Attractive Opportunities in 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFor the first time in five years, Asia’s U.S. dollar-denominated credit market as represented by the benchmark J.P. Morgan Asia Credit Index (JACI) registered a negative return (-0.77%) in 2018, with the high yield (HY) sub-index at -3.2%1. For most of the year, the market was under negative pressure from U.S. Federal Reserve tightening and the Chinese onshore deleveraging campaign. However, with government policies helping to offset negative pressure on fundamental factors, technicals turning more positive in 2019, and increasingly compelling valuations, we expect a stronger performance from Asian credit in 2019.

In terms of portfolio tilts, we have a preference for HY in spite of its historical higher volatility over investment grade (IG) since Asian HY valuations are more attractive, in our view. While Asian IG spreads widened in 2018, the upside is likely to be capped given that U.S. IG issuers are offering investors significant new issue concessions. On the other hand, given significant spread widening last year, Asian HY looks relatively attractive compared with U.S. HY and emerging market (EM) peers.

We believe that 2019 should provide interesting opportunities for active fixed income managers who can keep tabs of changing developments across sectors and take advantage of the robust issuance that we expect to come to market at potentially attractive levels. Despite our current preference for HY, we are selective in our exposure and believe that careful credit selection and active portfolio management are crucial to managing risks and seeking returns.

Market backdrop: Valuations, fundamentals and technicals looking more positive

Valuations. Asia’s underperformance in 2018 is anticipated to provide opportunity for credit investors this year, particularly compared with global credit alternatives in developed and emerging markets. Negative headlines on the U.S.-China trade conflict coupled with fading regional demand led to significant spread widening for the JACI in 2018 (+88 basis points (bps)) with the HY sub-index widening 244 bps. These movements have led to Asian credit underperforming not only the U.S., which enjoyed tailwinds from growth acceleration and tax cuts, but also similarly rated EM corporate credits. Following the sharp correction, the current spread level provides a higher carry which should help cushion further downside. The yield level is also compelling with the yield to worst (the lowest potential yield an investor could expect absent a default) for the JACI at 5.19% and the JACI HY corporate at 8.79%2.

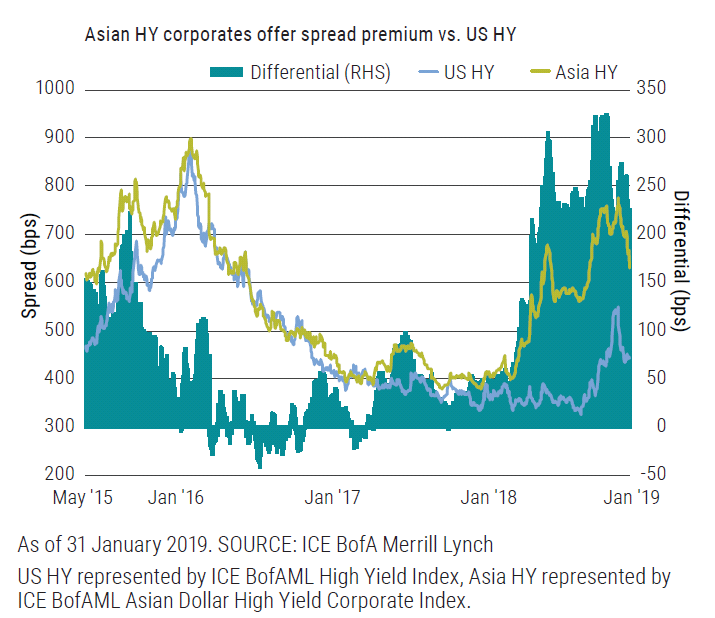

It is worth noting that the market has bounced back quite significantly in January and February this year, but given the extent of the spread widening in 2018, valuations still appear attractive on a relative basis (see chart).

Valuations for Asia high yield look attractive relative to U.S. high yield

Fundamentals. There are substantial differences across the universe of Asian credit with over 500 benchmark issuers across multiple sectors in 17 countries. We discussed some of the macro forces at play in our “Asia Market Outlook 2019,” but for investors in Asian credit there are two key themes. The first is the trade conflict between the U.S. and China. While there has not yet been any resolution, we are encouraged to see both sides engaging in constructive dialogue. More importantly, both central banks and policy makers have recognized the fragile situation. The U.S. Federal Reserve has signaled that it is going to be patient with monetary policy tightening in 2019, and Chinese authorities are engaging in monetary and fiscal easing to anchor economic growth. Both of these developments should be positive for Asian credit.

The second theme is the pause of China’s onshore deleveraging campaign, which put a strain on shadow banking and led to a meaningful contraction in 2018. With the escalation of trade conflict, demand for credit has naturally reduced in line with confidence as well. The latest policy has shifted toward growth stabilization, which should entail some degree of credit and fiscal easing by policymakers. We are encouraged that policymakers are also increasingly addressing the weak credit transmission affecting privately-owned companies (POEs) due to low appetite from banks for granting POE loans. Issuers in China’s industrial sector face a deteriorating trend in their financials with rising leverage. The government has announced policies such as corporate tax cuts, dedicated borrowing quotas for POEs and credit enhancement facilities that should help relieve the pressure. However, we expect the implementation will take time and the impact will likely not be felt until the second half of the year.

Technicals. While supply of credit in 2018 moderated from the record levels of 2017, it was still the second busiest year ever in terms of gross issuance. Net supply of HY credit from China was notably heavy given the reduction in the domestic credit market. For 2019, we expect a similar level of gross issuance but with heavier refinancing needs, although this will largely come from IG issuers and financials, which should create less market disruption. China’s onshore liquidity has materially improved with multiple deals reportedly over-subscribed despite lower yields. While the U.S. dollar offshore market will still be tapped by certain HY issuers who can access both channels, the supply pressure should be materially alleviated.

On the demand side, overall sentiment has turned more positive, with Chinese investors returning to the local market with new mandates to deploy. Chinese security houses and banks with asset allocation mandates are also actively engaging in primary market deals. Other market buyers include Asian private banks and regional real money funds, as well as bond investors with flexible global mandates. It appears that more attractive valuations have enticed these players to return and flows have turned positive for both regional funds and EM external fund categories.

Sector summary: Focus on careful credit selection is essential

Asset quality becoming a concern for Asian banks

As overall economic growth softens, asset quality is becoming an area of concern for Asia’s banks. We have already observed a significant deterioration in Indian banks’ asset quality and profitability. Although hefty credit losses related to bad debt are probably behind us, we expect credit growth to remain tepid due to capital constraints for India’s banks as well as companies’ limited borrowing appetite.

Elsewhere in the region, we expect credit costs to increase gradually but believe banks are generally well capitalized to withstand a more adverse operating environment. However, as part of China’s upcoming policy easing, the approximately USD 250 billion profit in the Chinese banking system will be one of the resources the government can mobilize to buffer economic growth. Banks may be required to lower their lending rates to small and medium-sized companies to stabilize urban employment and keep stressed companies afloat. They may also be asked to issue credit risk mitigation warrants for troubled private enterprises to refinance their bonds and there is a reasonable probability that they will lower retail mortgage rates. As a result, it is likely that banks will see a year-on-year decline in pre-provision earnings in 2019.

With the increase in capital use, Chinese banks, particularly those that are not considered global systemic important banks (G-SIBs), have been behind schedule in replenishing their capital ratios to comply with the G20’s agenda on total loss-absorbing capacity (TLAC) for its G-SIB banks by 2025. In fact, we estimate that there will be a circa USD 350 billion capital shortfall, which will provide a significant overhang to market supply across both onshore and offshore markets.

Attractive opportunities in Chinese property for HY bond investors

In our view, HY bonds issued by certain large cap Chinese property developers look attractive going into 2019. We expect a hard landing can be avoided in the broader China property market. In the face of tight policy control, the physical market remained resilient for most of 2018 although sales growth slipped into negative territory in the fourth quarter. Further slippage, to the tune of 5%-10%, may transpire in 2019 but in light of external trade pressures, the government will likely seek to stimulate the economy by boosting consumption and relaxing property market measures. Potential policy levers include easing credit conditions for developers, relaxing the price cap, partial relaxation of home purchase restrictions, lower mortgage rates, and better availability of mortgage loan quotas. In recent months, we have witnessed emerging signs of gradual relaxation at the local government level.

The other noteworthy trend that we have witnessed over the past few years has been accelerating sector consolidation. The country’s top 10 property developers increased their market share from a mere 5.4% in 2006 to close to 30% by 2018. Large developers enjoy significantly better access to a broad range of funding channels at lower costs, as well as being beneficiaries of government easing measures. As a result, our focus is on these industry consolidators who have begun to embark on deleveraging in recent quarters.

Valuations remain quite attractive with BB and B rated Chinese property bonds wider by around 200 bps and 240 bps, respectively, from year-end 2017 levels and currently yield around 7.3% and 9.3% (source: JP Morgan research). With 2- and 3-year bonds being issued with a 7.5%–10% coupon, the carry cushion is attractive and should help support demand.

China’s local government financing vehicles continue to struggle

We believe 2019 will be another year where China’s local government financing vehicles (LGFVs) struggle with re-financing. Based on data and market research from WIND, one of China’s leading financial data providers, we estimate there are around CNY 1.5 trillion (USD 200 billion) in onshore LGFV bonds that will mature in 2019, excluding any short-term notes (<360 days) issued and maturing within 2019. In addition to maturing bonds, there are also around CNY 570 billion (USD 80 billion) in onshore LGFV bonds whose options will become puttable in 2019. In 2019, the total value of maturing and puttable LGFV onshore bonds is roughly 2% of China’s GDP, or about a third of total maturing and puttable non-financial onshore corporate bonds. About half of puttable LGFV bonds are issued by HY entities.

We expect onshore re-financing pressure to push more LGFVs into tapping the offshore U.S. dollar market in 2019, adding to the approximately USD 10 billion of maturing U.S. dollar-dominated LGFV bonds that will require re-financing. Market expectations for defaults of maturing provincial- and key municipality-level LGFV U.S. dollar bonds are low given the policy support, but with the lack of transparency and weak standalone credit profile, we are cautious. In the event that direct offshore funding is not available, the National Development and Reform Commission (NDRC) has implemented fast track facilities for LGFVs to convert their onshore yuan (CNY) to foreign currencies. Having said that, we remain cautious on LGFV bonds issued out of lower tier cities, particularly those from the weaker provinces with high LGFV debt.

Weaker sentiment providing a headwind for growth in consumer companies

Consumer sentiment in China weakened in the second half of 2018, with negative year-on-year growth in automobile sales. Internet/consumer companies revised down their financial year 2018 revenue forecasts and remain cautious about 2019 growth prospects. While China’s “consumption upgrade” remains a secular trend, near-term growth depends on government stimulus and the resuscitation of consumer confidence. While tax cuts – a key feature in the fiscal easing so far – are supportive of consumption and corporate margins, first half earnings this year will be under pressure compared with the strength seen in the same period last year. We prefer market leading companies with high barriers to entry, secular growth potential and strong balance sheets, while maintaining an underweight in second- and third-tier names. While in general we favor internet companies, uncertainty surrounding regulatory risks remains high and can generate volatility.

Asia’s technology sector will be overshadowed by U.S.-China tensions over intellectual property protection in 2019. Weak orders from companies such as Apple will also weigh on the Asian semiconductor supply chain as growth from other smartphone producers might not be able to fully offset this. Long-term demand remains positive, however, since devices are getting more sophisticated and will require more silicon components produced in this region. We remain constructive on those companies that demonstrate visible growth opportunities and pricing power.

While certain Asian regions are expected to deploy 5G in 2019, it has not resulted in significant capex increases at the telecom operators as the initial rollout will be limited in scale and focus on urban areas only. Data growth continues to be the revenue driver in the region while smartphone penetration is increasing. We expect stable cash flow and leverage for major Asian telecom companies, except for India where the price war will continue to put pressure on Indian operators amid market consolidation.

Asia’s oil and gas sector should be resilient

The sector is dominated by state-owned companies, which have become much more disciplined in terms of cost control and capex spending since the previous oil price downturn. They are now more resilient to adverse oil price shocks and are better positioned to capitalize on higher oil prices. Fuel subsidies, by and large, have been eliminated in the region in recent years, which is a positive development for the sector. Nonetheless, a potential sharp spike in oil prices or significant depreciation in local currencies may lead to a return of these inefficient subsidy mechanisms.

Weaker outlook for metals & mining sector in H2 2019

Having ridden the 2015-2017 cyclical recovery, many credit issuers in the HY cohort in this sector have repaired their balance sheets as far as they are likely to. In the last year, some have started refocusing on growth opportunities. At the same time, following a wave of supply side policies from Chinese authorities, supply discipline for many commodities is getting looser, while the demand outlook is looking precarious at this late stage of the economic cycle.

We could see Chinese stimulus in the first half of the year to combat the economic slowdown, which may prolong demand for bulk commodities like iron ore and steel (geared towards China’s construction activity). However, a softening of the property market will reduce demand and suggest a weaker outlook for some commodities in the second half. Base metals, geared more towards late-stage construction and consumer products, will also be heavily influenced by economic conditions. We see less room for credit upgrades in the sector in 2019, and the risk/reward is therefore skewed to the downside, in our opinion, given the economic backdrop.

Diversity within the utilities sector providing opportunities

The utilities sector has become more diverse with the arrival of renewable power issuers in the HY cohort, providing diversification for investors used to seeing largely quasi-sovereign, strong investment grade players within this sector. However, risks are high given that in recent years, many bond issuers in this space are producing power at costs higher than more recently built renewable power plants and are reliant on government subsidies. Downside risks include a renegotiation of tariffs or power supply agreements, as we are seeing in India, or the current continued delays in government subsidies for renewable operators in China. In addition, some operators have underperformed on overly optimistic forecasts of wind/solar sources. As a result, we are very selective when investing in this sector. For example, despite the number of renewable bonds in China trading at double-digit yields due to liquidity risk, we remain cautious until there is more clarity on how the government will continue to fund the renewable subsidies, and see this sector as largely a high beta trade for now.

We have a favorable view on Chinese downstream gas distributors over the secular horizon. As part of its national clean energy strategy, the Chinese government is promoting natural gas consumption and has set a target for it to reach 10% of total primary energy consumption in 2020 and 15% in 2030, up from 7% in 2017. This implies double-digit annual volume growth in the next several years. Total gas consumption in China grew by 18.1% year-on-year in 2018 according to the NDRC, and we expect the positive momentum to continue in 2019. Leading gas distributors continue to outperform the industry and credit metrics remain strong with solid free cash flow.

Positive outlook for transport and infrastructure sectors

Asian transport infrastructure operators such as airports, toll roads and container ports are benefiting from increasing passenger traffic. Per capita transport service consumption remains low in emerging Asia and has ample room to grow. This is a defensive sector for bond investors with stable and recurring cash flow, decent hard asset coverage and oftentimes solid sovereign support. As the regulatory environment continues to evolve in many Asian markets, we prefer issuers in stable regulatory environments with transparent tariff-setting mechanisms.

We expect Chinese infrastructure construction and machinery companies to benefit from increasing government spending in 2019. Since the second half of 2018, the Chinese government has initiated a more proactive fiscal policy to support infrastructure projects to stabilize the economy, with a focus on transport infrastructures such as railways, metros and airports. Recently, the NDRC has accelerated approvals with over CNY 1.2 trillion in transportation infrastructure projects signed off since December 2018. Leading infrastructure contractors are the key beneficiaries in terms of revenue growth and cash flow over the cyclical horizon. We also hold a positive view towards construction machinery manufacturers given the higher infrastructure spending and healthy machinery replacement demand.

Credit spreads attractive, but careful credit selection required

Asia’s underperformance in 2018 is anticipated to provide opportunity for credit investors this year, particularly compared with global credit alternatives in developed and emerging markets. We favor Asian HY, in spite of its historical higher volatility, over investment grade credits since valuations are more attractive, particularly compared with U.S. HY and emerging market peers.

Despite this preference for HY, we are selective in our exposure and believe that careful credit selection and active portfolio management are crucial to manage the myriad risks and seek returns in this sector. One of the key risks that we recognize is the transmission problem in Asian HY whereby weaker issuers may be starved of credit in spite of abundant inter-bank liquidity. If government policy isn’t initiated to address this, we could see continued Chinese onshore defaults leading to a loss of market confidence and contagion creeping into offshore issues.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

References to specific issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold securities of those issuers. PIMCO products and strategies may or may not include the securities of the issuers referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

The ICE BofAML Asian Dollar High Yield Corporate Index tracks the performance of sub-investment grade US dollar denominated securities issued by Asian corporate issuers in the US domestic and eurobond markets. The ICE BofAML US High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the US domestic market. The JPMorgan Asia Credit Index (JACI) tracks total return performance of the Asia fixed-rate dollar bond market. JACI is a market cap-weighted index comprising sovereign, quasi-sovereign and corporate bonds and it is partitioned by country, sector and credit rating. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All