Doomed to Repeat the Tech Bubble?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe recently received an email inviting us to a webinar titled How to Position Portfolios for the “New Economy”. Anyone who lived through the late-1990s Tech Bubble is probably now cringing. It’s hard to believe that the Tech Bubble burst 19 years ago (NASDAQ’s bubble- related peak was March 2000), but George Santayana’s famous quotation unfortunately seems to sum up the current environment, “Those who do not learn history are doomed to repeat it.”

The basic principles of economics and finance don’t have a subparagraph saying, “this holds for every industry except for Technology.” Our bearish views on Technology in the late-1990s were based on the simple fact that return on capital is highest when capital is scarce. A mad rush to invest in anything (tulips, gold rush, technology stocks, housing, etc.) means that the longer-term investment returns will likely be subpar. The associated innovations may come to fruition, but investors should only care about their return on investment. The spread of the internet since the Tech Bubble has clearly had a major positive impact on the global economy, but many of the bubble’s hot stocks no longer exist.

Technology is cyclical

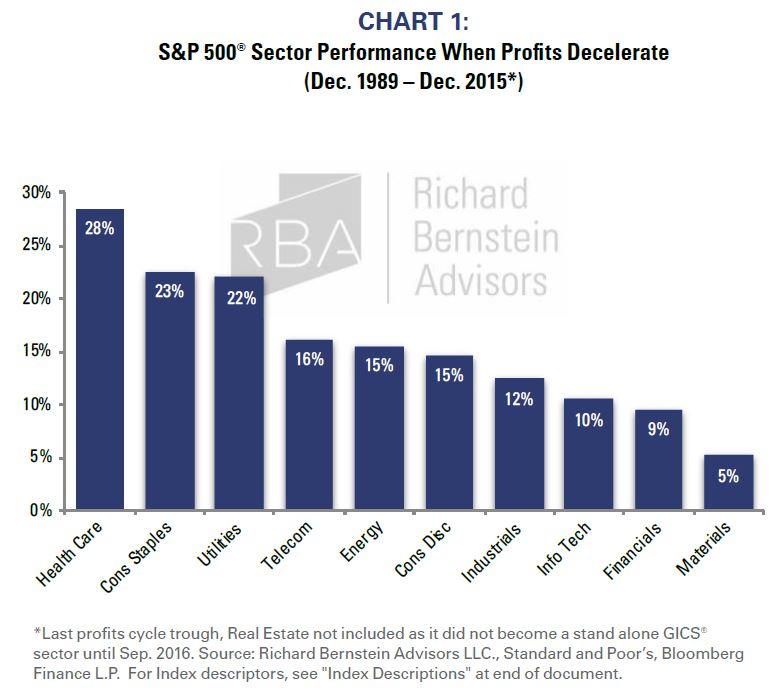

We significantly lowered our exposure to technology at the beginning of the year (from roughly 26% to about 11%) because Technology has historically been among the most cyclical sectors, and tends to underperform when profits cycles decelerate. Our forecast is that the S&P 500® GAAP profits growth will slow from roughly 23% in 2018 to 0-5% in 2019. If that forecast proves correct, then Technology has a high probability of underperforming.

Chart 1 shows the performance of S&P 500® sectors when profits decelerate. Technology is the third worst performing sector. Most investors know that technology stocks are high-beta stocks, and that they tend to be more volatile than is the overall market. However, investors seem to forget that beta is generally symmetric. In other words, the sector is sensitive to both the upside and the downside.

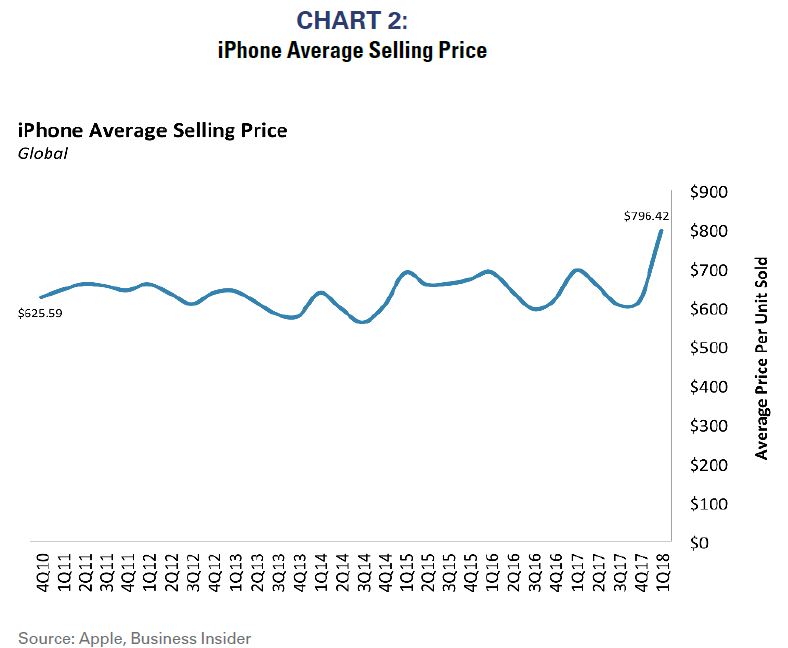

The inherent business of some technology companies may be more cyclical than analysts forecast. For example, Chart 2 shows the average selling price of an iPhone in the US. The current price of the 2018 models, roughly $750-$1,000, is higher than the average selling price of a dishwasher and comparable to washer/dryer combinations. Appliances are considered durable goods, and consumers don’t mind paying higher prices because they mentally amortize the cost over the appliance’s anticipated 15-20 year lifespan. Mobile phones rarely have a lifespan of even 5 years, but consumers are expected to pay durable goods prices for a non-durable good. Such odd economics might work when employment is strengthening (as it has been during the majority of the time period shown), but seem unlikely to work should employment cyclically weaken at some point.

Capital is flowing. Confidence is building

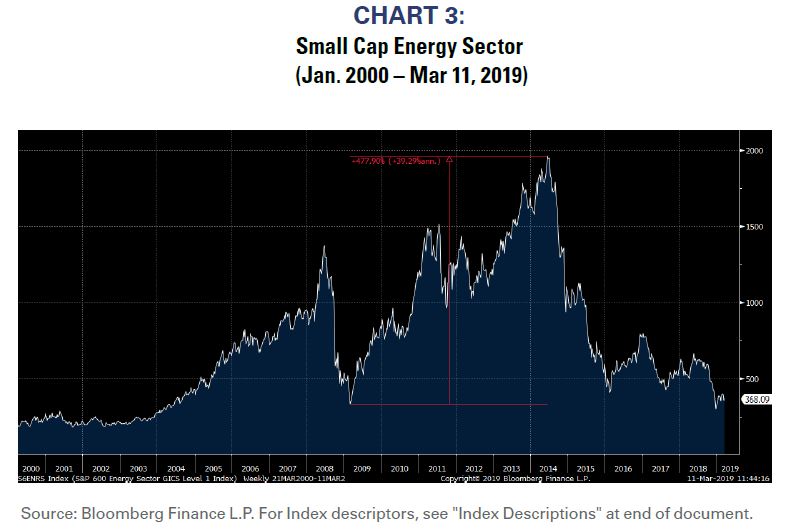

Regardless of the sector involved, investors tend to primarily focus on momentum toward the end of a cycle and ignore the simple principle that returns are highest when capital is scarce. For example, Chart 3 shows the performance of the S&P 600 SmallCap® Energy Sector. The sector appreciated nearly five-fold from 2009 to 2014, the last two years of which were a classic momentum period when stock performance and capital flows significantly outpaced fundamentals. It wasn’t only investors who acted imprudently during the momentum period. The availability of cheap capital led energy companies to build inventories, increasendebt, and expand capacity, which added tremendous operating and financial leverage to the businesses. As the cycle began to turn down, the added operating and financial leverage accelerated and exacerbated the downturn.

Technology is again the “new new thing” sector (credit to Michael Lewis), and capital is freely flowing to technology stocks and venture capital. There appears to be an insatiable demand for investing in “unicorns”, “disruptors”, or artificial intelligence, and every investor believes they’ve found the one manager who has unique investment insight. There should be no doubt that AI and the like will dramatically change the economy over the next decade, but investors should care only about expected returns, which tend to fall as allocated capital increases.

The lunacy of some investment ideas seems obvious if one ignores the hype. In 1999, it seemed blatantly obvious that investment priorities were misguided, and we pointed out that investors thought “buying a green pepper on the internet is technology, but building a fighter plane isn’t”. Consider for a second that today there are several companies competing to fly to Mars each funded by speculative capital flows. Yet, here on boring Earth, one can’t get to Penn Station on time during the morning commute.

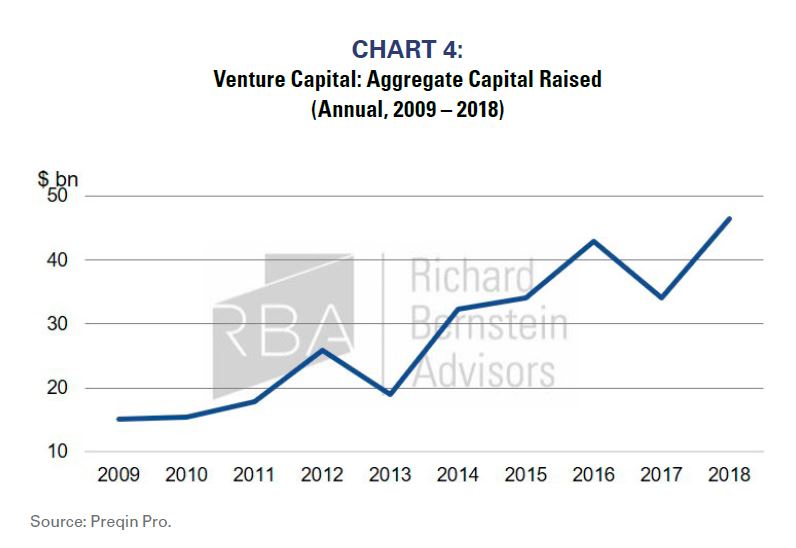

Chart 4 shows the annual flows to venture capital funds. Capital allocated to venture funds has basically tripled since the beginning of the bull market. Simple supply and demand of capital suggests expected returns and allocations to the asset class should be going down, not up.

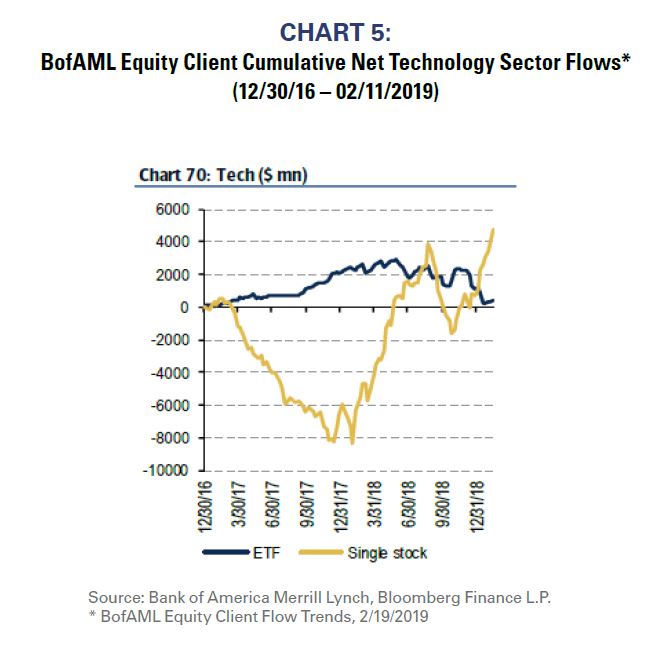

Chart 5 shows that individual investors are investing in individual technology stocks rather than in ETFs. Investor confidence is so strong that individuals apparently believe their stock-picking skills are superior and that diversification is unnecessary. It’s ironic that active management is under pressure yet individuals have increasing confidence in their own abilities to pick technology stocks.

No bubble-like returns, but getting close

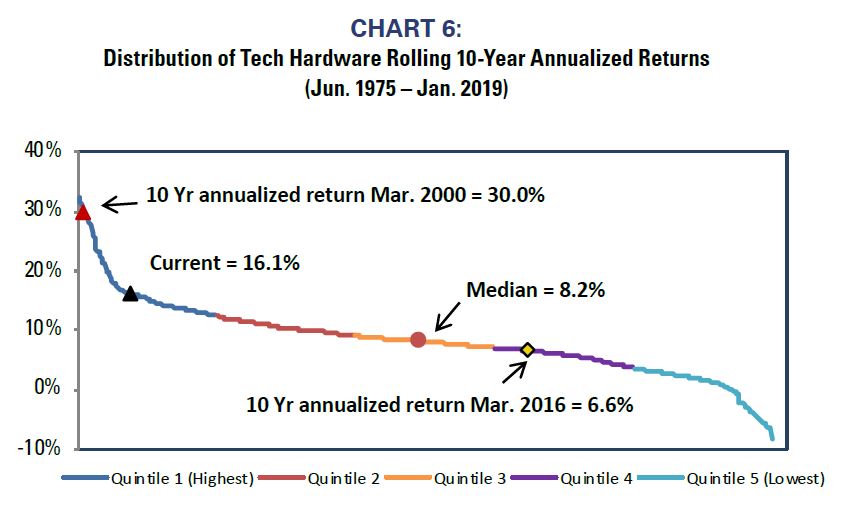

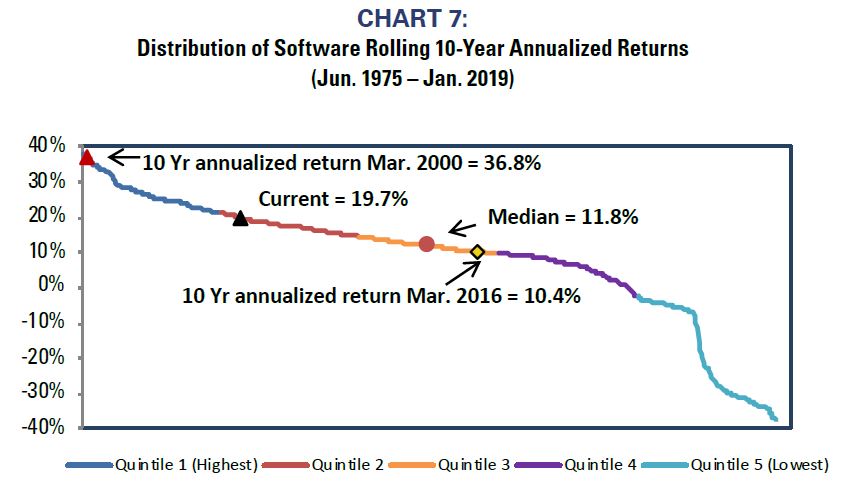

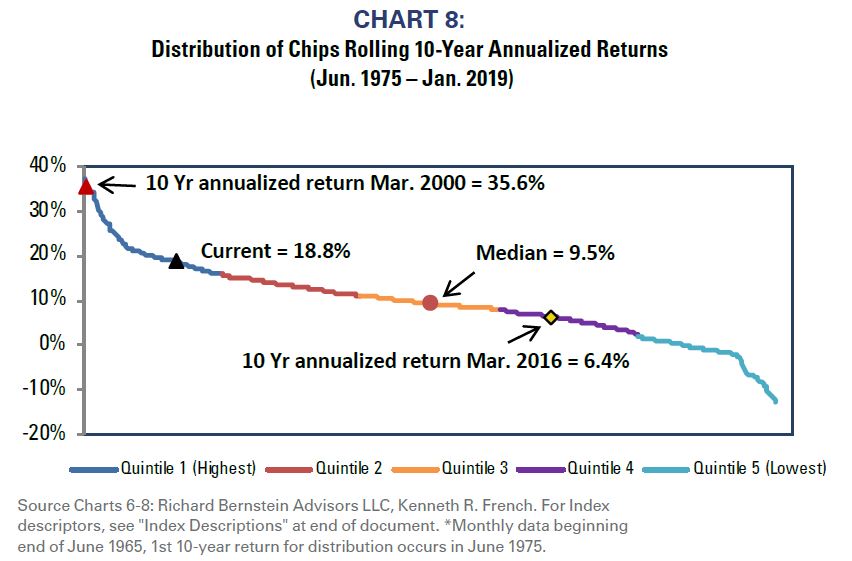

Charts 6-8 show the distribution of 10-year returns since 1975* for Hardware, Software, and Chips. We added significantly to our Technology holdings in the first quarter of 2016 because we forecasted overall corporate profits would significantly accelerate and, as noted earlier, Technology is a highly cyclical sector. 10-year historical returns at that time for the sector were below median.

Today, 10-year returns for Technology are starting to seem extreme. Returns are not as extreme as were those at the end of the Tech Bubble, but both Hardware’s and Chips’ 10-year returns are now in the highest quintile of historical returns and Software’s is in the second highest. It’s apparent that investors initiating technology investments today are doing so more toward the end of a normal return cycle than toward the beginning.

Doomed to repeat the past?

We significantly lightened our Technology exposure early in 2019 because Technology has historically been a cyclical sector and profits look poised to decelerate. In addition, strong late-cycle capital flows to Technology and venture capital may be suggesting that investors’ expected returns are too high for the sector.

The Tech Bubble deflated 19 years ago this month, but it increasingly appears that investors did not learn from that episode. We feel our reduced positions in Technology are very appropriate.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

S&P 600 SmallCap® Energy Sector: The S&P 600 SmallCap® Energy Index is an unmanaged, capitalization-weighted index designed to measure the performance of Small Capitalization companies in the Energy sector.

S&P 500® Sectors: The S&P 500 ® Sector references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

Technology Industries: Hardware, Software and Chips are represented by the Fama French 49 Industry Series as described below.

Hardware – Computers is comprised of companies in the CRSP database from the following sub-industries: Office computers, Computers, Computers – mini, Computers – mainframe, Computers – terminals, Computers – disk & tape drives, Computers – optical scanners, Computers – graphics, Computers – office automation systems, Computers – peripherals, Computers – equipment, Magnetic and optical recording media.

Software – Computer Software is comprised of companies in the CRSP database from the following sub-industries: Services – information retrieval services, Computer integrated systems design.

Chips – Electronic Equipment is comprised of companies in the CRSP database from the following sub-industries: Industrial controls, Telephone and telegraph apparatus, Communications equipment, Radio TV comm equip & apparatus, Search, navigation, guidance systems, Training equipment & simulators, Alarm & signaling products, Communication equipment, Electronic components, Search, detection, navigation, guidance.

About Richard Bernstein Advisors

Richard Bernstein Advisors LLC is an investment manager. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $9.1 billion collectively under management and advisement as of February 28th, 2019. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund, the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and also offers income and unique theme‐ oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial Renaissance® ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS, Merrill Lynch, Morgan Stanley Smith Barney and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.

© Copyright 2019 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

RBA Investment Process:

â Quantitative indicators and macro-economic analysis are used to establish views on major secular and cyclical trends in the market.

â Investment themes focus on disparities between fundamentals and sentiment.

â Market mis-pricings are identified relative to changes in the global economy, geopolitics and corporate profits.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided "as is" without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All