Green Shoots for the Global Economy

Membership required

Membership is now required to use this feature. To learn more:

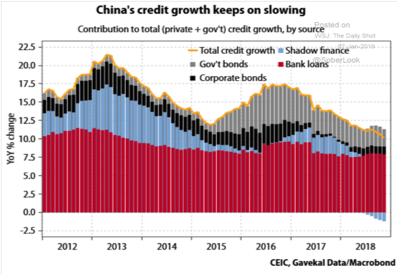

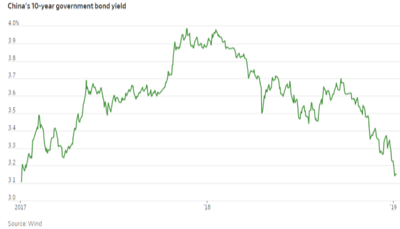

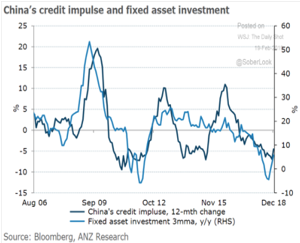

View Membership BenefitsWhat happens in China clearly does not stay in China so the outlook for China’s growth in 2019 is one of the keys to how the global economy will perform and how financial markets will respond to that level of growth. As discussed last month after the 19 Party Congress meeting in October 2017, China clamped down on the shadow banking system with a series of regulatory changes after a period of unchecked growth. The growth of the shadow banking system had soared from $1.5 trillion at the end of 2012 to more than $9 trillion at the end of 2016, fueled by Asset Management Products, Entrusted Loans, and Peer-to-Peer lending. In the short run the contraction in the shadow banking system caused the rate of change in Total Credit growth to slow. The reduction of credit growth through the shadow banking system during 2018 contributed to a slowdown in corporate loan growth, offset the growth in bank lending, and an economic slowdown especially in Q4. The success in curbing the shadow banking system provided policy makers the flexibility to loosen monetary policy through traditional measures. The Peoples Bank of China (PBOC) has significantly lowered the Required Reserve Ratio for large and small banks by 2.0% since October after announcing the fifth reduction in the past year. The reductions in the past year from 17.5% to 13.5% represent a drop of 22.8% almost twice as large as the easing in 2014 and 2015. In response to the PBOC’s easing, the yield on China’s 10-year bond has fallen from 3.70% in late September to 3.18% at the end of February.

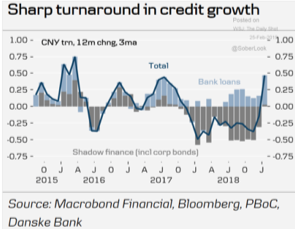

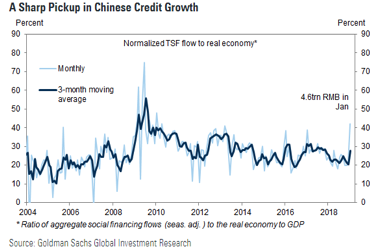

The expectation has been that the Chinese economy should begin to show the effects of the PBOC’s aggressive easing, if my expectation of a firming in the Chinese economy was to take hold by mid-year. Since it normally takes from 6 to 12 months for monetary policy changes to gain traction, filter through an economy, and begin to materialize in economic reports, it is important that confirmation of this outlook materialize. One initial sign would be that the additional liquidity freed up by the reductions in the Required Reserve Ratio is flowing out of the banking system and into the economy through increasing credit growth. Bank lending increased significantly in January which boosted the 12 month rate of change. The increased level of regulation after the 19 Party Congress meeting in October 2017 of the shadow banking system is clearly evident (grey shaded bars) and into the end of 2018. It appears that regulators eased up in late 2018 as the 12 month rate of change in the shadow banking system was far less negative. The January improvement in Total Social Financing is the largest increase since the PBOC’s response after the 2008 financial crisis. The easing of monetary policy and increased flow of credit has led to an upward reversal in fixed asset investment and, if continued, would help stabilize China’s economy in the short run and lead to a firming as 2019 unfolds.

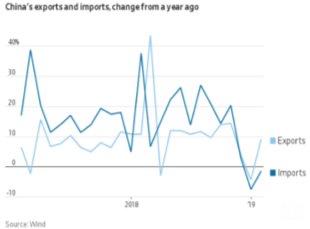

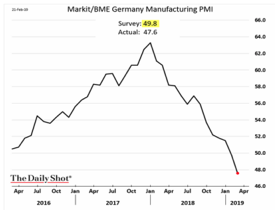

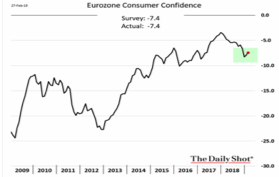

These “Green Shoots” would greatly allay fears about the global economy if further improvement develops in comings months as I expect. In January exports and imports rebounded which is another good sign for the global economy if maintained. In the primary 19 countries within the European Union, exports represented 47.4% of GDP in 2018 up from 45.7% in 2016. The largest customer for E.U. goods and services is China, which is why any improvement in China’s economy will provide a lift to the E.U. and especially Germany. This positive domino effect is why China is one of the keys to 2019. The slowdown in China and the subsequent drop in demand for German goods is one of the main reasons why manufacturing in German tumbled so much during 2018 and into the first quarter of 2019. It is important to note the service sector in Germany remains strong and why the German economy is expected to stabilize and show improvement if China firms by mid-year as expected. The German economy represents 30% of the E.U.’s GDP so any improvement in Germany will help GDP growth throughout the E.U. Consumer confidence has dipped in the E.U., but remains at a historically healthy level and did experience an uptick in January.

U.S Economy

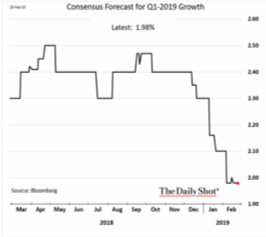

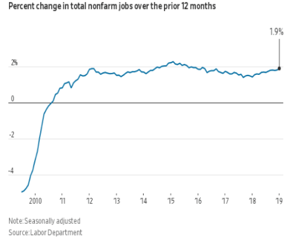

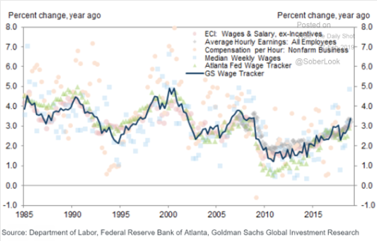

The U.S. economy was expected to slow in the first quarter but not as much as some forecasts with Q1 now below 1.0%. Due to the change in quarterly seasonality weighting by the Bureau of Economic Analysis (BEA) announced in July 2018, first quarter GDP will be adjusted upward by 0.5% compared to prior first quarters. Not sure this change by the BEA is widely known so it could provide a surprise. The consumer is in good shape as job growth remains unusually strong at this point in a business cycle, wages are rising and headed higher, and the rally in the stock market has bolstered Consumer Confidence.

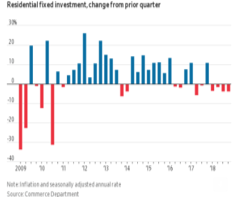

Housing has subtracted from GDP in the past two years but may subtract less or modestly add to GDP in 2019. Mortgage rates have come down as have home prices in some markets, which has improved affordability. Millennials have finally started to buy homes, which is a big shift in the trend during this recovery. The homeownership rate among households headed by someone who is 35 to 44 years old increased to 61.1% in the fourth quarter from 58.9% a year earlier, according to the Census Bureau. The rate for households with an owner under 35 years old rose to 36.5% from 36% in the same period. As long as mortgage rates remain steady and wage growth continues, this trend in millennial home buying should persist.

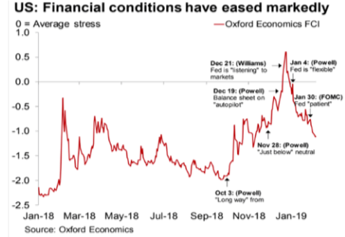

Financial conditions tightened abruptly in the fourth quarter as the spread between Treasury bonds and corporate bonds widened, the S&P 500 fell, and the Dollar rose. Importantly, financial conditions have improved since late December and reversed most of the tightening. They are back to where they were in the first half of 2018 which should help stabilize GDP growth in coming months. If the China trade negotiations produce a deal, business investment could pick up nicely in the U.S. and globally. In the second half of 2018 business investment growth slowed so it has the potential to add to GDP growth especially in the second half of 2019.

During the second half of 2017 and into the first quarter of 2018 global growth was widespread across all 34 countries followed by the Organization for Economic Cooperation and Development (OECD). This synchronized growth began to unwind in the spring of 2018, as first discussed in the May 2018 Macro Tides and morphed into Synchronized Slowing Growth as reviewed in the August Macro Tides. The expectation is that global growth has begun the process of bottoming and should exhibit signs of firming by mid-year. The wild cards are the U.S. trade negotiations with China and the European Union. Expectations for genuine progress have been raised regarding China reinforced by the delay in the implementation of additional tariffs scheduled for March 2. Financial markets would react negatively if any speed bumps develop with China in the next 60 days. Lurking in the shadows and receiving scant attention are the potential tariffs on auto and auto parts imports from the E.U. The Commerce Department provided its recommendations to President Trump on February 17 and he has 90 days to make his decision. The U.S. has long wanted the E.U. to open up its agricultural markets to U.S. farmers and has consistently been rebuffed. If the U.S. and China trade negotiations are resolved before May 17, an emboldened President Trump may threaten playing hard ball with the E.U. If the S&P 500 is above 2800 or at new highs, the President may feel he would be playing with house money and be further inclined to pressure the E.U. The global economy has slowed so it is more vulnerable to unexpected shocks than when synchronized growth was in high gear. This risk may not register with President Trump, who is far more focused on Making America Great Again.

Federal Reserve

The Federal Reserve will leave its policy rate unchanged at the March 20 meeting but may finalize details of the unwinding of its balance sheet. In testimony before Congressional committees on February 26 and 27 Chair Powell indicated the Fed will likely terminate the shrinking of its balance sheet with its balance sheet near $3.5 trillion, by the end of 2019 or shortly thereafter. This ‘news’ shouldn’t surprise anyone. Then again the markets were positively shocked when the FOMC included the word patient in its post meeting statement on January 30, after at least 5 FOMC members had given speeches during January extolling the virtues of the Fed being patient, including Chair Powell, Vice-Chair Clarida, and the most hawkish member Esther George.

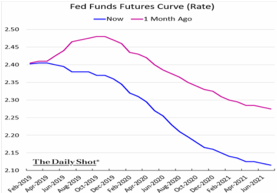

The one piece of information that could rattle the markets is the Fed’s dot plot. At the December 2018 meeting the dot plot indicated that the Fed would increase rates 2 times in 2019, rather than the 3 times it had projected at the September meeting. Currently, the markets are actually tilting slightly toward the Fed cutting rates before the end of 2019. The markets might be shaken if the dot plot reaffirms the outlook for 2 hikes in 2019, even if the Fed emphasizes it will remain patient as long as inflation is muted. In a speech on February 24 Vice-Chair Clarida highlighted why the global economy was a focus of the Fed. “The reality is that the global economy is slowing. You’ve got negative growth in Italy, Germany may just grow 1% this year, and a slowdown in China. On balance, that makes the global economy more fragile. These are all things that we need to factor in.” However, the leash on patience could be shortened if the global economy does show signs of improvement lowering concerns about the global economy.

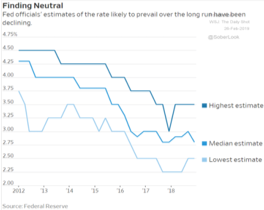

The number of forecasts suggesting the federal funds rate has peaked for this business cycle indicates that a good number of economists and investors are overlooking two longer term factors that are still in play. The Federal Reserve wants to get the federal funds rate up to a level that is neutral and no longer provides stimulus. Based on estimates by members of the FOMC in December, the neutral level for the federal funds rate ranged from 2.5% to 3.5% with a median of 2.8%. The median is 0.40% above the recent average of 2.40%, which implies more than one increase in the funds rate. The Fed pegs the long term non-inflationary growth rate for the U.S. economy at 1.8%. As the recovery enters into its 10th year, any growth above 1.8% is viewed by many FOMC members as inflationary however muted it may be. The faith in the Phillips Curve has diminished within the FOMC, but it hasn’t evaporated. If the global economy gathers its sea legs in the second half of 2019 and inflation pressure in the U.S. drifts upward, some members of the FOMC may begin discussing the need to push the federal funds rate above the neutral level. The FOMC would prefer if the cyclical peak in the federal funds rate were higher than 2.40%, since it will provide more ammunition to offset the next recession. This discussion does not take away from the fact that the Fed is data dependent and will only temper its patience if the data points the way. Most market participants believe the Fed’s next move is to lower rates with the only question being when. Markets react most strongly when expectations are proven wrong and no one would be surprised if there are no rate changes in 2019. But the prospect of an increase - Booo!

Inflation Targeting

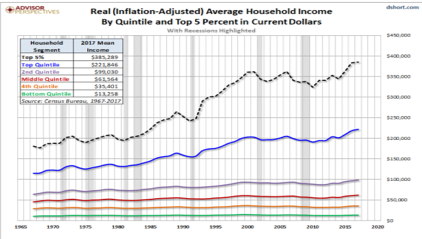

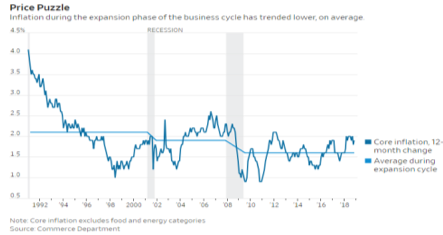

In 2012, the Federal Reserve publicly and formally declared for the first that it was pursuing an inflation target of 2.0%. As I have discussed previously, I have a problem with the Fed’s 2.0% inflation goal. If inflation averages 2.0% during the next 72 years the cost of living will quadruple. (rule of 72 = 72 years/ 2% = 36 years for money to double and quadruple in 72 years) The average lifespan is 78 – 80 years so a quadrupling of prices doesn’t sound that stable. With the cost of living rising that much, the odds are high that the purchasing power of most workers will not keep up, which means living standards fall. If inflation averaged 1.0% and wages grew 1.5%, the standard of living for most workers would rise, which seems like a better outcome than the Fed hitting a subjective inflation target. As the chart nearby clearly illustrates, the bottom 60% of workers in the U.S. have not experienced significant growth in inflation adjusted wages during the past 50 years. (Chart compliments of Doug Short, Advisor Perspectives) Fed policy has arguably contributed to the problem of income and wealth inequality, especially after the financial crisis when the Fed explicitly pursued Quantitative Easing with the express purpose of lifting the stock market. Rather than questioning the efficacy of its 2.0% inflation goal, the Federal Reserve is potentially doubling down.

St. Louis Fed President James Bullard believes that the Fed’s explicit target helps anchor inflation by influencing inflation expectations. “Modern economic theory says that inflation expectations are an important determinant of actual inflation.” If the Fed says it wants inflation at 2%, expectations can help get it there. “Firms and households take into account the expected rate of inflation when making economic decisions, such as wage contract negotiations or firms’ pricing decisions. All of these decisions, in turn, feed into the actual rate of increase in prices” according to Bullard. Firms and households have clearly not gotten the email explaining their role in setting expectations, since the average of core inflation in the past three expansions has dropped from 2.1% to 1.6%.

Although the core rate of inflation has moved modestly above 2.0% during the strongest part of prior expansions, it has fallen well below 2.0% once the economy entered a recession. In an effort to get core inflation to average 2.0% over a complete business cycle, the Fed is floating the idea allowing core inflation to move a bit higher above 2.0% during the expansion phase of the business cycle so when it fall below 2.0% when the economy is in recession, the average for the entire business cycle will be 2.0%. This proposal shows how important the 2.0% target is to some FOMC members and their commitment to achieving it. As Vice-Chair Clarida recently put it, “Persistent inflation shortfalls carry the risk that longer-term inflation expectations become poorly anchored or become anchored below the stated goal.” The amount of hubris expressed in this statement is noteworthy and reflective of a Masters of the Universe mentality. How dare consumers and businesses not conform to our inflation goals! And if owners of Treasury bonds express their displeasure with the Fed’s ambitions of allowing inflation to rise somewhat above 2.0% by selling bonds, Vice-Chair Clarida had a ready answer for that too. The Fed would simply establish a “temporary ceiling for Treasury yields at longer maturities by standing ready to purchase them at a preannounced floor price.” This is what the Bank of Japan did in recent years when it announced it would only buy bounds if yields rose to 0.10%, and it worked. The Federal Reserve also executed this strategy during World War II to fund the war effort at a low cost. Every Fed governor in the past 30 years (including Powell) has warned during their annual Congressional testimony that government spending cannot be sustained above the rate of GDP growth. Knowing and accepting the lack of political will in either party, the Fed is setting the table to accommodate the demographic driven spendthrift government spending coming in the next decade.

Where America Is Heading

In the primary for New York’s 14th Congressional district on June 26, 2018, Alexandria Ocasio-Cortez defeated 10-term fellow Democrat Joe Crowley by garnering 15,897 votes to his 11,761 votes. It was an impressive victory for someone who had never run for public office and who was outspent by Crowley by $3.4 million to $194,000 or a ratio of $17.50 for each $1.00. In the November 6 general election Alexandra Ocasio-Cortez (or AOC as she is popularly known) ran against Anthony Pappas an Economic professor at St. Johns University who did not actively campaign. AOC’s campaign posters were designed to resemble those of Cesar Chavez and Dolores Huerta who were Latino labor activists in the 1960’s and cofounders of the United Farm Workers union. AOC is a member of the Democratic Socialists of America. The 15,897 votes she received in the June Democratic primary represents of .0000486% of the 327.16 million people living in America, but AOC aims to change the direction of the U.S. for decades to come.

On February 7, 2019 Representative Alexandra Ocasio-Cortez teamed with Senator Ed Market to introduce the ‘Green New Deal’, which was co-sponsored by 60 members of Congress and nine senators all members of the Democratic Party. By 2030 the Green New Deal (GND) calls for generating 100% of the U.S.'s power from renewable sources, making all buildings energy efficient, and eliminating carbon dioxide and other greenhouse gas emissions from the transportation sector and industry. To accomplish these goals the GND proposes massive investments (government spending) in research and development to make the U.S. a global leader in clean energy technology. In a little over a decade the GND proposes remaking the U.S. economy on such a large scale that it makes President Kennedy’s goal of putting a man on the moon within a decade seem like a walk in the park.

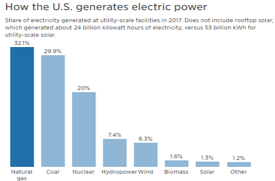

In 2017 renewable-energy sources like hydropower accounted for 7.4% of the U.S.'s electric power, followed by wind at 6.3%, with solar contributing just 1.3%. In total renewable-energy sources generated 17% of the U.S.'s electric power according to the U.S. Energy Information Administration. Although nuclear power plants only generated 20% of the U.S.'s electric power, nuclear power provided 63% of its zero-carbon power. It’s noteworthy that the GND does not intend to include nuclear power as part of the solution. One can assume that nuclear generated electricity isn’t ‘green’ enough, although it would lower carbon emissions and provide a constant source of electricity compared to the variability that is a given with wind and solar sources. The primary goal of the Green New Deal is to mobilize the nation's capital — its money, manpower and know-how — to advance clean tech and overhaul the American energy and transportation sectors. The goal is to drive carbon dioxide and other greenhouse-gas emissions to zero and prevent the potentially catastrophic impacts of climate change.

Goal: National mobilization of our economy through 14 infrastructure and industrial projects. Every project strives to remove greenhouse gas emissions and pollution from every sector of our economy:

- Build infrastructure to create resiliency against climate change-related disasters

- Repair and upgrade U.S. infrastructure. ASCE estimates this is $4.6 trillion at a minimum.

- Meet 100% of power demand through clean and renewable energy sources

- Build energy-efficient, distributed smart grids and ensure affordable access to electricity

- Upgrade or replace every building in US for state-of-the-art energy efficiency

- Massively expand clean manufacturing (like solar panel factories, wind turbine factories, battery and storage manufacturing, energy efficient manufacturing components) and remove pollution and greenhouse gas emissions from manufacturing

- Work with farmers and ranchers to create a sustainable, pollution and greenhouse gas free, food system that ensures universal access to healthy food and expands independent family farming

- Totally overhaul transportation by massively expanding electric vehicle manufacturing, build charging stations everywhere, build out high speed rail at a scale where air travel stops becoming necessary, create affordable public transit available to all, with goal to replace every combustion-engine vehicle

- Mitigate long-term health effects of climate change and pollution

- Remove greenhouse gases from our atmosphere and pollution through afforestation, preservation, and other methods of restoring our natural ecosystems

- Restore all our damaged and threatened ecosystems

- Clean up all the existing hazardous waste sites and abandoned sites

- Identify new emission sources and create solutions to eliminate those emissions

- Make the US the leader in addressing climate change and share our technology, expertise and products with the rest of the world to bring about a global Green New Deal

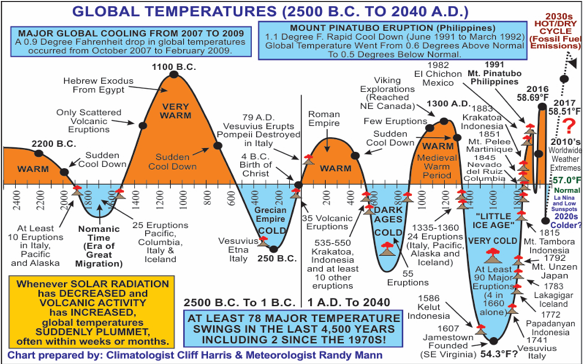

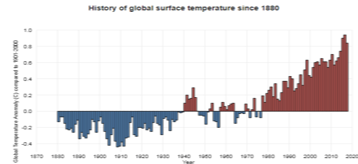

Geologic evidence shows our climate has been changing over millions of years. The warming and cooling of global temperatures are likely the result of long-term climatic cycles, solar activity, sea-surface temperature patterns and other long term ‘natural’ factors. Are climate models currently capable to precisely quantify how the next 100 years will unfold and how much temperatures will increase? Probably not. However, the burning of fossil fuels, massive deforestations, the replacing of grassy surfaces with asphalt and concrete, and the "Urban Heat Island Effect" are likely creating more harmful pollution. Since humans started cutting down forests, 46% of trees have been felled, according to a 2015 study in the journal Nature. Trees absorb not only the carbon dioxide that we exhale, but also the heat-trapping greenhouse gases that human activities emit. Tropical tree cover alone can provide up to 23% of the climate mitigation needed over the next decade. Global temperatures have clearly been rising, even after discounting the efficacy of current modeling. Common sense suggests "going green" whenever and wherever possible is reasonable. While the goals of the Green New Deal are directionally right, the timetable, technological hurdles, and costs are too extreme and the risk of economic harm too high to adopt it.

Climate scientists generally believe cutting emissions by 80% to 100% by 2050 would allow nations to collectively prevent global temperatures from rising above 2 degrees Celsius by 2100, the headline goal of the 2015 Paris climate agreement. In this light a target date of 2030 isn’t necessary. A longer timeline would allow reductions in emissions to occur without the risk of major disruptions to companies and consumers. The 10-year target would force utilities to shut down natural gas plants long before their useful life is over, threaten power disruptions, and increase the cost of electricity. A longer time runway would allow the learning curve to help avoid costly mistakes and improve the process as it unfolds, and create the opportunity to implement more technological advances that are surely to result over time.

Scaling up wind and solar power would require replacing hundreds of thousands of miles of transmission and distribution lines with high voltage wire, in addition to outfitting the infrastructure with sensors to create a smart grid."The idea of a wind and solar future — 100% in 10 years' time — that's a really big stretch in many places”, according to Francis O'Sullivan, head of research at the MIT Energy Initiative. O'Sullivan said the United States is "nowhere near" implementing a national smart grid, and he is skeptical the country could put one up in 10 years. Building out that infrastructure is a tortuous process that entails navigating a thicket of stakeholders, from local landowners to federal regulators. One could also anticipate opposition from environmentalists as was the case in San Benito Country in California. In 2010 County supervisors in San Benito County approved a solar panel project that would generate 399 megawatts and enough power for roughly 65,000 homes. Environmental groups sued saying the county had not done enough to protect endangered species including the San Joaquin kit fox, the giant kangaroo rat, and tri-colored blackbird. In July 2017 all sides approved a much scaled down project that will produce 130 megawatts, 67% less than the original approved project and 7 years after initial approval.

The Green New Deal also requires installing systems to store energy when the wind doesn't blow and the sun doesn't shine. The United States currently has 1.4 Gw of installed energy battery storage capacity, and it's on pace to grow that capacity to 4 Gw by 2023, just 4% of the electric power the nation can generate. "There is no solution for 100 percent renewable that doesn't require massive amounts of storage," according to Daniel Finn-Foley, senior energy storage analyst at energy research firm Wood Mackenzie. The dominant technology behind electric power storage is lithium-ion batteries which rely on rare earths like cobalt. More than half of the world's cobalt supply comes from the Democratic Republic of Congo, a central African nation with a record of instability and a history of child labor in the mining industry. To produce the needed battery storage the demand for cobalt would increase exponentially and, with half of the supply coming from a single source, so would the potential for the price of cobalt to soar. Over time new battery technologies that use less cobalt will emerge but not likely within the next 10 years.

The cost to transform the American economy to meet 100% of power demand through clean and renewable energy sources is significant. The American Society of Civil Engineers (ASCE) estimates it will cost $4.6 trillion at a minimum to repair and upgrade U.S. infrastructure. Any guesses on how much higher the final tally would be? The federal government paid $4,585 to weatherize each home in Michigan which would amount to $400 billion if the 95 million homes in the U.S. were upgraded for state-of-the-art energy efficiency. California has been developing a high speed rail system for the state since the 1990s. Voters approved a $10 billion bond to begin funding it in 2008. Cost projections in 2018 suggest it will cost at least $77 billion to complete 700 miles of track, which works out to $11 million for each mile. The GND intends to build out high speed rail at a scale where air travel stops becoming necessary, since air travel is the largest unregulated source of carbon pollution in the United States. Instead of flying from L.A. to New York in about 5 hours, passengers would board a high speed train which would take 12 hours to get to New York if it averaged 250 mph. That would certainly have a wonderful effect on the U.S.’s productivity! Based on California’s experience the cost of the rail line between L.A. and New York would be more than $300 billion. This would all be unnecessary if Boeing could just develop an airplane that doesn’t use fossil fuels. That may come true someday, but that day is certainly not in the next 10 years. I have no idea how much it will cost to create a sustainable, pollution and greenhouse gas free, food system that captures all the methane gas animals produce. I’m willing to bet the cost of food will rise and the system won’t capture all the methane produced by cows. Maybe every American can be coerced to become a vegetarian to save the planet. Methane problem solved!

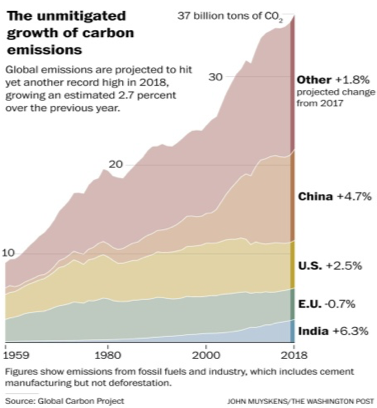

Based on the sense of urgency expressed in the Green New Deal one would think the U.S. has been a global emissions deadbeat while the rest of the world was doing their part. The fact is the U.S. has been doing a better job of controlling emissions than the European Union, Japan, and every other country that has signed the Paris Agreement. During the post crisis recovery, the U.S. has lowered emissions while emissions have increased everywhere else. You won’t be confronted with this information by those pushing the GND since it doesn’t serve their purpose of further scaring people who are already receptive to the message. The reality is most of the growth in emissions during the next 20 years will come from China and India. Unless they curtail their plans to build more than 700 coal-fired electricity plants in the next decade, it won’t matter if the U.S. burdens itself with the GND. All the CO2 billowing from China and India will find its way into the U.S. There are more than 350 million people in India who don’t have electricity and I suspect there no Indian politicians who will run on the platform of denying those without electricity to lower global CO2 emissions.

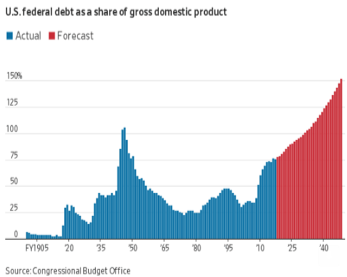

According to the Congressional Budget Office (CBO) total U.S. debt just surpassed $22 trillion in 2019 which is 105% of GDP. In the next 30 years the CBO estimates the debt to GDP ratio will rise to 150%. After reviewing a portion of the costs of the New Green Deal one wonders how the U.S. could afford to pay for the massive revamping of the economy given the already unstable fiscal foundation of the country. The sponsors of the GND would raise taxes on the rich by increasing the highest tax rate to 70%. Since higher income taxes won’t come close to covering the cost of the GND, the government will borrow the rest from the Federal Reserve. This was done during World War II and could be used now to fight the War Against Climate Change. (WACC1)

Advocates of Modern Monetary Theory (MMT) believe all money is ultimately created by the government, which prints it and puts it into circulation. Consequently, the thinking goes, the government can never run out of money. It can always make more. Taxes make the whole system work since the need to pay taxes compels people to use the currency printed by the government. Inflation could escalate as there could be too much money chasing too few goods and services. MMT has an answer for that problem. Raise taxes to curb demand so the economy slows down. Adjusting tax rates would play a more significant role in managing the business cycle, which means relying more on the judgment of politicians. What could wrong with that! On the surface MMT reduces the role of the Federal Reserve as its main purpose would be to absorb tens of trillions of Treasury bonds issued to fund the GND. The Fed would be expected to remit most if not all of the interest collected on its bond holdings back to the Treasury, so the actual cost of funding the GND could be close to nothing. This is a liberal’s fiscal fantasy of spending any amount money with no consequences. Who needs to diet if one can eat anything all day long and never gain weight! If it sounds too good to be true it probably is, an adage advocates of MMT and the dreamers of the GND are clearly not familiar with. According to Modern Monetary Theory the U.S. government would never need to balance the budget and attempts to balance the budget will only curb economic growth. Of course growth would be slowed by a balanced budget when the comparison is to growth spurred by unlimited government spending. Duh!

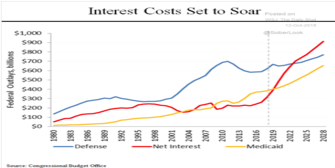

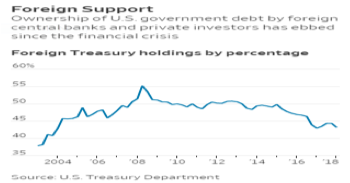

Even if the GND could be funded by essentially ‘free money’, interest expense on all the other government spending is expected to surge in coming years. According to the Congressional Budget Office within the next decade the amount of spending for interest on the outstanding federal debt will exceed what the government spends on Medicare and Defense in the annual budget. Foreigners own more than 40% of the federal debt so the interest payments on the debt held outside the U.S. are sent overseas. As the total amount of federal debt continues to climb, there is a risk that the appetite for Treasury bonds from foreigners could wane and lead to higher interest rates. If Treasury yields rise by 1.0% across the whole maturity curve, annual interest costs to the Treasury would increase by $150 billion. In other words, the CBO’s estimate for interest expense in the next decade could prove optimistic.

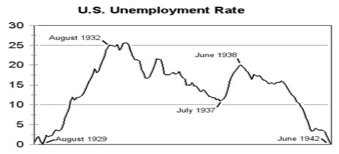

After taking office on March 4, 1933 President Roosevelt launched the New Deal and numerous government programs to revive economic growth and lower the unemployment rate which was 25%. The Works Progress Administration (WPA) was created to return the unemployed to the work force. At its peak the WPA employed more than 8.5 million workers who built 650,000 miles of highways and roads, 125,000 public buildings, like schools and hospitals, but also major projects like the LaGuardia Airport and the San Francisco–Oakland Bay Bridge. Today the unemployment rate is 4.0% and many employers say their biggest challenge is finding skilled workers. Implementing the New Green Deal with unemployment so low would make it very difficult to find enough workers en masse and with the skills needed to build hundreds of thousands of miles of transmission and distribution lines with high voltage wire, in addition to outfitting the infrastructure with sensors to create a smart grid, or to weatherize 95 million homes in the U.S. The cost of retraining current workers and the time required to develop a small army with the skills needed to accomplish the enormous tasks envisioned by the GND makes the timeframe of 10 years nearly impossible.

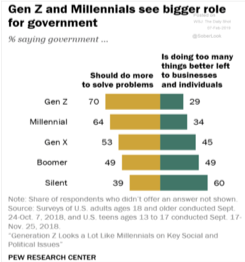

Based on the unrealistic timeline and costs of the Green New Deal it would be easy to dismiss the potential of its becoming policy or influencing policy anytime soon. Longer term, demographics suggest the U.S. is moving toward a time where the federal government will play a greater role. Members of the Millennial and Gen Z generations believe the government should do more to solve problems and think human behavior is affecting climate change. At the time of the 2020 election the population of Millennial and Gen Z’s will represent 37.5% of the population compared to 28.5% for Boomers and 9.5% of the Silent generation. Sometime in 2019 the Millennial generation will be larger than the Baby Boom generation. In the 2024 and 2028 elections Millenials will be voted into office in far greater numbers and play a larger role in setting policy. Gen Z’s will be voting in larger numbers and supporting many of the policy choices Millennials will place on the national agenda. As this new wave of voters enter the polling booth, members of the Silent generation will be gone and Baby Boomers will increasingly be riding off into the sunset.

According to a recent survey by the Pew Research Center, 64% of Millennials support more government intervention to solve societal problems, while Baby Boomers are split. In 2020 all of the Millennial generation will be old enough to vote, so their influence will be determined by their turnout compared to Baby Boomers. Gen Z’s support more government intervention (70%) than Millennials (64%), but only a small portion of Gen Z’s will be old enough to vote in 2020. That will increase in the 2024 and 2028 elections, so the influence of Gen Z’s will rise accordingly. According to an August 2018 poll by Gallup only 45% of Americans aged 18 to 29 view capitalism positively while 51% are positive about socialism. Only 24% of Baby Boomers had a positive view of socialism.

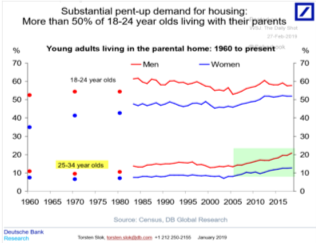

Socialism is a political and economic theory of social organization which advocates that the means of production, distribution, and exchange should be owned or regulated by the government. I doubt many Millennials or Gen Zs are not in favor of owning private property or want the government to exercise control over every aspect of the American society. Millennials are too young and Gen Zs weren’t even born when the Berlin Wall fell in 1989 to understand what that event represented. Capitalism hasn’t trickled down to Millennials as it did for prior generations. A recent study by the Federal Reserve Bank of St. Louis found Millennials born in the 1980s have a net worth 34% below what was expected. Younger Millennials and older Gen Zs have incurred a heavy burden of student debt which now totals $1.4 trillion. Student debt has had real world consequences as Millennials are older than prior generations in purchasing their first car, first home, getting married, and starting a family. Compared to 1960 a much higher percentage of Millennials (25-34 year olds) are living with their parents rather than on their own.

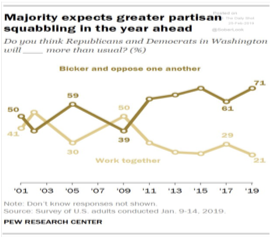

It is understandable that Millennials and Gen Zs would be open to a change in the role of government given the high level of political dysfunction that has resulted in very little progress on a myriad of social issues and problems in the past decade. Despite party affiliation, it is nearly impossible not to see that the level of rancor and divisiveness has exploded since the 2016 election. And most Americans, irrespective of their generation, expect partisan politics to only get worse, which doesn’t bode well for making progress on any issue. It shouldn’t come as a surprise that so many younger Americans have become disillusioned with the status quo and are thus receptive to something different. Most may not even know what true socialism really means, but they do know the current direction hasn’t been good for them.

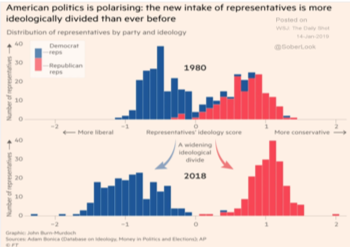

Politics have become more polarized since 1980 as both parties have become more ideological and further apart. In 1980 there were more Democrats who were right of center (noted by 0 on the X-axis). There was a significant ideological overlap of Democrats and Republicans in 1980, while Republicans were more diverse even though most were right of center. In 2018 Republicans are less diverse and moved further to the right of center. The Democrats have also become less diverse and more ideological and have moved further to the left of center. With the gap between the parties so wide it is difficult to be optimistic about the role of compromise on any issue. There is much debate about building a wall on the Mexican border, but no discussion about The Wall that has already been built between Democrats and Republicans. This Wall is far more important and will only be dismantled when both political parties identify more with being an American than a member of their political party. In 1780 Americans came together to fight against the British, an enemy outside the future U.S. Eighty years later the country was torn apart in 1860 by divisions within the U.S. by the Civil War. In 1940 and 80 years after the Civil War, a common enemy outside the U.S. motivated people to make sacrifices large and small to be victorious in World War II. Eighty years after 1940 is 2020, and just as in the 1860’s, the country is being torn apart from within. Ideology has become paramount and anyone who doesn’t agree is one of them. Maybe it’s time to celebrate what each American has in common, rather than diversity at any cost. Although I would like to be optimistic, I suspect it will take a crisis, larger than the financial crisis in 2008 to bring our country together.

Jim Welsh

@JimWelshMacro

[email protected]

© Macro Tides

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All