In Part I of this four-part series, we introduced this report and discussed the origin narratives of Modern Monetary Theory (MMT). This week, we will examine the principles and consequences of the theory.

Principles of MMT1

MMT begins its analysis with a focus on macroeconomic identities and flows.2 The theory states that the creation of money begins with government. The government buys goods and services and injects money into the economy. That money goes into the private sector through the banking system and is either spent or saved by households and firms. To prevent the money supply from becoming excessive, the government taxes households and businesses or issues bonds that absorb cash and, in return, become financial assets.

These macroeconomic identities all balance to zero, as referenced below in our WGR series from May 2017.

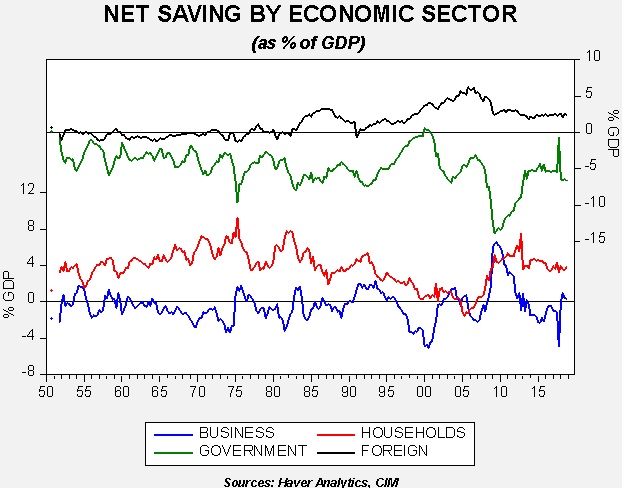

The government runs deficits most of the time. For most of the postwar period, the household sector was a saver, although households did dissave toward the end of the housing boom. Business tends to be a dissaver. Until the early 1980s, the U.S. mostly had a balanced current account; a current account deficit, the broadest measure of foreign flows, including trade and remittances, started to turn negative after 1980. A current account deficit is positive in the above chart because it is essentially importing foreign saving.

Note that business dissaving expanded when the Federal government ran a modest surplus in the late 1990s. Much of this dissaving supported investment in technology and triggered a bubble in equities.

Although these identities always balance, there is nothing, in theory, to determine the direction of causality. On any given day in the financial media, one will hear the statement that the U.S. undersaves and thus we run a trade deficit. However, it is equally possible that foreigners oversave and, since the U.S. economy has both open current and capital accounts, that foreign saving must be accommodated through dissaving by either government, households or businesses. The fact that the U.S. runs a trade deficit with low interest rates and a stable to strong currency would suggest that the reason for the importation of foreign saving is that it wants to come here, not that we need it. If we needed the saving, one would expect a weaker dollar and higher interest rates. And so, as foreign money flows into the U.S. economy, domestic net savings has to adjust. In the last decade, it adjusted mostly by household dissaving, which led to more borrowing and a housing bubble.

From the macroeconomic identities, MMT works if the sovereign currency is non-convertible. In other words, the government does not guarantee that the money it issues can be converted into gold or any other commodity. Although it isn't essential, a floating exchange rate gives policymakers less constraint on fiscal and monetary policy. If the sovereign currency has a fixed conversion rate to a precious metal or other commodity, or can be directly converted at a guaranteed rate for a foreign currency,3 then MMT doesn’t hold. In fact, under conditions of convertibility, the orthodox model of money holds. However, there is no developed nation on earth that has a convertible currency. Therefore, the primary condition of MMT does appear consistent with how developed economies manage their currencies.

The Consequences of MMT

Assuming MMT does hold, what does it mean for policy and the economy?

Governments that issue currency under conditions of MMT never face a monetary constraint. They can run deficits and always guarantee that bondholders will get paid. The risk under MMT isn’t from the government “running out of money,” but inflation. In other words, the constraint that governments face on fiscal spending is an inflation constraint, which is, in part, a capacity constraint.

Governments that issue a non-convertible currency can always afford to buy something. Throughout history, those trying to constrain government have argued against spending programs or deficits on the basis of affordability. Under a convertible currency, this is a legitimate argument; with a non-convertible currency, it isn’t true. However, just because they can doesn’t mean they should. Malinvestment by government does occur. Japan’s famous “bridges to nowhere,” infrastructure spending designed to lift growth, failed to boost the economy over the long term.4 For a central government that issues non-convertible currencies, spending issues are political, not based on affordability. Simply put, such governments are not households and analogies to household budgets violate the logical error of composition.

Not all governments are the same. If a government doesn’t issue currency it faces a situation similar to a government that has a convertible currency. In the U.S., state and local governments have to run balanced budgets. A state cannot deficit spend without running the risk of default. The recent default of Puerto Rico is a U.S. example. The Eurozone is another one; Greece found it could not service its debts because it didn’t control currency issuance. That was controlled by the European Central Bank.

When the government runs a deficit, it increases bank reserves and lowers interest rates. This is one of the more controversial elements of MMT. Keynesian economics, at least the type taught in most college courses, uses an IS-LM framework. In this framework, a deficit absorbs liquidity and raises interest rates. MMT rejects the IS-LM framework.5 If the central bank sets a desired policy rate and fiscal spending puts excess reserves into the banking system, then the central bank may need to raise rates to absorb the reserves that fiscal spending injects into the financial system. Since increased lending can be inflationary, the inflation impact may increase interest rates. But, by itself, deficit spending increases bank reserves and depresses interest rates.

Taxes are necessary, but not for revenue. The government doesn’t need taxes to spend. But it does need taxes to drive demand for the currency it issues.

Government finance should be based on functional needs, not on the need for balance. This notion comes from a seminal paper by Abba Lerner in 1943 in which he argued that governments should conduct budgeting not for “soundness,” that is, to balance, but to bring about full employment.6 Interestingly enough, early in his career, Milton Friedman postulated a similar position.7 These papers highlight that it is illogical to compare the government budgeting process of a nation that does not have a convertible currency to households or businesses. Instead, government budgets should focus on societal goals.

If taxes are not necessary for revenue, what should we tax? This was the topic of a famous paper8 by Beardsley Ruml, the chair of the Federal Reserve Bank of New York from 1941 to 1946. Ruml postulated that taxes:

1. Help stabilize inflation;

2. Give the state an instrument to affect the distribution of income;

3. Give policymakers tools to adjust for market externalities;

4. Assess costs for the use of certain public goods.

If there were too much money in the economy and inflation was rising, then taxes would effectively destroy money and reduce price pressures. If income inequality was determined to weaken democracy and affect labor markets, then high marginal tax rates would address that concern. Taxes could be used to lower demand for “bad” things (sin taxes, or pollution taxes) and increase the production of “good” things (lower taxes or subsidies for day care workers, kale growers). And, finally, if a particular industry or consumer benefited from a public good (e.g., roads, canals, locks and dams), Ruml thought they should pay for part of its provision.

Note that the redistribution argument isn’t about “Robin Hood,” taxing the rich to give to the poor; it’s about changing behavior.

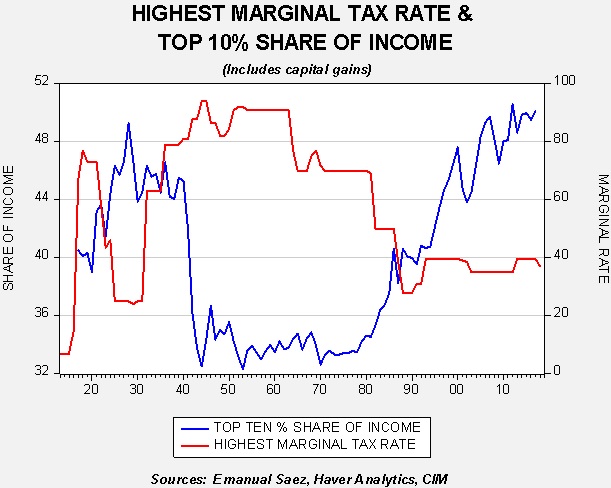

This chart shows the highest marginal tax rate along with the top 10% share of income. The pattern suggests that high marginal tax rates reduce the share of income that goes to the top 10% of households. When the highest marginal tax rate was reduced in the early 1980s, inequality rose and has continued to rise, reaching levels not seen since the 1930s.

Interestingly enough, the level of the highest marginal rate has little effect on the federal government’s revenue streams.

This chart shows the highest marginal tax and federal government revenue as a percentage of GDP. Since the time the income tax became universally applied in WWII, the government’s revenue share of GDP has been remarkably stable.

These charts suggest that the marginal tax rate affects income inequality but doesn’t change revenue flows. If the goal of high marginal tax rates is to increase revenue to give to the less fortunate, it fails. So, how does the marginal tax rate affect inequality if it doesn’t seem to increase revenue? After all, the point of high tax rates is to take money away from the affluent.

We suspect the high marginal tax rate affects corporate behavior. When marginal tax rates were elevated, companies “paid” their executives with “perks” such as company cars, special washrooms, reserved parking, country club memberships, etc. In addition, there is likely an element of status signaling involved with income. A person probably doesn’t need a billion dollars to survive but it does allow one to compare to others. It is possible that raising marginal tax rates will reduce the need to reward the upper income brackets and allow for income to be distributed to the lower income brackets. But, as we will discuss below, high marginal tax rates carry other costs.

Ruml also argued that corporate tax rates were bad taxes. He suggested that the incidence of the tax (who actually pays the tax) was difficult to determine, but either workers, shareholders or consumers (or potentially all three) were bound to pay. Since the incidence was difficult to determine, even if the presumed target was considered positive, the corporate tax could end up missing its goal. In addition, he argued it distorted corporate behavior (led to tax avoidance behaviors that may not be positive for the firm or the economy) and usually led to multiple taxation (the corporation paid its tax and the dividends it paid also generated a tax).

It should also be noted that if the goal of the tax was to maintain demand for the currency, then a simple flat tax could accomplish the same thing.

Part III

Next week, in our third installment, we will analyze the importance of paradigms and how MMT fits into the equality/efficiency cycle.

Bill O’Grady

March 18, 2019

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1 Although the purpose of this report is to examine MMT, our focus is more on the ramifications of the theory on hegemonic policy and exchange rates. For those interested in studying the theory more fully, see op. cit., Wray, or a simplified video is available: https://modernmoney.wordpress.com/2014/02/10/mmt-nutshell-diagrams-and-dollars/

2 For a deeper discussion of macroeconomic identities and flows, see WGR series, Reflections on Trade: Part I (5/1/2017); Part II (5/8/2017); Part III (5/15/2017); and Part IV (5/22/2017).

3 As is seen with a currency board.

4 https://www.nytimes.com/2009/02/06/world/asia/06japan.html

5 MMT proponents argue that the IS-LM framework is not Keynesian but a variant developed to integrate neo-classical economics with Keynesian economics. Keynes himself didn’t live long enough to see this integration but would have probably rejected it because he viewed investment as more than just a function of the level of interest rates.

6 http://k.web.umkc.edu/keltons/Papers/501/functional%20finance.pdf

7 ]https://miltonfriedman.hoover.org/friedman_images/Collections/2016c21/AEA-AER_06_01_1948.pdf

8 http://bilbo.economicoutlook.net/blog/wp-content/uploads/2010/04/taxes-for-revenue-are-obsolete.pdf

© Confluence Investment Management

More Fixed Income Topics >