The US Federal Reserve’s decision to keep interest rates steady at its March meeting came as little surprise, but its updated “dot plot” projections were interpreted by markets as sending a decidedly more dovish signal than expected. Franklin Templeton Fixed Income Group CIO Sonal Desai offers her take on the meeting, and why she feels markets shouldn’t read too much into the dots.

I’m surprised at how surprised—and frothy—market reaction has been at the outcome of the Federal Reserve’s (Fed) March policy meeting. My reading is that the Fed confirmed the patient tone it already adopted in January, and for the same reasons, but the Fed remains data-dependent and investors should focus on the economic outlook, not on the dots.

Fed policymakers pointed to the soft tone of first-quarter economic indicators, but the first quarter has typically had a seasonally soft bias. This justifies caution, but I don’t view it as a sign of a significantly weaker outlook.

Moreover, Fed Chairman Jay Powell’s tone in the Q&A session following the announcement was nowhere near as dovish as the immediate market reaction would suggest.

Don’t Depend on the Dots

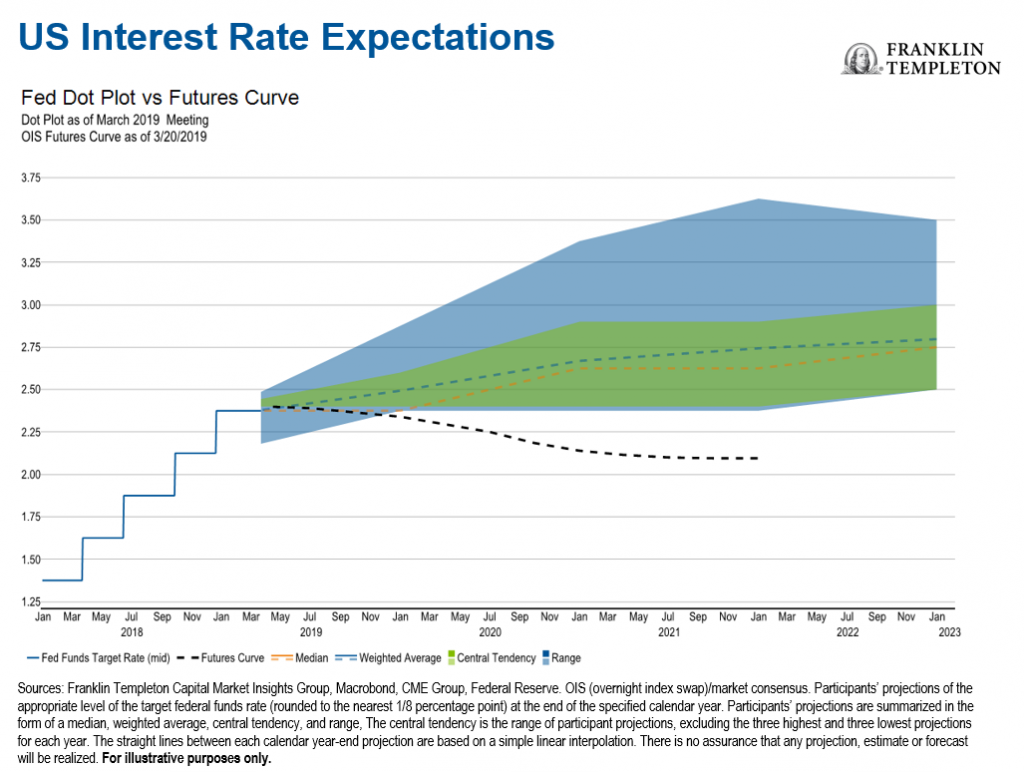

Markets saw the change in the “dot plot” as an important dovish surprise. The dots now show no more interest-rate hikes in 2019 and just one hike in 2020, whereas in December they reflected two rate hikes this year.

It’s important to understand, however, that the dot plot does not represent the collective, consensus view of the Federal Open Market Committee (FOMC), the Fed’s decision-making body. The dots simply represent the views of each individual FOMC member as to where the policy rate will likely be in each year. The dot plot has changed quite dramatically within three months in the past, and can easily do so again.

Indeed, Powell has been trying to de-emphasize the importance of the dots, because the Fed has abandoned its formal forward guidance and now wants to maintain flexibility to react to economic conditions. He specifically indicated the markets should not take the dots as a substitute for the forward guidance that the Fed has chosen to abandon, most recently in a speech at Stanford University. He repeated that message at the March policy meeting, but markets seem to have completely ignored it.

In fact, markets have gone even further: Fed funds futures show that 40% of investors now expect rate cuts already this year1, while the new Fed dots envision one more rate hike—albeit only next year—and then rates on hold through 2021.

Most importantly, the Fed has indicated clearly its policy will be data-dependent, and I continue to expect the data will warrant higher rates.

US Economic Projections

Media headlines have emphasized the downward revisions in the Fed’s monetary policy and economic forecasts, but these amounted to just marginal changes:

- The Fed lowered its 2019 US growth forecast to 2.1% from its prior forecast of 2.3%, and lowered its 2020 forecast to 1.9% from 2.0% prior.

- The 2019 inflation projection (based on Core Personal Consumption Expenditures) was lowered to 1.8% from 1.9%

- The projection for the unemployment rate edged up to 3.7% for 2019, from its prior projection of 3.5%

These are all marginal revisions, well within the margin of forecasting error.

Confidence in Controlling Inflation

In my view, the Fed has decided to keep interest rates on hold because it feels highly confident that once inflation starts to rise, it will be able to quickly pull it back under control. Given this, it prefers to stack the deck in favor of growth and let the economy run hot until it sees inflation move above the 2% target. The Fed is also confident that the risk of asset bubbles is limited—though there’s little doubt in my opinion that the markets are on a bit of Fed-fueled sugar high.

Trade Tensions Should Ease

The Fed reiterated that trade tensions and Brexit counsel prudence.

I think these are secondary considerations. The United States and China seem headed toward an agreement on trade in the near term. Brexit tensions have risen ahead of the March 29 deadline, but it looks like the United Kingdom will now get a 6-9 month extension, which will push the issue to the backburner as far as markets are concerned. Separately, it is difficult to imagine that markets have the ability to be further shocked by an event that they have been anticipating for almost three years now.

The main driver of Fed policy will remain the domestic economic outlook. As I noted in my February “On My Mind,” household consumption remains supported by a hot labor market and a robust balance sheet. As the global uncertainty diminishes, the US growth outlook will continue to warrant higher interest rates.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. Floating-rate loans and high-yield corporate bonds are rated below investment grade and are subject to greater risk of default, which could result in loss of principal—a risk that may be heightened in a slowing economy.

1. Source: CME Group. Fed funds futures are financial contracts representing the market’s view of where the daily official federal funds rate will be at the time of the contract expiry.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Alternative Investments Topics >