Trade Wars—The Dog That Didn’t Bark

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe prospect of a “trade war” between the United States and China has caused some investor trepidation over the past year. But are the fears of economic fallout from this “war” warranted? And, was there ever really a war at all? Franklin Templeton Fixed Income CIO Sonal Desai weighs in.

In the Sherlock Holmes story “The Adventure of Silver Blaze,” during the night a prized race horse gets spirited away from his stable and its trainer gets murdered. In the investigation, Sherlock Holmes calls attention to what didn’t happen: The dog on the property did not bark.

For over two years we have lived in fear of trade wars—fear that a spreading escalation of protectionist measures would cripple global trade flows and send the global economy tumbling into a severe downturn. The International Monetary Fund (IMF) has just stoked a fresh wave of alarmist media headlines with its newly released World Economic Outlook (WEO).

Yet global trade hasn’t collapsed, and the global economy hasn’t stalled. Global trade wars are the dog that didn’t bark.

I believe there are three reasons for this: The wars turned out to be limited skirmishes; free trade was never truly free to start with; and most importantly, the elasticity of global growth to global trade has undergone a structural change.

This has two important implications for financial investors, on which I will elaborate at the end: (1) global growth will likely surprise to the upside, and bond yields with it; and (2) the real action is at the company, industry and country-specific level, making portfolio selection more important than ever.

Rumors of Global Trade’s Death Have Been Greatly Exaggerated

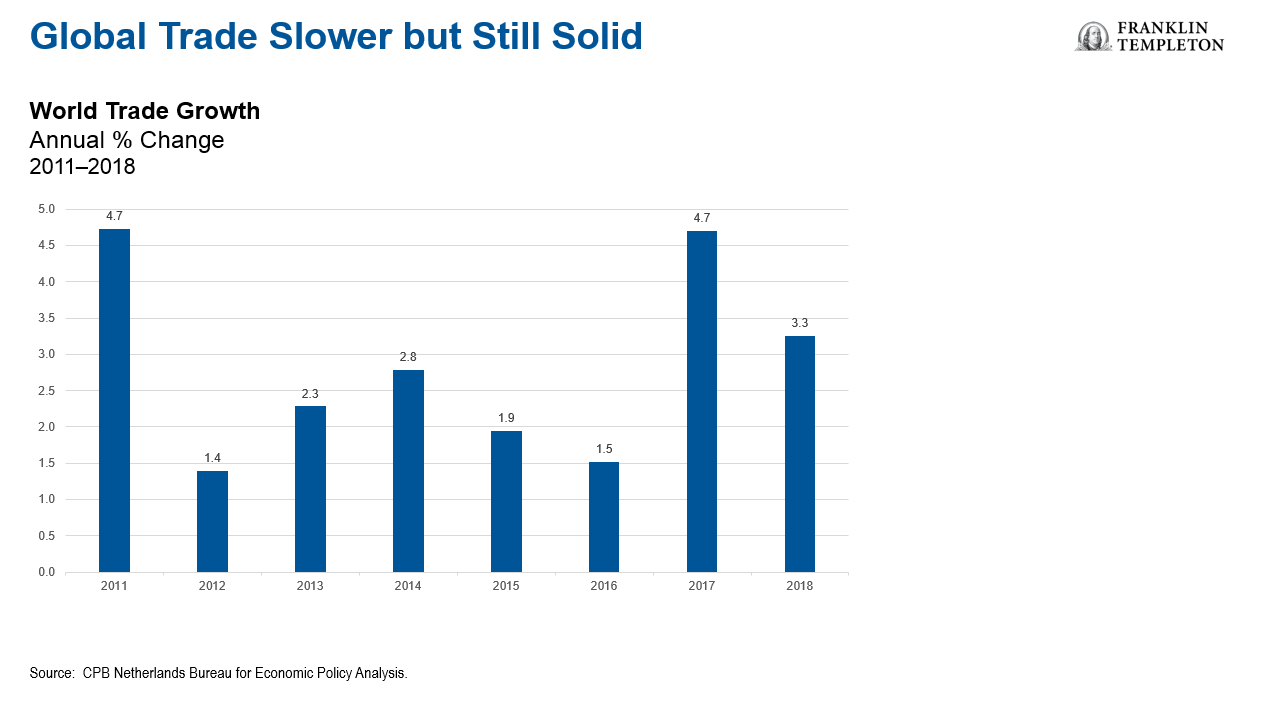

Global trade did slow down during 2018, but that partly reflected payback from a very strong 2017, when global trade expanded 4.7%—more than three times as fast as the year before. Last year’s 3.3% pace still compares favorably to the 2.0% average of 2012–2016.

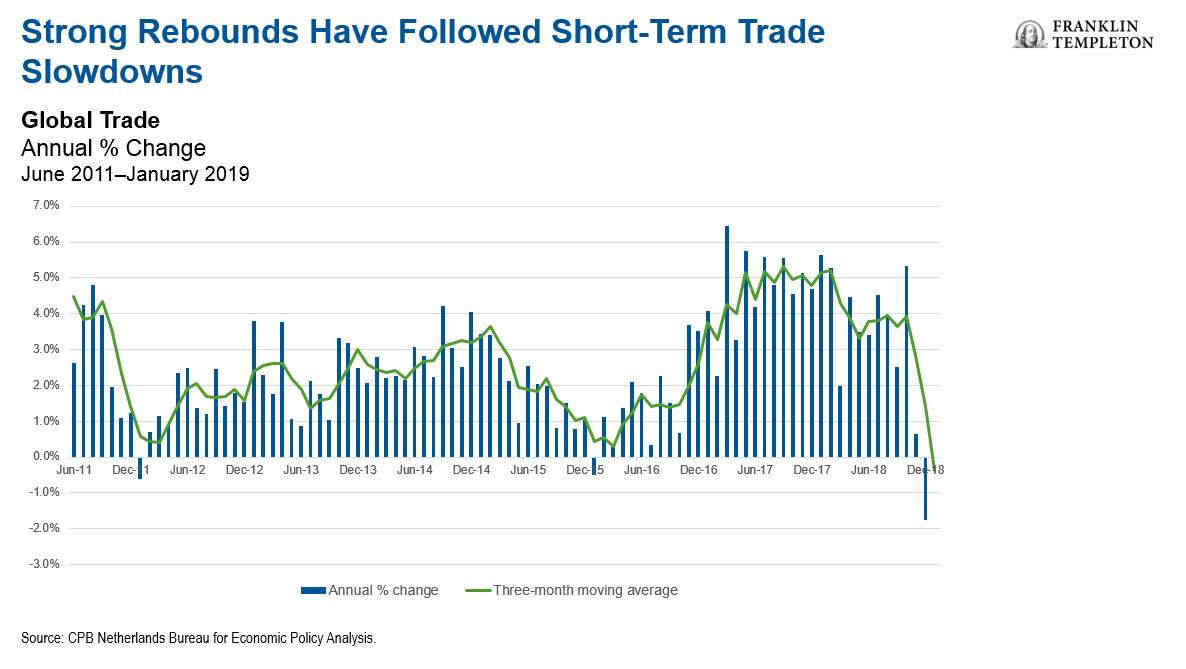

Global trade slowed further at the end of last year: The three-month moving average held around 5% for most of 2017, then stepped down one notch to about 4% for the second and third quarters of 2018, and crawled to a halt by January 2019. This needs to be watched closely, but before panicking we should note that we have seen significant decelerations in global trade twice before in this decade (2015–2016 and 2011–2012), and both times trade rebounded nicely.

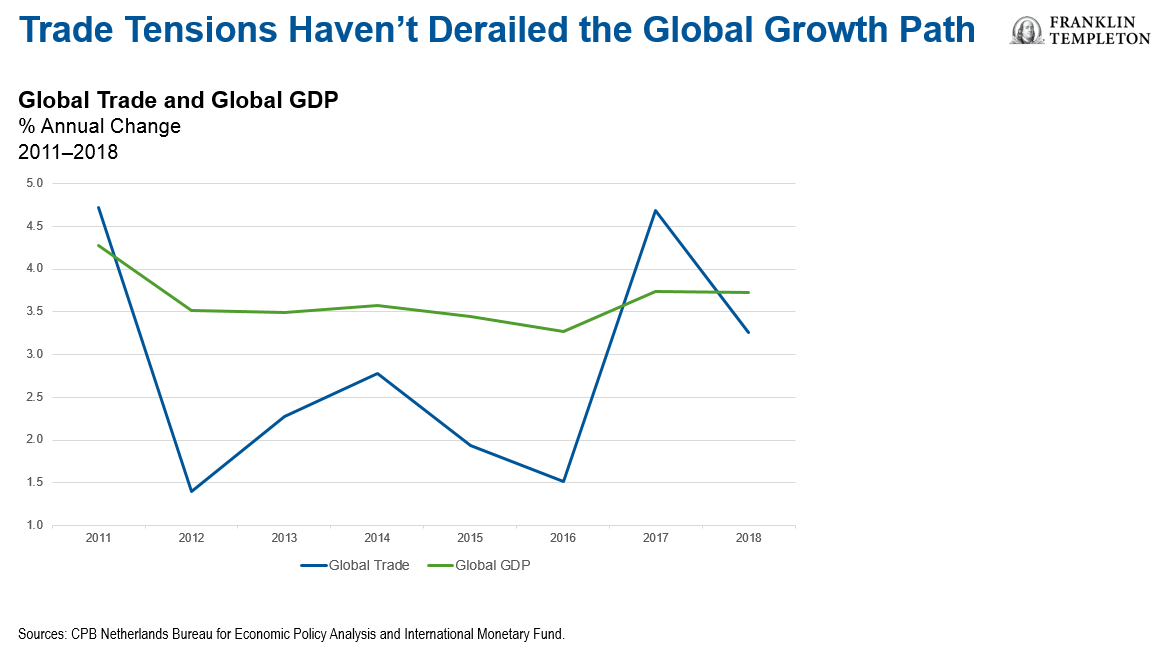

More importantly, note that global growth held steady at 3.7% last year, unchanged from 2017, even as global trade decelerated. Neither the fear of trade wars nor the actual slowdown in trade flows was serious enough to cripple global economic activity.

No Wars, Just Skirmishes

There are three reasons why global trade tensions have had limited impact on global growth. First, the specter of an all-out trade war with protectionist measures spreading like wildfire, which has been constantly invoked by pundits and the press, has not materialized. Even the toughest bilateral negotiations continue to be punctuated by targeted and measured actions, not a tit-for-tat escalation of tariffs.

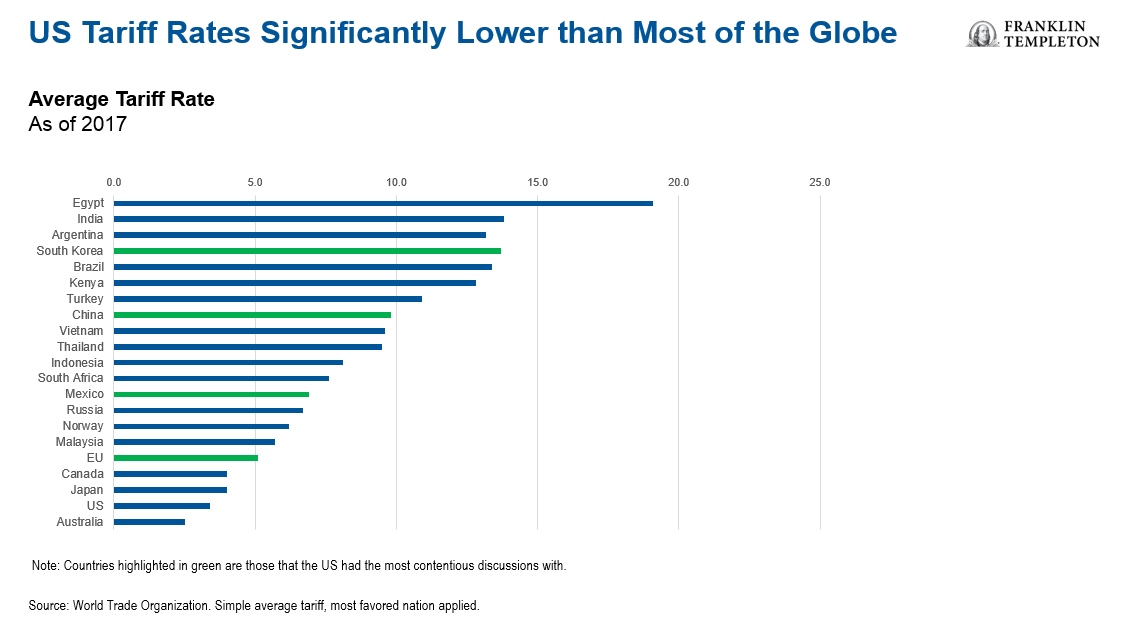

Why? Well, at least in part, because the United States does have a point: Almost everyone charges higher tariffs; even the European Union (EU) charges import tariffs that are on average 50% higher than the US (5.1% vs. 3.4%). The chart below shows that the countries that the US had the most contentious discussions with (highlighted in green) all have significantly higher tariffs than the US. No doubt, the US could be handling all this with greater finesse, but the reason other countries don’t just strike back in outraged vengeance is that they know this, and they have a lot more to lose from an escalation.

The impact on global commerce, therefore, has been limited, and I expect the coming months will show a stabilization in global trade flows after the recent deceleration.

Businesses Can Handle Uncertainty Better Than Pundits Do

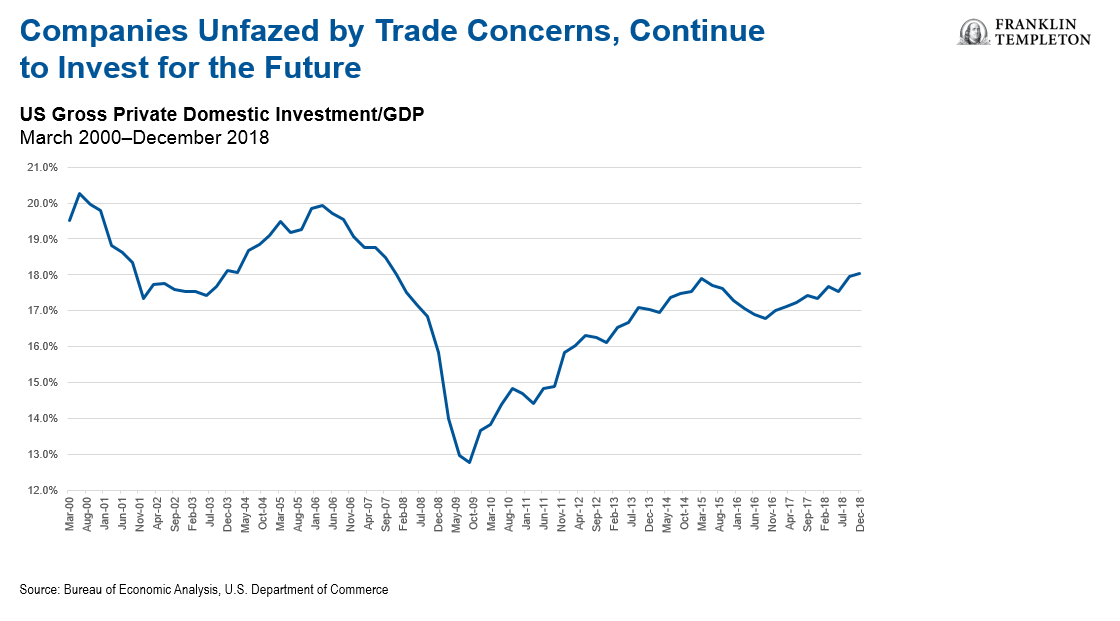

Second, businesses have not panicked. The concern was that the uncertainty caused by rising trade tensions would cause businesses to freeze investment plans. Now, while anecdotal evidence does suggest that corporate leaders are concerned about trade tensions, the data show that investment accelerated robustly through 2017 and 2018: gross private domestic investment rose from 17.0% of gross domestic product (GDP) at the end of 2016 to 17.4% at the end of 2017 and 18.1% at the end of 2018. Albeit while complaining, many businesses appear to have taken the headlines with a pinch of salt, and their confidence in a well-entrenched global recovery has so far outweighed concern about trade tensions.

Economists also appear to have underestimated companies’ ability to adapt to the limited supply chain disruptions seen so far. Also, to reiterate, free trade was never that free. As we have seen above, a number of countries levy significant tariffs. And the past decade had already witnessed a creeping rise in protectionism in the form of forced localization requirements in emerging markets (EMs) and other non-tariff barriers. Many businesses had already learned to adapt.

Structural Changes in Global Trade

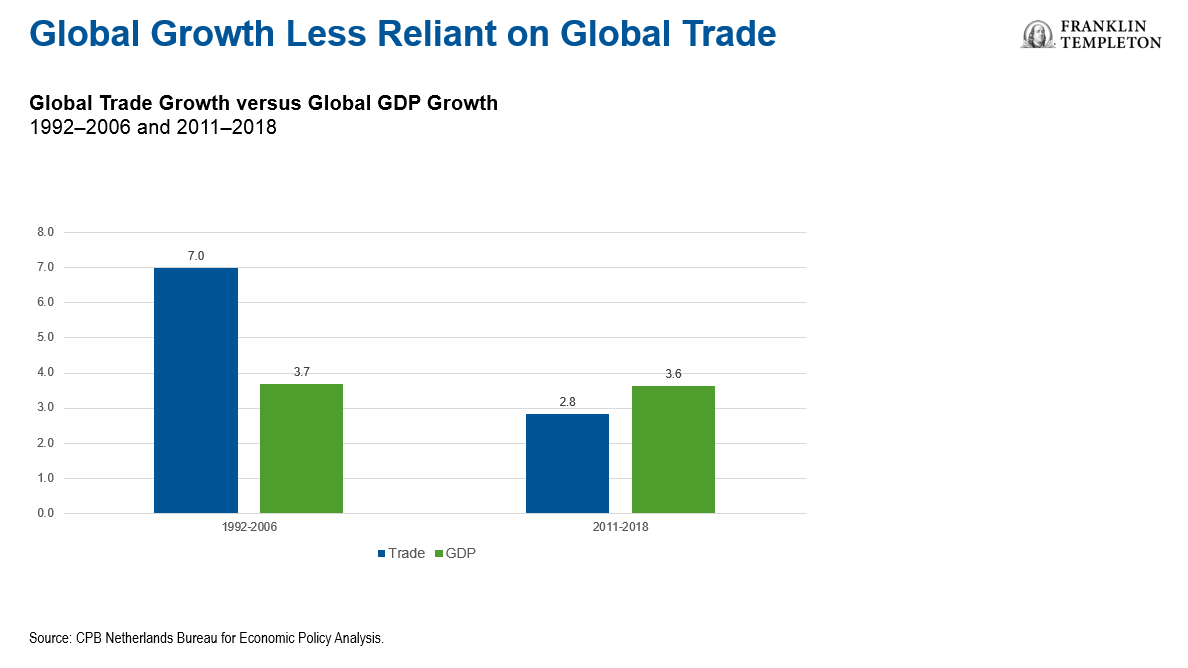

Third, and most important of all, the elasticity, or sensitivity, of global growth to changes in global trade has dropped sharply over the last 10 years. In the decade and a half before the global financial crisis, global trade expanded twice as fast as global GDP. Over the past 10 years, the pace of growth of global trade has been one-fifth lower than that of global GDP. But the global economy kept expanding on average at the same pace as when global trade was booming.

This amounts to an important structural change, driven by three major factors.

First, strong economic growth in EMs created a burgeoning middle class that started to absorb a growing share of global consumption. A larger share of the goods and services produced in China, India and other major EMs are now consumed locally rather than exported. The McKinsey Global Institute notes that EMs’ share of global consumption has risen about 50% in the last 10 years, and it projects that EMs will consume almost two-thirds of global manufactured goods by 2025.1China now exports just 9% of its production, a share that has almost halved from the 17% of 2007.

Second, several EMs have begun to develop stronger domestic supply chains, to improve efficiency and speed to market—for example, the McKinsey Global Institute report cited above notes that emerging Asia now imports just over 8% of the intermediate inputs needed for its production, down from over 15% just a year ago in 2017. This has increased the importance of intra-regional trade. And together with stronger EM consumption, it has boosted the so-called South-South trade (the proportion of trade that occurs across EMs rather than with advanced economies) by nearly 40% over the past decade.

Third, new advanced manufacturing technologies, from 3D printing to artificial intelligence-driven productivity solutions, have greatly reduced the importance of lower labor costs and encouraged advanced economies to reshore production to take advantage of better infrastructure, a more skilled workforce and, in the case of the US, declining energy costs. Similar technological innovations have also boosted the role of trade in services—including digital services and intangibles like intellectual property—which has been growing at a much faster pace than trade in goods.

These changes are likely to continue in the years ahead as living standards in EMs keep rising and technologies continue to evolve. Global trade still plays an essential role, but the current moderate pace of growth in global trade is consistent with robust global GDP growth.

To put it differently, the tariff wars that many are so worried about focus on traditional industrial sectors, while trade keeps shifting to the new sectors of the economy. This might explain why the impact of localized trade disputes remains limited. In its October WEO report, the IMF simulated a scenario in which the US-China trade war escalates, the US imposes a 25% tariff on all imported cars and parts and suffers a commensurate retaliation, business confidence gets hit and financial conditions for corporations tighten because of the hit to their margins.

The net result? The level of global GDP would be 0.4% lower after five years—implying an even smaller impact on GDP growth rates. While a 0.4% lower GDP level is not insignificant, it is certainly not dramatic.

In its just-released April WEO, the IMF unveiled a new analysis that simulates the impact of a 25% tariff on all trade between the US and China, but without the spillover impact of uncertainty on investment. It uses a battery of different econometric models, including the one used in the October simulations. As this has generated a new wave of alarmist media headlines, I would make two observations:

- The new simulation results are broadly consistent with the October ones, but are presented in a much more dramatic fashion, stating that “Annual real GDP losses range from -0.3% to -0.6% for the US and from -0.5% to -1.5% for China.” Predictably, this led even the Wall Street Journal to report that China’s GDP would decline by 0.5-1.5%. But this is not what the simulation implies. China’s GDP would not decline. It would keep growing, but at a slower pace.2

- Most important, a 25% tariff on all US-China trade is a worst-case assumption that seems extremely unrealistic, and therefore of little use to guide business and market expectation. There is no doubt that if the US and China were to levy a 25% across-the-board tariff on all bilateral trade this would have a significant impact on the two economies. But this reminds me of Philip the II of Macedon threatening ancient Sparta that “…if I bring my army into your land…” The Spartans laconically replied “if.”

Implications for Investors

For investors, this has two important takeaways.

First, global growth will likely surprise to the upside, because fears on trade remain exaggerated. This, in turn, will support an upward drift in yields compared to market expectations, despite the markets pricing and re-pricing US Federal Reserve interest-rate moves.

Second, the real action is at the micro level: Targeted sanctions will impact pockets of the corporate world, including through trade diversion. More importantly, developments with intellectual property protection and related security issues (think of the Huawei case) will impact productivity and relative competitiveness trends for both corporations and countries for decades to come. We will all need to pay closer attention to this as we calibrate our exposure to countries, sectors and individual corporations. In sum, bottom-up fundamental research combined with active portfolio management has never been more important.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

This information is intended for US residents only.

Important Legal Information

All investments involve risks, including possible loss of principal.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. Factual statements are taken from sources considered reliable but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

1. Source: McKinsey Global Institute, “Globalization in transition,” January 2019.

2. Unlike the October WEO, here only the subtitle in the relevant chart notes these are percentage point changes from the baseline. The April charts show global GDP about 0.2% below the baseline.

© Franklin Templeton Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits