Brexit negotiations are once again going to the wire. With no resolution in place and the clock ticking down, Sandy Nairn, chairman of Templeton Global Equity Group and CEO of Edinburgh Partners, looks at the possible outcomes. He explains why he thinks a long Brexit extension could be the most sensible option, and why he feels the deadlock might only be broken by a fresh plebiscite.

As the continuing turmoil over Brexit has amply demonstrated, illogical outcomes are entirely possible when you have competing interest groups with entrenched views on vital elements of the negotiation.

This fragmentation explains the inability of UK members of parliament (MPs) to reach a majority view on any individual Brexit solution. It also amplifies the looming danger of a default to the one outcome—“no-deal exit”—that the overwhelming majority of MPs wish to avoid.

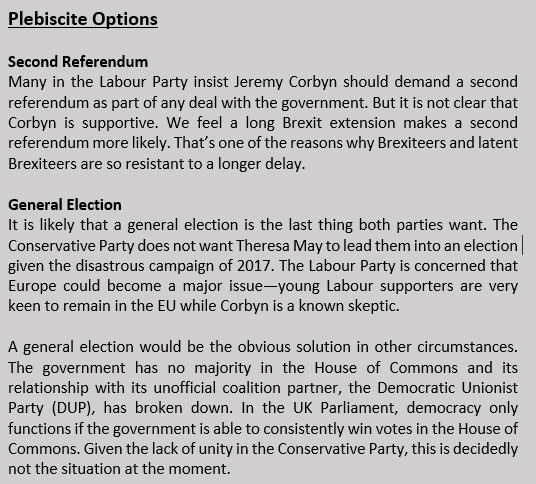

As a consequence, we think, it is highly likely that some form of plebiscite or new vote will be required to break the deadlock.

The simplest, in our view, would be the so-called “people’s vote,” in which voters decide between the competing options. An alternative would be a general election, which would open up a host of other considerations.

In either of these cases, we regard an extended delay to Brexit as almost inevitable.

A Delay, but for How Long?

UK Prime Minister Theresa May has made an official request to extend Article 50 until June 30. We’re skeptical that the EU leaders would countenance such a short delay unless they were convinced agreement on a deal was pending.

On the other hand, various parties, including President of the European Council Donald Tusk, German Chancellor Angela Merkel and the Irish government, appear strongly in favor of offering the UK a long extension.

France’s President Emmanuel Macron appears less keen—partly because of concerns over the disruption that anti-EU populist parties might cause in the upcoming European Parliament election, and partly because he sees significant upside for Paris from a potential shift in financial services from London.

Media speculation suggests other countries such as the Netherlands would like to see the United Kingdom remain in the EU but are frustrated by how the negotiations have been conducted and are therefore not taking a public position.

We think the EU would be comfortable granting an extension as long as it is seen as being more than simply a continuation of what has gone before. Therefore, it requires some kind of political process to a conclusion or a potential conclusion.

Understandably, the EU is very anxious to avoid being blamed for a hard Brexit. But it also wants to ensure the issue doesn’t drag on indefinitely.

The purpose of a long extension should be to work out the type of “soft Brexit” that parliament can agree on, we believe.

So what are those soft Brexit options?

Customs union appears to be the most likely option. Brexiteers object to this on the grounds they believe a customs union would prevent the UK from signing new trade deals.

This is an oversimplification, in our view. Turkey is in a customs union with the EU and has many trade deals with third countries—indeed it is negotiating a deal with China currently.

A customs union requires a country to charge the same external tariff on goods—other important features of trade deals such as product standards, intellectual property (IP) protection, investor protection and services are not restricted.

An extension could also be used to open a dialogue with members of the European Free Trade Association (EFTA) and the European Economic Area (EEA) to discuss whether they would consider the UK joining.

The United Kingdom is currently discussing these as potential options but in our view, they are only feasible if the members of these groups are willing to accept the UK. Moreover, discussion thus far has been superficial and a national debate on the merits of the different options should precede any application to join either organization. Again, we think this would naturally end with a second referendum to confirm the decision.

European Parliamentary Election Concerns

EU member states are very concerned about the impact of the UK participating in European parliamentary elections while en route to an exit.

Although the lawyers for the EU have concluded that the European Parliament would still be entitled to sit even if the UK doesn’t participate in the elections, the European authorities want to avoid a situation in the future in which another member state could hold the European Parliament to ransom by using non-participation in elections as leverage.

There are further complicating considerations: the UK’s seats in the European Parliament have already been reallocated to those member states (Germany, France, Spain) that are proportionately under-represented. The law does provide for a reversal of the reallocation of UK seats but this has to happen by the week of April 15. That was the driving factor behind the EU’s initial imposition of the April 12 deadline.

Other Possible Outcomes

Throughout the entire Brexit process, the one constant has been the uncertainty of outcome.

Even though the UK government has requested a further Brexit delay, there remain a number of possible outcomes that could resolve Brexit over the coming days.

- Parliament Approves a Deal Before April 12

There is still a very slim possibility that the House of Commons could approve a withdrawal deal before April 12. May has been forced by the lack of support from her own party to reach out to the leader of the opposition Labour Party.

However, we think the probability of a solution emerging from these talks is low given the reticence of the Labour Party to be seen as part of the problem. It may be in the interests of the Conservative Party to spread the blame across the whole political spectrum but for many in the Labour negotiating team this would be anathema.

In our view, the talks are therefore unlikely to produce an outcome. They could, however, lead to a process for deciding the best alternative—a type of alternative votes endorsed by the government. Mrs. May potentially believes she can get her deal through with some small additions to buy Labour votes—this is unlikely to work.

A no-deal exit could still happen by accident. There are well-founded rumors that 17 members of the cabinet are actively pushing for the UK to leave without a deal. It is known that 188 Tory MPs voted for such an outcome at the last round of indicative votes.

The importance of factional politics is emphasized when the majority of the Conservative Party and a proportion of the cabinet support “no deal” against the backdrop of resistance from the Bank of England, key UK and multinational companies, the Confederation of British Industry (CBI) and several trade unions.

Where Does All This Leave Us?

A no-deal exit could still happen but it would be by dint of a combination of mistakes rather than as a policy goal for the majority of parliament.

In our view, a long extension is most likely given the low probability of a solution emerging in the near term that would be acceptable to the EU.

A long extension raises the likelihood of a second referendum to confirm or repudiate whatever solution emerges. Assuming the referendum question was for the agreed leaving terms or remain, we believe there would be a degree of market relief. Currently, the polls suggest “remain” would win but one should not ascribe that too much importance at such a febrile time.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Current political uncertainty surrounding the European Union (EU) and the financial instability of some countries in the EU may increase market volatility and the economic risk of investing in companies in Europe.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Alternative Investments Topics >