Once upon a time, US municipal bonds were generally considered less risky than corporate bonds. Backed by the full faith and credit of state governments, investors had confidence they would receive their principal plus interest without fail. Times have changed. For some states and local governments, decades of financial mismanagement and massive pension liabilities are threatening to upend the full faith and credit pledge. In this article, Franklin Templeton Fixed Income takes a look at the situation, with Illinois being an example of a particularly dire case.

As municipal bond analysts, assessing pension risks hinges partly on the willingness of elected officials to implement tangible pension reforms. Absent that, large pension obligations can significantly degrade budgets, credit quality and eventually impair bondholders.

Here’s the good news: after excluding some local bond exposures, like Chicago’s, that still leaves well over 85% of the general municipal market available for investment. In some instances, we think essential-service revenue bonds offer more stability than general obligation bonds.

A Global Challenge that Feels Very Local

If there’s one issue where frictions between budget reforms and politics burn brightest, it’s pensions. With the proportion of retired pensioners and lifespans increasing across the globe, many governments face a challenging dilemma: how to raise enough tax revenues from the young to pay for the pensions promised to the retired? It’s a vexing issue that impacts our firm’s sovereign bond research as much as it does our municipal bond analysis.

Consider Brazil, for example. Pension liabilities currently absorb a third of Brazil’s federal tax receipts and fuels chronic deficits. Transitioning to a sustainable glidepath means Brazil’s new president, Jair Bolsonaro, must pass sweeping reforms that require changing Brazil’s constitution. Even if the reforms make it through congress this year, there’s nothing stopping a future president from reversing them.

Case in point: Italy. After passing reforms in 2011—increasing the retirement age to 67, shifting more workers to defined contribution schemes, and stopping inflation indexing of pensions above a certain income level— Italians elected a new government in 2018 that promised to overturn them.

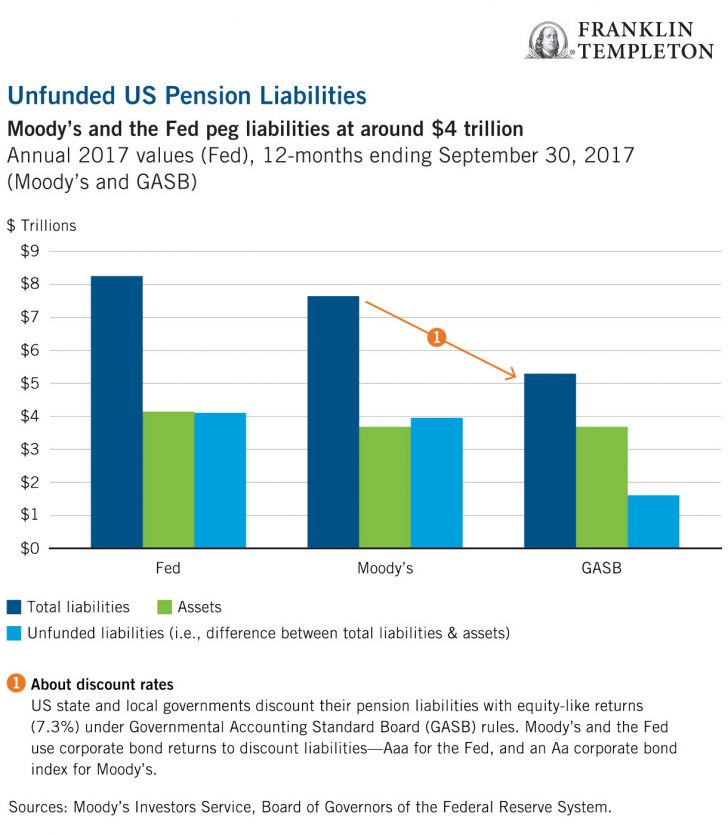

In the United States, unfunded pension liabilities loom particularly large at the state and local level, making them a key focus for our municipal analysis. The scale of the liabilities is unnerving.

In August of last year, Moody’s reported that adjusted net pension liabilities across US states spiked to $1.6 trillion in fiscal 2017—increasing 25.5% from the prior year and representing 147.4% of state revenues.1 When Moody’s and the US Federal Reserve add up unfunded pension liabilities across state and local US governments they total around $4 trillion.2

Pension liabilities didn’t rattle US municipal bond markets much before the financial crisis a decade ago. General obligation bonds, after all, are senior in the capital structure and backed by the full faith and credit of state and local governments. Even when major cities faced insolvency—New York City in the 1970s, Cleveland in the 1980s, and Philadelphia in the 1990s—filing for bankruptcy and impairing bondholders was taboo. In these three cases, each city’s state stepped in to ensure all obligations were paid; either by creating a financial bail-out vehicle or by installing a state-controlled board to oversee local finances.

That practice changed after the financial crisis. For cities like Chicago, decades of chronic pension underfunding and unsustainable benefit enhancements had grown silently into giant and toxic pension liabilities. Faced with unescapable budget shortfalls—set in motion by long-retired predecessors—several cities filed for bankruptcy, including Detroit, Michigan in 2013.

In some cases, pensioners received preferential treatment over bondholders. Most Detroit bondholders, for example, eventually recovered 14–74 cents on the dollar after the bankruptcy, whereas pensioners recovered 95 cents per dollar. The new reality is this: pension obligations may hold a senior position to a bond’s full faith and credit pledge.

Bankruptcies and defaults are still rare overall, thankfully. In today’s political climate, however, we’ve seen cities and policy advocacy groups threaten bankruptcy to wring more funding from state governments; or utilize bankruptcy filings to restructure their debt, renegotiate union contracts and reform pensions.3

As municipal bond analysts, our main question now is not just whether a city or state is able to pay their debts (we do the math), but this: are politicians willing to impair bondholders in order to honor their predecessor’s pledge to pensioners? Willingness to enact meaningful pension reforms is harder to analyze than the mathematical ability to pay debts.

Chicago’s Pension Beast

Consider Chicago, Illinois. In 2015, Chicago became the only major metropolitan US city outside Detroit to receive a junk rating from the Moody’s bond rating agency, largely because of its escalating pension bills.

Chicago’s then-mayor Rahm Emanuel promptly fired Moody’s from rating the city’s new bond issues and castigated them in the press. The mayor publicly attacked Moody’s again in 2017 during a run-up to a $1.2 billion bond sale, over frustrations his city had to pay higher interest rates.4

We’re interested to see how Chicago’s new mayor, Lori Lightfoot, responds to rating agencies like Standard & Poor’s—particularly if they drop Chicago below investment grade because of pension challenges as Moody’s did. Lightfoot spoke bluntly about the city’s pension dilemma during her campaign. The situation is indeed dire. The city’s four pensions are about $28 billion short of being fully funded.

By state law, Chicago must produce an additional $1 billion in revenues annually starting in 2023 to feed the beast—an enormous increase for an already strained budget. It’s also a heavy burden for a tax base of Illinois voters already reeling from (and moving away from) recent Chicago property tax increases to pay for these pensions.

State Constitutions

Chicago proves just how challenging large pension liabilities can be. The risks, however, vary significantly across the United States. Since the financial crisis, 74% of state pensions and 57% of local government plans have taken positive actions by either reducing pension benefits and/or increasing contributions.5

A common reform involves reducing cost-of-living adjustments (COLA), which shrinks future liabilities and frees up money to service debt obligations. The Colorado state legislature, for example, capped COLAs at 1.5% last year, and increased state and employee pension contributions.

Cutting pension benefits is dicey for politicians who fear voter backlash. It’s especially challenging for states that legally shield their pensions from reforms. Illinois’ state constitution, for example, says existing pension benefits “shall not be diminished or impaired”—effectively ruling out solutions like COLA adjustments unless the legislature amends the constitution. That presents Illinois’ governor with a big challenge: absent amending the constitution to reduce pension benefits, the governor must raise substantial new revenues in order to feed the $250 billion of unfunded pension liabilities (the largest of any US state).

Drowning in Liabilities

The bond market is aware of pension shortfalls in states like Illinois ($250 billion), Connecticut ($71 billion) and New Jersey ($116 billion), and prices in that risk through higher spreads.6 Our analysis shows Illinois’ bondholders (and Chicago bond holders, for that matter) are in a uniquely dangerous situation the market isn’t fully pricing.

Illinois’ pension payments are mandated by state law to grow annually—rising 10%, for example, to $9.14 billion in 2020. Illinois is already struggling to keep its head above water to meet this year’s pension payment, let alone successively larger ones over the next 30 years. Here’s the real kicker: for as large and painful as these payments are, they still aren’t big enough to stop Illinois’ pension liabilities from growing even larger—something ratings agencies call negative amortization. That means Illinois’ pensions (a fire-breathing monster that dwarfs Illinois’ revenue-generating capacity) will still be at risk for insolvency if we head into a recession or have a market downturn.

Illinois bond ratings are already skating just one notch above “junk” status. If Illinois gets downgraded, the pain could be sharp.

The Illinois Exodus

In our view, the writing on the wall lies with Illinois’ collapsing population. According to the US Census Bureau, Illinois saw the second biggest drop in residents in 2018 after New York, losing 45,116 residents. Since 2013, over half a million Illinois residents have left the state seeking lower taxes, nicer weather and better economic opportunities across the US.7 From a revenue perspective, many of the people leaving are of working age while the population left behind is aging, according to the Northern Illinois University’s Center for Governmental Studies.

Chicago’s taxpayers face an especially onerous dilemma having two pension beasts to slay at once. They’ve seen record property tax increases to help pay for (but not resolve) the city’s pension crisis, and now face a state income tax hike to forestall (but not resolve) the state’s pension emergency.

Will Illinois’ governor and Chicago’s mayor eventually impair bondholders rather than push for sensible pension reforms? We think it’s more likely than not, unfortunately. Neither has been willing to broach the subject of reforms, focusing mostly on new taxes or selling off capital assets like land, buildings and infrastructure. When we add up the projected revenues, the math still doesn’t work. It’s for this reason that we have not and will not own uninsured general obligations of the State of Illinois, or bonds from the City of Chicago and Chicago Public Schools.

This doesn’t rule out investing in Illinois entirely, however. Essential-service revenue bonds—which finance income-producing projects such as toll roads and airports—help eliminate questions about willingness to pay. The returns these bonds generate come from the usage fees these services charge, which are specifically assigned to pay debt service. The bonds aren’t backed by a full faith and credit pledge, but issuers can increase user rates if the dedicated revenue stream falls short.

In past bankruptcy cases, revenue bonds proved to have stronger protections than some general obligation bonds. Is there something that could change our minds about Illinois’ pension dilemma? Yes—a willingness of elected politicians to educate the public on the true scope of the situation and enact sensible pension reforms.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in lower-rated bonds include higher risk of default and loss of principal. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Municipal bonds are debt securities issued by state and local governments and are generally exempt from federal income tax and also from state and local taxes for residents in the state where the bond was issued. They typically offer income, rather than capital appreciation potential. Corporate bonds are issued by corporations. Bonds with lower ratings and higher credit risk (risk of default) typically offer higher interest rates to compensate investors for the higher risk associated with the investment.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Source: Moody’s Investors Service, “Medians – Adjusted net pension liabilities spike in advance of moderate declines,” August 27, 2018.

2. Source: Moody’s Investors Service, “Federal Reserve revision pushes unfunded pension liabilities to more than $4 trillion,” September 26, 2018.

3. Source: T. Dabrowski and J. Klinger, “Pensions 101: Understanding Illinois’ massive, government-worker pension crisis,” Illinois Policy Institute, February 3, 2016.

4. Source: J. Holman, “Chicago Mayor Pushes Moody’s to Rescind City’s Junk-Bond Rating” Bloomberg, January 11, 2017.

5. Source: J. Aubry and C. Crawford, “State and Local Pension Reform Since the Financial Crisis,” Series on State & Local Pensions, no. 54. Boston: Center for Retirement Research at Boston College, January 2017.

6. Source: Moody’s Investors Service “Medians – Adjusted net pension liabilities spike in advance of moderate declines,”August 27, 2018

7. Source: Moody’s Investors Service “Illinois (State of): Pensions, taxes, out-migration top list of credit issues facing new governor,” February 5, 2019.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments