Macro Factors and Their Impact on Monetary Policy, the Economy, and Financial Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFrom Trade War to Cold War

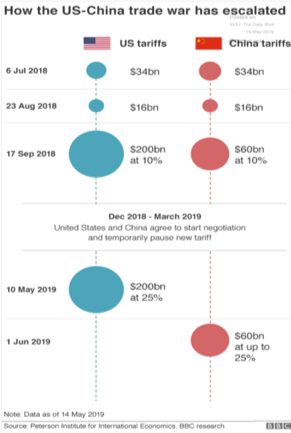

The expectation of a global rebound in the second half of 2019 was predicated on a positive resolution in the trade talks between the U.S. and China and the U.S. and the European Union. With a burst of stimulus from the Peoples Bank of China and Chinese fiscal stimulus since last summer, the global economy was beginning to show signs of improvement. A positive outcome on trade was likely to engender a pick-up in business investment in the U.S. and globally, as the uncertainty of the trade issue was removed. With solid job growth, the highest wage growth in ten years, and Consumer Confidence near 20 year highs, a trade deal would have provided a boost that was likely to lift core inflation above 2.0% and drive the unemployment rate lower. This outcome would have eliminated any chance the Federal Reserve would lower rates before the end of 2019 and potentially raise the specter of an increase. Since the majority of markets participants were expecting the Fed to lower rates, the prospect of an increase would have caught investors off balance. Much has changed since May 5 when President Trump indicated tariffs would increase form 10%to 25% on May 10. As I noted in a bit of understatement in the May 3 Macro Tides, “Should negotiations collapse with either China or the EU the outlook for the second half of 2019 would be negatively altered.”

During the Cold War between Russia and the U.S. the concept of mutually assured destruction established an uneasy balance since a full-scale use of nuclear weapons would cause the complete annihilation of both the attacker and the defender. In October 1962 the MAD doctrine was tested as the U.S. and Russia went toe-to-toe after Russia placed ballistic missiles in Cuba. After 13 days of intense negotiations Russia agreed to remove its missiles, if the U.S. removed its missiles from Turkey. For Baby Boomers born in the years after the end of World War II, the Cuban missile crisis was a point of passage as noted by Billy Joel in his song ‘Leningrad’.

A full-blown trade war between the two largest economies in the is an economic version of MAD, which is why it was assumed that a trade deal had to occur. Throughout history the folly of man has provided many examples of self inflicted suffering on a scale seemed unimaginable prior to the cascading of events. Whether the current Trade War will morph into a lasting Cold War will be determined by the willingness of China to make adjustments after 20 years of using almost any means to achieve growth.

President Clinton was supportive and an advocate for allowing China to join the World Trade Organization (WTO) in 2001 believing China would be become a more open society and allow greater freedom for its people. “By joining the WTO, China is not simply agreeing to import more of our products it is agreeing to import one of democracy’s most cherished values, economic freedom. When individuals have the power not just to dream, but to realize their dreams, they will demand a greater say.” The growth of the internet, in particular, Mr. Clinton argued would undermine Beijing’s control and make China more like the U.S. China did not open up politically. Beijing tamed the internet by limiting its use to commerce, technology and social media. It blocked political organizing by threatening and sometimes jailing those who posted critical comments. In an Orwellian twist China has in recent years turned the internet into an instrument of the state by using it to identify and track dissidents.

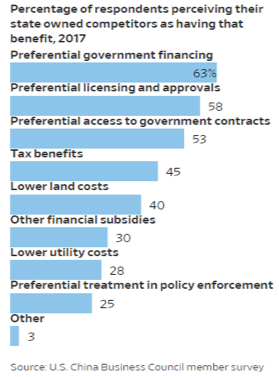

As part of joining the WTO China promised to curb the power of China’s state-owned enterprises (SOEs) allow the Chinese private sector to grow, and increase access to the Chinese market by foreign companies. On the surface this did occur as the share of GDP from SOEs fell from 50% in 2001 to 25% in 2016. However, more than 80% of SOEs are now concentrated in vital or high-profit industries such as finance, power, energy, telecommunications, and defense. Thanks to easy loans and unfettered access to government funding and assistance, these giants have been able to amass assets in areas where their private and foreign partners were either restricted or found hard to compete. In the past few years, investment in the SOEs has grown three times faster than private investment, so SOEs have once again become the heart of Chinese economic policy-making. Since 2013, SOEs have received more than 60% of all new loans in China each year, and 78% in 2016. As a result the 100 centrally administered SOEs have grown much bigger. By 2017, the assets of these enterprises had reached $10.4 trillion, up more than tenfold from 2003. According to official Chinese estimates, centrally administered SOEs will account for over 70% of the total value of infrastructure projects in the ‘Belt and Road Initiative’. China has not followed through on many of the promises it made when it joined the WTO.

President Xi Jinping announced China’s ‘Made in China 2025’ in 2015, which is the plan to update China’s manufacturing base by rapidly developing high-tech industries by 2025. Electric cars, next-generation information technology and telecommunications, advanced robotics, and artificial intelligence are the core of the plan. These sectors are central to the so-called fourth industrial revolution, which refers to the integration of big data, cloud computing, and other emerging technologies into global manufacturing supply chains. China accounts for about 60% of global demand for semiconductors, but only produces some 13% of global supply. Made in China 2025 set specific targets. By 2025, China aims to achieve 70% self-sufficiency in high-tech industries, and by 2049, China seeks a dominant position in global markets, which just happens to be the 100th anniversary of the People’s Republic of China as a communist nation.

China’s ‘Made in China’ 2025 has raised protests from U.S. companies that find that they are often competing with the Chinese state, rather than individual Chinese companies. China provides low cost funding through State Owned Banks to Chinese companies so their cost of capital is far lower. In solar and wind power, Chinese over-investment created a global glut that drove prices down and many foreign companies out of business. Like all WTO members China is supposed to publish all of its subsidies so that others can respond to them. China often circumvents this rule because many subsidies come from state-owned enterprises rather than the government directly, and take the form of low-cost loans, raw materials, and cheap land. As required by WTO rules China promised to open up its markets to foreign investment in return for entry into the U.S., Europe, and the other 152 trading partners within the WTO. While China has enjoyed almost unfettered access to the markets of WTO members, China has limited access to its market through various barriers. Companies based in the United States, Europe, and elsewhere complain of an asymmetry in which China is free to invest in foreign companies, but foreign companies selling to and operating in China are highly constrained by investment requirements and other regulations.

Companies that have gained entry into China have encountered other problems. Foreign companies report they are routinely compelled to transfer technology to Chinese companies to do business there, in violation of Beijing’s WTO commitments. China’s discriminatory licensing treatment and its failure to better police the theft of foreign intellectual property violates its obligations under the WTO’s side agreement on intellectual property. According to a July 2018 survey by the American Chamber of Commerce in Shanghai, about one in five companies say that they’ve been pressured to transfer their technology. China has also directed the systematic investment and acquisition of foreign companies by Chinese firms to obtain cutting-edge technologies and intellectual property to facilitate the transfer of technology to Chinese companies. The Pentagon warned in 2017 that state-led Chinese investment in U.S. firms working on facial-recognition software, 3-D printing, virtual reality systems, and autonomous vehicles is a threat because such products have “blurred the lines” between civilian and military technologies. In April 2018, U.S. intelligence agencies said that Chinese recruitment of foreign scientists, its theft of U.S. intellectual property, and its targeted acquisitions of U.S. firms constituted an “unprecedented threat” to the U.S. industrial base.

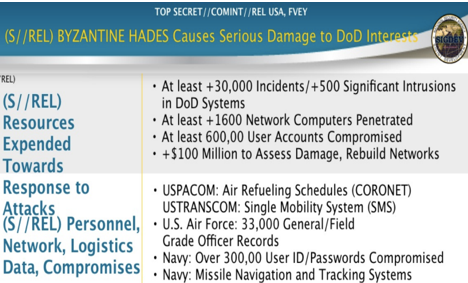

China conducts and supports the theft from the computer networks of foreign companies to acquire intellectual property and trade secrets. In January 2015 the German magazine Der Spiegel published an analysis by the National Security Agency (NSA) detailing how cyber spying was carried out by a Chinese military unit called the Technical Reconnaissance Bureau. According to the NSA the Chinese were able to obtain more than 50 terabytes of data from U.S. defense and government networks "the equivalent of five Libraries of Congress”. The NSA estimated in the Top Secret briefing slide that the Chinese had conducted more than 30,000 cyber attacks as part of their massive defense industrial espionage, and that more than 500 attacks were "significant intrusions in Department of Defense systems." More than 1,600 network computers were penetrated and at least 600,000 user accounts were compromised. In all, the NSA concluded that the Chinese compromised key weapons systems including the F-35, the B-2 bomber, the F-22 fighter-bomber, the Space Based Laser, and other systems. By learning the secrets, the Chinese were able to include the design and technology in Beijing’s new stealth jet, the J-20. The stolen data could allow Chinese air defenses to target the F-35 in a future conflict. Chinese Foreign Ministry spokesman Hong Lei dismissed the documents’ disclosures that China stole F-35 secrets. Hong told reporters on January 19, 2015, "The so-called evidence that has been used to launch groundless accusations against China is completely unjustified."

In 2015 President Obama and Chinese President Xi Jinping signed an agreement that called for the U.S. and China to refrain from cyber attacks that steal intellectual property for commercial gain. In February 2018 Adm. Mike Rogers, the director of the National Security Agency, testified before the Senate Armed Services Committee and noted that China had not adhered to the agreement and was in violation of established international norms. "Subsequent evidence, however, suggests that hackers based in China sustained cyber espionage that exploited the business secrets and intellectual property of American businesses, universities, and defense industries.” It was the first time a senior military or intelligence official confirmed China had failed to adhere to the 2015 agreement the Obama administration touted as halting Chinese cyber attacks.

Based on speeches and Tweets by President Trump the initial trade negotiations with China seemed focused on narrowing the annual $500 billion trade surplus with the U.S. As the talks intensified and evolved it became clear that the U.S.’s strategic aim was addressing China’s failure to fulfill the responsibilities it assumed when China became a member of the World Trade Organization and the promises it has made to the U.S. to curtail its cyber espionage and corporate theft of intellectual property. For the U.S. these issues outweigh the annual trade balance with China since they require fundamental changes in how China has manufactured its growth. President Trump has effectively drawn a red line and told China that it must alter the way it has be doing business not just with the U.S. but with the European Union, Japan, and the rest of the world, since China has used the same tactics against every industrial power.

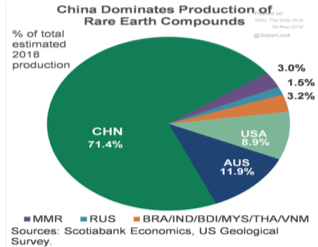

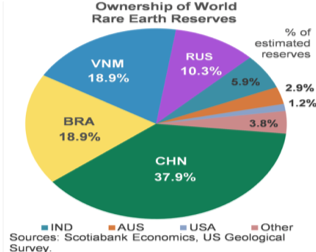

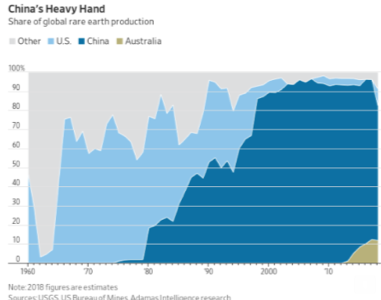

The hardliners within China have a different perspective. The hardliners set a course for China years ago to reestablish China as the dominant nation in the world by 2049 which holds great symbolism for China. The People’s Republic of China was founded as a communist nation in 1949 so 2049 is the 100th anniversary. China has become the second largest economy and integrated within the global economy to successfully resist any pressure to change. In a country that reveres the concept of saving face the hardliners believe no country has the right to tell China what it can or can’t do. This is why the trade negotiations broke down and why there has been an increase in state sponsored nationalism against the U.S. The People's Daily is the biggest newspaper group in China and an official newspaper of the Central Committee of the Communist Party of China. On May 29 an editorial in the People's Daily warned the U.S. not to underestimate China’s capacity to fight a trade war and used a specific phrase to emphasize the point. The phrase means “Don’t say I didn’t warn you.” This phrase was used in 1962 before China went to war with India and in 1979 before hostilities between China and Viet Nam began. The editor-in-chief of the People’s Daily Tweeted that China is seriously considering restricting rare earth exports to the U.S. China Central Television (CCTV) is the predominant state television broadcaster in Mainland China. During an interview on CCTV on May 29 an official at the National Development & Reform Commission stated that the Chinese people won’t be happy to see products made with exported rare earths being used to suppress China’s development. The expression of these views follows a visit by President Xi to a rare earth plant in Jiangxi province on May 20. China produces more than 70% of the world’s rare earths so it the largest producer by far. China supplies about 80% of U.S. imports of rare earths, which are used in smart phones, electric vehicles, and wind turbines. In the short term the cessation of Chinese exports of rare earths could become a choke hold, but longer term not so much. In December 2017 President Trump signed an executive order to reduce the U.S.’s dependence on external sources of critical minerals, including rare earths, which was aimed at reducing U.S. vulnerability to supply disruptions. Rare earths aren’t particularly rare. Cerium, the most abundant, is more common in the Earth’s crust than copper. According to the U.S. Geological Survey, all other rare-earth elements, besides promethium, can be found more widely than silver, gold, or platinum. If China does restrict exports of rare earths, production facilities will be built elsewhere to minimize the U.S.’s dependence on China.

The increase in anti-U.S. rhetoric in China and pointed threats regarding rare earths suggest the hardliners within China are laying the groundwork for an extended impasse that is likely to include a further escalation. China understands the political process in the U.S. and may expect sentiment against the tariffs to increase which would further their agenda. China has aimed its tariffs at U.S. farmers who voted for Trump but whose support may waiver if no progress is achieved. No doubt that hardliners in China have tuned into CNN and listened to the constant anti-Trump drumbeat and the increasing likelihood that the Democrats will pursue impeachment.

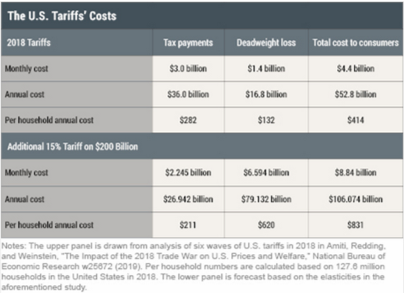

On May 22 the New York Federal Reserve published research that estimated the 25% tariff on $200 billion of Chinese imports on May 10 will cost the average U.S. household $211 a year from the tariffs, and an additional $620 in ‘deadweight costs”. Deadweight costs occur from companies shifting from producers in China to producers in other countries whose products are more expensive, although cheaper than products from China after the 25% tariff is factored in. The hardliners in China must be aware that the media in the U.S. is on balance critical of many of President Trump’s policies and the media are likely to use the New York Fed’s research to emphasize the downside of President Trump’s trade war with China. I have listened to a number of reports from mainstream TV news that have featured interviews with U.S. farmers and consumers buying products affected by the tariffs (higher cost), without any mention of China’s habit of stealing intellectual property and military secrets, or the strategic long term value of confronting China on these issues. I suspect that many reporters don’t understand their importance. By ratcheting up anti-U.S. sentiment in China and postponing trade talks with the U.S., the hardliners in China may be calculating that public support within the U.S. will decline and thus pressure President Trump to accept a trade deal that doesn’t require any fundamental changes by China.

After China communicated on May 9 its unwillingness to base future discussions on curbing the theft of intellectual property, the use of cyber attacks, and lowering restrictions to access the Chinese markets, President Trump imposed additional tariffs on May 10. Rather than accepting a scaled down trade deal centered on narrowing the trade deficit with China, President Trump has conveyed his willingness to hold fast and accept the short term negative impact on GDP growth and the stock market to achieve the more important long term goal of reining in China’s penchant for operating outside of signed agreements. Neither China or President Trump seem willing to blink which suggests there will be a further escalation before talks are likely to resume. In 1962 the United States and Russia went to the brink of a nuclear war before negotiating a settlement that gave both sides a ‘win’. There is a good chance a similar trajectory will develop in coming months before the U.S. and China can agree on a deal. Mutually Assured Destruction has been replaced by Mutually Assured Disruption

Global Economy

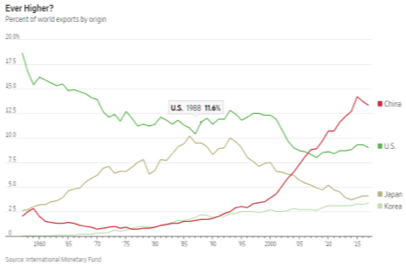

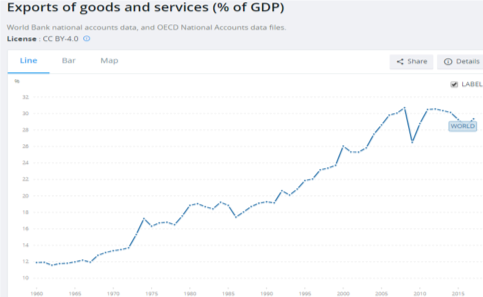

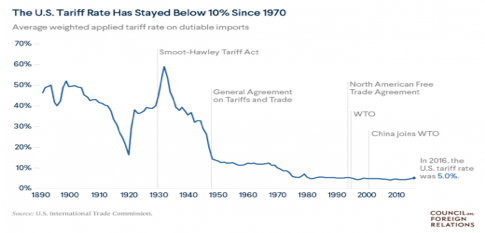

Trade has been one of the primary drivers in global GDP growth during the past 55 years. Exports as a percent of global GDP were 12.0% in 1965 and by the end of 2017 were up almost 150% and represented 29.3% of global GDP. This growth was made possible by the reduction of tariffs and trade barriers that originated with the establishment of the General Agreement on Tariffs and Trade (GATT) in January 1948 and supported by 23 countries. In 1947 the average tariff level for these 23 countries was about 22% and subsequently fell to 8.5% in 1994. The World Trade Organization was the negotiated successor to GATT and was launched in 1995 with 123 countries participating. The increase in global trade led to further reductions in tariffs, which by the end of 2017 had fallen to 2.59% according to the World Bank. The increase in global trade and the globalization of supply chains during the past 20 years raised more than a billion people out of extreme poverty worldwide. This positive outcome also came with the unintended consequence of millions of good paying jobs that were lost as production factories were closed in the U.S. President Trump’s imposition of tariffs is intended to roll back a portion of the negative impact from globalization. His effort will also produce unintended consequences that are and will continue to weigh on global growth and slow growth in the U.S. as well.

The Smoot-Hawley Tariff Act was passed in June 1930 and increased the average tariff from 17% to 60% and ignited a wave of protectionism around the world. The Tariff War in the 1930’s resulted in a 60% decline in global exports contributing to the Great Depression. A full blown trade war has not started but is the direction we’re heading.

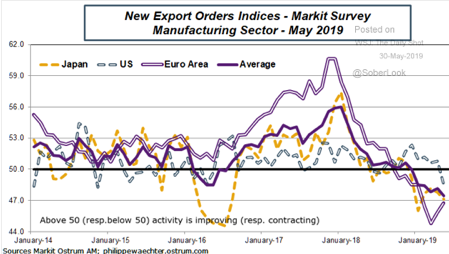

The current Trade War and tariff battle has already had a pronounced impact on trade as measured by the average Markit ISM Surveys for New Export Orders, which has plunged from 60 in January 2018 to under 47 in the May 2019 surveys. The uncertainty surrounding trade has caused business investment in the U.S. and around the world to slow markedly which has weighed on global growth. These factors led the Organization for Economic Cooperation and Development (OECD) to reduce its 2019 global GDP estimate to 3.2% from 3.2% which would be down from 3.5% in 2017 and 3.7% in 2017.

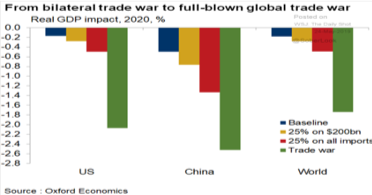

According to analysis by Oxford Economics the recent increase to 25% on $200 billion of imports from China will have a modest impact on GDP growth in 2020 in the U.S. (-0.3%), China (-0.8%), and the global economy (-0.2%). Should President Trump apply a 25% tariff on all of the imports from China the impact will almost double and become a far larger drag on growth. The real risk in these estimates is that they prove optimistic since humans often react differently than any model can forecast. The estimates do not include the new tariffs President Trump levied on Mexico on May 31. In the unlikely event that a full blown Trade War develops, the odds of a recession would increase significantly in the U.S., while growth in China and the global economy would take a big hit.

U.S. Economy

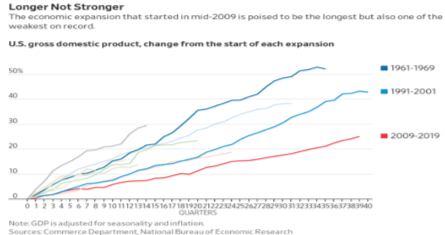

In July the U.S. economy will set a record for the longest economic expansion in U.S. history at 121 months. However, it has been one of the weakest recoveries, as measured by the cumulative growth in GDP. The recovery that began in June 2009 has been half as strong compared to the 1961 – 1969 expansion and 60% as strong as the 1990’s expansion that ended in 2001.

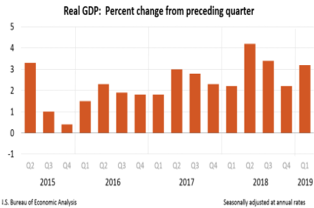

The Commerce Department revised its estimate of GDP growth in the first quarter of 2019 from 3.2% to 3.1%. Although that sounds good one must understand that inventory building and an increase in exports and fall in imports contributed 1.6% or half of Q1 GDP. After calculating Nominal GDP the Commerce Department subtracts its estimate of inflation to arrive at Real GDP which is the number that garners the headlines. After clocking in at 1.5% in the fourth quarter, the GDP deflator fell to 0.6%, which lifted Real GDP by 0.9%. There is a high degree of volatility in the quarterly swings in inventories and trade which is why looking at Final Sales can provide a clearer assessment of the economy’s health. Since peaking at 4.0% in the second quarter of 2018, Final Sales have progressively weakened and grew just 1.3% in the first quarter.

The second quarter might get a lift from inventory building by the auto manufacturers rushing to get parts prior to tariffs on Mexico, which are projected to increase from 5% on June 10 to 10% on July 1. That may offset some of the likely drop in inventories, after the big build up in the first quarter. The 1.0% gain from trade in Q1 is likely to reverse in the second quarter, and the GDP deflator can be expected to rebound from Q1’s low level of 0.5%. It is likely that GDP growth in the second quarter could be noticeably less than 2.0% when the first estimate is published near the end of July. The headline could intensify concerns about the speed of the slowdown from the first quarter raising fears of an imminent recession. In reality, the first quarter was not as strong as the 3.1% GDP number implied and the second quarter may not be as weak as the first GDP estimate suggests.

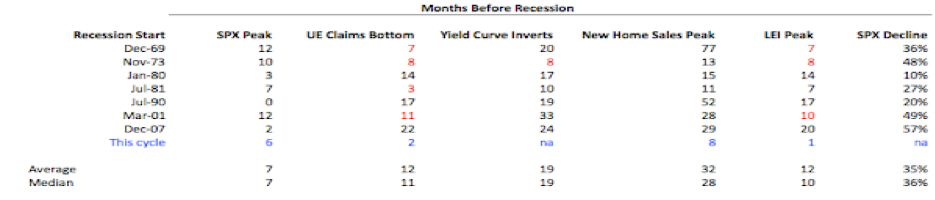

As discussed in the April Macro Tides, the Leading Economic Index (LEI) is superior to inversions in the yield curve in forecasting a recession. In the seven recessions during the past 50 years the median lead time prior to a recession was 10 months for the LEI compared to 19 months after the Yield Curve inverted. The lead time for both may be shortened in the current situation. The U.S. economy is being buffeted by forces (Tariff War) that have not been active since the 1930’s, while Treasury yields in the U.S. are being dragged down by the historic aberrant monetary policy actions of the European Central Bank (ECB) and Bank of Japan (BOJ). Both factors are outside of normal U.S. monetary policy considerations. The uniqueness of the current situation won’t stop jabbering kibbitzers from criticizing the FOMC no matter what decision the FOMC makes.

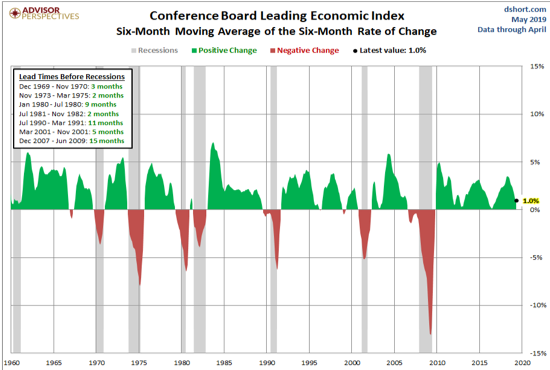

Although we are in uncharted waters a review of what is known is appropriate. The LEI reached its highest level ever in May which suggests a recession may be at least 10 months away since it hasn’t even turned down yet. But since this is uncharted territory and the dynamics of a contraction may quicken if President Trump slaps tariffs on another $300 billion of imports, using a six month rate of change (ROC) on the LEI may be helpful. (Chart compliments Doug Short Advisor Perspectives) The average lead time in the prior recessions falls from 10 months to 6.7 months. There were two false negatives (1966, 1998) and one false positive (1981) so some additional interpretation is required. The six month ROC was still positive in May and will likely remain positive even if the LEI index weakens materially in June. At worse this suggests a recession may be possible in the first quarter of 2020.

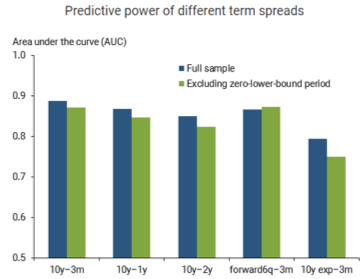

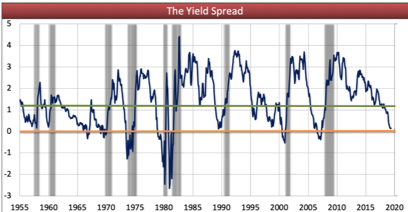

While more attention is focused on the 2-year minus the 10-year Treasury curve, the spread with the best predictive value is the 3-month T-bill minus the 10-year Treasury bond, according to research by the Federal Reserve of San Francisco. The 90-day T-bill yield was 2.36% and the 10-year Treasury yield was 2.14% for the week ending May 31, so this curve was inverted by 0.22%. This is the first time this spread has been negative since August 2007 and just before the FOMC began cutting the federal funds rate in September 2007.

On May 31 the 10-year German bund provided a yield of -0.20%, which is lower than the -0.187% recorded on July 3, 2016. Anyone buying and intending to hold for 10 years is guaranteeing a loss for the next decade. This seems like a competitive form of insanity of doing the same thing but expecting a different outcome. This behavior is encouraged by the ECB whose policy rate is -0.40%. Globally, almost $11 trillion of sovereign bonds are selling with a yield below 0.0%, so the insanity is global. If this seems too stupid to be true it probably isn’t, as the folly of man is expressed in many different ways. It would be difficult to argue that the 234 basis point spread between German and U.S. 10-year yields isn’t exerting downward pressure on Treasury yields. This fact cautions that jumping into a recession is coming soon camp based on the yield curve inversion in the U.S. alone may be premature.

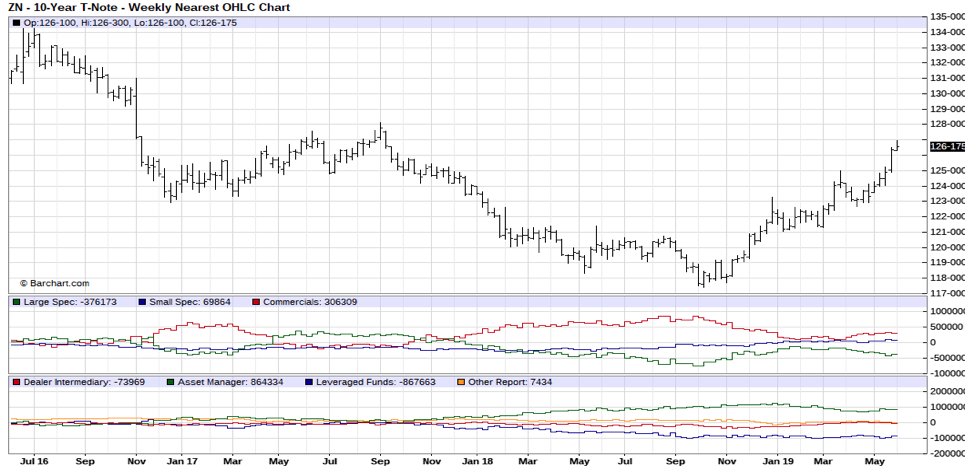

Positioning in Treasury bond futures has also played a role in bringing the 10-year Treasury yield down so much in such a short period of time. Large Speculators are trend followers so they buy (go long) Treasury futures as bond prices are rising, and sell long positions as bond prices fall. If a downtrend lasts long enough Large Speculators will switch from a net long position to a net short position in anticipation of a further decline in bond prices. The activity of Large Speculators is recorded by the green line in the middle panel in the chart above. If you track the trend of the green line with the trend in bond prices, you can see how correlated they are. In October Large Speculators had an enormous short position in 10-year Treasury bonds which was why I expected bond yields to fall as noted in the October 2018 Macro Tides. “The positioning in 10-year Treasury futures shows Large Speculators holding a far larger short position now than in March 2017, after which the 10-year Treasury subsequently fell from 2.62% to 2.03% in September 2017.” As 10-year Treasury bond prices rose from the low in October to early February, Large Speculators reduced their short position by buying futures, which contributed to the price increase. However, as bond prices climbed higher in March and April, rather than trimming the size of the short position as they normally would, Larger Speculators increased their short position. This out-of-character behavior was likely spurred by the expectation that a trade deal would occur.

The large short position was one reason why I expected the Treasury bond ETF (TLT) to rally as noted in the May 6 Weekly Technical Review (WTR) when TLT was trading at $124.00. In the May 13 WTR I explained why TLT could be expected to rally above $130.00 in coming weeks. “The weekly chart suggests TLT may rally above the September 2017 high of $129.56. From the November low of $111.90 TLT moved up $11.96 and an equal rally from the February low of $118.64 would target $130.60. TLT rallied $8.05 from the low in February and an equal rally from the April low of $122.11 would target $130.16.” On June 3 TLT traded up to $132.58 but is likely nearing a high in June as discussed in the May 6 WTR. “From the momentum low in December 2016, TLT rallied until early September 2017 or just over 8 months. A comparable rally in time from the low in Treasury bond prices on October 5 would target mid June for the next high in Treasury bond prices.”

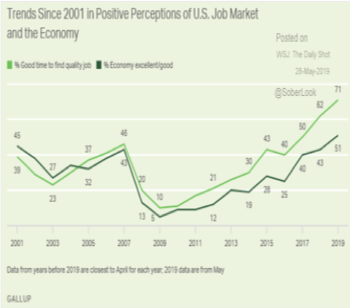

In the short term the U.S. economy may prove resilient and disappoint investors who are expecting the Federal Reserve to cut rates soon. A recent Gallup survey found that the percent of consumers who rate the economy Excellent/Good is the highest in at least the past 20 years. Wage growth is the highest in a decade and job growth is good. Consumer spending comprises 68% of GDP and with confidence high and wage growth strong, spending can be expected to hold up in the near term. Job growth is likely to slow in coming months as companies express their cautiousness by hiring less and further lowering business investment. Some companies most affected by the increase in tariffs may begin to lay off workers, but the majority of employers will wait until they are convinced the slowdown could morph into a contraction. The U3 unemployment rate ticked up to 4.0% in June 2018 and January 2019, and in May it was 3.6%. An increase in coming months above 4.0% would represent a break out and would be a sign that the risk of recession was ramping higher.

Federal Reserve

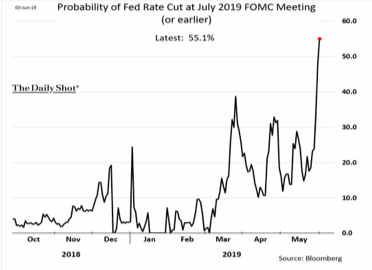

Expectations are rising that the Fed will lower the federal funds rate when the FOMC meets on July 31 based on the inverted yield curve and decline in stock prices. This is being fueled by the perception that the FOMC flip flopped last December when it decided to pause in response to the almost 20% drop in the S&P 500 in the fourth quarter. The misperception of why the FOMC paused may contribute to a miscalculation of how quickly the FOMC will act. The primary reasons why the FOMC hit the pause button are overlooked or underappreciated. The FOMC wanted to lift the federal funds rate in 2018 until it was at a neutral level. After the hike in December the funds rate was certainly in the zip code of neutral. Changes in monetary policy often take 6 to 12 months to affect the economy. After raising the federal funds rate 1.75% from December 2016, the FOMC wanted to wait to learn how much of a drag on growth would result. The boost provided in 2018 from fiscal stimulus was also forecast to wane, which is why the FOMC expected GDP growth to slow from 3.0% in 2018 to 2.3% in 2019. The icing on the cake was the tightening in financial conditions during the fourth quarter as the Dollar rose by 3%, the spread between corporate bonds and Treasury bonds widened, and the S&P 500 fell sharply. To conclude that the FOMC decided to pause largely due to the decline in stock prices reflects a lack of understanding of how the FOMC conducts monetary policy over time.

The FOMC is in a challenging environment since the fundamentals of the U.S. economy are in good shape, but that could change quickly if President Trump continues to ramp up tariffs on China and Mexico in the next few months. The European Union was given a reprieve until November on the 25% tariffs on imports of autos and auto parts. The FOMC has said it would be patient in raising rates and until there is more evidence that the U.S. economy is slowing dramatically, the FOMC is going patient in lowering the federal funds rate. Trade decisions by the U.S. and China in the next few months are going to have a major impact on economic growth. In a fluid situation the members of the FOMC are going to react to events and not act preemptively. If President Trump waits to impose additional tariffs, the FOMC will be more patient than equity and Treasury bond investors expect, which could lead to a reversal lower in bond prices and additional weakness in the stock market. The next FOMC meeting is on June 18-19 and investors will be expecting and hoping that the FOMC provides strong hints that it will be cutting rates sooner rather than later. The FOMC statement and, in his post meeting press conference, Chair Powell will emphasize that the FOMC is data dependent and will respond by lowering rates if warranted. But Powell is also likely to review the current health of the U.S. economy and conclude that it is projected to grow by more than 2% in 2019 based on a healthy labor market and consumer spending. Financial markets will be receptive to the first message but less so to the second more upbeat comments.

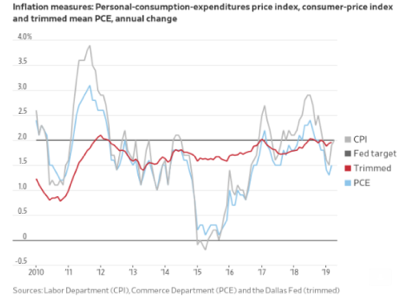

Although the Trade War will dominate monetary discussions for the foreseeable future, members of the FOMC are publically discussing their preference for the Dallas Fed’s Trimmed Mean Inflation Rate (TMIR) over the Personal Consumption Expenditures (PCE) Index. In recent weeks, Fed Chair Powell and Vice Chair Clarida have highlighted the TMIR, as have a number of district presidents, including Rosengren (Boston), Bullard (St. Louis), Kaplan (Dallas), and Williams (New York). Although all 12 Federal Reserve Districts are equal, the New York Fed is first among equals which makes William’s support noteworthy. The TMIR is far more stable than the PCE which probably appeals to members of the FOMC since that limits the risk of overreacting to any extreme move in the short term. It is worth noting that the TMIR is barely below 2.0% while the PCE is closer to 1.6%. As the FOMC waits for more clarity regarding trade and tariffs, the TMIR suggests that inflation is not as low as the PCE and is thus less supportive of a rate cut. If it weren’t for the trade issues, this discussion would be garnering far more attention as it will influence monetary policy decisions in the future.

Jim Welsh

@JimWelshMacro

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits