The US Federal Reserve kept interest rates steady at its June meeting; it emphasized its data-driven approach to policy decisions but noted it believes the case for lower interest rates to be strengthening. Franklin Templeton Fixed Income CIO Sonal Desai offers her take on the meeting, and why the Fed might actually be exacerbating market volatility ahead.

Boxed in by financial markets pricing in 75 basis points (bps) of interest-rate cuts this year, Federal Reserve (Fed) Chairman Jerome Powell took another dovish twist today at the June Federal Open Market Committee Meeting—but in a way I believe will further increase uncertainty on the Fed’s strategy and therefore will likely increase market volatility.

In his post-meeting comments, Powell stressed increased uncertainty related to global trade tensions and noted that risk sentiment in financial markets has deteriorated. The latter assertion stands at sharp odds with equity markets holding at record highs, something that Powell seemed to ignore completely.

And perhaps in defense of future rate cuts, Powell emphasized that Fed policymakers felt it was important to “sustain the expansion” for the benefit of US consumers across socioeconomic groups. It is unclear to me, however, to what extent Fed rate cuts would sustain the economic expansion as opposed to sustaining a continued rally in financial markets, and particularly risk assets.

In the Q&A with the media after the meeting ended, Powell said that the shift in rhetoric in today’s statement had been driven by data and events that emerged in the last couple of weeks, and noted that new data and information would of course become available between now and the next Fed policy meeting. But if the Fed’s language is going to shift with every new batch of data, this seems to guarantee more swings like we have seen since late last year—causing more market volatility. It also contradicts Powell’s claim that the Fed wants to react to clear trend change, not to individual data points and shifts in sentiment.

US Economic Conditions Out of Sync with Dovish Stance

The Fed’s assessment of US economic conditions seems equally out of sync with this dovish shift in language: a very strong labor market (“prospects for job seekers have seldom been better”), wage growth in line with inflation and productivity growth, strong consumption, and the only shadow being some deceleration in business investment.

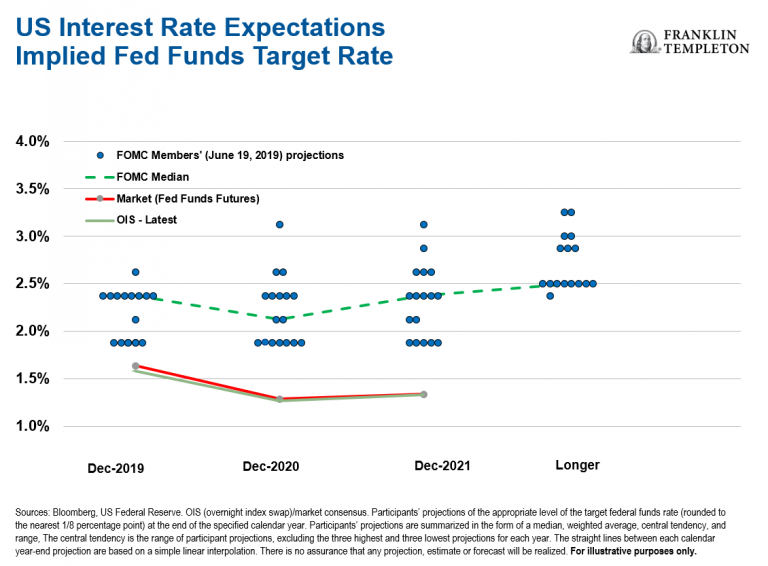

Here are the latest economic projections from the Fed:

- The Fed maintained its 2019 US GDP growth forecast of 2.1%, but increased its 2020 forecast to 2.0% from its forecast of 1.9% in March.

- The 2019 inflation projection (based on Core Personal Consumption Expenditures) was lowered to 1.5% from 1.8% in March.

- The projection for the unemployment rate edged down slightly to 3.6% for 2019, from its prior projection of 3.7%.

The Fed today tried to appease the markets, and predictably markets are immediately clamoring for more: They now fully expect a rate cut next month with 2-3 more cuts to follow in the remainder of the year. I really doubt that the data in the next few weeks are going to show the deterioration in trend that would justify a Fed cut—so the Fed will again be in a very tough spot, in my view. I would note that the median dot in the Fed’s “dot plot” (as illustrated below) still shows no cuts this year.

Balance of Risks: Exacerbating Volatility

After today’s press conference, the balance of risk for the next monetary policy move is clearly towards a cut. I no longer expect the Fed to hike again this year—so my baseline has shifted to no change. My concern is that any rate cuts will be driven entirely by market pressures rather than economic developments. And if that is the case, the Fed will then exacerbate the financial froth and distortions we already observe in some asset markets.

In its attempt to pacify the markets, the Fed keeps trading less volatility today for greater volatility—and financial risks—later down the line.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. Floating-rate loans and high-yield corporate bonds are rated below investment grade and are subject to greater risk of default, which could result in loss of principal—a risk that may be heightened in a slowing economy.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Fixed Income Topics >