Trade issues continued to dominate headlines in June, with easing in US-China trade tensions providing a boost to emerging markets overall during the month. But Franklin Templeton Emerging Markets Equity cautions trade-related headwinds could persist. The team shares its latest emerging-market outlook and explains why the small-cap space looks attractive right now.

Three Things We’re Thinking About Today

-

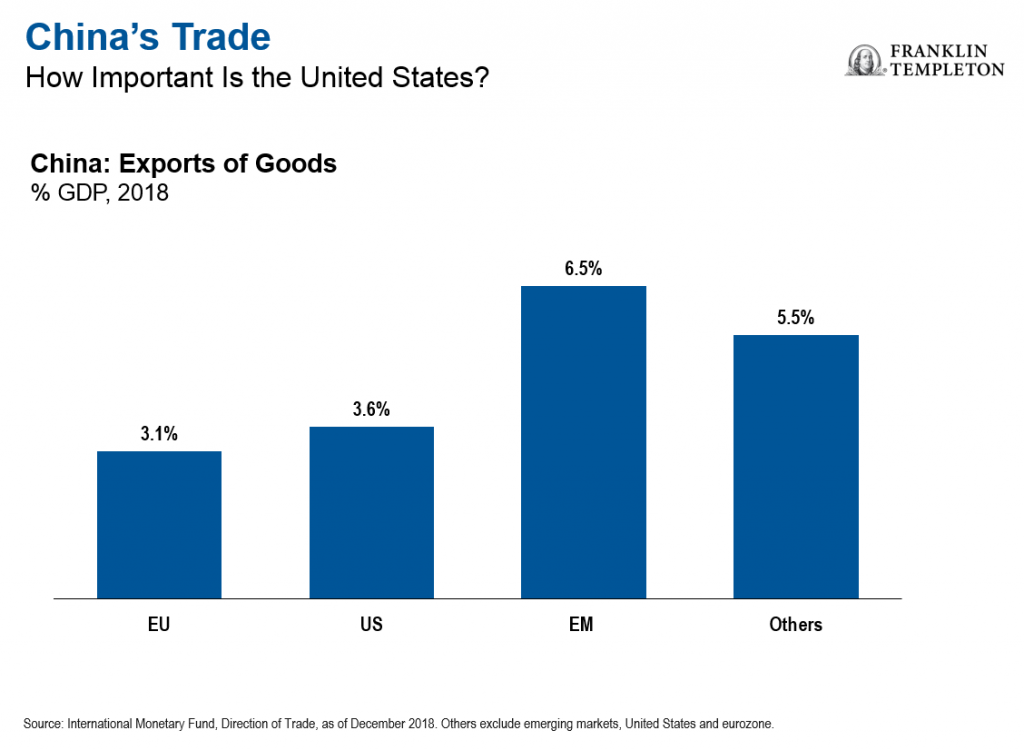

- The United States and China agreed to resume trade talks at the G20 summit in late June. The United States also decided against imposing new tariffs and easing some restrictions on Chinese telecommunications company Huawei, while China agreed to substantial purchases of agricultural and other products from the United States. Although this truce has reduced the likelihood of further escalation in the short term, we expect prolonged discussions in view of the pending issues between the two countries. Markets globally—and especially the technology sector—reacted positively to the news. Meanwhile, in addition to diversifying its trading relationships, China in general has been turning less dependent on trade. In contrast, domestic consumption now makes up the lion’s share of China’s economic growth, accounting for 76% of gross domestic product (GDP) in 2018, up from 59% in 2017.1

Net exports, however, were a 9% drag on growth in 2018, compared to a 9% contribution in 2017.2 Further, with only 19%3 of Chinese exports destined for the United States in 2018, we have thus far seen limited impact from US tariffs on Chinese exporters.

- As widely expected, index provider MSCI promoted Kuwait to EM status in June. Kuwait’s MSCI Emerging Markets (EM) Index weighting is expected to be about 0.5% with implementation in May 2020. With substantial reserves, low levels of debt and a stable banking sector, Kuwait stands out in an EM context. Kuwait also continues to make significant progress in terms of fiscal and structural reforms and is committed to developing a dynamic and vibrant private sector. And while there is still some way to go, the results of Kuwait’s move to reduce the role of the public sector in the economy are encouraging, in our view. The country is moving away from oil dependence by developing its infrastructure, investing in human capital and promoting private-sector involvement. Despite trading at a premium to its EM peers, valuations in Kuwait remain reasonable, in our estimation. Moreover, we believe the earnings outlook for listed Kuwaiti companies supports a valuation premium. On a sector view, we remain particularly upbeat about Kuwait’s banking sector, which is showing improving profitability on the back of falling provisioning and improving asset quality.

- The EM small-cap space remains attractive to us. We continue to find investment opportunities in the health care sector, as well as companies that stand to benefit from long-term secular trends relating to consumption and innovation. Demographic shifts and aging populations in many EM countries are intensifying pressures on health care systems. In our view, these factors will continue to be a boon for hospitals, dietary supplements, medical devices and pharmaceuticals. The health care landscape is also changing, with growing consumer awareness fueling medical and wellness needs. We are seeing more consumers embrace preventive health care out of a desire to look and feel better. Rising domestic consumption also remains a long-term secular driver for EMs. EM companies have not only embraced the use of technology but have become global market innovators in many areas. We expect technology to continue to reshape EMs, as technology disruptors become the norm by transforming industry landscapes, and companies continue to embrace technology and innovation.

Outlook

EM equities marched higher in the first half of 2019, supported by the US Federal Reserve’s (Fed’s) dovish pivot, attractive EM valuations and a search for higher-yielding assets. Volatility, however, remained an overarching feature as negotiations between the United States and China progressed early in the year but then stalled in May. A decision to restart talks in late June, however, provided some immediate relief.

We expect the US-China trade conflict to remain a major headwind. Even as we welcome a temporary truce in the trade battle, we believe it is unlikely to mark the end of longer-term tensions. In our view, investors should be prepared for more market volatility as the two major powers continue to iron out outstanding differences across a wide range of economic and geopolitical issues.

We continue to stand by our bottom-up investment approach in this uncertain environment. We believe that it takes first-hand research, proprietary insights and an extensive network across EMs to analyze the impact of the trade war beyond tariffs and identify attractive investment opportunities.

We remain focused on seeking companies that demonstrate sustainable earnings power and trade at a discount relative to their intrinsic worth and other investments available in the EM investment universe.

Emerging Markets Key Trends and Developments

EM equities finished a volatile quarter with modest gains and lagged developed market stocks. Global trade relations and central-bank rhetoric dominated investor sentiment. The United States and China agreed in June to restart trade talks, after negotiations hit an impasse in May and triggered a new round of tariff hikes and trade restrictions. The Fed struck a dovish tone in the face of growing economic uncertainties, fueling market expectations for interest-rate cuts. EM currencies collectively strengthened against the US dollar. The MSCI Emerging Markets Index returned 0.7% over the quarter, compared with a 4.2% return in the MSCI World Index, both in US dollars.4

The Most Important Moves in Emerging Markets in the Second Quarter of 2019

- Asian equities swung between gains and losses in the second quarter before ending the period lower. Chinese stocks fell amid a flare-up in US-China trade tensions and weak economic data. Market losses were capped by hopes for a truce in the trade war ahead of a meeting between US President Donald Trump and Chinese President Xi Jinping at the end of June. The outcome of the meeting was largely constructive—the United States said it would hold off on fresh tariffs on Chinese goods and loosen trade restrictions against Huawei, in return for more purchases of US goods from China. Markets in Pakistan and South Korea also declined. Conversely, stocks in Thailand, the Philippines and Indonesia rose. The confirmation of General Prayuth Chan-o-cha as Thailand’s prime minister in June following a general election in March lifted political uncertainty in the country.

- Latin American stocks advanced, aided by gains in Argentina, Brazil and Mexico. Argentina’s market rallied on the back of its inclusion in the MSCI Emerging Markets Index. Investors also welcomed President Mauricio Macri’s choice of a moderate opposition leader as vice-presidential candidate in the lead-up to the country’s general election. In Brazil, equities rose as prospects for a pivotal pension reform brightened. Policymakers indicated that the lower house of Congress could vote on a reform proposal targeting fiscal savings of more than R$900 billion (US$234 billion) over a decade in July. Mexican stocks posted subdued returns amid trade tensions. Mexico agreed to step up control of migration toward the United States to avert trade tariffs proposed by President Trump. Meanwhile, Chile, Colombia and Peru were regional underperformers. Peru’s economic growth was nearly flat in April, due in part to weakness in the mining and manufacturing sectors.

- Stocks in the Europe, Middle East and Africa region as a whole rose. Russia, Egypt and South Africa were among markets recording solid gains. Undemanding equity valuations in Russia were a draw for investors. The country’s central bank also trimmed its key interest rate in June and flagged the likelihood for further cuts. Egypt’s economic growth gathered steam in the first quarter, and the government projected a further uptick for the second quarter. South Africa’s market was supported by advances in mining stocks as prices of gold and other metals climbed. In May, the country’s ruling African National Congress party won the national election. In contrast, stocks in Hungary and the United Arab Emirates declined.

Regional OutlookAs of June 30, 2019+-

The graphic above reflects the views of Franklin Templeton Emerging Markets Equity regarding each region. All viewpoints reflect solely the views and opinions of Franklin Templeton Emerging Markets Equity. Not representative of an actual account or portfolio.

__________________________________

1. National Bureau of Statistics of China.

2. Ibid.

3. International Trade Centre.

4. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

http://emergingmarkets.blog.franklintempleton.com

© Franklin Templeton Investments

More Energy Topics >