Health Care Sector Innovation: How Biopharma Scientists Save Lives Globally

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn today’s world of disruptive innovations, biotechnology is entering the most transformative phase our health care analysts have seen in 25 years. Since mapping out the human genome in 2003, drugs using new treatment paradigms—like gene and cellular therapies—have jumped out of laboratories and into the marketplace to tackle humanity’s most vexing diseases.

In this excerpt from the latest “Franklin Templeton Thinks: Equity Markets,” we examine how technology is transforming health care, how research and development drive innovation, and how drug patent expirations impact companies.

The newest medicines can sound like science fiction; for patients, the results are quite real.

Consider children suffering from late-stage leukemia. In 2017, a newly approved treatment gave leukemia patients the ability to have their own immune cells reprogrammed to recognize and attack their cancer. For cancer patients and their families, this treatment is life-altering and priceless.

For biotechnology scientists, it’s the start of a new chapter in our understanding of human biological pathways and how we can disrupt diseases.

As investors, our focus for this discussion is large biopharma; most of the market capitalization in the health care sector resides here, and large players are better equipped to commercialize new medicines. Small firms often can’t pull this off by themselves.

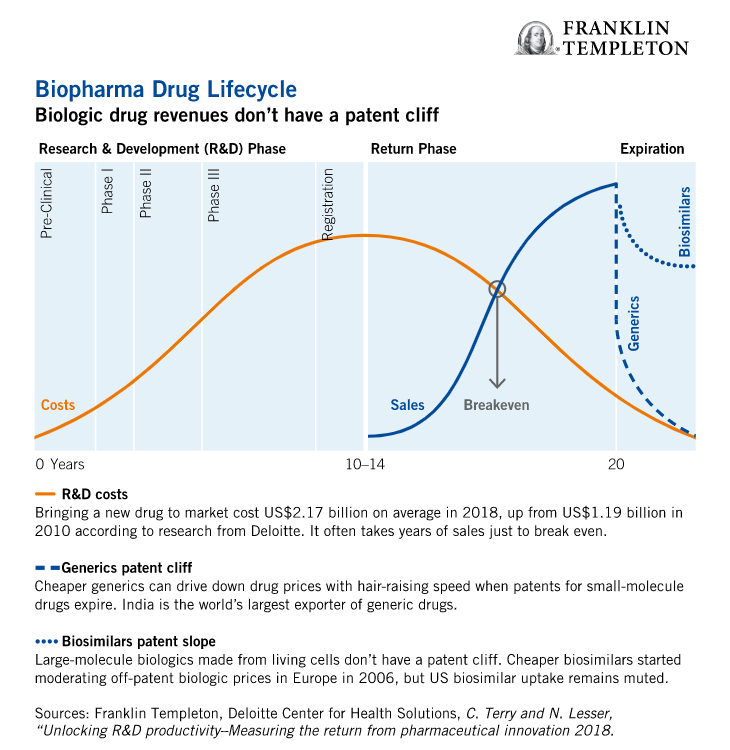

Biopharma Revenues Have Built-in Expirations

If there’s one event our analysts agree impacts biopharma market valuations more than others, it is drug patent expirations. Expirations are part and parcel of the revenue lifecycle of every drug and form the backbone of our analyst cash flow models. Why? Without patent protection, cheaper generics swoop in and drive down drug prices.

Revenues can drop with hair-raising speed when a drug reaches the “patent cliff.” It’s for this reason that new medicines—drugs a decade from patent expiration that command premium prices—are top of mind for every biopharma CEO and for our health care analysts. Without a well-stocked pipeline of drugs constantly under development, a drug maker’s prospects can look rather grim.

To illustrate this point, let’s look at a new cancer drug: Vitrakvi (pronounced: vı-tr˘ak-vee). The first treatment of its kind, Vitrakvi targets tumors with a specific genetic mutation and is opening the door to a genetics-based approach to conquering cancer. With the precision of a heat-seeking missile, Vitrakvi has shown great success in clinal trials.

Breakthrough medicines like Vitrakvi command premium pricing—a year’s supply of Vitrakvi costs $393,000 wholesale. It’s important to point out here that biologics—which are derived from human cells and not chemically manufactured—don’t have patent cliffs; instead, they have a gradual “patent slope.”

When biologics made the leap from laboratories to the markets in the late 1990s, scientists couldn’t make exact copies of living antibodies (the key ingredient of most biologics) without the confidential production methodology of the original drug. With no revenue expirations on the horizon, biologics gave biopharma CEOs more breathing room to discover the next wave of blockbusters.

Scientists eventually grew antibodies that produced the same therapeutic outcomes of original biologics, just not exact copies—it’s why the industry calls them bio “similar.” Fast-forward to today, sales of cheaper biosimilars are surging across Europe—enough so that future off-patent revenues for many biologics now have a patent slope inside our analyst cash flow models.

Looking forward, we think off-patent biologic revenues will fall even more steeply. Governments and consumers are chafing at biologic price tags and eagerly switching to cheaper biosimilars. Now more than before, biopharma CEOs need their research-and-development (R&D) engines firing on all cylinders to make up for future lost biologic revenues.

Tuning up Biopharma R&D Engines

Speaking with our health care analysts, it was clear that the inexorable march toward patent expirations makes R&D productivity a linchpin for market valuations. Less clear is whether large biopharma firms can innovate the way smaller, nimbler firms often do. After years of acquiring and merging with biotechnology firms, are today’s biopharma giants up for the challenge?

To grasp the true scope of the industry’s R&D challenge, it’s worthwhile stepping back to understand how biopharma has evolved. Over several decades, biopharma R&D has been shifting away from primary care—treating chronic conditions like high cholesterol in large populations—toward specialty care that serves smaller populations.

The low volumes of a breakthrough cancer drug like Vitrakvi, for example, can’t match the volumes of a cholesterol pill sold to millions. Just as sales volumes are declining, the average cost of bringing a new drug to market has increased to $2.17 billion in 2018—almost double the average cost of $1.19 billion in 2010.1 Those costs account for the fact that only one in 10 drugs that go into clinical trials gets approved.2

One cause of failures is that standard clinical trials haven’t evolved in 50 years, and are ill-suited for diseases like cancer that can require mixing treatments (drug cocktails) to merit approval.

Facing expirations on older blockbuster pills, today’s biopharma CEO might need a half dozen niche treatments to maintain growth. Without an R&D engine running full throttle, market values will fall.

Redesigning Clinical Trials

We think mixing laboratory talent across firms makes a lot of sense—sharing R&D costs can de-risk the downside when drug trials fail, while sharing gains from successful breakthroughs. We also think cross-company collaborations could dramatically improve clinical trials with a new design called “master protocols.”

Clinical trials have often been a time-consuming money pit because they test single treatments on one disease sequentially. Master protocols can work faster and more efficiently by analyzing multiple treatments from different drug sponsors on one or multiple diseases. To pull this off, drug sponsors must discuss and agree upfront how they wish to share data, publication rights and the timing of regulatory submissions.

The US Food & Drug Administration (US FDA) has received multiple inquiries from companies on master protocols and thinks more will flock to these trials once they see them work.3

Collaborative clinical trials could yield powerful results, but that doesn’t overcome all the hurdles with new drug discovery. A lot of time and money is wasted manually sifting through data. Boosting productivity with machine learning could augment human decision-making. Algorithms, for example, can process much higher volumes of data than humans can handle. In turn, machines are more likely to discover random (and potentially valuable) biologic associations that have otherwise gone unnoticed.

Our value and growth analysts are seeing innovation take hold at biopharma giants like Roche, Novartis, MSD and Eli Lilly because they absolutely must. Many of the industry’s older biologics face a looming challenge from cheaper biosimilars. The faster biosimilars take hold in the United States, the faster the biologic patent slope will shift into a cliff.4

Western Biopharma Hugs China

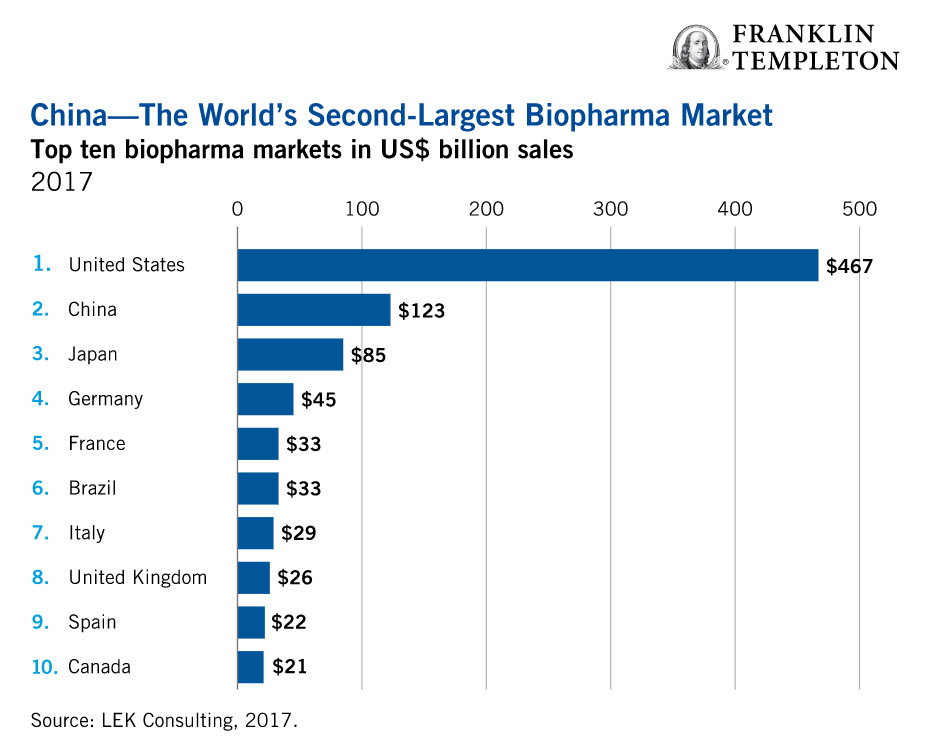

China is the world’s second-biggest market for biopharmaceuticals after the United States. It’s a crucial market for hitting growth targets for many companies—just not in the way it used to be.

Instead of simply unloading older off-patent drugs on China, Western firms are also bringing their new, more expensive medicines to China’s burgeoning middle class. When generic drugs dampened sales of off-patent drugs in the United States and Europe, biopharma companies typically aimed their sights on China.

Chinese consumers willingly pay a premium for Western brand-name pills for one primary reason: they don’t trust China’s locally produced generics.

In an effort to choke the rising drug costs for individual treatments, the Chinese government rolled out a new initiative mandating large public hospitals switch to cheaper generics. Some estimate China could save upwards of $30 billion with this shift.5

Beijing has also raised standards for its domestic drug makers, closing the quality gap with Western brands. So far, this year’s bidding process has mostly rewarded Chinese generics. As of May, public hospitals in China’s 11 largest cities no longer use Pfizer’s Lipitor, Sanofi’s blood thinner Plavix, or Astra’s Crestor—instead relying on much cheaper Chinese generics. It’s a sign of more to come.

If China is becoming a dead end for off-patent biopharma brands, it’s building a superhighway for more innovative (and more expensive) medicines to reach its 1.4 billion consumers. To meet local demands, China has finally sped up its sluggish approval process for complex biotech therapies and biologics.

In the past, companies waited an extra seven years before selling a new drug in China after launching them in Western markets, due to hurdles like rerunning medical trials.

In 2017, Beijing scrapped its rule to rerun trials for drugs already approved overseas and has increased its drug approval staff eightfold since 2014.6 Last December, China’s National Medical Products Administration (NMPA) approved an innovative new treatment for chronic kidney disease. What makes this notable is the approval comes well before the US FDA is expected to rule on the drug. Rather than trail behind the United States, China is turning the tables.

Catching up to India

Despite stepping up quality standards, China’s army of small drugmakers still has a way to go before competing on the global stage. Our value and emerging market analysts estimate China is 5–10 years behind India in terms of producing quality generics.

India is currently the world’s largest exporter of generic drugs, and home to about 6,000 drugmakers, according to its government estimates. US FDA data show Indian firms currently receive almost half of new US approvals for generics.

The relative simplicity of small-molecule chemical compounds is key to India’s success. With its vast supply of cheap labor, and a knack for reverse-engineering chemical compounds, India churns out huge volumes of quality generics at dirt-cheap prices. As a result, today’s generics industry has become a cutthroat low-margin business—not a fruitful long-term theme—though ideal for automation.

Biologic Sticker Shock

Making biologics and their biosimilar equivalents is a technically challenging and expensive exercise. It takes 8–10 years and $100–$200 million to replicate and market a biosimilar, compared to 3–5 years and $1 million–$5 million for a small-molecule generic drug.7

Some companies that invent and manufacture biologics, like Amgen and Novartis, also make and sell biosimilars. It’s a business strategy that could be described as, “if you can’t beat them, join them.” Other biopharma firms like Roche have outsourced biologic production to firms like Samsung Biologics in South Korea, which can offer low-cost production with superior quality.

China is a boon for older biologics like Roche’s cancer treatment Rituxan. China’s government, however, isn’t happy with Rituxan’s sky-high price tag. This May, China’s Fosun Pharma started marketing a cheaper version of Rituxan, the first NMPA-approved biosimilar made in China. With more than 200 biosimilars in clinical trials, China has more biosimilars in its pipeline than any other country in the world.8

Biologic “sticker shock” isn’t unique to China. It’s a global phenomenon that varies by country and is currently most acute among US consumers. Consider the world’s best-selling drug, Humira. A year-long supply costs $40,000 in the United States, higher than anywhere else in the world. Depending on insurance plans, co-pays for a single refill may cost as little as $50 or as much as $1,300.

Europeans, however, aren’t suffering from biologic price fatigue the same way these days. Why? Europe has eclipsed the United States (and China for that matter) in its uptake of cheaper biosimilars.

In Europe, the European Medicines Agency approved its first biosimilar in 2006 and currently has more than 40 biosimilars approved for use.9 The US FDA approved its first biosimilar in 2015. As of last summer, only four biosimilars were sold in the United States, and they didn’t make a dent in US biologic prices.10

A Familiar Tipping Point

The pace of change and competition in the biopharma industry has always been fast. Firms like Pfizer and MSD, who orchestrated mega mergers in 2009, did so partly to move into much sought after biologic medicines. Now, more than a decade later, the biopharma industry finds itself at a familiar tipping point. As patent expirations and biosimilars encroach on revenues, it’s up to scientists (as always) to churn out new therapeutic treatments at premium prices that can help biopharma CEOs maintain strong revenue growth.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity. Investments in fast-growing industries like the technology sector (which historically has been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments.

________________

1. Source: C. Terry and N. Lesser, “Unlocking R&D productivity–Measuring the return from pharmaceutical innovation 2018,” Deloitte Center for Health Solutions, 2018.

2. Source: Wright, R. “Biopharma Innovation–Value at Any Price,” Life Science Leader, May 15, 2017.

3. Source: Dunn, A. “FDA’s Woodcock defends accelerated approvals and talks of culture shift in clinical trials,” Biopharmadive, June 5, 2019.

4. Source: R. Langreth, B. Migliozzi, and K. Gokahle. “The U.S. Pays a Lot More for Top Drugs That Other Countries,” Bloomberg, December 18, 2015.

5. Source: Paton, J. “China May Save $30 Billion With Generic-Drug Plan, Novartis Says,” Bloomberg, April 4, 2019.

6. Source: T. Hancock and W. Xueqiao, “China health reforms help global pharma groups despite price cuts,” Financial Times, August 26, 2018.

7. Source: US Federal Trade Commission.

8. Source: Lyu, D. “China’s Fosun Pharma Takes on Roche with Biosimilar Launch,” Bloomberg, April 27, 2019.

9. Source: Zhang, J. “Biosimilars in China,” PharmExec, April 23, 2018.

10. Source: US Food and Drug Administration.

© Franklin Templeton Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All