Franklin Equity Group’s Steve Land discusses why the rally in gold that began in May is different from other rallies in recent years. He also gives his take on what it means for gold-mining equities.

Investor sentiment toward gold turned bullish in June, pushing gold spot prices to six-year highs in US dollar terms in July. As a result, there is excitement in the industry that, if prices hold, third-quarter corporate earnings results for gold miners may indicate a return to strong cash generation.

As long-term investors, we don’t make specific predictions on the short-term direction of gold prices or how long this current rally could last. However, we do see some potentially supportive market catalysts for gold and gold-mining companies.

Catalyst #1: Widening Expectations for Looser Monetary Policy

The shift in central-bank strategy around the world—from one of monetary tightening toward easing—seemed to be the primary trigger for the increased investor buying and recent move higher in gold. Lower interest rates present less of an opportunity cost to holding gold, as the metal provides no yield and often comes with storage and insurance fees.

At its June meeting, the US Federal Reserve (Fed) kept interest rates steady but emphasized its data-driven approach to policy decisions and noted it believes the case for lower interest rates to be strengthening. This was enough to swing market expectations, with most commentators now expecting the Fed to lower rates in 2019, which would be the first cut in over 10 years.

Lower interest rates could also weaken the US dollar’s trade-weighted value, which may lead to higher gold prices, given the historically negative correlation. Much of the price-sensitive demand for gold comes from outside of the United States, and a weaker dollar means people can buy more gold for the same amount of their local currency, adding upward pressure to the gold price. In our view, the fact that gold has moved higher during the recent rally with minimal US dollar weakness is impressive.

Catalyst #2: Geopolitical Tensions

Another reason why investors tend to flock to gold is for a potential hedge against rising geopolitical uncertainty. Gold is not tied to any one country or economic system, making it particularly attractive right now.

Conflicts between the United States and heavily sanctioned Iran, and breakdowns in ongoing US-China trade negotiations, are two of the concerns supporting gold this summer. Political turmoil in the United Kingdom over Brexit has also boosted gold’s investment appeal. Similarly, uncertainty ahead of the 2020 US presidential election could be supportive of gold prices next year.

Catalyst #3: Concerns about Global Economic Growth

Gold, which many investors regard as a “safe-haven” asset, is back in demand amid increasing concerns over the health of the global economy. On April 9 of this year, the International Monetary Fund (IMF) cut its 2019 outlook for global growth to the lowest level since 2009—the tail end of the global financial crisis.1 In the quarterly update of its World Economic Outlook issued in July, the IMF said trade tensions could cause the global economy to stall further. It trimmed the global forecast issued in April by 0.1 percentage point this year and next, with growth expected to hit 3.2% in 2019 and 3.5% in 2020.2

Gold and gold-mining companies have been out of favor since mid-2011 as the overall equity market has steadily pushed higher. However, a less certain economic outlook may draw attention back to this sector, in our view. Higher gold prices create an improving backdrop for gold-mining companies, at a time when other types of companies may be showing the negative impacts from a slow-growth environment.

Catalyst #4: Central-Bank Gold Buying

Central banks have been increasingly active buyers of gold over the past several years. According to the World Gold Council (WGC), net central bank gold purchases in 2019’s first quarter were 145.5 metric tons (mt), the highest first-quarter level since 2013. Buying momentum has carried over from last year’s 74% rise, when 651 mt of gold was accumulated—the largest annual purchase since 1971, when the United States stopped the dollar’s convertibility into gold.

Accumulation by central bank repositories extended into April and May at a combined 92.9 mt of bullion.3 In early July, the National Bank of Poland announced that they had purchased 100 mt of gold in the first half of 2019, which was not reflected in the previous WGC data. Even without the full June data, H1 2019 gold purchases are running ahead of the very strong 2018 levels. Forward demand also holds the potential to be robust. According to a mid-July WGC survey, most global central banks expected global gold reserves to build further in the year ahead.4

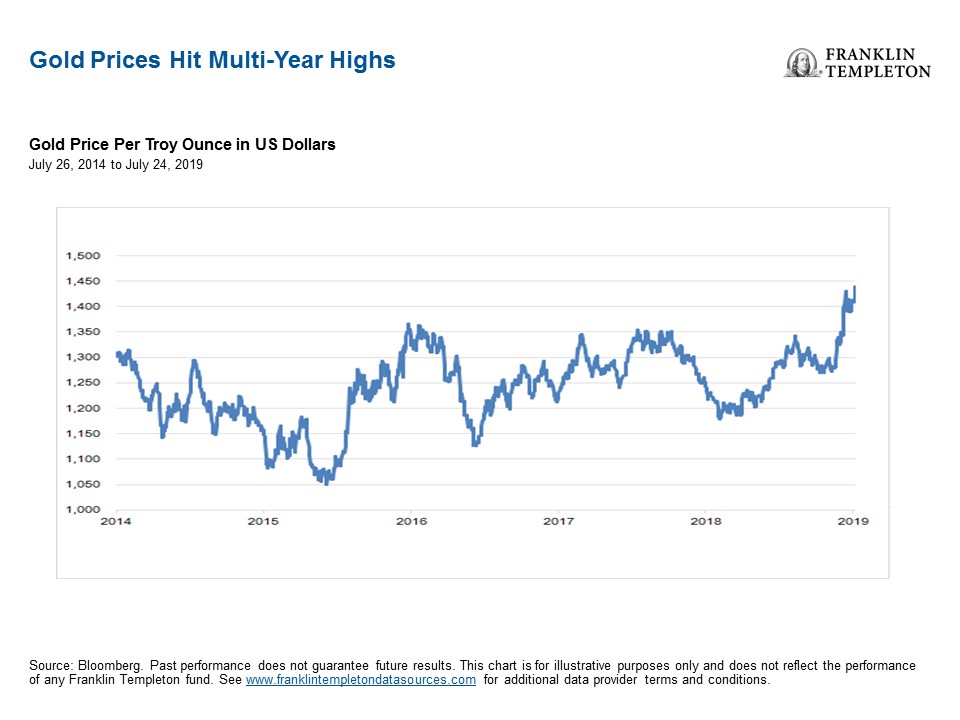

In terms of demand sources, gold continues to be bought primarily as jewelry, a component in high-end electronics, a safe-haven investment or a portfolio diversifier. Before the recent breakout, gold had been range-bound for the past five years, trading between $1,050 and $1,370 an ounce (oz) while averaging about $1,250/oz. In that environment, many gold-mining companies struggled to generate enough cash to sustain their businesses.

In our view, the current gold rally is an opportunity for gold-mining companies to show how much cash they can generate in slightly better gold markets. Mining operational costs tend to be fairly fixed, especially in a low inflationary environment like we are currently seeing. So, if gold prices stay above $1,400/oz through the rest of the third quarter, gold miner earnings reports released in September and October should show strong free cash flow.

That said, if gold prices weaken, most gold-mining companies should maintain a focus on improving the cost structure of their operations, debt repayment and asset rationalization. We believe these streamlining efforts should result in improved performance potential going forward. According to our analysis, management teams are increasingly focused on converting the profit margin from higher gold prices into free cash flow, to be reinvested in potentially high-return projects or returned to shareholders through dividends.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

______________________________________

1. Source: Bloomberg, “IMF Cuts Global Growth Outlook to Slowest Pace Since Crisis,” April 9, 2019.

2. Source: IMF World Economic Outlook Update, July 23, 2019

3. Source: World Gold Council, “2019 Central Bank Gold Reserve Survey,” July 18, 2019.

4. Ibid.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments