Central Bank Shenanigans

Membership required

Membership is now required to use this feature. To learn more:

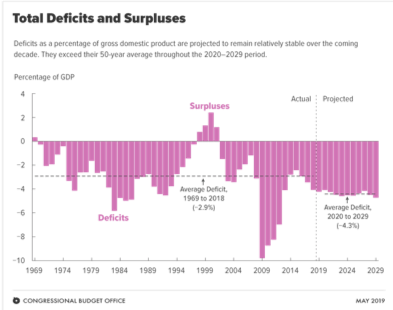

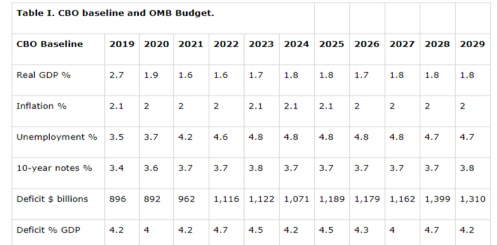

View Membership BenefitsIn May the Congressional Budget office (CBO) updated its 10-year fiscal estimates for federal revenue, spending, and annual deficits through 2029. The CBO is a non partisan agency tasked with analyzing data to provide Congress estimates for GDP growth and the impact on government spending and revenue from changes in tax laws. As the Summary notes the outlook for the next 10 years and beyond is not good and the long term fiscal health of the U.S. economy is projected to weaken. “Revenues and outlays are both projected to rise through 2029, but the gap between them is projected to persist, resulting in large deficits and rising debt. According to CBO’s estimates, the $896 billion deficit now projected for 2019 would grow to $1.3 trillion by 2029. Relative to the size of the economy, the deficits that CBO projects would average 4.3 percent of GDP over the 2020–2029 period. Other than the period immediately after World War II, the only other time the average deficit has been so large over so many years was after the 2007–2009 recession. Over the past 50 years, deficits have averaged 2.9 percent of GDP.”

The CBO’s projections are based on a number of economic assumptions that are worth reviewing. The CBO expects GDP growth to average 1.8% which is the economy’s long term non inflationary growth potential, according to the Federal Reserve. The main takeaway is that the CBO expects the U.S. economy to avoid a recession through 2029, although it does project growth to slow in 2021, 2022, and 2023 to 1.6%. In July the U.S. just set the record for the longest expansion in history. If the CBO is correct and no recession develops, the expansion that began in June 2009 would be 20 years old in 2029 double the prior record. That seems optimistic. If a recession does occur the CBO’s projections for government revenue would prove too high and spending too low, which would result in larger annual deficits and a larger increase in total debt outstanding.

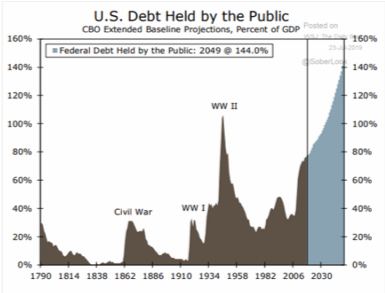

If the CBO projections prove reasonably accurate, public debt will be 78% of the nation’s Gross Domestic Product (GDP) in 2019, compared with 35% in 2007. The CBO expects public debt to increase to 92% by 2029, and to 144% of GDP by 2049. Faced with this likely outcome the CBO issued a warning. “That level of debt would be the highest in the nation’s history by far, and it would be on track to increase even more. The prospect of such high and rising debt poses substantial risks for the nation, and presents policymakers with significant challenges.” The CBO noted that over the last 50 years public debt has averaged 42% of GDP and only exceeded 70% during World War II. The highest peak in U.S. history was recorded in 1946 when the public debt-to-GDP ratio reached 106%. According to the CBO public debt could make a new record high in 2027. The budget gap for the 2019 fiscal year that ends Sept. 30 is on course to exceed $1 trillion, which is comfortably above the $89 billion previously estimated by the CBO.

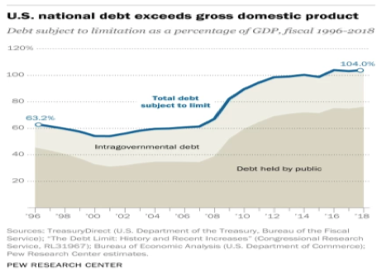

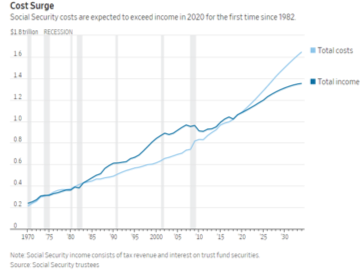

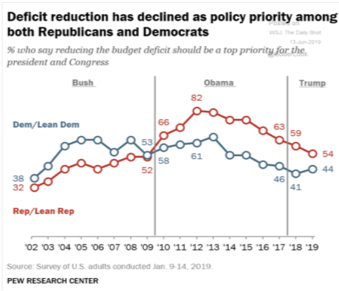

The amount of public debt doesn’t really show the complete picture. In 2018 26.5% of total debt (about $5.83 trillion) is owed to the government, with the single biggest creditor being the Social Security program. When all the outstanding debt is included, debt as a percent of GDP is already up to 104.0%. More than 10,000 Baby Boomers turn 65 every day, which is why Social Security outlays are expected to exceed contributions in 2020. Sometime around 2034 the Social Security Trust Fund will go broke requiring an increase in Social Security taxes or a 21% reduction in benefits. This coming disaster is known and a certainty, but I haven’t heard a single Democratic candidate address this issue or a single Tweet by President Trump. Social Security not only affects those who are old enough to begin receiving benefits but it also impacts every private sector worker in the U.S. With neither party possessing the courage to talk about the coming Social Security crisis it isn’t a surprise that awareness of this issue has receded. A recent poll by Pew Research shows that voters of both political parties are not concerned, although it will affect far more people than almost any issue that dominates CNN, MSNBC, and FOX 24/7.

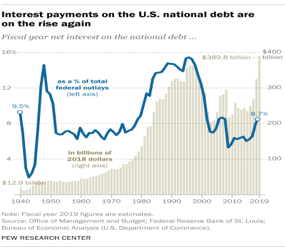

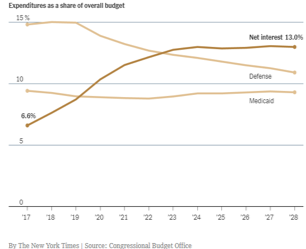

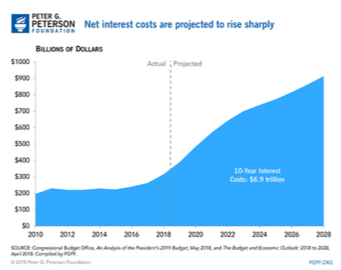

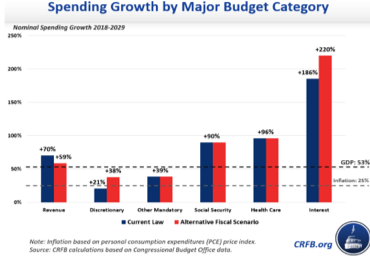

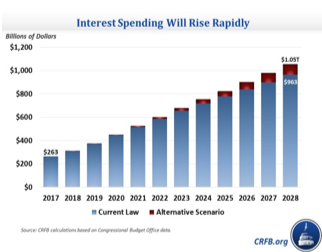

Another budget is interest expense. Within a few years annual interest expense is projected to exceed, as a percent of the Federal budget, the amount the federal government spends on Defense, Medicaid, and the Disability Insurance component of Social Security. The CBO projects that interest payments will skyrocket from $325 in 2018, to $389 billion in 2019, and to a staggering $914 billion in 2028. Net interest costs will total nearly $7 trillion over the next decade. Spending on Social Security will rise by 90% from 2018 through 2029 and Health Care spending will increase by 96%. In comparison the increase in expenditures on interest payments will soar by 186% according to CBO estimates.

On April 10, 1912 everyone boarding the Titanic knew they were getting on the largest passenger ship ever built. Before Mr. and Mrs. Albert Caldwell boarded, a Titanic crewman told them “Not even God could sink this ship.” What the Caldwell’s, the crewman, and everyone else aboard the Titanic didn’t know was that at 11:40 p.m. on April 14 the Titanic would hit an iceberg and sink at 2:20 a.m., less than 3 hours after striking the iceberg. Today, most Americans don’t realize that the U.S. economy is sailing toward a financial iceberg of excessive debt and unfunded government programs and promises. The coming collision between demographics and projected spending in Social Security, Medicare, Medicaid, and interest expense has the potential to cause an upheaval in the social, political, and economic foundations of this country. The precise timing of the coming collision can’t be known, but the need for educating the public about this issue and discussing how to proceed should be a political priority.

Instead, the 20 Democrats seeking the presidency are advocating free college education for anyone who wants one, and free health care for all including those who aren’t citizens. The prior analysis of the future fiscal health of the U.S. indicates that the U.S. will have a difficult time paying for all the promises already made, so increasing liabilities is irresponsible. The Republicans passed a large tax cut that was promised to boost job and wage growth, productivity and business investment, but would not be used for stock buybacks. The tax cut modestly helped job and wage growth, and business investment has weakened after a spurt in 2018. The tax cuts impact on stock buybacks is undisputable. The Democrats and Republicans are charting a course toward the financial iceberg and increasing the cruising speed of our Titanic.

The Federal Reserve has two mandates: maximum employment and stable prices. The unemployment rate is near a 50 year low and inflation is modestly below the Fed’s 2.0% target. The Federal Reserve defined stable prices in January 2012 when it formally adopted the 2.0% target. In May 2003 the European Central Bank (ECB) set the medium-term target for inflation to a value “below but close to 2%” to achieve price stability. In January 2013 the Bank of Japan (BOJ) established 2% as its inflation target and said it would pursue "open-ended" monetary easing, pledging to carry on with purchases of financial assets and a virtual zero interest rate policy as long as it is deemed necessary to achieve its inflation target.

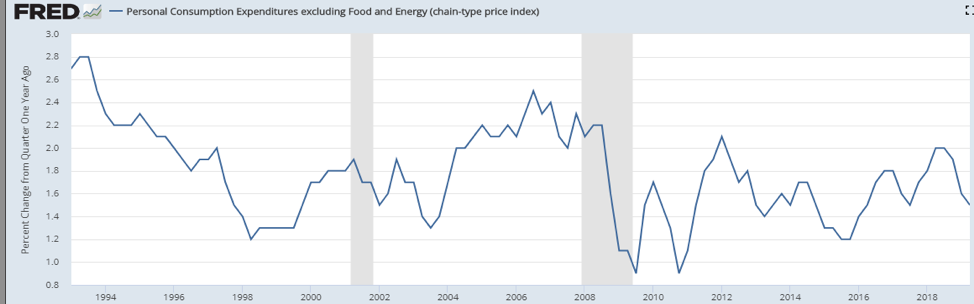

The Federal Reserve’s preferred inflation measure is the Personal Consumption expenditures index (PCE). Since 1994, the PCE has only been above 2.0% from mid 2004 until mid 2008 and briefly in 2012, or less than 5 of the past 25 years. The ECB and BOJ have experienced the same disappointing results.

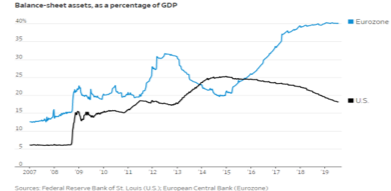

No one can say the Central Banks haven’t tried. The Federal Reserve held its policy rate near 0% from 2008 until December 2015 before raising it 9 times over 3 years to 2.4%. (The FOMC lowered the federal funds rate to 2.15% on July 31.) The ECB lowered its policy rate below 0% in early 2014 and to -.40% in early 2016. At the ECB’s recent meeting on July 25 it pledged to lower rates further. The BOJ lowered its policy rate to 0% in 1999 where it remained until it was increased to 0.5% in 2007 before returning to 0% after the financial crisis. In early 2016 the BOJ lowered it to -.10%. All three central banks have employed Quantitative Easing programs to augment their near zero or below zero interest rates. The ECB’s balance sheet is 40% of Eurozone GDP and the BOJ’s is an astounding 102.0% of GDP. Although the Fed began trimming its balance sheet from 25% in 2015 it is still 17% of GDP.

One would think that after so much effort and so little success the PhD’s at the Central Banks would question whether their monetary tools were insufficient to lift inflation to 2.0%. That of course would require a measure of humility. Instead, Central Bankers have just pledged that more of the same will eventually allow them to achieve their inflation goal and restore the credibility lost by not getting inflation up to 2.0%. In a May 21, 2019 speech in Hong Kong St. Louis Federal Reserve President James Bullard said the Fed “may want to consider ways to re-center inflation and inflation expectations at the 2% target. A downward policy-rate adjustment even with relatively good real economic performance may help maintain the credibility of the [Federal Open Market Committee’s] inflation target going forward. A policy rate move of this sort may become a more attractive option if inflation data continue to disappoint.” The U.S. economy just set a record for the longest expansion in history, unemployment is at a 50 year low, GDP growth is still chugging along at 2.0% to 2.5% and inflation is 1.6%. That sounds like a great outcome and hardly a disappointment.

Central bankers believe that inflation expectations play an important role is the level of inflation. James Bullard explained their role in a 2016 essay.”Modern economic theory says that inflation expectations are an important determinant of actual inflation. How does expected inflation affect actual inflation? Firms and households take into account the expected rate of inflation when making economic decisions, such as wage contract negotiations or firms’ pricing decisions. All of these decisions, in turn, feed into the actual rate of increase in prices. Given that central banks are concerned with price stability, policymakers pay attention to inflation expectations in addition to actual inflation.” The concern is that if inflation expectations remain too low for too long Central Bankers will find it more difficult in getting real inflation up to 2.0%. What a shame! Some economists are so serious about this ‘problem’ that they have urged the Fed to adopt price-level targeting in which the Fed would pledge to achieve future inflation that is 1.0% above the Fed’s 2.0% target. As if the Fed had that much power by simply pledging to raise inflation above the target they have failed to reach in 20 of the past 25 years! What hubris!

In a June 2018 a number of important findings about the value of inflation expectations were uncovered in a research paper published by the National Bureau of Research entitled Inflation Expectations as a Policy Tool? The researchers found that households and firms generally do not have well-informed expectations of future inflation, and often do not know what the inflation rate has been recent years. Large policy-change announcements in the U.S., the United Kingdom, and the Eurozone, seem to have only limited effects on the inflation expectations of households and firms. Since the early 2000’s the expected inflation rate by households in the U.S. averaged around 3.5% and well above the actual rate. In addition, when the researchers asked hundreds of top executives for their U.S. consumer inflation forecasts over the next 12 months, some 55% said they did not know. Among those who offered an inflation forecast, the average was 3.7%, again way too high. These finding don’t surprise me since I’ve never attended a party or gathering where the topic of inflation expectations ever came up. I doubt the 100 million of shoppers going into a Wal Mart store each week were motivated by their inflation expectations, as opposed to wanting to buy what they need at a good price.

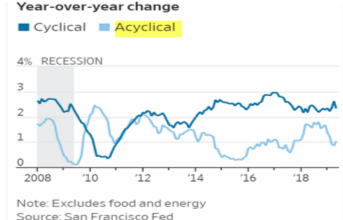

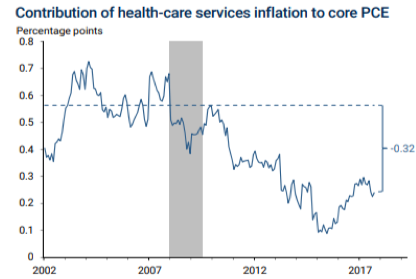

As noted the Fed’s preferred inflation measure is the Personal Consumption Expenditure Index (PCE), but there may be a problem in the components within the PCE. In 2017 economists at the Federal Reserve Bank of San Francisco published an analysis of the PCE in a paper entitled What’s Down with Inflation? They divided the components of the PCE into two categories: procyclical and acyclical. They found that the categories exhibiting a procyclical relationship make up 42% of the PCE and include housing, recreational services, food services, and some nondurable goods. The acyclical categories, which make up the remaining 58%, include health-care services, financial services, clothing, transportation, and other smaller categories. They found that the cyclically sensitive components of core inflation had accelerated to 2.33% annually by May 2017 from 0.41% in mid-2010. The procyclical categories have behaved as they did from 2002 to 2007. However, core inflation in the acyclical categories slowed from 2.26% in mid 2010 to 1.04% in May 2017. (Chart on pg. 5 has been updated through May 2019) The key driver holding down acyclical inflation has been persistent changes to the health-care sector that began after the end of the recession. Cuts to Medicare payment growth rates have restrained health-care services inflation. Health care makes up a large share of the PCE, so price changes within this sector have a sizable effect on overall PCE inflation. The economists at the San Francisco Fed concluded that low health-care services inflation is currently subtracting about 0.3% from core PCE inflation. Core PCE inflation, which has been running about 1.6% would be close to 2%, if acyclical inflation were behaving as it did prior to the financial crisis.

Despite years of failure in lifting inflation to 2%, policy makers still believe they need to manipulate inflation expectations so core PCE inflation rises to 2.0%. In his testimony before Congress in July Chair Powell reiterated that if consumers and businesses expect such low inflation to persist, they may adjust their own price and wage-setting behavior accordingly. That could cause low inflation to become entrenched, leading to a vicious cycle economists now call “Japanification’. As Powell told members of Congress, “That road is hard to get off of. I think it’s quite important that we fight to keep inflation up to 2% and use our tools to achieve that.” After listening to Powell I’ll bet consumer inflation expectations are already climbing. After the FOMC lowered the federal funds rate .25% on July 31, smart consumers will rush to buy before prices go up. Credible research suggests that Central Banker’s fixation on inflation expectations is misguided and the San Francisco Fed has provided analysis that explains why falling acyclical inflation has contributed to PCE core inflation coming up short of the Fed’s 2.0% target.

In football offenses run misdirection plays that pull the opponents defense in one direction to create an opening in the other direction. For example, on the snap of the ball, the offensive line pulls to the right, the quarterback moves to his right, and fakes a hand off to the halfback who is moving to his right, so it appears the play is intended to be a run around the right side. In reaction to the offense moving right the defense reacts by moving to block the apparent running play, which opens the left side of the field. The offense exploits this opening by having the tight end on the right side fake a block on the middle linebacker before running to an open spot on the left side. After faking the hand off to the half back, the quarterback rolls back to the left and throws a pass to an often wide open tight end. Misdirection plays work well against defenses that are quick and aggressive since they react quickly.

Skip down to the third video to see an example of misdirection.

https://www.49erswebzone.com/commentary/1966-film-room-george-kittle-play-action-passing-game/

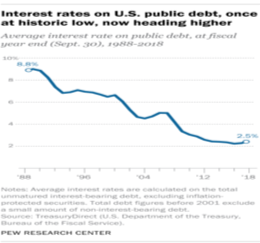

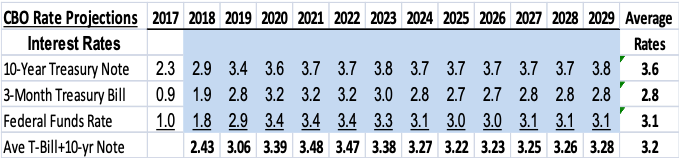

The Federal Reserve and compatriots at the ECB and BOJ have repeated the goal of getting inflation to 2.0% so often that it has become a Mantra. When the Fed adopted the 2.0% inflation goal in 2012 followed by the BOJ in 2013, I have no doubt both central banks fully expected to reach it within a short time. Their failure has turned it into a point of credibility and pride, but maybe something else too. As discussed interest expense is projected by the CBO to soar in the next decade and could total $7 trillion. The CBO’s estimate is based on where it expects interest rates to be as the total of outstanding debt climbs through 2028. According to the Treasury Department, the average interest rate on the public debt was 2.232% in 2016. After additional rate increases by the FOMC in 2017 and 2018, the average rate rose to 2.492% in 2018 and up to 2.567% in June 2019. In its 10-year budget projections the CBO includes its estimates of the federal funds rate, 90-day T-bill rate, and 10-year Treasury yield. I created a blend of the 90-day T-Bill rate and 10-year Treasury Note that approximated the average rate in 2018 (2.43% vs. 2.492%) and provides a guidepost for the next decade.

The CBO expects the FOMC to increase the federal funds rate to 3.4% in 2020, 2021, and 2022 before a slowdown in the economy allows it to be lowered to 3.1%. The yield on the 90-day T-bill is closely tied to the federal funds rate. The CBO forecast that the yield on the 10-year Treasury note will rise to 3.6% in 2020 and average 3.6% for the entire period. On August 1 the 90-day T-bill yielded 2.11% and the yield on the 10-year Treasury note was 1.9% for an average of 2.0%. The Treasury saves approximately $200 billion for each 1.0% change in the average rate on public debt. If in the pursuit of its 2.0% inflation target, the Federal Reserve pursues a combination of rate suppression and a resumption of its Quantitative Easing program to keep the 10-year Treasury yield below 2.6%, the Federal Reserve could save the Treasury about $2 trillion in the next 10 years. Of course the Federal Reserve would never publically say that its goal was to suppress rates and save the Treasury money. But the Fed has been laying the ground work for years in convincing everyone of the need to achieve its 2.0% inflation target. On July 31 the FOMC justified its decision to lower the federal funds rate from 2.40% to 2.15% in part due falling short of its inflation target, even though the domestic economy is in good shape. The Federal Reserve can use its 2.0% inflation target as its misdirection play to hide the real intent. By lowering the amount of money within the annual budget spent on interest in the next decade, spending on other safety net programs can be maintained.

As discussed in the May 2019 issue of Macro Tides, members of the Millennial and Gen Z generations believe the government should do more to solve problems. According to a recent survey by the Pew Research Center, 64% of Millennials support more government intervention to solve societal problems, while Baby Boomers are split. Those born after 1996 are part of the Gen Z generation and are even more supportive of the government doing more (70%) compared to their Gen X parents (53%). As the children of Baby Boomers, Millennials are 15% more in favor of the government taking a bigger role, while Gen Z’s are 17% more supportive of a larger role for government than their Gen X parents. A University of Chicago’s GenForward Survey of Americans age 18 to 34 conducted in 2017 found that 62% think “we need a strong government to handle today’s complex economic problems,” with just 35% saying “the free market can handle these problems without government being involved.” If this survey was conducted in July 2019, and given the low support for President Trump from Millennials and Gen Zs, my guess is the numbers would be even more skewed than in 2017.

Millennials and Gen Z’s will become the largest number of voters in the next 10 years. At the time of the 2020 election the population of Millennial and Gen Z’s will represent 37.5% of the population compared to 28.5% for Boomers and 9.5% of the Silent generation. Sometime in 2019 the Millennial generation will be larger than the Baby Boom generation. In the 2024 and 2028 elections Millennials will be voted into office in far greater numbers and play a larger role in setting policy. Gen Z’s will be voting in larger numbers and supporting many of the policy choices Millennials will place on the national agenda. As this new wave of voters enter the polling booth, members of the Silent generation will be gone and Baby Boomers will increasingly be riding off into the sunset. Millennials will hold more elected positions in federal, state, and local governments than Baby Boomers, and therefore be in position to set policy and the direction of this country.

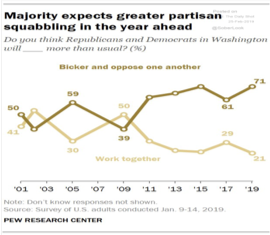

It is understandable that Millennials and Gen Zs would be open to a change in the role of government given the high level of political dysfunction that has resulted in very little progress in the last decade on a myriad of social issues and problems. Despite party affiliation, it is nearly impossible not to see that the level of rancor and divisiveness has exploded since the 2016 election. And most Americans, irrespective of their generation, expect partisan politics to only get worse. This doesn’t bode well for making progress on any issue. Nor should it come as a surprise that so many younger Americans have become disillusioned with the status quo and are thus receptive to something different. Most may not even know what socialism really means, but they do know the current direction hasn’t been good for them, or in their view, the country.

As the U.S. sails ever closer to its financial iceberg, politicians will be forced to address the funding needs of the numerous mandatory spending programs within the Federal Budget. The annual report by the Medicare Board of Trustees released in April noted the Hospital Insurance Trust Fund will run out of money in 2026. After 2026 incoming payroll taxes and other revenue will be sufficient to pay 89 percent of Medicare hospital insurance costs and will decline slowly to 78% in 2043. This confirms that current funds can't cover the 60 million seniors and disabled beneficiaries who currently count on Medicare for healthcare coverage. It seems a reasonable question to ask the Democrats running for President, who are proposing Medicare for all including those in the U.S. illegally, why they wouldn’t first shore up funding beyond 2026 for those currently on Medicare. For politicians of any stripe, the prospect of having to raise taxes or cut benefits for those depending on Medicare, Medicaid, and Social Security is a sure way to be voted out of office. Sooner or later politicians from both parties will look to the Federal Reserve to help fund the mandatory spending programs in the annual budget

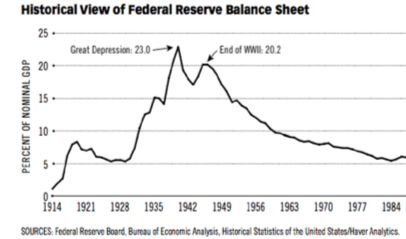

In July 1942 the Treasury Department asked the Federal Reserve to lower borrowing costs on the debt issued to fight World War II. The Federal Reserve agreed to purchase 90-day T-bills at .375% and longer dated debt at less than 2.5%. In the process the Federal Reserve expanded its balance sheet to 23% of GDP, compared to 25% at the end of the Fed’s QE program in 2014. There is a cadre of liberal Democrats who advocate using Modern Monetary Theory to fund the Green New Deal. While support for the Green New Deal is narrow, support for funding safety net programs would likely draw broad support not only from Millennials and Gen Z’s, but certainly from aging Baby Boomers. This is a far less painful solution than cutting benefits, and raising taxes on the top1% won’t generate enough money to cover the promises.

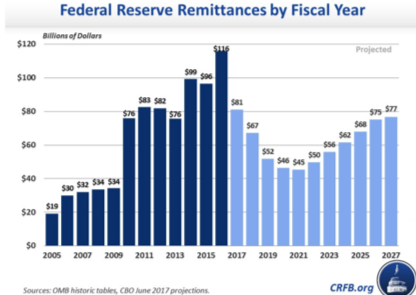

As part of the Fed’s QE program, the Fed remitted most of the interest it collected from its Treasury holdings back to the Treasury. The amount of the interest remittance more than tripled from 2009 to 2016. The amount of the remittance has fallen from $116 billion in 2016 to an estimated $52 billion in 2019. The decline reflects the shrinkage in the Fed’s balance sheet and higher payments to banks as the Fed increased the federal funds rate from .12% to 2.40%. The Fed’s balance sheet is currently $3.5 trillion, but it could easily be expanded to $10 trillion or more, especially in order to fight the next recession or fund mandatory programs. Providing full funding will increase annual budget deficits and drive the debt to GDP ratio to higher levels than the CBO has projected. The Federal Reserve could lower the interest expense on the debt issued to shore up mandatory spending programs by simply remitting the interest from bonds issued for mandatory spending to the Treasury. Once politicians embrace this concept of virtually free money to fund mandatory spending, how many will resist? The Democrats and Republicans were able to come together in July to pass a budget deal that pushed the debt ceiling beyond the 2020 election and also increased spending. It passed by 67 to 28 in the Senate with 23 Republicans and 5 Democrats voting against it. Increasing spending and ducking fiscal responsibility may be the only issue that Democrats and Republicans can agree on.

Central Bankers agree on using any tool available to get inflation up to 2.0%. The intended consequence of their effort allows politicians around the world to enjoy cheap money to fund government spending. But as with any major policy intervention and manipulation whether it is fiscal or monetary actions, there are unintended consequences. The Federal Reserve kept the federal funds rate comfortably below the rate of inflation so the real funds rate was negative from December 2001 until November 2004. This provided the cheap money that spurred the housing bubble. The FOMC increased the funds rate at 17 consecutive meetings until it reached 5.25% in July 2006. The Fed provided the air to blow up the bubble and the pin to pop it. The Federal Reserve and other government agencies also failed by not paying attention while investment banks increased their leverage to 30 to 1, even as mortgage lending standards became nonexistent. The lax lending standards received an endorsement from the Department of Housing and Urban Development, (HUD) which gave Fannie Mae and Freddie Mae quotas for buying subprime loans. In 2004 HUD raised its target for Fannie and Freddie Mac to purchase subprime loans to 56% from 50%, so lower income Americans could partake of the American dream of owning a home. Within a few years the dream became a nightmare. In 2010 Ben Bernanke, then Chair of the Federal Reserve and with the benefit of hindsight, provided this assessment. ‘I would say that the recent financial crisis was more a failure of economic engineering and economic management than economic science.” Wait a second! Wasn’t economic science what guided the Fed as it set the funds rate from 2001 until July 2006 and after the crisis? The Federal Reserve targeted higher stock prices as one of its goals when it launched the second round of QE in 2010 in the expectation that the wealthy would spend a portion of their equity profits and thus spur economic growth. That didn’t happen but the Fed did succeed in further increasing wealth inequality, which a number of Democrats want to understandably attack. Was this another failure of economic engineering or economic science?

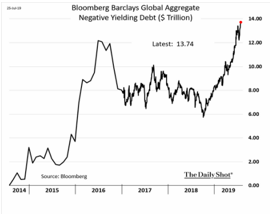

The collective actions by the major Central Banks have distorted and virtually eliminated the value of price discovery in the bond market. Trading in the Japanese bond market is by appointment only since so few bonds actually trade. Globally there is almost $14 trillion of bonds that yield less than 0%. Would any bond buyer willingly buy a bond that guarantees a loss if it the bond is held to maturity, unless a Central Bank was pressing yields lower? In a free market when governments and companies borrow money, the debtor pays the creditor interest based on the prevailing level of interest rates, the strength of the issuer, and the quality of the assets backing the debt being issued. Creditors are compensated for the risk of buying and holding debt. Central bankers have managed to turn the world of credit upside down. Now governments and some strong companies can borrow money at a rate below 0% which means the creditor is paying the borrower for the privilege of loaning money!

Germany comprises 30% of Eurozone GDP and has been the engine of growth in the EU. Banks throughout Europe provide 70% of credit creation in the EU compared to 30% in the U.S. since the U.S. bond market provides the bulk of credit issuance. The ECB’s negative policy rate has crushed German bank stocks, which impedes German banks from strengthening their balance sheets through the issuance of equity. This has and will continue to hurt lending and GDP growth in Germany. No worries though the ECB plans to do more stimulus!

U.S. Market Valuation

Sometimes investors attempt to use valuation as a timing indicator. This is a mistake since valuations can become more expensive or cheaper as investor sentiment drives prices well above or below any reasonable valuation. This does not mean that monitoring valuation is a waste of time since knowing whether the market is overpriced or on sale provides an important perspective. Too often investors get mired in the daily slog of political noise, social headlines, economic news, and the recent trend in the market. Perspective helps keep one grounded and assessing valuations can provide a level of detachment every investor can use.

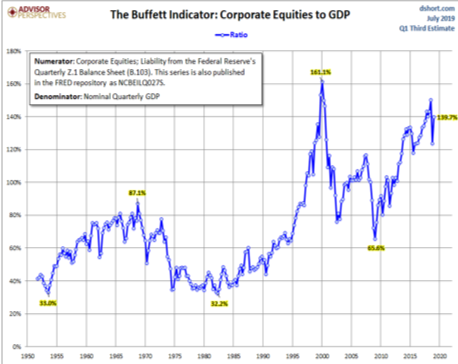

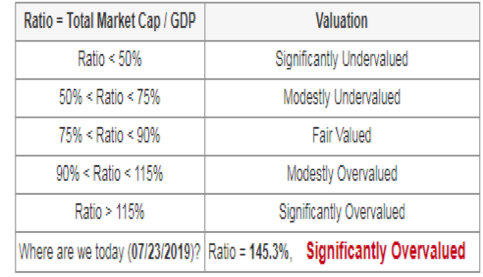

There are a number of valuation metrics but my favorite is comparing the Total Market Capitalization (TMC) of all US stocks to Gross Domestic Product (GDP). This became known as the Buffett indicator after Warren Buffett said it was his favorite valuation metric in a Forbes interview years ago. Corporate earnings are dependent on the economy but valuations are determined by a number of non-economic factors on such as investor sentiment and future expectations. Over a period of several decades investor sentiment will swing from being depressed to giddy happy, which causes stock values to rise well over 100% of GDP and plunge to under 50% in waves of despair.

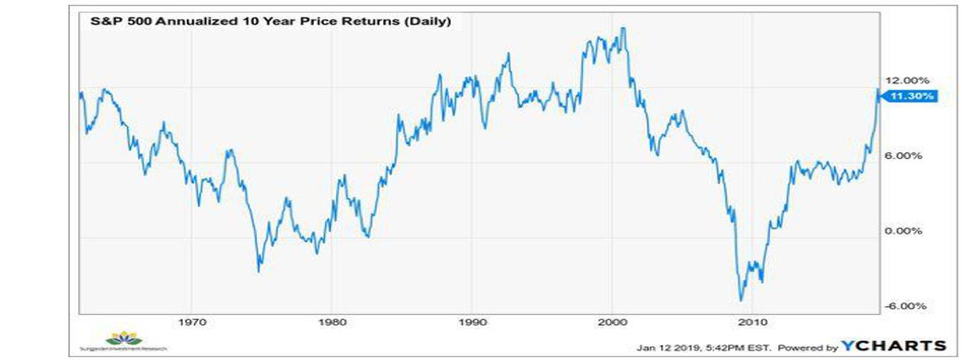

While valuation measures like the Buffett Indicator should not be used to identify tops and bottoms in the stock market, they do provide an insight into future returns. This is important risk management information that can guide investors and provide a framework about the bigger picture. It can also help set expectations for all investors that are realistic, rather than assuming the S&P 500 will average its long term compounded return of 10.0%. The S&P 500 has averaged a Compound Annual Growth Rate (CAGR) of 10.02% from 1926 through 2018. That figure masks the wide fluctuations that have occurred over time. The chart above shows the 10-year Annualized returns for the S&P 500 since 1950 with the first 10 year data point beginning in 1960. There have been two times when the 10 year return was negative and an extended period when it was comfortably above 12.0%. The S&P 500 bottomed in March 2009 which is why the 10-year annualized return has zoomed higher since March 2019.

For the unfortunate investor who began investing in the mid 1960’s, when the Buffett Indicator was modestly above 80%, the next 10 years provided a negative annualized return. An investor who bought in 1982 when the Buffett Indicator was under 35%, the subsequent 10 years and 20 years were unbelievably good. The first investor would have been tempted to forswear the stock market after 10 terrible years in 1974, while the second investor would have been a vocal advocate for investing in the stock market after 20 years of riding a rising tide of appreciation. Both investors would have benefited had they been able to review the Buffett Indicator. The first investor would have seen that not remaining patient was a mistake and the second investor would have been more sober about their good fortune and far more cautious about the future. It’s about perspective.

The Buffett indicator is suggesting that investors should be on notice that the stock market is vulnerable to a large decline when the economy enters the next recession. More importantly, the message from the rolling 10-year return chart and Buffett Indicator is that expectations for future returns should be tempered. On July 23 the Buffett Indicator was 145.3, which indicates that the S&P 500 is significantly overvalued. What should investors expect to earn in coming years given the current valuation of the S&P 500?

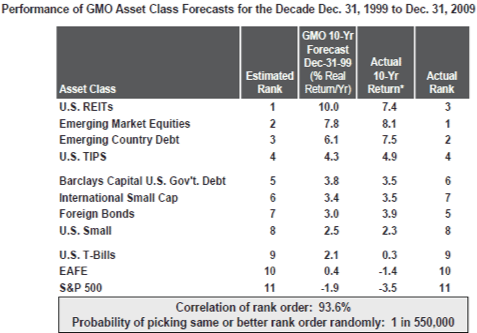

Grantham, Mayo, Van Otterloo (GMO) is a legendary value investment firm that forecasts the expected seven year returns for a number of asset classes. This value based analysis has enabled GMO to predict and outmaneuver nearly all the major market bubbles and tumbles in recent decades, including the late 1980’s Japanese stock-market bubble, the late 1990’s dot-com bubble, and the housing bubble and subsequent financial crisis in 2008. Professor Edward Tower of Duke University went back to 2000 and looked at GMO’s forecasts from December 31, 1999 and subsequent years, and then compared them with the subsequent seven-year returns, adjusted for inflation. Professor Tower found that GMO has been pretty good at predicting which assets would do best over the subsequent seven years and their expected rates of return. The correlation of GMO’s rank of best asset to worst was 93.6% and the probability of randomly picking a better ranking order was 1 in 550,000. Certainly far better than any coin flipper or dart throwing monkey.

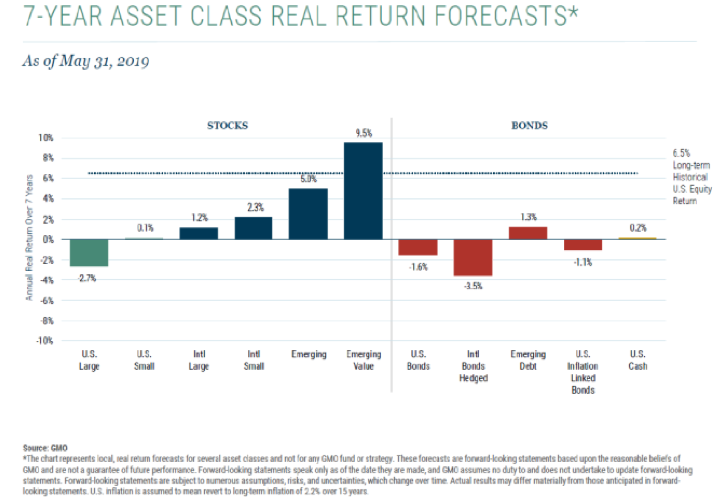

Analysis of a number of asset classes based on valuations as of May 31, 2019 by GMO suggests investment returns over the next seven years are likely to be negative for U.S. Large Cap equities (-2.7%), barely positive for U.S. Small Cap equities (+0.1%), with modest positive returns for International Large Cap (+1.2%) and Small Caps (+2.3%). The best equity returns are likely to be found in Emerging Market Equities (+5.0%) and Emerging Market Value stocks (+9.5%). With global interest rates so low it is no surprise that returns for U.S. and International bonds are likely to be lousy. Emerging Market debt is forecast to return just +1.3%, while U.S. Treasury bonds are expected to lose -1.6%. The next seven years is not likely to reward traditional asset allocation or the buy and hold approach. If GMO’s projections are remotely correct, financial advisors and individual investors will need to implement a tactical strategy for a portion of their portfolio to navigate the coming twists and turns most asset classes are likely to experience in order to produce a reasonable positive return. My job is to help to you.

The Role of Interest Rates on Valuations

From 1966 until the summer of 1982 the stock market traded in a wide range and in the process lowered the S&P 500’s Price/Earnings ratio from 18 to below 8. Amazingly, by 2000 the S&P 500’s P/E ratio had soared to over 32. In 1982 investors were only willing to pay 8 times for a dollar of earnings, but by 2000 were excited to pay 32 times the same $1.00 of earnings. Academics would argue that the decline in interest rates between 1982 and 2000 explains the expansion in the S&P 500’s P/E ratio. The federal funds rate fell from 20% in 1981 to 5.50% in 2000, while the 30-year Treasury yield dropped from 14.0% to 6.0%. If that logic held true, one would expect the valuation of European stocks would be higher than in the U.S. The ECB’s policy rate is -0.40% compared to the Federal Reserve’s federal funds rate of 2.15%. The forward P/E for the S&P 500 is 17.1 while the forward P/E for the Euro Stoxx 50 is 13.4 or 21.6% below the S&P 500. The 10-year Treasury yield is 1.90% while the 10-year German Bund yield is -0.45%. The forward P/E ratio for the German DAX is 13.1 or 23.3% below the S&P 500. The Bank of Japan’s policy rate is -.10% and the 10-year government bond yields 0.00%. Despite the lower policy rate and government bond yield when compared to the U.S., Japanese stocks have a forward P/E that has a discount of 24% to the S&P 500.

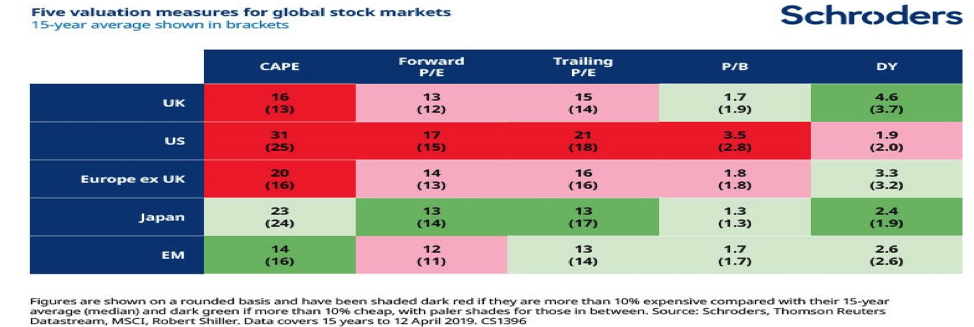

The graphic below compares the valuations of the major stock markets around the world using 5 different valuation measures. Whether it is the Cyclically Adjusted Price Earnings Ratio (CAPE), Forward or Trailing P/E’s, Price to Book ratio, or Dividend Yield, the US stock market sells at a premium to every other developed equity market even though interest rates are higher in the U.S.

The European Central Bank (ECB) launched its Quantitative Easing (QE) program in March 2015. When it ended its QE buying in December 2018 it had purchased $3 trillion of European sovereign and corporate debt, or roughly $8,000 for every person in the Eurozone and 38% of Eurozone GDP. The ECB’s QE program was so successful in bringing government bond yields down that more than $13 trillion of sovereign bonds yield less than 0%. Despite lower yields European stocks have consistently underperformed the S&P 500 since the ECB launched its QE program in March 2015. Not the outcome the ECB or most investors expected.

When people go to the race track no one bets on the smartest horse. Everyone wants the fastest horse in the race and place their bets accordingly. The foundation of portfolio management is diversification which is expected to lower risk as no one knows how various assets classes will perform over time. This assumption isn’t necessarily true but advocates of diversification rarely if ever acknowledge it. Invariably diversification addicts will look at valuations as a guide of where to invest in the anticipation that what is cheap now will become wanted in the future, reward patience, and provide a good return. In recent years the gap between the valuation of the U.S. stock market and the rest of world has become wider as the Schroders table illustrates. This has led portfolio managers and advisors to recommend a greater weighting to Europe in part due to additional monetary accommodation by the ECB. The European ETF with the largest amount of assets is Vanguard’s VGK. The top panel in the weekly chart below is the relative strength of VGK compared to the S&P 500. After outperforming the S&P 500 in 2006 and 2007, VGK has underperformed ever since, other than a few brief spurts based. This analysis indicates that allocating money to Europe in the past decade may have accomplished a level of diversification but it hurt investment returns. While VGK did move higher after the financial crisis, Europe as provided diversifiers a lower return than had they invested in the S&P 500 or elsewhere. Although valuations appear compelling and have been for some time, underweighting Europe or avoiding it has been prudent. The second chart shows VGK’s relative strength to the S&P 500 on a daily basis. There is nothing that indicates Europe’s relative strength to the S&P 500 is improving. I have no idea when Europe will begin to outperform. But by measuring its relative strength an investor can avoid the ‘value’ trap Europe has been for a long time and better identify when a change is afoot.

Jim Welsh

@JimWelshMacro

[email protected]

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits