Bouts of market volatility are an unnerving, but normal, feature of long-term investing. They’re not fun, but you can expect to see market declines periodically throughout your investing career. Our investing principles don’t change when the market is down, and yours shouldn’t either.

Yet it’s hard to sit still when the market is sliding. You can’t help but think: “Shouldn’t I be doing something?” Every investor is different, but here are a few steps that everyone should consider.

During market volatility:

-

Resist the urge to sell based solely on recent market movements. Selling stocks when markets drop can make temporary losses permanent. Staying the course, while difficult emotionally, may be healthier for your portfolio. This doesn’t mean you should hold on blindly, but we suggest taking into account an investment’s future prospects and the role it plays in your portfolio, rather than being guided by noise and fear.

-

Adapt your trading to fast-moving markets. If you must trade during volatile markets, take current conditions into account when entering orders. There are defensive steps you can take to protect an unrealized gain or limit potential losses on an existing position, such as stop orders and stop-limit orders.1 These can help give you more confidence when markets are volatile.

-

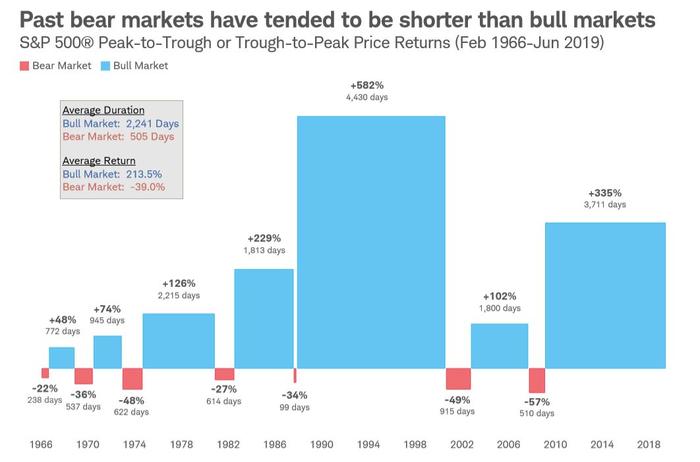

Take the long view. Markets typically go up and down, and you’re likely to experience several significant declines during a long investing career. But even bear markets—that is, periods when the market fell by more than 20%—historically have been relatively short. The Schwab Center for Financial Research looked at both bull and bear markets, based on the S&P 500® Index, going back to 1966, and found that the average bear market lasted a little longer than a year (505 days). The longest of the bears was roughly two and a half years (915 days), and it was followed by a nearly five-year bull run. Timing the market’s ups and downs is nearly impossible, but all investors would do well to ignore the noise and stay focused on their plans.

Source: Schwab Center for Financial Research with data provided by Bloomberg. The market is represented by daily price returns of the S&P 500 Index. Bear markets are defined as periods with cumulative declines of at least 20% from the previous peak close. Its duration is measured as the number of days from the previous peak close to the lowest close reached after it has fallen at least 20%. In the chart, periods between bear markets are designated as bull markets. Indices are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance does not guarantee future results.

-

Review your risk tolerance. Some investors learn the hard way that they aren’t as willing to face a sharp drop in the value of their portfolios as they had assumed. Similarly, risk you took on years ago may no longer make sense given your current situation and life stage. An aggressive allocation has historically gained more over time, but at the price of greater volatility—which can be especially risky if you don’t have much time to recover. Market downturns sometimes can be a wake-up call to consider adjusting your target asset allocation.

-

Make sure you have a diversified portfolio. Volatile markets also can reveal that portfolios their owners thought were appropriately diversified in fact aren’t. If you haven’t looked at your portfolio recently to make sure you understand what each asset class is doing and that the mix matches your target asset allocation, now is a good time to become reacquainted with it. Schwab’s investor profile questionnaire can help you determine your profile and match it to an appropriate target asset allocation. If you need more help, call 800-355-2162 to be connected to a Schwab investment professional.

-

Consider including defensive assets for more stability. Defensive assets, such as cash and cash equivalents, Treasury securities and other U.S. government bonds, can help stabilize a portfolio when stocks are slipping. Also, if you expect to spend from your portfolio within the next few years, it’s a good idea to hold those funds in assets that historically have been relatively liquid and less volatile than stocks, such as cash and short-term bonds. This can help you avoid having to sell in a down market.

-

Rebalance your portfolio as needed. Market changes can skew your allocation from its original target. Over time, assets that have gained in value will account for more of your portfolio, while those that have declined will account for less. Rebalancing means selling positions that have become overweight in relation to the rest of your portfolio, and moving the proceeds to positions that have become underweight. It’s a good idea to do this at regular intervals.

1 There is no guarantee that execution of a stop order will be at or near the stop price.

Important Disclosures

Please read the Schwab Intelligent Portfolios Solutions™ disclosure brochures for important information, pricing, and disclosures related to the Schwab Intelligent Portfolios and Schwab Intelligent Portfolios Premium programs.

Schwab Intelligent Portfolios® and Schwab Intelligent Portfolios Premium™ are made available through Charles Schwab & Co. Inc. ("Schwab"), a dually registered investment advisor and broker-dealer. Portfolio management services are provided by Charles Schwab Investment Advisory, Inc. ("CSIA"). Schwab and CSIA are subsidiaries of The Charles Schwab Corporation.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Investing involves risk, including loss of principal.

Past performance is no guarantee of future results.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower rated securities are subject to greater credit risk, default risk and liquidity risk.

Diversification, asset allocation and rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

The S&P 500 Index is a market-capitalization-weighted index comprising 500 widely traded stocks chosen for market size, liquidity and industry group representation

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0819-9C5W)

© Charles Schwab & Co.

© Charles Schwab

More Factor-Based Investing Topics >