Real Assets Could Be the Alternative

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGiven the backdrop of a slowing global economy and shaky investor sentiment tied to trade tensions, Franklin Templeton Multi-Asset Solutions’ Ed Perks and Gene Podkaminer are calling for an active investment approach. In the latest edition of “Allocation Views,” they outline six major themes driving their current views: slower global growth, subdued inflation, monetary policy effectiveness, the importance of nimble management, real assets, and alternative assets that aren’t really alternative enough.

Slower Global Growth A Rising Concern

The global economy continues to show downward momentum. Trade in goods has been the transmission mechanism for declining sentiment; the big question remains whether contagion from manufacturing threatens the more resilient services sector.

Stress in the traded goods sector of the economy has been broader based than just the flows directly impacted by tariffs imposed by the United States, or the retaliatory measures enacted by China. Indeed, threats to expand the theater of this trade dispute continue to pose a direct threat to European automakers. This hit to confidence has already started to impact manufacturing employment, and with factory orders in Germany showing little sign of a rebound, the risks to growth remain skewed to the downside.

However, it is the seeming intractability of the conflict between the United States and China that has become a bigger concern. We view trade disputes as only one symptom of broader tensions between an incumbent global power and its challenger for supremacy.

Taking a broader perspective of the major economies, the United States remains better placed than some in Europe. However, both regions show high levels of employment, and the relative confidence of consumers remains intact. This provides some cause for optimism.

While we continue to see few signs of late-cycle imbalances that typically foretell recession, and the probability of recession remains moderate, the risks are rising. The deeper the trade slowdown and the longer it persists, the harder it is to see the global economy escaping some form of contagion.

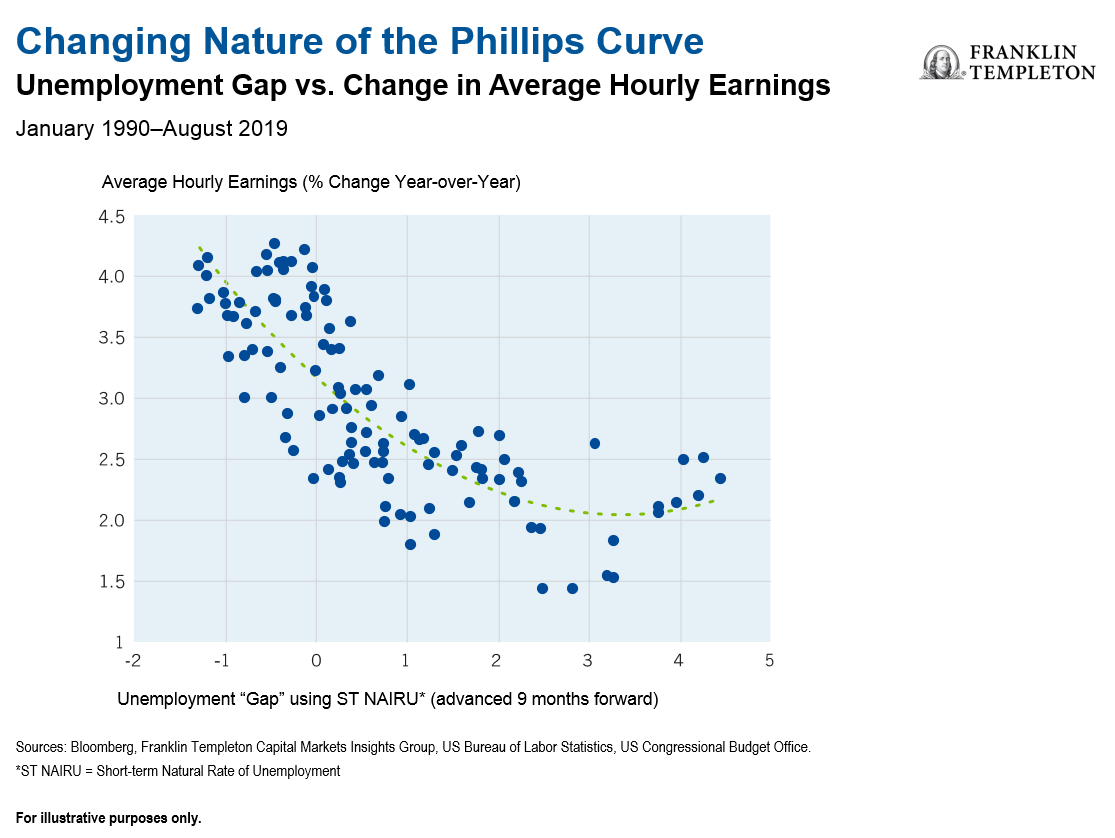

Subdued Inflation Across Economies

Subdued inflation expectations remain the main concern of key central banks. At this late stage in the business cycle, it is unusual to see such limited pass-through from tight labor markets to higher wages and ultimately broad measures of inflation. When combined with the headwinds facing global growth, an inability to generate the targeted level of inflation starts to feed concerns that inflation expectations might become “un-anchored.”

Survey measures of longer-term inflation expectations in the United States remain close to historical lows, matching levels last seen in late 2016. As a result, it is unsurprising to see the US Federal Reserve’s (Fed’s) continued focus on this issue.

Corporate fundamentals have remained relatively strong, despite the moderation in global growth. With labor markets tight in many economies, wage inflation has been picking up to some extent. However, the ability to pass this cost on to consumers appears limited. After a long period of expansion, profit margins have peaked and are likely to slow the pace of earnings growth.

Together with cyclical drivers of inflation that are weakening, commodity price declines since the middle of 2018 have put pressure on headline measures of inflation. Underlying disinflationary forces from demographics, technology and globalization have not been reversed, although some of their impact might be offset by growing protectionism and the impact of populism.

Approaching the Limits of Monetary Policy Effectiveness

Policymakers are facing a challenging few months. Investors’ expectations, in broad terms, appear to be discounting continued interest-rate cuts from the Fed, which are being mirrored in a range of developed and emerging economies. However, given the low levels of current official rates, many central banks may be running out of ammunition. Growing concern that conventional policy measures are nearing the end of their effectiveness puts more pressure on alternative policy measures and leaves investors worrying about policy impotence.

In Europe, heightened fears of recession have prompted calls for fiscal policy to be used to complement monetary policy. Although Christine Lagarde, incoming president of the European Central Bank (ECB), supports policy coordination, we do not underestimate the challenge of making progress in this area. The ECB may struggle to achieve the political consensus required for an early adoption of these measures until a deeper slowdown raises the fears of a renewed crisis in the eurozone.

At the same time, stock market resilience in the face of slower global growth appears to reflect ample liquidity more than corporate earnings expectations. We are concerned that central bankers will collectively fail to meet the full extent of market expectations. When combined with political pressure on the Fed and the complex interaction between trade rhetoric, market sentiment and monetary policy, we would not be surprised to see continued sharp moves in asset prices.

Nimble Management Required

Over recent quarters, we have highlighted continued divergence between various financial markets and the global economy. A return to long-run levels of market volatility since early 2018, rather than the muted levels seen for much of the past 10 years, indicates that we have entered a new volatility regime.

The decline in bond yields that accompanied the prospect of US-China tariff increases makes the next move even harder for the Fed. Markets now appear to anticipate a succession of rate cuts through year-end, at least in part to offset the impact of trade concerns, as well as any hit to market confidence. Increasingly, it looks like the Fed is being pushed toward actions that it is less able to justify on the basis of its dual mandate of stable prices and maximum employment. This has driven an inversion of the US Treasury yield curve, as the 10-year note’s yield falls below that of Treasury bills. Such a development is often a signal for impending recession, though we maintain a somewhat more constructive view of the US economy.

Against a backdrop of slower growth, global equities as a whole are not cheap, in our analysis. Any market disappointment over the Fed’s delivery of potential rate cuts might hurt market stability. Having taken a more cautious stance on risk assets in the first half of the year, we continue to believe navigating the challenges 2019 presents will require nimble management.

Real Assets Could Be the Alternative

By a significant margin, energy has been the most important factor driving consumer prices over recent years. The cost of a barrel of oil rebounded strongly and then corrected again. Despite its relatively modest weight in the overall Consumer Price Index (CPI), oil has accounted for a large part of the volatility in headline CPI inflation. That energy is considerably more volatile than most other components of CPI is not new or surprising. Indeed, this is why central bankers and market-watchers tend to look at underlying “core” inflation, which is the headline reading minus the volatile food and energy segments.

Headline inflation increases have a direct impact on the return from certain real assets. Inflation-linked bonds’ capital value and income stream rise in direct proportion to the increase in the headline US CPI (or other price index that certain countries’ bonds follow), delivering explicit inflation protection. Today, unless oil prices rebound, the rate of headline inflation is likely to continue slowing during the next few months. Similarly, an increase in prices that comes about because of import tariffs may have an immediate impact on inflation. However, the longer-term impact (on a sustained basis) is dependent on changes to consumer behavior. For now, longer-term inflation expectations remain relatively well anchored.

In contrast, market-based expectations for inflation, derived from the yields of nominal and real return bonds, have fallen sharply. These so-called breakeven inflation rates (where the prospective return on nominal and real-return bonds are equal) have responded directly to recent commodity price declines.

Some further modest decrease in market-based measures of long-term inflation rates could occur, but to see a move appreciably lower would require consumer expectations to become less well-anchored. Such an event would likely be a catalyst for an acceleration in the pace of monetary easing by the world’s leading central banks and may see broader market changes—weaker stock markets or, in the longer term, higher bond yields. It is this combination of “ shocks” that provides the environment where holding a diversifying asset such as TIPS might enhance return potential and lower portfolio volatility.

Management of Risk Profile—Duration Considerations

How would we take exposure to inflation protection? If we buy inflation-linked bonds out of our short-term bond holdings, we will take additional exposure to the level of interest rates (duration1 or interest-rate risk as well as the term premium seen in longer-dated yields). This might help to diversify against equity risk. However, we may not wish to add further to this exposure given historically subdued yield levels.

If instead we sell other bonds to fund this position, we would be reducing exposure to the defensive component of a multi-asset portfolio and not adding to overall duration. However, in our analysis, the overall portfolio would be more correlated to equity markets and more cyclical in nature, which runs counter to our defensive posture overall. Any reduction in overall diversification needs to be considered in deciding how to fund an investment in inflation-linked bonds.

Alternative Assets that Aren’t Really Alternative Enough

We anticipate that certain other alternative assets might show uncorrelated return potential. Real estate is widely viewed as providing some protection against a general rise in inflation. However, as global growth slows, this would impact the ability of tenants to continue to cover rent and risks falling occupancy rates. Similarly, any rise in bond yields could put pressure on property valuations through the current, relatively subdued yield. While directly held property might weather this storm, and even potentially benefit from a modest rise in inflation, listed alternatives such as real estate investment trusts (REITs) would be more vulnerable to a correction due to their equity-like characteristics, in our analysis.

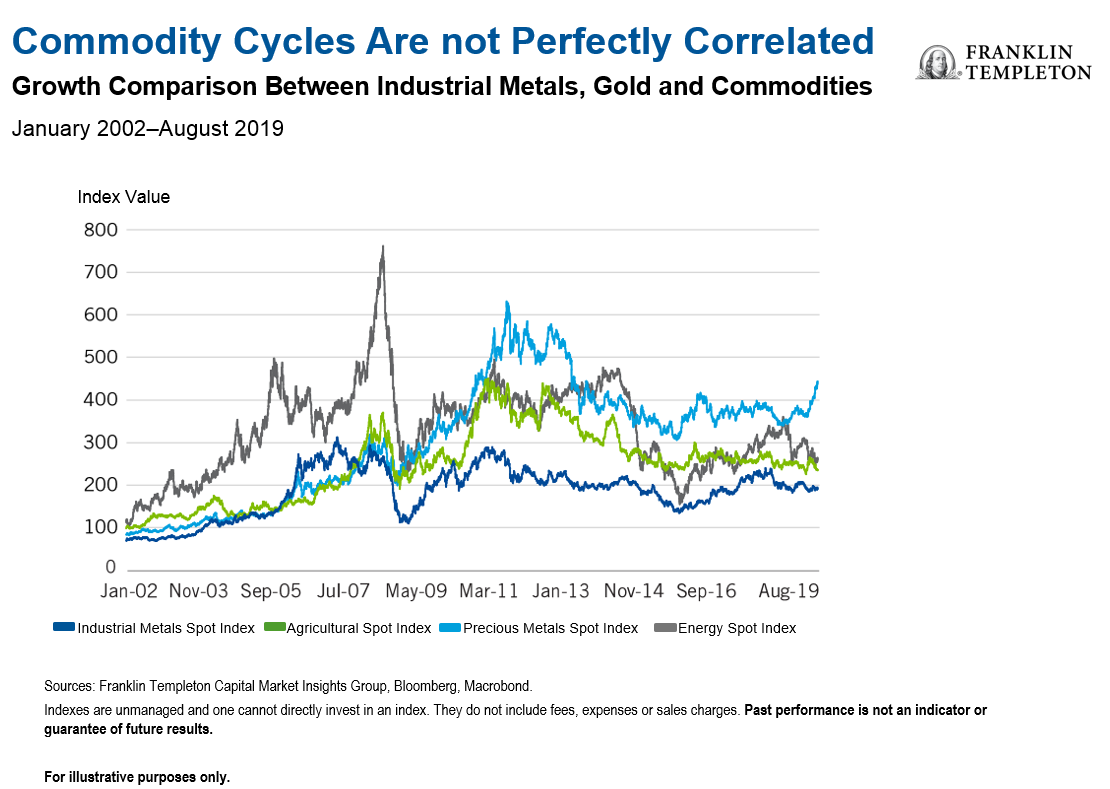

Broad commodity prices typically perform well in the latter stages of a business cycle, but they have been weak over the past year. They would benefit from any increased demand, driven by a renewed capital investment cycle. Commodities often see prices rise as a result of supply constraints, but this has been offset by demand concerns as China rebalances its economy toward domestic consumption. We retain a less optimistic view of real assets such as commodities, despite their potential diversification benefits.2

More specifically, certain commodities may offer alternative diversification benefits. Precious metals such as gold may not follow the same trend as industrial metals or broad commodities. At times of financial market or geopolitical stress, they can offer perceived safe-haven benefits and are viewed as a hedge against the debasement of fiat currencies.3 Our analysis of the drivers of precious metals shows that they would tend to fare better if the US dollar were to depreciate. Also, as an asset that generates no income, they compete better in a falling interest-rate environment. Currently, we find the specific attractions of gold somewhat more compelling than those of commodities more broadly.

What Are the Risks?

All investments involve risks, including possible loss of principal. The positioning of a specific portfolio may differ from the information presented herein due to various factors, including, but not limited to, allocations from the core portfolio and specific investment objectives, guidelines, strategy and restrictions of a portfolio. There is no assurance any forecast, projection or estimate will be realized. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Derivatives, including currency management strategies, involve costs and can create economic leverage in a portfolio which may result in significant volatility and cause the portfolio to participate in losses (as well as enable gains) on an amount that exceeds the portfolio’s initial investment. A strategy may not achieve the anticipated benefits, and may realize losses, when a counterparty fails to perform as promised. Currency rates may fluctuate significantly over short periods of time and can reduce returns. Investing in the natural resources sector involves special risks, including increased susceptibility to adverse economic and regulatory developments affecting the sector—prices of such securities can be volatile, particularly over the short term. Real estate securities involve special risks, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments affecting the sector. Investments in REITs involve additional risks; since REITs typically are invested in a limited number of projects or in a particular market segment, they are more susceptible to adverse developments affecting a single project or market segment than more broadly diversified investments.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

This information is intended for US residents only.

1. Duration is a measure of the sensitivity of the price of a fixed income investment to a change in interest rates. Duration is expressed as a number of years.

2. Diversification does not guarantee profit or protect against risk of loss.

3. Fiat currency is money that is not backed by a physical commodity. Most modern paper currencies, such as the US dollar and euro, are fiat money. They are issued by a government, which guarantees the validity of that currency for use in economic trade.

© Franklin Templeton Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits