Despite the US-China trade war, Franklin Templeton Emerging Markets Equity’s Sukumar Rajah doesn’t think the opportunity set for emerging markets is lost. He explains how a saturated smartphone market could create innovation opportunities in emerging market countries in Asia.

As tensions remain high over ongoing US-China trade negotiations, we recognize all eyes will be on the next development in the tit-for-tat tariff saga. Given the globalized nature of the supply chain, technology products are at the center of this dispute, causing concern among some emerging market investors. Some commentators have suggested US President Donald Trump’s decision to delay an increase in tariffs on some Chinese goods until December was based on a reluctance to see prices increase for mobile phones, laptops and video game consoles in the run-up to the US holiday season. However, US-Chinese tensions are not the only issue facing the technology sector.

Moreover, the deterioration in Korean-Japanese relations over the past year due to historical issues has also led to uncertainty in the technology sector. Japan has tightened rules on exports of three key materials to South Korea’s semiconductor industry.

While the trade spat between Japan and South Korea has yet to have a material near-term impact, it has led to lower visibility for the industry’s medium- to longer-term outlook as the timeline for a resolution between South Korea and Japan is unclear. If the Korea-Japan trade issues were to persist or worsen, crucial smartphone component makers such as Samsung Electronics and Hynix could face both production bottlenecks and challenges moving towards next-generation technology, as it will take time to localize and/or shift the supply change.

Despite this uncertainty, we remain positive on the structural trends in the technology hardware industry and still see pockets of opportunity within the smartphone industry, particularly for companies with strong innovation capabilities and financial characteristics.

Smartphone Manufacturers’ Fight for Innovation Crown

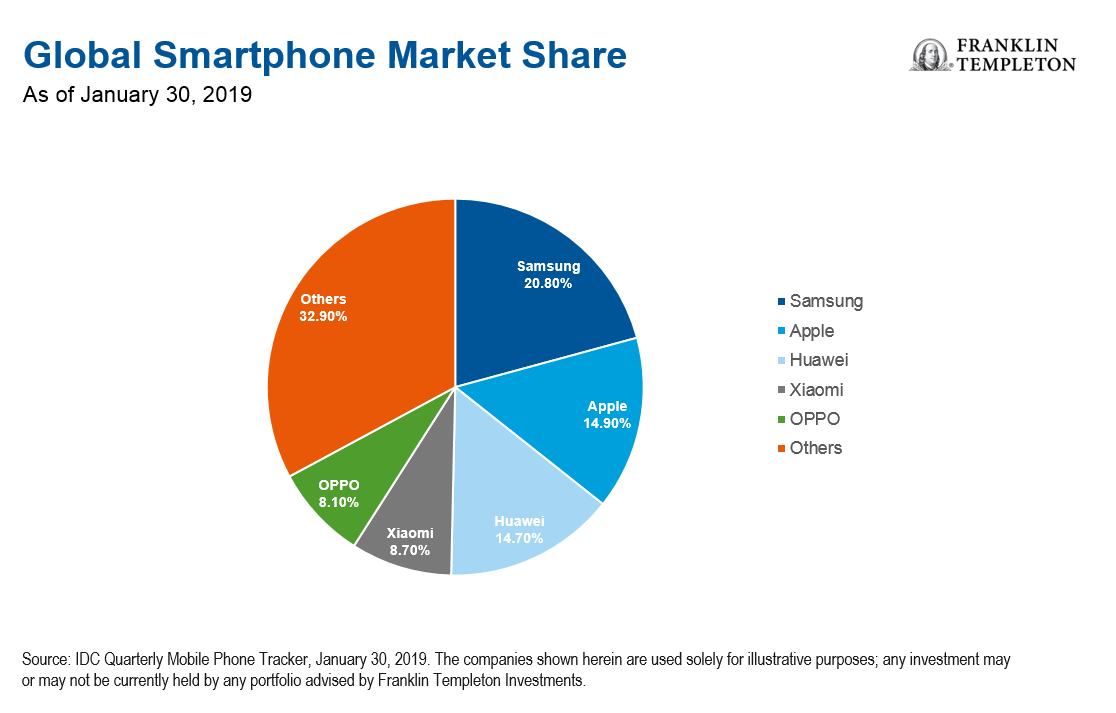

The growth in smartphone sales over the last decade has been phenomenal. By 2016, global smartphone sales had reached nearly 1.5 billion, enough devices for every fifth person in the world.1

Many smartphone manufacturers are preparing to launch devices with fifth-generation (5G) capabilities to tap into new 5G mobile networks that are being rolled out in countries such as South Korea. However, there are signs that the global smartphone market may have reached saturation—smartphone shipments appear to have fallen in the second quarter of 2019.2

While the unit growth of smartphones has slowed down, we expect smartphone manufacturers to continue to spend more per phone on improving select handset features to attract consumers and gain share. That race to enhance consumer value should create investment opportunities among handset component manufacturers.

One area we might see smartphone manufacturing companies looking for differentiation is in the quality of their in-phone cameras. Leading companies have featured an increasing number of cameras, more complex camera designs, as well as higher resolution lens sets in their smartphones.

This demand for continued innovations in the optical space benefits the technological leaders within the smartphone lens space as it allows them to continue to increase not only the volume but also the average selling price. This is because the fast pace of upgrades in the space allows the leaders to continue to maintain and even increase average selling price as the laggards struggle to catch-up to increasingly higher technological and quality requirements.

Trade War Stress Opens Market Share Opportunities

As US-Chinese trade tensions drag on, we see an opportunity for non-Chinese smartphone component competitors to gain a larger market share.

The reason why companies are relocating certain aspects of smartphone production and assembly to countries outside China boils down to rising costs of land, labor and general production of goods in China. The US-China trade war has accelerated this trend.

We’ve seen evidence multinationals are investing in suppliers with the ability to diversify away from the Chinese smartphone market and into low-cost manufacturing centers in Asia. Vietnam and India have been attractive relocation options. Both countries are home to thriving manufacturing industries and we think both stand to benefit as companies invest heavily in factories, equipment and supply chains. An increasing number of firms have set up cutting-edge research and development labs in Vietnam and India, where operational costs are typically lower than in advanced economies.

In India, cumulative foreign direct investment (FDI) inflows came to US$64 billion for the last year.3 Noida, a city on the outskirts of New Delhi, is now home to one of the world’s largest smartphone manufacturing hubs. According to industry estimates, that hub is set to produce 120 million units a year for one company alone.

Vietnam has also captured global attention. FDI investment accumulation came to US$19 billion for 2018.4 The former garment manufacturing hub has moved up the value chain to produce technology-related goods, including smartphone components. And, given the country’s geographical proximity to China, it makes it easier for companies to integrate Vietnam into often complicated smartphone supply chains.

While Vietnam’s prospects look promising, it does currently face some constraints to achieve the production capacity and capability of China. However, we see Vietnam and other smaller economies gaining market share, particularly in certain niche industries.

Tying it All Together

On balance, we believe that select segments of the smartphone industry offer long-term growth potential that could see investment for years to come. In our view, current trade tensions present opportunities for select companies that can navigate and sustain earnings power in an already saturated market.

As long-term investors, we seek to identify companies that we believe are likely to benefit from the structural trends discussed. We look for companies with high-quality management, strong innovation capabilities and robust cash flow generation. In our view, these characteristics will help these companies navigate and potentially gain market share in the more complicated operating environment borne out of the US-China trade war.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security.

Past performance is not an indicator or guarantee of future results.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Investments in fast-growing industries like the technology sector (which historically has been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement.

1. Source: International Monetary Fund, “A New Smartphone for Every Fifth Person on Earth: Quantifying the New Tech Cycle,” January 2018.

2. Source: IHS Markit, August 2019.

3. Source: Ministry of Commerce & Industry, July 2019.

4. Source: Vietnam’s Ministry of Planning & Investment, December 2018.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Alternative Investments Topics >