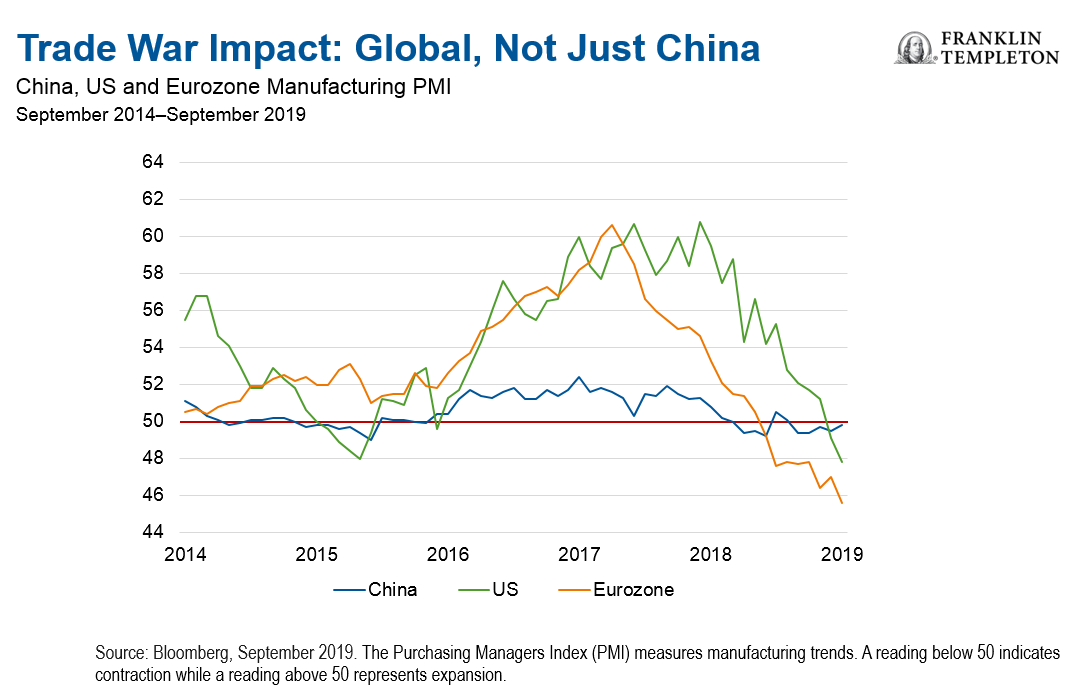

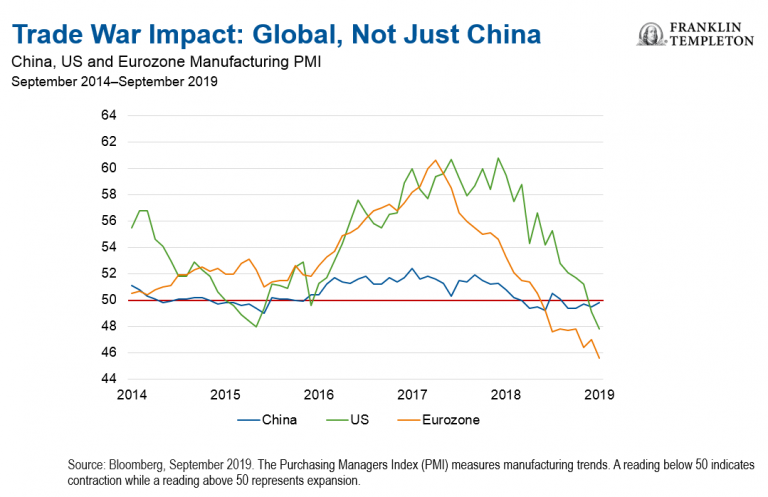

The US-China trade conflict has remained at the forefront of investor concerns in recent months, with both governments imposing tariffs on each other’s goods. While continued tensions are likely to result in continued market volatility, Franklin Templeton Emerging Markets Equity nonetheless finds reasons to be positive about emerging markets, with a more dovish global central bank backdrop offering support.

Three Things We’re Thinking About Today

- Finance Minister Nirmala Sitharaman announced a meaningful reduction in India’s corporate tax rates to help spur investment and boost growth in the country’s slowing economy. These changes came as a positive surprise and send a strong signal that the government has recognized the stress that corporates face from weak sentiment and subdued economic activity. While there has been some concern that the measure will result in a decrease in revenues, we believe there are mitigating factors that could reduce the loss in revenues. It is also important to note that the level of impact differs from sector to sector, particularly in sectors subjected to the highest effective tax rates. For instance, banking would be a key beneficiary as it is a full-tax paying industry. Most consumer companies also benefit from the corporate tax cuts. However, companies that currently receive tax relief or incentives from the local state government will not benefit as much. Overall, we think India’s corporate tax cuts should help spur investment over the longer term. We continue to favor companies that can benefit from secular growth drivers such as favorable demographics, infrastructure investment, urban and rural consumption growth and increasing income levels.

- China recently announced the removal of the investment quotas under its Qualified Foreign Institutional Investor (QFII) and RMB Qualified Foreign Institutional Investor (RQFII) programs. Increasing market access for foreign investors has been an ongoing process, as China undertakes structural reforms to its capital markets and allows foreign firms greater control over their assets. The move also follows a recent decision to allow foreign financial firms an option to take majority stakes in joint ventures. Certainly, the lifting of these restrictions on foreign investment in China was a welcome surprise. However, we think it is unlikely to have a dramatic impact in the short term because the existing quota system was underutilized. If we see further measures to liberalize and enhance market access that will encourage index providers such as MSCI and FTSE to increase the inclusion factor, we think China’s weighting in global benchmark indexes will invariably rise, and passive funds may have no choice but to step up their purchases of Chinese securities. While the overall immediate impact of China’s move to lift restrictions on foreign investment may not be drastic, we think the initiative signifies China’s commitment and long-term strategic decision to further increase access to its financial markets.

- Optimism surrounding the government’s economic agenda, including the key social security reform, has resulted in a more favorable climate in Brazil. While the country’s economic recovery has been slower than expected, with the government forecasting gross domestic product (GDP) to grow by 0.85% in 2019, government and central bank efforts could improve the country’s longer-term GDP growth potential.1 Inflation has also remained under control, allowing the central bank to lower interest rates to record-low levels to stimulate the economy. We believe the approval of pension system reform is key to stimulating investment and credit, which should help improve economic activity, as well as help significantly reduce Brazil’s fiscal deficit. A major privatization plan has also been announced, and we expect tax and other reforms that could improve the ease of doing business to follow. We maintain a positive outlook on the equity market and continue to have a favorable view on domestic-oriented themes, including financials and consumer-related sectors.

Outlook

The US-China trade conflict has remained at the forefront in recent months, with both governments imposing tariffs on each other’s goods. However, it should be emphasized any impact of the trade war has not been limited to China; rather, we have seen a global impact. While the resumption of trade talks expected in October indicates the willingness of both sides to work toward resolving outstanding issues, we remain cautious and expect continued volatility in the interim.

Political turmoil in the United States following the launch of an impeachment inquiry on the US President Donald Trump added to increased market volatility in the interim. However, reduced expectations of further escalation led investors to refocus on the US-China trade dispute and US Federal Reserve (Fed) policy. The Fed has reduced its benchmark rate twice in the last three months, with expectations rising for another rate cut by the end of 2019.

Slowing economic growth expectations, declining inflationary pressures and easing monetary policy in developed economies, including the United States and the eurozone, have led central banks in emerging markets (EMs) to generally turn more dovish this year. We expect this trend to continue with rate cuts in a number of larger EMs, including India, Brazil, Russia and Mexico. Coupled with improving earnings expectations and relatively undemanding valuations and dividend yields, we believe the outlook for EM equities remains attractive.

Emerging Markets Key Trends and Developments

Stock markets worldwide weathered a volatile quarter amid bumpy US-China trade negotiations and global recession fears. Central banks in several major markets, including the United States, cut interest rates to support economic activity. EM equities declined in US-dollar terms, while developed market stocks recorded a modest gain. EM currencies as a whole fell against the US dollar. The MSCI Emerging Markets Index lost 4.1% over the quarter, compared with a 0.7% return in the MSCI World Index, both in US dollars.2

The Most Important Moves in Emerging Markets in the Third Quarter of 2019

Most Asian markets finished the quarter lower as trade tensions clouded the economic outlook for the region. The US-China trade row remained in focus—both countries announced more tariffs in August but made conciliatory moves in September. An escalating trade dispute between South Korea and Japan added to market uncertainty. Stocks in China and South Korea retreated. In India, equities fell as the economy’s momentum faltered, though corporate tax cuts and other stimulus measures helped stem the decline. Bucking the downtrend, Taiwanese equities rose. Suppliers to Apple were lifted by encouraging pre-orders for the latest iPhone.

Markets in Latin America declined over the quarter with Argentina, Peru and Chile leading the way down. Although declining, Mexico and Brazil performed better than their regional peers. Despite a rebound in September, the Argentine market lost nearly half its value in US dollar terms over the three-month period on increased political uncertainty, debt re-profiling and the imposition of capital controls. Market turmoil, however, remained largely contained to Argentina. Brazil’s central bank lowered its key interest rate by 100 basis points to an all-time low of 5.5% to stimulate the domestic economy. Progress on the reform front further supported investor confidence. In August, Mexico’s central bank reduced its benchmark interest rate for the first time in more than five years, citing weak domestic growth and lower inflation.

The Europe, Middle East and Africa region as a whole lagged their EM peers in the third quarter. South Africa and Poland were among the weakest performers, ending the quarter with double-digit losses. Turkey and Egypt, in contrast, recorded strong returns, while the United Arab Emirates (UAE), Qatar and Russia also outperformed regional peers. The South African Reserve Bank left interest rates unchanged in September, following a 25 basis-point cut in July, as it continued to balance economic growth concerns and inflation expectations. A weaker South African rand also pressured returns in US dollar terms. Attractive valuations in Russia and the UAE supported investor sentiment with some comfort, while a larger-than-expected 150 basis point interest-rate cut amid a downward inflation trend drove returns in Egypt.

Important Legal Information

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. Past performance is not an indicator or guarantee of future results.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

1. There is no assurance that any estimate, forecast or projection will be realized.

2. Source: Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Tax Planning Topics >