In early 2018, Templeton Global Macro (TGM) published Global Macro Shifts issue 9—Environmental, Social and Governance Factors in Global Macro Investing [GMS-9]. The paper explored how we evaluate environmental, social and governance (ESG) factors in our macroeconomic research process and described the process of codifying the team’s research discussions into quantifiable scores. GMS-9 formally introduced our proprietary ESG scoring system, the Templeton Global Macro ESG Index (TGM-ESGI), which was one of the first methodologies in the sovereign fixed income markets to focus on projected changes in ESG scores as a source of investment insight.

Going forward, we intend to publicly update our TGM-ESGI scores on a recurring basis. This update contains a brief background on our ESG philosophy as well as an update on our methodology, notably including an improvement we made to adjust from overweighting S and G factors in previous iterations to an equal weighting of each of the E, S and G factors going forward. The paper also provides updated TGM-ESGI scores for 56 countries, along with brief case studies for three countries with improving projected scores and two countries with declining projected scores. As the sovereign ESG landscape continues to evolve, we also continue to look for ways to enhance and refine how we measure ESG factors and how we use that information to inform investment decisions.

TGM’s ESG Philosophy and Process

Below is a recap of the five key principles that define how TGM views the application of ESG factors in the research and investment process. These points reflect how TGM believes ESG can be best used by investors in the sovereign investment space.

- ESG is most effective when fully integrated into the other components of research, including traditional economic analysis and on-the-ground visits. These issues help form our core macroeconomic views on a country, and ESG factors are then expressed through analysis of economic issues such as growth and inflation.

- Focus is placed on forward-looking data points. Rather than current ESG performance, which is strongly correlated with income levels, we believe that momentum, or change in score, is the measure that truly matters for both investment performance and for where capital can be harnessed to generate the most positive impact.

- ESG is an important tool for identifying investment opportunities in addition to highlighting areas of risk. Within TGM, we are most interested in the “tails” signaling major ESG shifts in either direction.

- In order to benefit from ESG analysis, investors must have a sufficiently long time horizon. ESG factors guide a country’s fundamentals, which can be obfuscated in the short term by cyclical or temporary conditions. Conviction in the view and patience to see that view come to fruition are requisites to successful ESG investing.

- Emphasis as investors on a country’s long-term fundamentals provides an effective base from which to open communications with policymakers interested in discussing best economic practices. This dialogue is important for our ability to serve clients, and for government officials interested in the perspectives of private markets.

ESG Methodology

The TGM-ESGI is the composite of 13 subcategories (see GMS-9, page 4) determined to be material to macroeconomic performance, scored from 0–100. The research team assigns these scores by overlaying their views on specific global index scores and then providing projected numbers for how conditions are expected to change over the medium term. The final scores are calculated by applying an equal weight of 33% for governance, 33% for social and 33% for environment, with the projected change in scores simply being the projected score minus the current score.

Refinement of our environmental scoring

The equal weighting across the E, S and G scores represents a refinement in our scoring process—we previously weighted the E factor lower at 20% (with S and G each at 40%), given our view that environmental factors typically develop over relatively longer time periods. However, we have revised that assessment given that environmental factors have, in our view, recently had increasingly acute effects on a growing number of sovereigns. The adjustment to an equal weighting of E factors has had a modest effect on the overall country scores thus far and has not materially altered our current investment views. However, the potential for environmental factors to have a greater impact on our investment views going forward has increased due to the higher weighting.

Part of the drive to equal weight the scores is in recognition that environmental factors are becoming urgent concerns in major emerging countries like India and Brazil, among others. A number of countries have also been enduring above-average environmental events for decades, including countries in the Horn of Africa, with its droughts and concomitant lack of food security, or in certain Caribbean nations that remain exposed to devastating natural disasters but lack sufficient capacity to cope with their impacts. The longer-term impacts of environmental trends and (mis)management of the environment remain well-known concerns. For instance, a World Bank report found that environmental degradation costs India US$80 billion per year, a rate that would threaten the sustainability of future economic growth.1

Additionally, a European Environment Agency report concluded that climate change could cause a substantial drop in agricultural income in southern European countries over the next several decades.2 Research from the European Academies Science Advisory Council also indicated that climatological events such as droughts, forest fires and extreme temperatures have doubled since 1980, making their impacts on countries and populations increasingly damaging.3

But environmental issues should not be viewed only in isolation—in addition to the potential direct impacts on a sovereign, environmental factors may also have spillover effects on social and governance factors. In a sense, mismanagement of the environment can be considered a lack of governance: In Brazil for instance, fires raging in the Amazon rainforests will not only exacerbate climate change over the long run, but they also risk creating social discontent, causing lower approval rates for the government in the short term and potentially diverting attention away from important economic reforms.

Refinement of our benchmark selection

In order to construct the TGM-ESGI, our research team overlays their views onto a set of representative global indexes for each indicator. These indexes are used as benchmarks and are published by reputable sources like the World Bank or World Economic Forum, often as an aggregation of other sources of data. In the current update we have refined the overall set of indexes by replacing the ones formerly used for Unsustainable Practices and Infrastructure with indexes from the World Economic Forum4 (Global Competitiveness Report, Infrastructure) and the Social Progress Index5 (Environmental Quality), which we believe provide more comprehensive characteristics for our scoring process.

Countries with notable score changes due to methodology refinements

A result of the changed TGM-ESGI weighting is that countries with a deteriorating environmental score such as Brazil, India, Nigeria and the United States generally see a slightly stronger overall negative change in score, while countries that have projected improvements on environmental factors, like energy insecurity (Egypt, Ghana and Peru) see a somewhat positive change in their overall score.

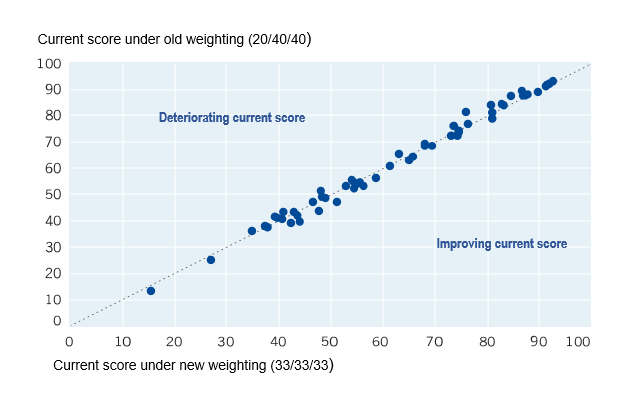

The major side effect that must be accounted for is that countries that are projected to remain stable on environmental factors but experience negative changes in governance or social areas (such as Poland, Hungary and Italy) actually see their projected change in ESG score modestly increase. Meanwhile, countries that are improving on social and governance factors (for example, Brazil and Indonesia) see their projected change in ESG score modestly decline. In all cases the impact on the projected-change scores is within the range of –1 to +1, which we deem to be an acceptable deviation. Exhibit 1 shows a tight linear regression for the effects the change in methodology has had on current scores.

New TGM-ESGI Current Scores Show a Tight Linear Regression with Former Scoring Methodology

Exhibit 1: Regression of August 2019 TGM-ESGI current scores using new weightings (33/33/33) vs. August 2019 TGM-ESGI current scores using old weightings (20/40/40). (As of August 2019)

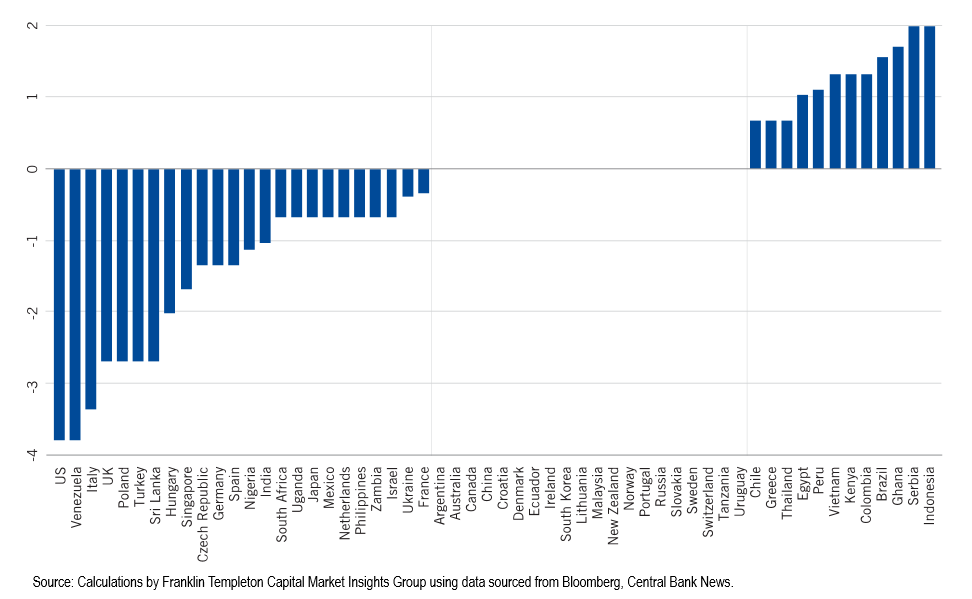

Countries with notable score changes due to changing ESG conditions

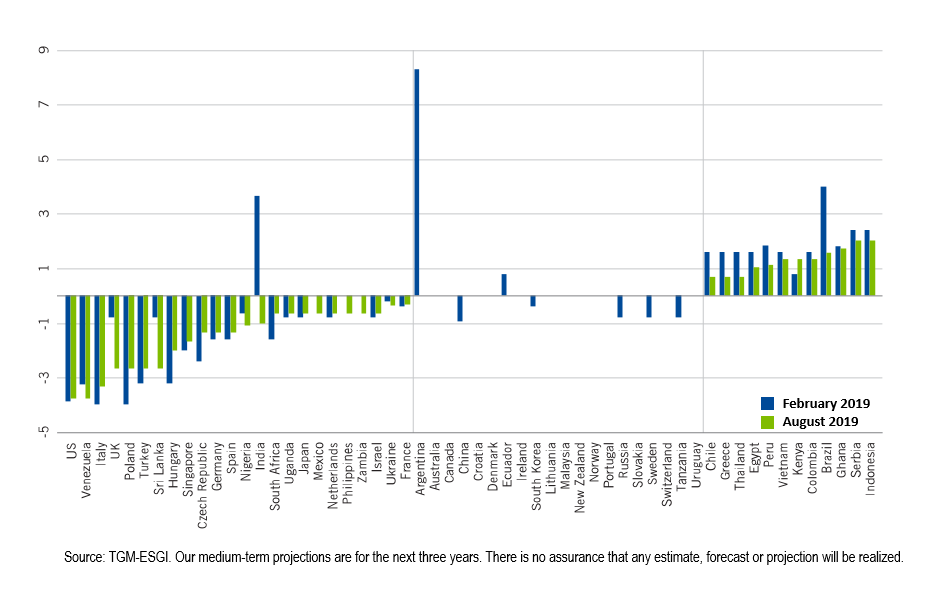

Compared to the February 2019 iteration of the TGM-ESGI scores, we now see fewer countries positively progressing on TGM-ESGI metrics. The average projected change in score was –0.1 in the February 2019 round of scoring, a number which has declined further to –0.4 in the latest update.

There are now 12 countries with a projected positive change compared to 15 in the last round, and the average projected change for these countries has come down from +2.4 to +1.3. For countries that are projected to deteriorate, the average projected score change has remained around the same as seen in the February 2019 scoring, at –1.6. Countries including India, Mexico, the Philippines and Zambia have shifted from having a projected neutral or positive ESG delta to showing a projected deteriorating score.

Additionally, the number of countries where we project no change in ESG scores has increased from 16 to 20, and now includes the likes of Russia, Argentina, Sweden, China and South Korea. Some of the countries in this grouping were previously assessed as deteriorating, but it should be noted that in such cases an “upgrade” to neutral can be either the result of a previously projected negative score improving, or the current situation in fact deteriorating to align with a previous negative projection.

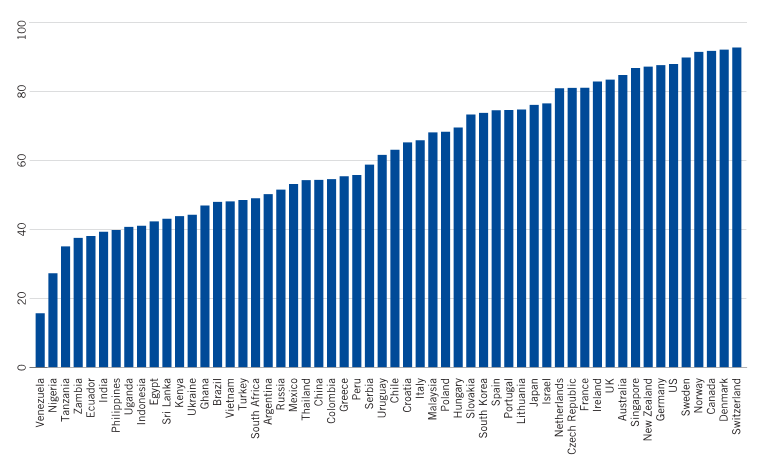

Updated TGM-ESGI Scores

The results from our latest 2019 scoring update are shown in Exhibits 2 and 3. We have continued to focus on a set of 56 countries, consistent with our February 2019 update.

Environmental, Social and Governance Scores by Country (TGM-ESGI)

Exhibit 2: TGM-ESGI scores: Current (As of August 2019)

Exhibit 3: TGM-ESGI scores: Projected change (As of August 2019)

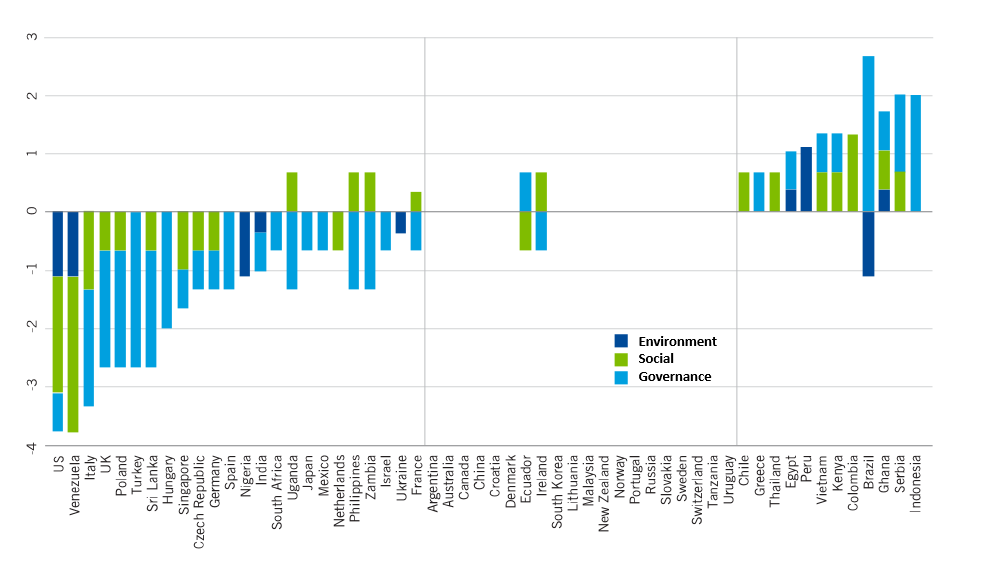

Exhibit 4: TGM-ESGI Scores: Projected change by E, S and G factors (As of August 2019)

Exhibit 5: Projected TGM-ESGI score comparison: February 2019 vs. August 2019 (As of August 2019)

Case Studies

In the following case studies, we highlight a few of the countries that are seeing some of the more significant projected positive changes (Indonesia, Ghana and Brazil). We also review two countries with projected negative changes (UK and India). India is notable because it represents a significant reversal from our last round of ESG scores in February 2019.

Three countries with projected improvements in ESG scores

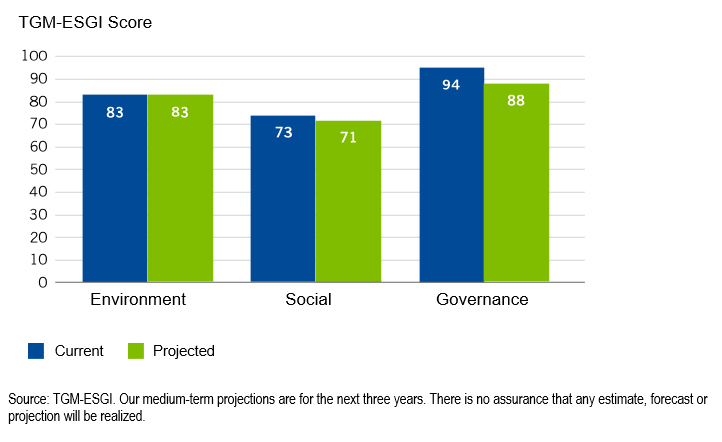

Indonesia: Full speed ahead with important reforms

- President Joko Widodo won a second term in April, opening the door to further progress on his reform agenda, which includes closing the infrastructure gap with other emerging markets, improving the ease of doing business and addressing corruption. Going forward, there will likely be increasing emphasis on improving the lives of rural Indonesians by reducing poverty and inequality, as well as further expansion of basic health insurance.

- Reforms had stalled pre-election, though significant progress had at that point already been made, with Indonesia jumping from 120th to 73rd on the World Bank Ease of Doing Business ranking between 2014 and 2019.

- Economic management in Indonesia remains orthodox, with an emphasis on prudent budgets and consistent monetary policy. The number and quality of technocrats within the administration has strengthened.

- Social cohesion in Indonesia is expected to deteriorate, putting the country at risk of declining religious diversity and lower social tolerance.

- Indonesia performs poorly on environmental factors, with no significant positive changes currently projected. The country is exposed to natural disasters, including volcanoes, flooding and droughts, while slash and burn tactics are used to clear vegetation for crops, producing gases and thick smog.

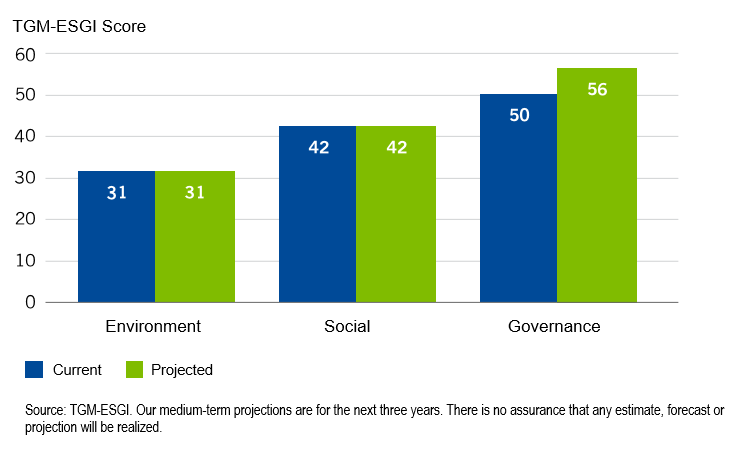

Exhibit 6: Indonesia: Current and projected conditions (TGM-ESGI) As of August 2019

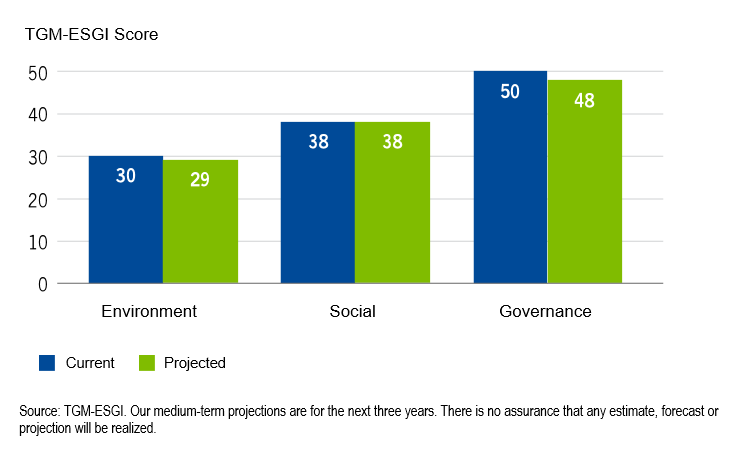

Brazil: Critical reforms underway, but deforestation of the Amazon is concerning

- The economic crises and political scandals of the past have sparked a period of significant reform in Brazil. The economy is recovering, benefiting from already passed reforms addressing labor rigidities, corruption, and privatization of state-owned enterprises, which should help improve the business climate.

- While there is broad consensus on the need for reforms in areas like social security (and potentially tax reform and trade liberalization), political risk is currently high, and we see less support for other reforms due to frictions between the different government branches.

- Social cohesion remains at a low level, as society is still dealing with the ramifications of Lava Jato—a corruption scandal also known as Operation Car Wash—leading to general distrust of the establishment. Moreover, the new government has brought far-right sentiment into the mainstream, though institutions such as the Supreme Court are pushing back against that shift.

- Brazil has in the past compared relatively favorably to emerging market peers on environmental sustainability; however, the current administration’s lax environmental policy could allow deforestation in the Amazon to proceed at an unsustainable pace.

Exhibit 7: Brazil: Current and projected conditions (TGM-ESGI) As of August 2019

Ghana: One of Sub-Sahara Africa’s strongest democracies, with improved fiscal management and heightened energy production

- Ghana is one of the most stable democracies in Sub-Saharan Africa. The country tends to rank higher than its peers on indexes for global peacefulness and media freedom. It is rich in natural resources and has a relatively advanced industrial base. Moreover, its elections typically focus more on policy than ethnicity, which is not always the case in neighboring countries.

- The government of President Nana Addo Dankwa Akufo-Addo has succeeded in achieving primary surpluses and is committed to prudent fiscal policy, as well as orthodox monetary policy. Moreover, the government has led efforts to clean up the country’s struggling financial sector, which was previously plagued by a lack of governance and improper lending. Both factors should help to improve business conditions over the medium term.

- Economic reforms should enhance investments in infrastructure, improving road, rail, air transport and ports, while boosting Ghana’s status as a transport hub in West Africa.

- Ghana’s agriculture sector (which employs more than half of its working population) is acutely susceptible to climate shocks, facing issues like drought and floods. Moreover, illegal gold mining has wrought severe environmental damage, including in areas used for cocoa cultivation.

- We are projecting energy security to improve further as the domestic power sector benefits from heightened natural gas production.

Exhibit 8: Ghana: Current and projected conditions (TGM-ESGI) As of August 2019

Two countries with projected deteriorations in ESG scores

UK: Pervasive uncertainty over economic outlook due to Brexit

- In the UK, pervasive uncertainty over the long- and near-term economic outlook will remain until there is more clarity around Brexit. By October 31, 2019, the UK must choose to postpone its departure from the European Union (EU), ratify an exit treaty or opt for a “no-deal” Brexit.

- Social cohesion and effectiveness of government are projected to deteriorate as Brexit negotiations have become more contentious. Society is highly divided. Different polls show people who favor “Remain” and those who favor “Leave” to be within a small margin. The social cohesion risk of Brexit is not limited to England—polls on remaining in the UK are highly divided in Scotland.

- Brexit will likely make the UK less competitive in EU markets (which received 46% of its exports in 2018), particularly in a no-deal scenario. In addition, there could be possible reductions in foreign investment.

- The UK gets a top score on numerous ESG metrics like infrastructure, corruption and the policy mix, and it ranks close to the top with direct peers like Australia and Singapore. The slight deteriorations will bring it closer to the likes of the Netherlands or the Czech Republic.

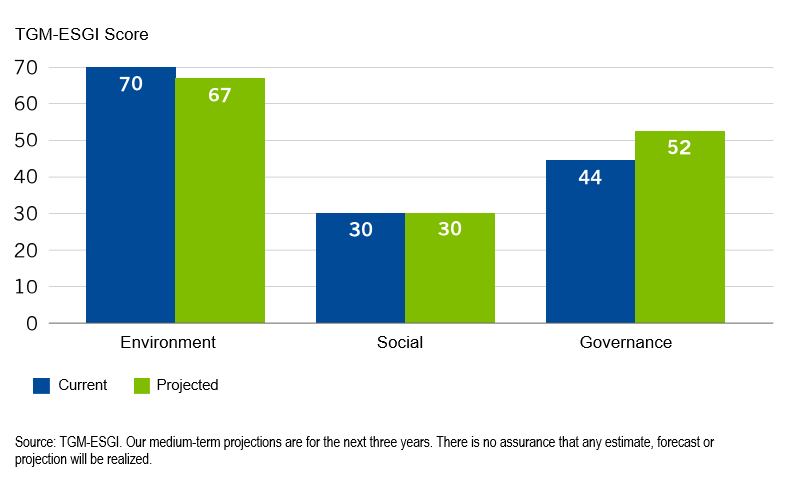

Exhibit 9: UK: Current and projected conditions (TGM-ESGI) As of August 2019

India: Policy continuity under Modi, but mounting economic and environmental challenges

- The size and scale of the May 2019 election victory has earned significant political capital and brought continuity in the policy path under the leadership of Prime Minister Narendra Modi. However, this capital will need to be deployed quickly, as economic challenges mount while counter-cyclical policy to respond to a slowdown has appeared inadequate.

- Institutional independence in India has appeared to weaken as the influence of the government on institutions has recently increased.

- Social cohesion remains in a delicate balance given a history of conflict between Hindus and Muslims. High crime rates, plus income and caste inequality, remain a significant challenge for becoming an inclusive and progressive society.

- Environmentally, pollution remains a major issue as Indian cities are ranked among the worst for air pollution. Twenty-two of the world’s thirty worst cities for air pollution are in India, according to Greenpeace and AirVisual analysis (report based on 2018 air quality data from public monitoring sources).

- India ranks 13 among the 17 worst-affected countries where water stress is “extremely high,” according to the World Resources Institute. This means that the country is running out of ground and surface water.

- The government has increased its focus on environmental issues and has launched schemes to tackle water and air quality concerns. But given the magnitude and the depth of these challenges, far higher resources would need to be allocated on an urgent basis.

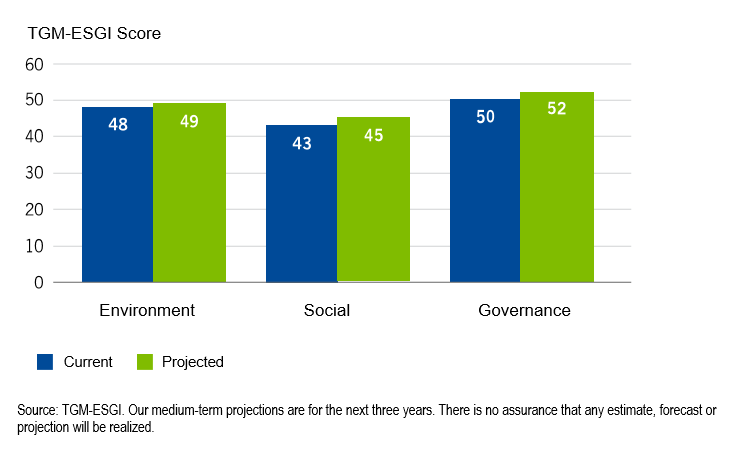

Exhibit 10: India: Current and projected conditions (TGM-ESGI) As of August 2019

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

Important Legal Information

This material reflects the analysis and opinions of the authors as of October 8, 2019, and may differ from the opinions of other portfolio managers, investment teams or platforms at Franklin Templeton Investments. It is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed and the comments, opinions and analyses are rendered as at the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market, industry or strategy.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

1. Source: The World Bank, “India: Green Growth—Overcoming Environment Challenges to Promote Development,” March 6, 2019.

2. Source: European Environmental Agency, “Climate change threatens future of farming in Europe,” September 4, 2019.

3. Source: European Academies Science Advisory Council, “New data confirm increased frequency of extreme weather events, European national science academies urge further action on climate change adaptation,” Press Release, March 21, 2018.

4. “The Global Competitiveness Report” is an annual report published by the World Economic Forum (WEF), which ranks countries based on a global competitiveness index. The “infrastructure” report is used as the benchmark for the Infrastructure factor in the TGM-ESGI Social category as of August 2019, due to its comprehensive integration of macro and microeconomic factors in its competitiveness scoring. It replaces the previous benchmark used for the TGM-ESGI which was the “World Bank Logistics Performance Index, Infrastructure,” an index that is more focused on the logistics of infrastructure.

5. “The Social Progress Index” measures the extent to which countries provide for the social and environmental needs of their citizens. The index is published by the Social Progress Imperative. It is used as the benchmark for the Unsustainable Practices factor in the TGM-ESGI Environment category as of August 2019, due to its scope and field-leading expertise in the study of social and environmental development within countries. It replaces the previous benchmark used for the TGM-ESGI which was the “Yale Environmental Performance Index,” an index that is more focused on ranking countries by performance indicators, and employs less direct local research than the Social Progress Index.

© 2019. Franklin Templeton Investments. All rights reserved.

© Franklin Templeton Investments

More Factor-Based Investing Topics >