Volatility has receded, but stocks have made little headway due to the lack of enthusiasm surrounding a trade truce between the United States and China.

Economic “surprises” have been mixed across the board and key indicators have not confirmed a resumption of strength; while the monetary policy outlook remains elusive.

The timeline for a Brexit deal has been fluid, yet support is building along with a somewhat brighter forecast for the U.K.’s economy.

“An investment in knowledge pays the best interest.” ― Benjamin Franklin

Sound and fury

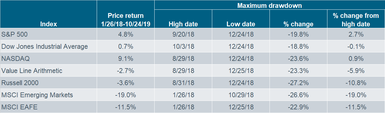

While volatility has subsided of late, U.S. stocks remain in a wide trading range and have yet to surpass their July highs. Mixed earnings and economic data; persistent skepticism surrounding a U.S.-China trade truce and Brexit; and monetary policy’s perceived impotence have kept equities around the world from breaking out to the upside. U.S. stocks are at relatively strong levels and continue to crawl towards new highs, but myriad non-confirmations have revealed that little progress has been made in the past 21 months. Since January 26, 2018, nearly every major global index has experienced a bear market at some point; and some have failed to come back to their prior highs. You can see from the table below that U.S. large-cap and technology stocks have eked out positive gains up until now, but U.S. small-cap and international stocks have been left behind; along with the Value Line Arithmetic Index, which includes 1,700 stocks and represents a broader swath of the U.S. stock market

Performance Since January 2018 Has Been Quite Mixed

Source: Charles Schwab, Bloomberg, as of 10/24/2019. MSCI data as of 10/23/2019.

With the exception of small caps’ weakness, U.S. stocks overall have managed to stay above their January 2018 highs; yet the current bull market has had some weak underpinnings—not least being extreme bouts of volatility (notably, the near-bear market in the fourth quarter of 2018) and defensive sectors’ leadership. As you can see from the following table, sectors that are considered “safe havens” have led equities higher; showing that underlying market behavior is reflecting ongoing economic uncertainty.

Defensive Sectors Continue to Lead Cyclicals

Source: Charles Schwab, Bloomberg, as of 10/24/2019.

An update (or lack thereof) on trade

Trade tensions have cooled since the Chinese delegation’s visit to Washington in early October. Optimism initially soared on the heels of President Trump’s announcement of a “phase one” trade deal; but investors dialed back their exuberance after realizing that the agreement had yet to be put into writing. Not to mention, the major issues surrounding Huawei, technology transfers, and intellectual property theft have not been meaningfully addressed. The increase in tariffs from 25% to 30% on $250 billion in Chinese goods was delayed, but the already-imposed tranches remain in place; and the December 15 round—which directly hits consumer goods—is still set to take effect. You can see from the chart and table below that the combination of imposed and threatened tariffs still has the potential to shave over a full percentage point off of U.S. gross domestic product (GDP) growth; thus confirming that a truce does little to address weaker domestic growth.

Tariffs’ Impact on Economic Growth

Source: Charles Schwab, Cornerstone Macro, as of 10/24/2019.

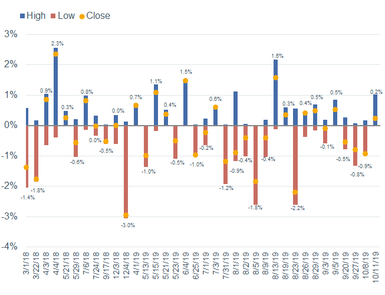

Given U.S. stocks’ rather muted activity since the announcement of the trade truce, it appears that investors have sifted out the reality that very little progress appears to have been made; and have thus maintained a cautious stance. Yet, despite a lack of increasing tensions in the past couple of weeks, reactions to trade developments have been nothing short of intense since the start of the trade war. As you can see in the chart below, trade news has driven larger market swings, with the S&P 500 “traveling” (on average in absolute value terms) 40 points on trade news days; versus 28 points on non-trade news days.

Trade News Drivers Larger Market Swings

Source: Charles Schwab, Bloomberg, as of 10/24/2019. Close represents the percentage change from the opening price that day (as indicated by each dot and corresponding data label), not the closing price of the preceding trade day.

Absent a comprehensive trade deal—one that encompasses the major structural issues at stake and addresses both sides’ list of desires—we continue to foresee bouts of market volatility that could continue to spread throughout the confidence channels. Business confidence has taken a hit, and an increasing number of companies continue to cite tariffs/trade on earnings calls. Capital spending intentions also remain under pressure, as supply chain disruption and persistent uncertainty have forced C-suites to adopt defensive postures. Additionally, should the December tariffs kick in, we may soon start to see the business malaise wade into the consumer side of the economy, given that the goods targeted for those tariffs are heavily consumer-oriented.

Are earnings estimates to be believed?

Earnings season is well underway and this quarter’s S&P 500 “blended” (reported plus expected) year-over-year growth estimate—as measured by Refinitiv—is -2.3% (-0.2% if you exclude the energy sector). Companies managed to post gains in the first half of the year, but slashed expectations set the bar quite low. Notwithstanding this year’s harsher macroeconomic environment, the year-over-year comparisons are automatically difficult due to the tax cuts’ boost to 2018’s earnings. So far, 80% of companies have beaten estimates this quarter, but the rub is that the beat rate tends to come down as more companies post results. [For more on earnings, see It’s Late: So Says the Profits Spread and Leading Indicators].

Surprise: party of one

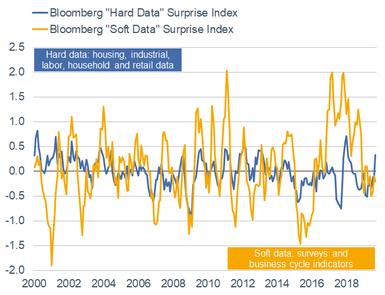

Economic data has been mixed of late, with “soft” and “hard” measures telling different stories. You can see from the chart below that soft data surprises—which measure whether surveys and business cycle indicators are better/worse than expected—have remained in negative territory; whereas hard data surprises—which track whether actual reported data are better/worse than expected—have turned positive and taken the lead.

Hard Data Reigns Supreme for Now

Source: Charles Schwab, Bloomberg, as of 9/30/2019.

Soft data has been pulled down by an increased souring of sentiment; as surveys like the ISM Manufacturing and Non-Manufacturing Purchasing Managers’ Indexes (PMIs), and The Conference Board’s Leading Economic and Consumer Confidence Indexes fell below expectations in September. Hard data hasn’t caught down, though; as new home sales, building permits, and the unemployment rate beat consensus estimates last month. The uptick in overall economic surprises as measured by the Citi Economic Surprise Index was driven mostly by more lagging indicators. On the other hand, leading business cycle components—which are housed in the Bloomberg Surveys & Business Cycle Indicators Surprise Index—have failed to move into positive territory; thus signaling that we are not yet out of the woods.

Cutting it out

Over 90% of investors are pricing in a rate cut at the next Federal Open Market Committee (FOMC) meeting later this month—due to myriad geopolitical uncertainties and the apparent weakness that has spread from manufacturing into services. Despite the FOMC’s decision to cut rates twice this year, economic activity has failed to pick up, which has aided the argument that rate cuts are unlikely the full elixir for what ails the broader economy. Separately, some have posited that larger structural issues—falling inflation expectations, aging populations, and muted productivity—have somewhat diminished the effects of monetary policy. As global nominal neutral rates have continued to fall due to aging populations’ rush into bonds for safety, central banks have felt the need to move further towards their lower bound. This has greatly reduced their ability to lift inflation; thus rendering monetary policy less effective with regard to the economy—although still effective in boosting asset prices. This has sparked a question as to whether more fiscal levers need to be pulled to combat future economic slowdowns.

Brexit: Ending phase 1

Two key votes in the House of Commons this week revealed that a majority now exists in favor of Prime Minister Johnson’s Brexit deal; but not for the Withdrawal Agreement Bill’s (WAB) passage through the House of Commons, or the House of Lords, in time for the U.K. to leave the European Union (EU) by October 31. This is the first time Parliament has expressed a majority in favor of any Brexit deal—although that support appears to be conditional on the ability to attach some amendments to the bill.

Johnson has asked Parliament to approve an election on December 12—after which he hopes to win a majority to ratify his deal without changes. Parliament will vote on October 28 whether to allow the election; a two-thirds majority is required. If the election fails, as has been the case during the prior two instances, any amendments would have to pass through Parliament; and it is possible that no binding or material changes would be put in the agreement already established with the EU. In particular, an amendment that would attach a second referendum to the WAB appears unlikely to pass. In any case, the EU will likely grant the U.K. a three-month extension to January 31 to allow time for an election, a debate on the WAB, and room to plan next steps.

The good news is that the risk of a hard Brexit has fallen, while a soft version could occur sometime over the next three months. The U.K. will remain in a customs arrangement with the EU until December 2020 (which could be extended), or until a better solution is found to keep the Irish border open. As a result, there will be no need for tariffs, quotas, or land border checks between the U.K. and the EU. Importantly, most U.K. financial services companies will be able to access the EU market, as long as the U.K. maintains similar regulations to the EU.

Brexit will soon be transitioning to a new phase. Once an agreement is passed, another series of potentially contentious negotiations may begin surrounding the post-“customs arrangement” trading relationship between the U.K. and EU. Additionally, all of the other U.K. trade agreements would need to be re-negotiated, including that with the U.S. (with which the U.K. has a trade deficit). Yet, this may not hamper a return of business spending, which has slowed markedly since the referendum in 2016 and subsequently turned negative in 2018.

U.K. Business Investment Has Stagnated

Source: Charles Schwab & Co, Bloomberg data as of 10/23/2019.

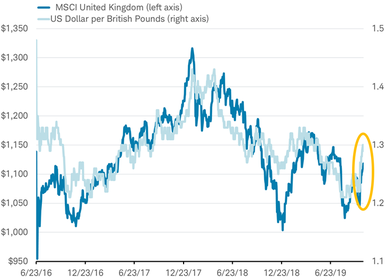

This development puts the U.K. on track to avoid the start of a deep recession in the fourth quarter—what would have been the result of a “no deal” Brexit on October 31—and may set the stage for some improvement in growth momentum. In its latest quarterly update, the International Monetary Fund (IMF) forecasted a slight acceleration in U.K. growth next year. Reflecting the broader global economic backdrop, U.K. manufacturing is weak and economic support has come primarily from consumer spending; rising wages and slowing inflation have supported consumers’ purchasing power. While Brexit hasn’t been a major worry for global markets this year, the lessened risk of a shock to economic growth and the financial system is a welcome relief. U.K. stocks and the pound have rallied in the past couple of months, pricing in the emerging signs of a deal.

Recent Rally in U.K. Stocks and Pound

Source: Charles Schwab & Co., Inc., MSCI and Factset data as of 10/23/2019.

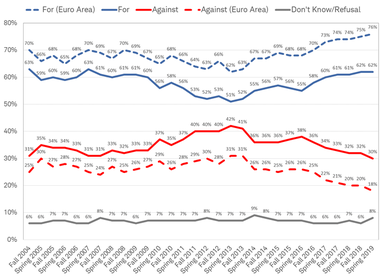

One surprising outcome of the Brexit battle has been the revival in support for the Eurozone throughout Europe. Rather than signal the broader desire for a breakdown of integration in Europe (thus posing risks to global economy and financial system), Brexit has coincided with a 20-year high in support for the economic and monetary union. You can see below that being part of Europe has never been so popular.

Support for the Euro at High Levels

Percentages reflect responses to question: “What is your opinion on: A European economic and monetary union with one single currency, the euro?” (Euro Area) refers to citizens of the 19 Eurozone member countries as a subset of the 28 European Union members. Source: Eurobarometer September 2019.

So what?

While volatility has receded lately and geopolitical tensions haven’t heated up, little-to-no progress has been made on a comprehensive U.S.-China trade agreement; while the timetables for Brexit continue to shift. Although U.S. stocks are trading near their all-time highs, investor hesitation has persisted due to mixed economic data, the questionable effects of monetary policy and trade uncertainty. We continue to recommend that investors use volatility to rebalance and stay near their strategic asset allocations; maintaining our neutral stance on U.S. equities (with a bias toward large caps at the expense of small caps), and our neutral stance on both developed international and emerging market equities.