Data science has brought investors powerful new tools to help generate returns, so is there still need for a human touch? Franklin Templeton Fixed Income CIO Sonal Desai weighs in on the role of quantitative science within the active-passive investment debate.

As data science has made its way into investment management, it has generated a polarized debate—as fierce as the one between passive and active investment and, in my view, a lot more interesting and consequential.

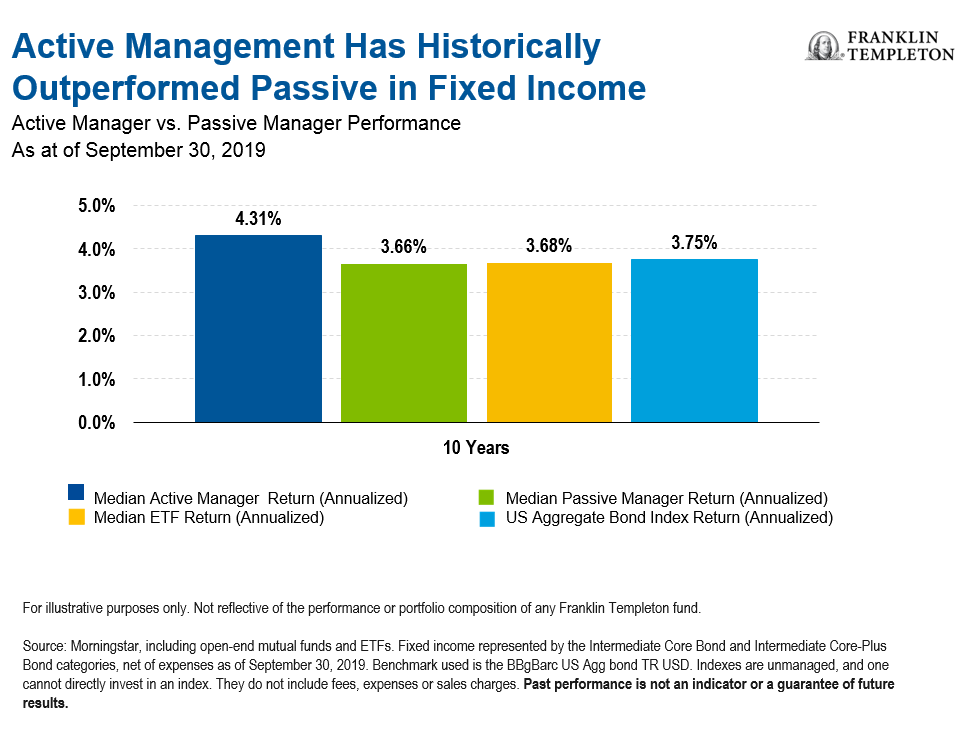

Before I get to it, though, let me point out one thing on the active versus passive choice: in the fixed income world, active investment has historically beaten passive hands down. Over the past 10 years, the median active fixed income investment manager has beaten the median passive strategy by 65 basis points1 (bps) and median exchange-traded fund (ETF) strategy by 63 bps on an annualized basis (as of September 30, 2019, with manager performances measured net of expenses).

So, in fixed income, active investment historically has been the winning strategy. The question is what kind of active investment works best.

Quantitative Science—Actively Adding to Fixed Income Decisions

Advocates of the quantitative (or “quant”) approach argue that it beats traditional, fundamentals-based investing. They say their algorithms can identify rules-based factors that generate alpha2 more effectively and reliably. Supporters of a more traditional active approach counter that experienced economists and credit analysts will always have the edge over algorithms that mine data without context.

I think the entire active versus quant debate is a false dichotomy.

At Franklin Templeton Fixed Income Group, we bring the two approaches together. We believe the future of fixed income investing lies in marrying quantitative science with fundamentals-based active management.

We have just released a white paper outlining how we do it, and why we believe it’s by far the best strategy for us.

Top-down fundamental analysis plays a crucial role in our approach (I am an economist, after all). Our process starts with the macroeconomic outlook our economists have built, articulated in a range of economic forecasts. The quant and data science teams then jump in and translate the economists’ views into standardized macro variables that feed into a regression tree algorithm. This translates the macroeconomic outlook into sector views—making it easier to compare and debate sector views. In turn, this forms the basis for our proprietary sector allocation process.

Meanwhile, our factor models generate prioritized buy and sell recommendations within corporate credit, independently from the analysts. Then we compare the “best ideas” from factor models and credit analysts on an industry-by-industry basis. The process is especially useful when the fundamental views of our analysts diverge from the models’ recommendations—that’s when we learn the most. Through debate and reconciliation, we get to our highest-conviction investment ideas and positions.

Working together, our analysts and the models our quants generate challenge each other and seek to make each other better.

An example I love is how we developed our dynamic factor tilts: our data scientists have programmed a gradient-boosting algorithm to incorporate a series of macroeconomic variables that capture the credit cycle. The algorithm can predict the relative performance of different factors (in the value, quality and momentum categories) based on the evolution of the credit cycle indicators. It can then tilt the factor weights, giving more power to those factors that we think should perform best based on the evolution of the credit cycle.

Data science has brought us a powerful new set of tools to generate excess returns. But algorithms are not enough; algorithms cannot drive themselves in noisy financial and economic environments—they need the support of human reasoning and experience.

The future of fixed income has already arrived—it lies in successfully marrying quantitative science with fundamentals-based active management. Today that’s what we at Franklin Templeton Fixed Income Group do. Our economists, analysts, data scientists and portfolio managers work together. They push and challenge each other, and create a virtuous loop between quantitative and fundamental analysis.

It’s not easy—but this is the future.

What used to be a simple two-dimensional process (top-down and bottom-up) becomes a four-dimensional chess game as fundamentals and quants feed into each other. That’s where we find the insights and the competitive edge to navigate an especially uncertain and challenging investment environment.

Important Legal Information

This material reflects the analysis and opinions of the authors as of October 28, 2019, and may differ from the opinions of other portfolio managers, investment teams or platforms at Franklin Templeton Investments. It is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed and the comments, opinions and analyses are rendered as at the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market, industry or strategy. The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value.

ETFs trade like stocks, fluctuate in market value and may trade at prices above or below their net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price, not their Net Asset Value (NAV), on the exchange on which they are listed. Shares of ETFs are tradable on secondary markets and may trade either at a premium or a discount to their NAV on the secondary market.

Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

______________________

1. A basis point is a unit of measurement. One basis point equals 0.01%.

2. Alpha is a risk-adjusted measure of the value that a portfolio manager adds to or subtracts from a fund’s return.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Active Management Topics >