Macro Factors and Their Impact on Monetary Policy, the Economy, and Financial Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLong Term Growth Outlook for Global Economy Dims

In October the International Monetary Fund (IMF) lowered its 2019 GDP forecast to 3.0% from 3.2% in July. This represents a marked slowing from global growth of 3.8% in 2017. The primary driver of the slowdown has been a retrenchment in global trade and business investment in response to the ratcheting up of trade tariffs since early 2018. Global trade has been a significant engine for the global economy for the past 70 years rising from just 5% of global GDP to almost 25%. This trend was supported by a decline in global trade tariffs and trade agreements that opened up individual country’s economies to the global economy. The rising tide of trade ushered in a period of competitiveness that resulted in lower inflation and access to products from around the world for consumers. The surge in global competitiveness pushed companies in advanced economies to lower their cost of production and shift production outside their domestic economy to take advantage of cheap labor. In advanced economies the migration of production resulted in the loss of millions of middle class jobs, even as the increase in globalization lifted hundreds of millions of workers in Asia and elsewhere out of extreme poverty. For those adversely impacted as factories closed and jobs were lost in advanced economies, the reduction in extreme poverty is an abstraction that had and continues to have little meaning.

The United Nations defined extreme poverty in its 1995 report for the World Summit for Social Development. “Extreme poverty is a condition characterized by severe deprivation of basic human needs, including food, safe drinking water, sanitation facilities, health, shelter, education and information. It depends not only on income but also on access to services.” According to estimates by the United Nations there were 1.9 billion people living in extreme poverty in 1990, 1.2 billion in 2008, and 734 million in 2015. As the number of those living in extreme poverty plunged, global population grew from 5.327 billion in 1990 to 7.379 billion in 2015. Between 1990 and 2015 the percent of global population living in extreme poverty fell by 72%, declining to 9.95% from 35.6% in 1990. The number of those not living in extreme poverty has soared due to population growth and the decline in extreme poverty. Nothing like this has ever occurred in human history and the increase in global trade and globalization played a significant role in making it happen.

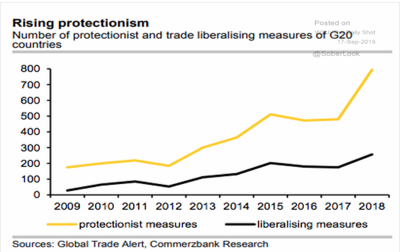

The trade winds which for decades filled the sales of global growth have shifted. In the decade leading up to the financial crisis World GDP grew consistently above 4.0% except for a brief dip in 2001 – 2003, according to the World Bank. In 2009 World GDP plunged to -1.70% before rebounding to 4.28% in 2010. But in 2011 and 2012 World GDP slumped to less than 3.0% and has barely climbed above 3.0% in the years since. The World Bank expects World GDP to increase 2.6% in 2019 compared to the IMF’s forecast of 3.0. Although the world economy has expanded close to 3.0% annually since 2010, the deceleration doesn’t feel good, especially relative to the pre-crisis experience and expectations. With growth coming up short many countries chose to look at trade critically, which is an easier target than addressing domestic issues that could be politically challenging. Beginning in mid 2012, and probably partly in response to slower growth globally, G20 countries in aggregate moved to protect their domestic economies by adopting protectionist measures at a faster pace than measures to liberalize trade. This trend accelerated as the U.S. – China Trade War erupted in 2018 and global growth slowed further. This shift away from globalization is occurring as the rise in populism and nationalism has taken root around the world. This represents a tidal change that is not likely to be reversed, even if a cease fire is achieved in the Trade War since other factors are also at work.

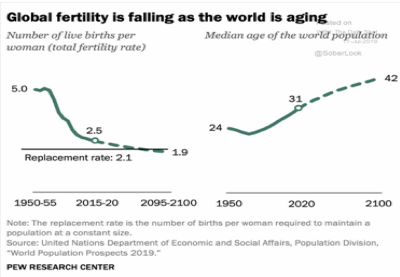

To state the obvious, economic growth depends on having enough bodies to produce the goods and services every society needs. The major economies are facing a demographic headwind in coming decades that will keep economic slower than in the past when birth rates were far higher. Since 1950 the global fertility rate has been cut in half, falling from 5.0 births per woman to 2.5 in 2015. By the end of this century the United Nations projects it will fall below 2.1 which is the Replacement rate. If this comes to pass global population will contract possibly for the first time since the Bubonic Plague swept across Europe in 1347 – 1451 killing almost 100 million people.

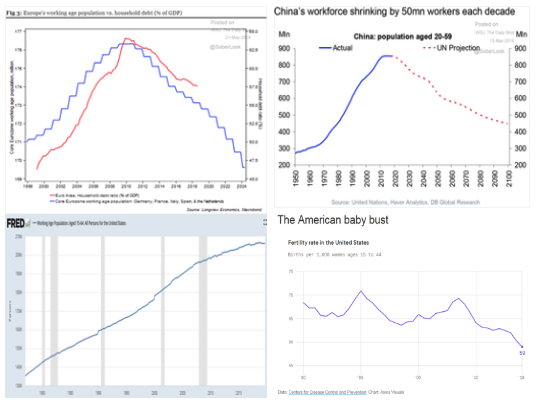

The working age population in Europe peaked in 2012 and topped in China in 2015. Although the Baby Boom wave of retirement in the U.S. began in 2011, the working age cohort is still growing but at a snail’s pace. However, the fertility rate in the U.S. has fallen by more than 14% since the financial crisis, which suggests the working age population in the U.S. could begin to shrink within the next decade. Immigration is the quickest way to boost a country’s working age population, but is currently out of favor in the U.S. With the exception of Germany, immigration has faced a growing backlash throughout Europe, mirroring the rise in populism. Labor market growth is a primary factor in determining any economy’s long term growth potential, along with changes in productivity. While most voters in advanced economies desire better economic growth, few understand or know the link between an increase in immigration and how it can lead to faster GDP growth. Public opinion about immigration is often shaped by demagogic politicians who often prefer to prey on the public’s lack of economic knowledge.

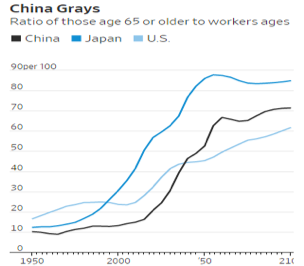

China has designs on being the dominant global power by 2049 but will have to overcome a huge surge in the number of people who will be older than 65 by 2052. Japan began to experience a similar surge in the late 1980’s, which undoubtedly has been a contributing factor in the stagnation of the Japanese economy since 1990. The Chinese Communist Party exercises an authoritarian control over the Chinese economy and its citizens, but this demographic shift is likely to prove more problematic than they realize. The U.S. is also experiencing an increase, and even though it is more gradual, the rise in the number of aging Americans over 65 will weigh on growth in the next 30 years.

India faces many daunting challenges as it attempts to replace China as the fastest growing country in the world, but also could be a positive in the global demographic story. Electricity is essential and more than 15% (240 million) of India’s 1.4 billion citizens don’t have access to electricity. Although India has made much progress in recent years in connecting more people to its electric grid, many areas are affected by unreliability with some depending on less than 12 hours of power per day. In China 100% of its citizens have access to reliable electricity. On Friday September 20 the Indian government cut the corporate tax rate for Indian companies to boost economic growth. Going forward local firms will pay a 22% corporate tax, down from 30%. India is also offering companies that may be contemplating moving supply chains out of China an incentive to open up shop in India. Companies that begin manufacturing within the next four years will be subject to a tax rate of only 15%. This is a fundamental change that should help improve economic growth in India in coming years and attract foreign investment. While the lower corporate tax rate will entice global companies with a supply chain in China to consider India, India will need to improve its educational system to capitalize on the change in its tax rate going beyond the next four years. India’s literacy rate is just 72% compared to 96% in China, so a commitment by India to vastly improve its educational system could overcome any reluctance foreign firms may have about India’s long term labor pool. Transparency International publishes its Corruption Perceptions Index (CPI) ranking 180 countries and territories by their perceived levels of public sector corruption among experts and businesspeople. In 2018 India was ranked 78th with a value of 41 up from 38 in 2015. India is moving in the right direction but clearly has room for improvement. China was ranked 87th with a value of 39 which was down from 41 in 2017, so China is moving in the wrong direction. Since 2016 the U.S.’s rating has fallen from 74 to 71 which earned the U.S. a rank of 22. India’s working age population will continue to rise in the next 30 years, unlike China or the U.S.

For 17 years the World Bank has published its Doing Business analysis which quantifies the ease of doing business in 190 countries. It incorporates 10 different variables with a heavy focus on government regulation.

“At its core, regulation is about freedom to do business. Regulation aims to prevent worker mistreatment by greedy employers (regulation of labor), to ensure that roads and bridges do not collapse (regulation of public procurement), and to protect one’s investments (minority shareholder protections). All too often, however, regulation misses its goal by replacing one inefficiency with another, especially in the form of government overreach in business activity. By documenting changes in regulation in 12 areas of business activity in 190 economies, Doing Business analyzes regulation that encourages efficiency and supports freedom to do business.” The Doing Business 2020 study highlights some striking differences between developing countries and advanced economies. “An entrepreneur in a low-income economy typically spends around 50% of the country’s per-capita income to launch a company, compared with just 4.2% for an entrepreneur in a high income economy. It takes nearly six times as long on average to start a business in the economies ranked in the bottom 50 as in the top 20.”

In the Doing Business 2020 report India is ranked 63rd of the 190 countries covered, so it is in the top 33%. China is ranked 31st, the U.S. is 5th, with New Zealand and Singapore in the top two spots. However, India was one of the top ten countries registering the most improvement. Improving the ease of doing business could make India more attractive to companies considering moving their supply chains. India’s Chamber of Commerce can use the Doing Business report to woo foreign investment.

The long term growth prospects, reduction in corporate tax rates, and better business climate are reasons why an allocation to India is worth considering. In the short term the Reserve Bank of India has lowered its policy rate five times which should boost growth in 2020. The India ETF (INDA) rallied from $24.00 in February 2016 to over $38.00 in January 2018, before pulling back to $29.00 in October 2018. An equal rally of $14.00 could lift INDA up to $43.00 by the summer of 2020.

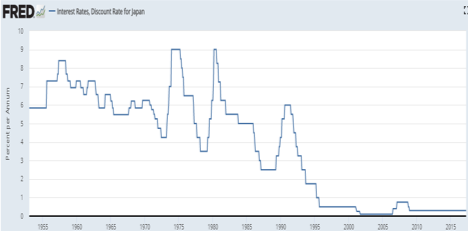

Central banks always knew they could reverse a recession and ignite a recovery by lowering their policy rates, since most recessions were preceded by central banks increasing their policy rates and tightening credit. Simply loosening the tourniquet constricting the flow of credit and voila a recovery would soon blossom. Central bank confidence began to erode in the 1990’s as the Bank of Japan (BOJ) cut its policy rate to just 0.50% in 1996. Despite lowering its policy rate to the lowest level in the BOJ’s history, the action didn’t result in an economic rebound, even though the global economy was doing just fine. The BOJ learned an invaluable lesson albeit too late. By the time the BOJ had lowered its policy rate to 0.50% prices were falling throughout Japan, so that the inflation adjusted policy rate (real rate) was well above 1.0% and not as stimulative as the BOJ presumed. Japan had entered the Black Hole of deflation and there wasn’t much the BOJ could do about it.

After the U.S. economy entered a recession in 2001, which was exacerbated by the events of September 11, Fed Chair Alan Greenspan lowered the federal funds rate to 1.0% and below the inflation rate to avoid the trap the BOJ had fallen into. Greenspan saw the policy mistake the BOJ had made and made sure the Fed didn’t repeat it. Notice how the policy rates of the BOJ and the Fed since 1980 have posted a lower high at the end of each business cycle. Two conclusions can be drawn from this pattern: Each recovery required even lower rates to get it going, and each recovery stalled at a lower peak in the policy rate.

In 2000 the BOJ launched an aggressive Quantitative Easing (QE) program to reverse the recession and deflation that developed after the Asian Financial Crisis in 1997. The BOJ’s QE program included buying government debt but also private debt and stocks. Between 1995 and 2007, Japanese GDP fell from $5.45 trillion to $4.52 trillion in nominal terms, while inflation spent more time below 0% than above 0%, despite the BOJ's efforts. The financial crisis exposed a painful truth for the Federal Reserve and eventually the ECB. Central bank’s primary and historically most powerful policy tool – the policy interest rate – was no longer effective. The Federal Reserve launched its first QE program in December 2008, and followed with QE2 in November 2010 and QE3 in September 2012. The ECB lowered its policy rate to -0.10% % in June 2014 before initiating its first QE program in March 2015. Following the ECB’s lead the BOJ adopted a -0.10% policy rate in January 2016. At the ECB’s September 2019 meeting the ECB announced it would initiate another round of QE in November of $22 billion a month. The ECB also lowered its policy rate to -0.50%, more than 5 years after it said its negative rate policy would be temporary.

The financial system was on the brink of collapse in December 2008 when the Fed launched its first QE program. In my opinion it stabilized the global financial system and very likely prevented another Great Depression from taking hold. While there should be little debate on the need and efficacy of QE1, the value of QE3 was minimal in economic terms, although it certainly helped inflate stock prices. No one can measure how the economies of the U.S., European Union, and Japan would have performed in the absence of the subsequent QE programs by each central bank, or the introduction of negative rates. It seems fair to accept they helped spur economic growth minimally, but there have been unintended negative side effects that may curb future economic growth. A healthy banking system is the foundation of a modern economy but the negative interest policies of the ECB and BOJ have eviscerated Japanese and European banks. Since the BOJ lowered their policy rate to 0.50% in 1995, the Topix Bank Index is down more than 75% and shows no signs or recovery. The ECB lowered its policy rate to 0.25% in December 2011 and 0% in June 2012, before going negative at -0.10% in June 2014. The Euro Stoxx bank Index has persistently underperformed the Euro Stoxx Index since 2010 and especially during the ECB’s low and negative policy rate regime since 2011. The decline in bank stocks in Japan and Europe make is very expensive for banks to fortify their balance sheets through the sale of equity. The inability to strengthen bank sheets will curb banks lending capacity, which is likely to impair economic growth in coming years. With bond yields below 0% in many countries, European banks simply can’t make much money making loans which is contributing to lackluster growth in the EU. The U.S. banking system is healthier and stronger than banks in Japan or Europe, since U.S. banks cleaned up and strengthened their balance sheets quickly after the financial crisis. Despite doing all the right things U.S. bank stocks have significantly underperformed the S&P 500 in part due to a flat yield curve. The negative rates in the global bond market are holding U.S. rates below their natural level, so the ECB’s and BOJ negative rate policy is distorting the U.S. yield curve.

The takeaway is that central banks no longer have the power to manipulate monetary policy to achieve the desired outcome. Central banks will not be able to count on policy rates to conduct monetary policy as they have since World War II to lift their economy out of a recession and ignite a recovery. Instead they will resort to huge Quantitative Easing programs when the next recession develops, which will be beneficial but not as powerful as significantly cutting the policy rate. Central bank monetary policy will be far less effective in coming years compared to the last 40 years, which will weigh on global economic growth for years to come.

After World War II policy makers were able to deliver a 1-2 punch to pull an economy out of recession. Central banks would lower their policy rate and the politicians would provide a boost from fiscal spending by running a budget deficit. This prescription always brought a sinking economy back to life, but the effectiveness of fiscal stimulus is not what it used to be. According to the Institute of International Finance (IIF), each new dollar of debt is generating less GDP growth than it did 20 years ago. In the decade from 1997-2007 a dollar of debt provided almost $1.00 of GDP growth in Emerging Market economies ex. China, $.60 of growth in China, and just $.30 in advanced economies, i.e. U.S, EU and the U.K.. The impact on growth from additional debt for the decade of 2007-2017 was far weaker, as governments needed larger deficits to offset the weakness from the financial crisis. In the decade that ended in 2017 Emerging Market economies experienced an increase of $.60 for each new dollar of debt, while China’s boost fell to $.24, and advanced economies rose by $.20. Pushing the fiscal pedal to the medal just ain’t what it used to be, which indicates that future increases in debt will generate even less GDP growth in coming decades for each new dollar of debt.

Global debt continues to reach record heights, so the risk of reaching a tipping point where there is simply too much global debt is drawing closer. The IIF calculates that as of March 31, 2019, worldwide debt totaled $246.5 trillion, which was nearly 320% of global GDP, up about 20% since 2012. This figure includes non-financial corporate debt (no bank debt), government, financial, and household debt. The nearby graphic illustrates how debt has increased in each of these sectors since 1997, 2007, and through September 2017. In the decade ending 2017, government debt jumped 50% as a percent of global GDP rising from 58% to 87%, as governments increased deficit spending in the wake of the financial crisis. Household debt barely grew as mortgage debt fell due to housing crisis defaults and financial debt was held in check as banks bolstered their balance sheets.

Although global debt only rose by 18.4% from the end of 2012 through March 31, 2019, debt rose by 27.5% in the U.S. and soared by 140% in China. China’s total corporate, household, and government debt rose to 303% of GDP in the first quarter of 2019. Since the financial crisis the largest contributor to the increase in China’s debt burden has come from the corporate sector. Since 2008 China’s corporate debt as a percent of GDP has increased from 85% to 150% as of March 31, 3018, and is the highest of all the major economies.

The disparity between corporate debt levels in China and the rest of the world is likely due to state owned banks in China lending aggressively to Chinese state owned enterprises (SOEs). China has long subsidized SOE’s with loans with low interest rates to provide them with a competitive advantage in a global economy. Although this type of lending is in violation of World Trade Organization rules, China has persisted in this practice. In the U.S. corporate debt as a percent of GDP is at its highest level in history at 47%, and has generated a slew of articles expressing concern since a peak in corporate debt levels has preceded each of the last three recessions in the U.S. This is a legitimate concern that will be unmasked in the next recession. It is worth noting that U.S. corporate debt as a percent of GDP is just one-third the level in China.

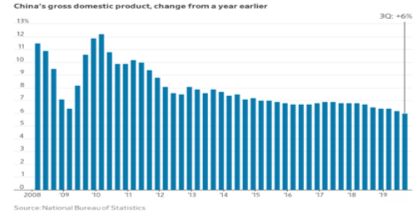

In 2001 China joined the World Trade Organization and its GDP was $1.3 trillion that represented 2.5% of global GDP of $51 trillion. By 2008 China’s GDP had tripled rising to $4.6 trillion, which was 7.2% of global GDP. By 2018 China’s GDP had tripled again from 2007 reaching $13.6 trillion and 15.5% of global GDP. The growth in China’s economy has accounted for a growing proportion of the growth in global GDP since 2001. China’s GDP growth has slowed from 10.6% to 6.0% in 2019, and is expected to continue to slow. The tailwind that China has been for global GDP growth since 2001 will provide less of a lift going forward.

Most of the GDP growth since 2007 in China has been fueled by the Chinese banking system whose assets exploded from $8 trillion to $40 trillion in 2019. Chinese bank assets’ are now double the $19 trillion for U.S. banks and larger than EU banks, which is why the four largest banks in the world are Chinese. Regulators in China began to clamp down on the shadow banking system in 2018 as discussed in the February 2019 Macro Tides. “In March 2018, the Central Commission of Comprehensive Reforms endorsed new regulations targeting “shadow banking” and regulation that will increase the transparency and capital adequacy requirements for non-financial investors to buy into banks, insurers and brokerage houses. Since March 2018 the growth rate in the shadow banking system has plunged from an annual rate of 7.5% to a contraction of -1.6%.” The steps to reign in China’s shadow banking suggest that policy makers in China understand that credit growth must grow at a slower rate if China is to maintain a stable banking system. While this is constructive it is also why GDP growth is expected to slow further in coming years.

For decades the global economy has benefited from a number of long term trends that helped to lift the standard of living for the majority of people around the world. Many of the beneficial trends that made this possible – open trade, globalization, effective central bank monetary policy, positive demographic trends, capacity for timely and extended fiscal stimulus, low and manageable levels of debt, and the addition of China as a productive contributor to the global economy – have been slowing with some trends already reversing. Since each of these factors is long term in nature, this process will take time to evolve, with periods of intensification and ebbs that help mask what is developing. As global growth remains more subdued in coming years than during the past 40 years, the risk to the global economy from unforeseen shocks will be greater. Throughout history extended periods of economic malaise have been a breeding ground for instability, often leading to wars. This is why the rising tide of nationalism and populism are already taking root around the world and are likely to flourish in coming years. This is why Bernie Sanders and Elizabeth Warren are running for President and their campaigns can’t be dismissed. In the U.S. (and other countries as well), disenchantment and divisiveness are rampant with more energy expended criticizing established institutions, societal norms, and especially capitalism. A lot of the criticism is warranted and overdue. At another time in our history there would be constructive discourse which would lead to positive changes. In the current environment of political polarization, the level of vitriol on TV and in social media precludes conversation and compromise. In 1967, another time of disenchantment and divisiveness, Buffalo Springfield’s song ‘For What It’s Worth’ had a timely message for 1967 and now. “There's battle lines being drawn Nobody's right if everybody's wrong.” According to a recent Pew Research survey, Republicans (77%) and Democrats (72%) say that their opposing Republican and Democratic voters cannot agree on basic facts, which makes having a constructive conversation nearly impossible.

Global Economy Set to Stabilize

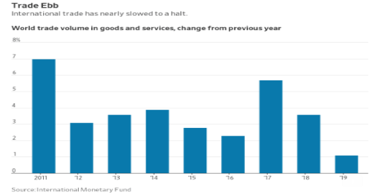

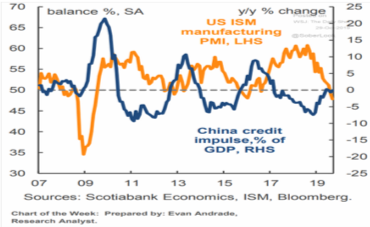

Most of the slowing in the global economy is due to the sharp deceleration in global trade from 5.8% in 2018 to just above 1.0% in 2019. Global GDP growth has slowed from 3.8% in 2017 to 3.0% in 2019, according to the IMF. With trade representing 25% of global GDP, the decline in trade since 2017 accounts for almost all the slowing in the global economy. In response central banks have enacted 42 rate cuts representing a total of 2,070 basis points. These rate reductions are the most aggressive since the financial crisis. Short term rates have been lowered by central banks and long term rates have also fallen significantly during the last year. Financial Conditions have eased a lot since the first quarter of 2019, which will progressively provide a lift to the global economy in the first half of 2020. So far the amount of easing in Financial Conditions (0.5%) is appreciably less than the easing in 2017 (1.0%). One reason for the disparity is that China has not eased policy as aggressively as it did in 2013 and 2016, although the People’s Bank of China has lowered its policy rate and eased reserve requirements for Chinese banks. The U.S. ISM Manufacturing Index has improved after China’s credit impulse has climbed above 0 with a lag of 6 months or so. The increase in China’s credit impulse from below zero to zero would be expected to also provide some support for the U.S. ISM Manufacturing Index in coming months. However, comparisons with the past may not have the same correlation given the Trade War and its impact on U.S. manufacturing. The support from monetary accommodation is likely to offset most of the softness in manufacturing, business investment, and less trade, and will help stabilize global GDP near current levels. However, unless a true cease fire in the Trade War with China is achieved, and the U.S. refrains from implementing tariffs against the EU in mid November, a solid reacceleration in global growth is not likely.

Germany is heavily exposed to the global economy as 47% of its GDP comes from exports, and manufacturing represents 22% of GDP compared to just 11% for the U.S. Germany comprises 30% of the European Union’s GDP and is why the EU’s GDP growth has been much slower than in the U.S. since mid 2018, and has slowed to just 0.8% in both the second and third quarter of 2019. Although the German Service PMI is above 50, it has slowed significantly since early 2018, and is why Germany may slip into a recession before the end of 2019 or early 2020. Employment growth has been slowing since the fourth quarter of 2018 and could turn negative if the trend persists.

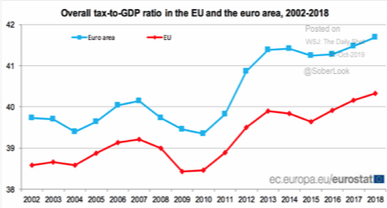

If Germany does enter a recession and unemployment begins to increase in 2020, pressure will build within Germany to stimulate its economy. Germany has been running an annual budget surplus of 1.0% for years so it certainly has the fiscal room to spend. Christine Lagarde became president of the ECB on November 1 after spending 8 years as the head of the IMF. She does not have an economics degree, but her experience at the IMF sharpened her diplomatic and negotiating skills, which she will need in navigating the post Mario Draghi era at the ECB. She is taking the helm at a critical period for the EU with anemic economic growth, negative interest rates, and a bloated ECB balance sheet after years of QE. The only policy tool she has to spur growth is to convince Germany, France, and the Netherlands is to loosen fiscal policy. Since 2010 tax rates in the EU and the broader Euro area have increased by 2.0%, so taxes could be lowered. It will take great persuasion by Lagarde to get Germany on board and time to coalesce a consensus within the EU to augment monetary policy with fiscal stimulus. Her most persuasive argument will be the feeble growth that is likely to persist until the EU launches a fiscal stimulus program.

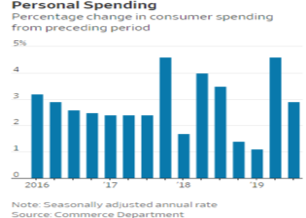

The U.S. has been largely insulated from the slowdown in global growth and the Trade War, since trade represents just 12% of GDP and manufacturing only 11%. The U.S. may be insulated but it has not been immune as GDP growth has slowed from 3.1% in the first quarter to 2.0% in Q2 and, based on the Bureau of Economic Analysis’s first estimate, 1.9% in Q3. As expected consumer spending slowed in the third quarter to 2.9% from the second quarter’s torrid pace of 4.6%. Consumer spending is expected to hold up since Consumer Confidence remains ebullient and job and wage growth is solid. The Household Savings Rate is 8.3% which indicates consumer spending has been maintained without a drawdown in savings.

Although Consumer Confidence continues to hold near 20 year highs, there is one worrisome sign. Consumer’s plans to purchase a new vehicle plunged in October to the lowest level in years, according to the Conference Board. I wouldn’t read too much into one’s month’s data point since the overall health of consumer’s finances are good, but this does imply car sales may slow in coming months and further weigh on manufacturing. Changes in bank lending standards are one of the best recession warning signals, since a negative change in the availability of credit has a meaningful impact on economic growth in the following 6 to 9 months. Lending standards were increased well before the recessions in 2000 and 2008, but remain easy now.

U.S. Manufacturing is in a recession and the ISM Non-Manufacturing Index has weakened but is still OK. As much as consumers remain confident, CEO confidence continues to fall. Over time the correlation between CEO Confidence and the ISM Non-Manufacturing Index has been fairly high. CEO Confidence has likely been more affected by the slowing in the global economy and the Trade War than consumers, since CEO’s have a front row seat to the global slowdown and have been paying the tariffs. Whether the ISM Non-Manufacturing Index responds as it has in the past is debatable, but Business Investment is not likely to improve until CEO’s see improvement in the global economy and a lasting lessening in trade uncertainty. The primary risk to the developing stabilization in the global economy is from trade.

A Second Front in the Trade War

In 1974 Muhammad Ali used his Rope-A-Dope to defeat George Foreman in the Rumble in the Jungle. Muhammad Ali protected himself by covering his face and mid section with his arms and hands, while allowing George Foreman to throw punch after punch without doing any damage. The goal of the Rope-A-Dope was to allow Ali’s opponent to wear himself out from throwing punches, which is exactly what happened to Foreman. Ali knocked a tired Foreman out in the 8th. https://www.youtube.com/watch?v=AW4BnOOKY2o I think China has been employing its version of a Rope-A-Dope strategy in the trade talks with the U.S, with the goal of dragging them out in hopes that President Trump will eventually accept a watered down deal.

Investors continue to expect and hope that the U.S. and China will sign a Phase I agreement before the end of November. The odds of some kind of deal have improved, but the litmus test indicating that it is a serious deal will only be confirmed if the U.S. agrees to roll back some of the tariffs already imposed. China has reportedly made a deal conditional on a roll back in tariffs. Given President Trump’s style of negotiating, a roll back seems unlikely. China has also express doubts about the potential for a bigger deal. In late April it appeared that China and the U.S. had reached a deal, until China backed out at the last minute. My guess is something similar is likely to occur as the effort for a broad deal fails to materialize and disappoints investors again. Trade negotiating Rope-A-Dope.

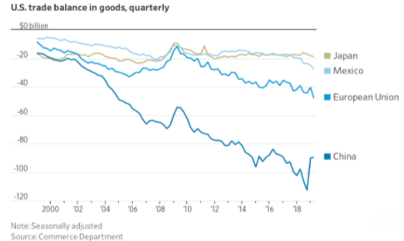

With all eyes focused on China the bigger trade risk may be a Second Front in the Trade War launched against the European Union on November 14. The US has a $160 billion trade deficit with the EU, second only to the trade deficit with China. A large contributor to the trade deficit with the EU comes from the export of cars to the U.S., so the imposition of tariffs on auto imports would be a natural target. The S&P 500 has been at or very near an all time high as President Trump has decided to ramp up the Trade War with China. It’s as if he feels he is playing with house money. With the S&P 500 making a new all time high and potentially some progress with China, President Trump may feel emboldened to engage the EU, since there has been no indication of any progress since the EU was given a tariff extension on May 13. The EU is one of America’s largest trading partners, accounting for $806.5 billion worth of trade in 2018. The U.S. exported $318.6 billion worth of goods to the EU, and imported $487.9 billion for a deficit of $169.2 billion, according to the Census Bureau. In 2018 the U.S exported $120 billion of goods to China and imported $540 billion from China. The EU theoretically has more leverage with the U.S. than China since exports to the EU are $318 billion versus just $120 billion to China. If a second front in the Trade War develops with the EU, it could be more problematic for the global economy than what has occurred with China. And no one seems to be paying attention to this risk.

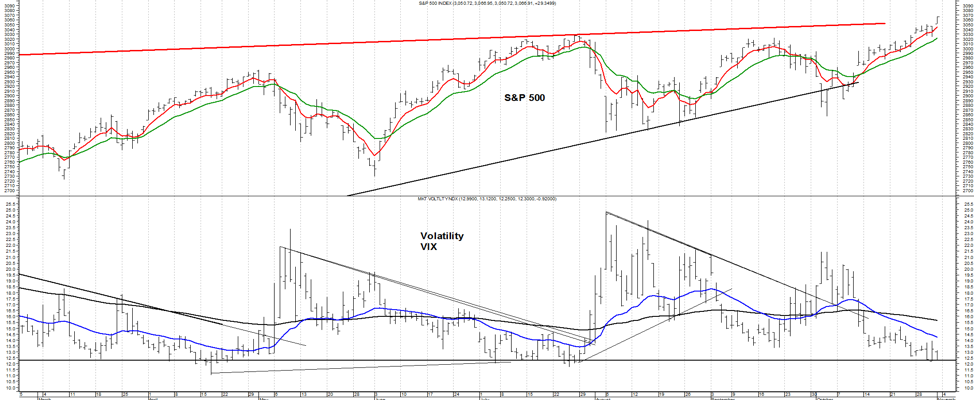

If a second front in the Trade War develops with the EU and the U.S., the developing stabilization in the global economy will be disrupted and the risk of a more pronounced slowing will increase. A 10% to 15% correction in equity markets globally would quickly follow and dent consumer confidence and spending in the U.S., and raise concerns about a U.S. recession in 2020. The negativity surrounding trade and recession fears that were widespread in late August as the S&P 500 fell to 2822 has been replaced by optimism. The level of volatility as measured by the Volatility Index (VIX) has fallen to the same level that accompanied the highs in the S&P 500 in late April and late July, which preceded corrections of -7.6% in May and -6.7% in August.

In addition, the positioning in the VIX futures shows that Large Speculators (Green line middle panel) have a larger short position than in January 2018, September 2018, April 2019, and July 2019. The table is now set for a sharp decline and a spike in volatility.

Jim Welsh

@JimWelshMacro

[email protected]

NOTES: I have referenced many sources for this month’s issue of Macro Tides. Given the topics discussed it seemed appropriate to provide a Link to the majority of research sources used to provide this analysis so you can access them.

https://openknowledge.worldbank.org/bitstream/handle/10986/32436/9781464814402.pdf

https://en.wikipedia.org/wiki/Extreme_poverty

https://www.investopedia.com/terms/q/quantitative-easing.asp

https://www.barrons.com/articles/5-years-into-negative-rates-europes-banks-feel-the-pain-51570831182

https://www.cnbc.com/2019/10/18/ecb-members-voice-concern-over-its-negative-rate-policy.html

https://www.wsj.com/articles/ecb-holds-steady-in-draghis-final-policy-decision-11571918124

https://www.iif.com/Portals/0/Files/Global%20Debt%20Monitor_January_vf.pdf

https://www.iif.com/Portals/0/Files/content/GDM_Aug2019_vf.pdf

https://www.merics.org/en/china-monitor/chinas-corporate-debt

https://data.worldbank.org/indicator/NY.GDP.MKTP.KD

https://en.wikipedia.org/wiki/Historical_GDP_of_China

https://www.people-press.org/2019/10/10/the-partisan-landscape-and-views-of-the-parties/

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits