As investors ponder the prospects for the Middle East and North Africa (MENA) region, Franklin Templeton Emerging Markets Equity’s Bassel Khatoun and Salah Shamma take stock of the investment landscape. They highlight some of the market developments in Saudi Arabia, Kuwait, Egypt and the United Arab Emirates (UAE) that have caught their attention.

It was a climactic year for the Middle East and North Africa (MENA). Saudi Arabia was officially included in MSCI’s Emerging Markets Index (MSCI EM) and Saudi Aramco, the state-owned oil company, announced its intention to float on the local stock exchange, the Tadawul, in December 2019. The MSCI is also likely to announce Kuwait’s inclusion in the MSCI EM Index in December 2019.

While we did see geopolitical tensions escalate this year, including an attack on Saudi Aramco’s oil facilities and a reinvigorated standoff between the US and Iran, our sentiment towards the region’s stock markets remains constructive.

Following years of fiscal consolidation, regional governments have finally turned inwards to promote private consumption and stimulate growth. Meaningful social and economic reforms have been implemented with far-reaching ramifications. In fact, we see encouraging signs of an early recovery. And though we can’t look at the region in isolation, we see distinct opportunities across MENA markets as we close out 2019.

Saudi Arabia

The results of Saudi Arabia’s far-reaching economic and social reform agenda are beginning to show. With its budget deficit significantly reduced, and a record budget expenditure in 2019, Saudi Arabia’s overall economic fundamentals have improved. Overall confidence and consumption are trending higher. This is reflected in improving corporate earnings, while valuations also remain attractive in specific areas of the market.

MSCI EM Index Inclusion

Following the last and final MSCI EM inclusion tranche in August, the Saudi market has reverted to trading on fundamentals. Previous MSCI index inclusions have also witnessed stock markets pull back as an MSCI event passes, and we see Saudi Arabia as no different.1 As expected, the market retraced some of its earlier gains, losing more than 12% since its early May highs.2 We believe Saudi Arabia’s medium-term outlook remains on a positive trajectory. The positive year-to-date equity market return in Saudi Arabia, for example, still largely reflects the strong performance in large-cap stocks, despite some recent weakness.

And while we see pockets of opportunities across the entire Tadawul, we are particularly excited about mid-cap stocks which, in our view, are under-owned by foreign investors and should offer sustainable earnings growth as the domestic economy recovers.

To date, we’ve seen more than US$21 billion of foreign inflows into the country since the start of 2019 from international institutional investors, including passive flows.3 Foreign ownership levels of listed stocks also rose to 5.38% by August 2019, up from 1.78% in June 2018 when the decision to include Saudi Arabia in the MSCI EM Index was first announced.4

Saudi Aramco IPO

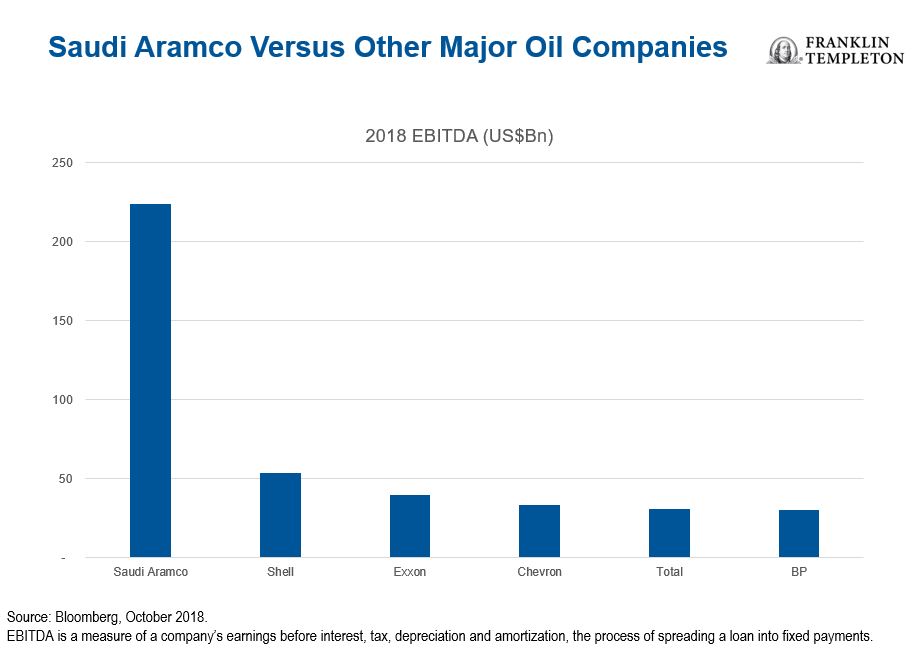

Aramco’s initial public offering (IPO) is a central pillar of the Kingdom’s Vision 2030. There were initially plans to float on the Tadawul, followed by listing on an exchange abroad. However, Aramco decided to sell a 1.5% stake (approximately US$25.6 billion) locally, shelving plans to go global for now. The company’s valuation will also likely fall between US$1.6-$1.7 trillion, and though short of Crown Prince Mohammed bin Salman’s $2 trillion target, it should still be the world’s most valuable company.

Our view is that while a local listing could kick-start the Kingdom’s IPO pipeline, help it diversify its economy and set the standard for corporate governance and transparency locally, we are keen to see an international listing follow. We think the company is a unique asset and in a class of its own when it comes to profitability and cash flow generation. Not listing abroad could be seen as a “miss” in the eyes of international investors. A global listing would allow the company to greatly diversify its shareholder base, further strengthen its corporate governance framework and support Saudi Arabia’s longer-term vision to attract international investors in its plans to diversify away from oil.

Kuwait

Kuwait is in the midst of a multi-year effort to introduce fiscal reforms, increase investment and diversify away from oil dependence. MSCI has also stated that it is next in line for an emerging-market upgrade during its next review in December 2019. Given that Kuwait has made all of the necessary changes to its market infrastructure, we are confident MSCI will announce a positive decision.

Bolstering our investment outlook for Kuwait is the fact that fundamentals are continuing to improve. With substantial reserves, low levels of debt and a stable banking sector, we think Kuwait stands out amongst numerous regional and emerging-market peers. Add to this a budget breakeven oil price of just US$49 a barrel for 2019, the lowest by some margin in the region, and a “AA”5 credit rating, we believe Kuwait could be considered a low beta,6 defensive investment destination.7

Egypt

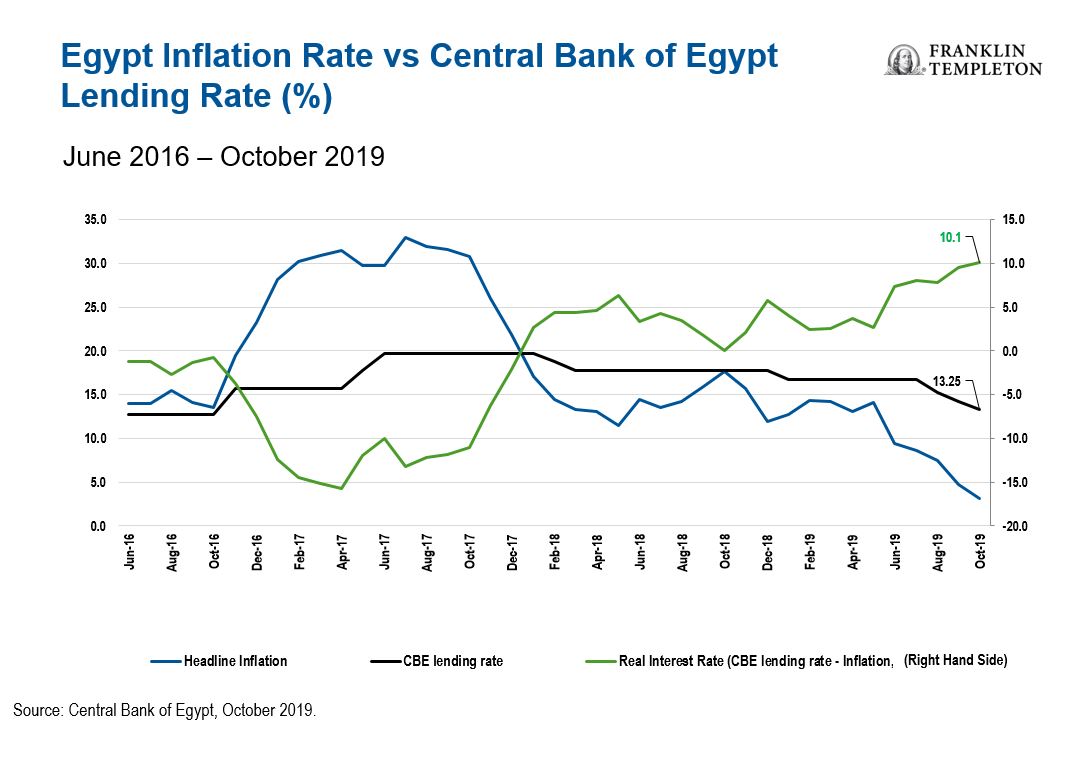

The recent Egyptian protests have not changed our investment case for the country. Egypt’s economy is at the tail end of a successful three-year International Monetary Fund US$12 billion funding program, which we think should help Egypt return to sustainable growth.

Bold, but much-needed policy reforms in past years have stabilized the currency and put the economy on more sustainable footing. Inflation, which has structurally been stubbornly high, has also been dropping, allowing the Central Bank of Egypt to kick-start a monetary loosening policy that has resulted in a 450-basis point (bps)8 interest-rate cut year-to-date. We expect muted inflationary pressures and a solid macro stance to allow for a continuation of the monetary easing cycle, which in turn should support overall domestic consumption and economic growth.

Valuations for Egyptian equities also remain attractive to us, and the earnings growth prospects lead us to believe the country could cultivate an encouraging investment environment. We think that corporations should continue to benefit from the central bank’s easing policies, which should likely continue into next year.

UAE

The UAE continues to offer value, in our view, despite current challenges. Its economy continues to swing between consolidation pressures and favorable government policies that promote both population and economic growth. We think the recent reforms to residency and corporate ownership laws, for example, should further support the economy and cement UAE as a regional hub for business. In fact, the Dubai International Finance Centre was included in the top ten of the Global Financial Centers Index for the first time, placing it alongside other renowned financial hubs like New York, London, Hong Kong and Singapore.

Further policies to promote lending to under-serviced small and medium-sized enterprises (SMEs) should also be important for stimulating economic growth and demand, in our view. The government is keen to encourage both government- and privately-owned banks to help SMEs meet financing needs through programs, such as the “Dubai Silk Road Initiative” due to start in June 2020. It would allow SMEs to access credit, insurance and bank guarantees to stimulate growth and increase the UAE’s attractiveness as a global business hub.

Tourism figures and the number of new business licenses issued in Dubai are also on the rise. And we expect that the upcoming Expo 2020, which will be hosted in Dubai, should further drive tourism and infrastructure growth.

What’s Next?

Looking towards 2020, there are opportunities to invest selectively across the MENA region—most of which are driven by attractive valuations and sound fundamentals in countries that continue to implement and benefit from fiscal and social reforms. We see promise in the improving economic and corporate data in some countries, leading many markets to revert to trading based on fundamentals, rather than liquidity.

It’s important to note that our view on the global economy remains cautious given the elevated political and economic risks, primarily due to the recent trade war spat between the United States and China and an increasing probability of a recession in the US. However, global central banks have shifted to broadly supportive policy stances in recent months, so we expect accommodative policies and interest rates to prevail in the near to mid-term. In fact, US rate cuts provided a welcome reprieve for the MENA region this past year.

We’ll continue to carefully monitor what effects oil price volatility and political and economic crises could have on the MENA region’s improving trajectory. But broadly, we believe regional stock markets remain relatively insulated from this noise, and we look forward to ringing in the new year.

Important Legal Information

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. Past performance is not an indicator or guarantee of future results.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

1. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-markets countries. MENA representation in the index currently includes Qatar, United Arab Emirates and Egypt. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

2. Source: Bloomberg, as of November 20, 2019.

3. Source: EFG Hermes estimates, data provided on September 11, 2019.

4. Source: Bloomberg, September 2019.

5. Moody’s Definition of AA Credit Rating: Obligations rated AA are judged to be of high quality and are subject to very low credit risk.

6. In the world of investing, beta has traditionally been a measure of a security’s or portfolio’s volatility in comparison to the stock market as a whole. Today, the word “beta” is also used as shorthand to describe getting broad stock-market exposure, typically through investments that often track the S&P 500 and other major indexes.

7. Source: International Monetary Fund, June 2019.

8. Source: Central Bank of Egypt. A basis point is a unit of measurement. One basis point is equal to 0.01%.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments