Prelude to Crisis

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSimple Conceit

Radical Actions

Ballooning Balance Sheet

Merry Christmas and the Happiest New Year

Ignoring problems rarely solves them. You need to deal with them—not just the effects, but the underlying causes, or else they usually get worse. The older you get, the more you know that is true in almost every area of life.

In the developed world and especially the US, and even in China, our economic challenges are rapidly approaching that point. Things that would have been easily fixed a decade ago, or even five years ago, will soon be unsolvable by conventional means.

There is almost no willingness to face our top problems, specifically our rising debt. The economic challenges we face can’t continue, which is why I expect the Great Reset, a kind of worldwide do-over. It’s not the best choice but we are slowly ruling out all others.

Last week I talked about the political side of this. Our embrace of either crony capitalism or welfare statism is going to end very badly. Ideological positions have hardened to the point that compromise seems impossible.

Central bankers are politicians, in a sense, and in some ways far more powerful and dangerous than the elected ones. Some recent events provide a glimpse of where they’re taking us.

Hint: It’s nowhere good. And when you combine it with the fiscal shenanigans, it’s far worse.

Simple Conceit

Central banks weren’t always as responsibly irresponsible, as my friend Paul McCulley would say, as they are today. Walter Bagehot, one of the early editors of The Economist, wrote what came to be called Bagehot’s Dictum for central banks: As the lender of last resort, during a financial or liquidity crisis, the central bank should lend freely, at a high interest rate, on good securities.

The Federal Reserve came about as a theoretical antidote to even-worse occasional panics and bank failures. Clearly, it had a spotty record through 1945, as there were many mistakes made in the ‘20s and especially the ‘30s. The loose monetary policy coupled with fiscal incontinence of the ‘70s gave us an inflationary crisis. Paul Volcker’s recent passing (RIP) reminds us of perhaps the Fed’s finest hour, stamping out the inflation that threatened the livelihood of millions. However, Volcker had to do that only because of past mistakes.

Recently, reader Mourad Rahmanov, who has thought-provoking (and sometimes lengthy) reactions to almost every letter, kindly sent me some of his personal favorite John Mauldin quotes. One was this passage which succinctly captures my feelings about the Fed. (Context: This was part of my response to Ray Dalio’s comments on Modern Monetary Theory.)

Beginning with Greenspan, we have now had 30+ years of ever-looser monetary policy accompanied by lower rates. This created a series of asset bubbles whose demises wreaked economic havoc. Artificially low rates created the housing bubble, exacerbated by regulatory failure and reinforced by a morally bankrupt financial system.

And with the system completely aflame, we asked the arsonist to put out the fire, with very few observers acknowledging the irony. Yes, we did indeed need the Federal Reserve to provide liquidity during the initial crisis. But after that, the Fed kept rates too low for too long, reinforcing the wealth and income disparities and creating new bubbles we will have to deal with in the not-too-distant future.

This wasn’t a “beautiful deleveraging” as you call it. It was the ugly creation of bubbles and misallocation of capital. The Fed shouldn’t have blown these bubbles in the first place.

The simple conceit that 12 men and women sitting around the table can decide the most important price in the world (short-term interest rates) better than the market itself is beginning to wear thin. Keeping rates too low for too long in the current cycle brought massive capital misallocation. It resulted in the financialization of a significant part of the business world, in the US and elsewhere. The rules now reward management, not for generating revenue, but to drive up the price of the share price, thus making their options and stock grants more valuable.

Coordinated monetary policy is the problem, not the solution. And while I have little hope for change in that regard, I have no hope that monetary policy will rescue us from the next crisis.

Let me amplify that last line: Not only is there no hope monetary policy will save us from the next crisis, it will help cause the next crisis. The process has already begun.

Radical Actions

In September of this year, something still unexplained (at least to my satisfaction, although I know many analysts who believe they know the reasons) happened in the “repo” short-term financing market. Liquidity dried up, interest rates spiked, and the Fed stepped in to save the day. I wrote about it at the time in Decoding the Fed.

Story over? No. The Fed has had to keep saving the day, every day, since then.

We hear different theories. The most frightening one is that the repo market itself is actually fine, but a bank is wobbly and the billions in daily liquidity are preventing its collapse. Who might it be? I have been told, by well-connected sources, that it could be a mid-sized Japanese bank. I was dubious because it would be hard to keep such a thing hidden for months. But then this week, Bloomberg reported some Japanese banks, badly hurt by the BOJ’s negative rate policy, have turned to riskier debt to survive. So, perhaps it’s fair to wonder.

Whatever the cause, the situation doesn’t seem to be improving. On Dec. 12 a New York Fed statement said its trading desk would increase its repo operations around year-end “to ensure that the supply of reserves remains ample and to mitigate the risk of money market pressures.”

Notice at the link how the NY Fed describes its plans. The desk will offer “at least” $150 billion here and “at least” $75 billion there. That’s not how debt normally works. Lenders give borrowers a credit limit, not a credit guarantee plus an implied promise of more. The US doesn’t (yet) have negative rates but the Fed is giving banks negative credit limits. In a very precise violation of Bagehot’s Dictum.

We have also just finished a decade of the loosest monetary policy in American history, the partial tightening cycle notwithstanding. Something is very wrong if banks still don’t have enough reserves to keep markets liquid. Part of it may be that regulations outside the Fed’s control prevent banks from using their reserves as needed. But that doesn’t explain why it suddenly became a problem in September, necessitating radical action that continues today.

Here’s the official line, from minutes of the unscheduled Oct. 4 meeting at which the FOMC approved the operation.

Staff analysis and market commentary suggested that many factors contributed to the funding stresses that emerged in mid-September. In particular, financial institutions' internal risk limits and balance sheet costs may have slowed the distribution of liquidity across the system at a time when reserves had dropped sharply and Treasury issuance was elevated.

So the Fed blames “internal risk limits and balance sheet costs” at banks. What are these risks and costs they were unwilling to accept, and why? We still don’t know. There are lots of theories. Some even make sense. Whatever the reason, it was severe enough to make the committee agree to both repo operations and the purchase of $20 billion a month in Treasury securities and another $20 billion in agencies. They insist the latter isn’t QE but it sure walks and quacks like a QE duck. So, I and many others call it QE4.

As we learned with previous QE rounds, exiting is hard. Remember that 2013 “Taper Tantrum?” Ben Bernanke’s mild hint that asset purchases might not continue forever infuriated a liquidity-addicted Wall Street. The Fed needed a couple more years to start draining the pool, and then did so in the stupidest possible way by both raising rates and selling assets at the same time. (I don’t feel good saying I told you so but, well, I did.)

Having said that, I have to note the Fed has few good choices. As mistakes compound over time, it must pick the least-bad alternative. But with each such decision, the future options grow even worse. So eventually instead of picking the least-bad, they will have to pick the least-disastrous one. That point is drawing closer.

Ballooning Balance Sheet

Underlying all this is an elephant in the room: the rapidly expanding federal debt. Each annual deficit raises the total debt and forces the Treasury to issue more debt, in hopes someone will buy it.

The US government ran a $343 billion deficit in the first two months of fiscal 2020 (October and November) and the 12-month budget deficit again surpassed $1 trillion. Federal spending rose 7% from a year earlier while tax receipts grew only 3%.

No problem, some say, we owe it to ourselves, and anyway people will always buy Uncle Sam’s debt. That is unfortunately not true. The foreign buyers on whom we have long depended are turning away, as Peter Boockvar noted this week.

Foreign selling of US notes and bonds continued in October by a net $16.7b. This brings the year-to-date selling to $99b with much driven by liquidations from the Chinese and Japanese. It was back in 2011 and 2012 when in each year foreigners bought over $400b worth. Thus, it is domestically where we are now financing our ever-increasing budget deficits.

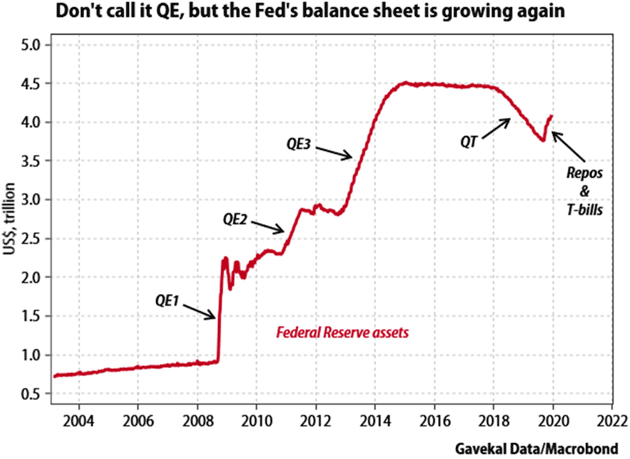

The Fed now has also become a big part of the monetization process via its purchases of T-bills which also drives banks into buying notes. The Fed's balance sheet is now $335b higher than it was in September at $4.095 trillion. Again, however the Fed wants to define what it's doing, market participants view this as QE4 with all the asset price inflation that comes along with QE programs.

It will be real interesting to see what happens in 2020 to the repo market when the Fed tries to end its injections and how markets respond when its balance sheet stops increasing in size. It's so easy to get involved and so difficult to leave.

Declining foreign purchases are, in part, a consequence of the trade war. The dollars China and Japan use to buy our T-bills are the same dollars we pay them for our imported goods. But interest and exchange rates also matter. With rates negative or lower than ours in most of the developed world, the US had been the best parking place.

But in the last year, other central banks started looking for a NIRP exit. Higher rate expectations elsewhere combined with stable or falling US rates give foreign buyers—who must also pay for currency hedges—less incentive to buy US debt. If you live in a foreign country and have a particular need for its local currency, an extra 1% in yield isn’t worth the risk of losing even more in the exchange rate.

I know some think China or other countries are opting out of the US Treasury market for political reasons, but it’s simply business. The math just doesn’t work. Especially given the fact that President Trump is explicitly saying he wants the dollar to weaken and interest rates go even lower. If you are in country X, why would you do that trade? You might if you’re in a country like Argentina or Venezuela where the currency is toast anyway. But Europe? Japan? China? The rest of the developed world? It’s a coin toss.

The Fed began cutting rates in July. Funding pressures emerged weeks later. Coincidence? I suspect not. Many factors are at work here, but it sure looks like, through QE4 and other activities, the Fed is taking the first steps toward monetizing our debt. If so, many more steps are ahead because the debt is only going to get worse.

As you can see from the Gavekal chart below, the Fed is well on its way to reversing that 2018 “quantitative tightening.”

Louis Gave wrote a brilliant essay recently (behind their pay wall, but perhaps he will make it more public) considering four possible reasons for the present valuation dichotomies. I’ll quote the first one because I believe it is right on target:

1) The Fed’s balance sheet expansion is only temporary.

The argument: The Fed’s current liquidity injection program is not a genuine effort at quantitative easing by the US central bank. Instead, it is merely a short-term liquidity program to ensure that markets—and especially the repo markets—continue to operate smoothly. In about 15 weeks’ time, the Fed will stop injecting liquidity into the system. As a result, the market is already looking through the current liquidity injections to the time when the Fed goes “cold turkey” once again. This explains why bond yields are not rising more, why the US dollar isn’t falling faster, and so on.

My take: This is a distinct possibility. But then, as Milton Friedman used to say: “Nothing is so permanent as a temporary government program.” The question here is: Why did the repo markets freeze in mid- to late September? Was it just a technical glitch? Or did the spike in short rates reflect the fact that the appetite of the US private sector and foreign investors for short-dated US government debt has reached its limit? In short, did the repo market reach its “wafer-thin mint” moment?

If it was a technical glitch, then the Fed will indeed be able to “back off” come the spring. However, if, as I believe, the repo market was not the trouble, but merely a symptom of a bigger problem—excessive growth in US budget deficits—then it is hard to see how, six months before a US election, the Fed will be able to climb back out of the full-on US government monetization rabbit hole in which it is now fully immersed.

In this scenario, the markets will come to an interesting crossroads around the Ides of March. At that point, the Fed will have to take one of two paths:

1. The Fed does indeed stop its “non-QE QE” program. In this scenario, US and global equities are likely to take a nasty spill. In an election year, that will trigger a Twitterstorm of epic proportions from the US president.

2. The Fed confirms that the six-month “temporary” liquidity injection program is to be extended for another “temporary” six months. At this point bond yields everywhere around the world will shoot up, the US dollar will likely take a nasty spill, global equities will outperform US equities, and value will outperform growth, etc.

Looking at the US government’s debt dynamics, I believe the second option is much more likely. And it is all the more probable since triggering a significant equity pull-back a few months before the US presidential election could threaten the Fed’s independence. Still, the first option does remain a possibility, which may well help to explain the market’s cautious positioning despite today’s coordinated fiscal and monetary policies (ex-China).

Just this week Congress passed, and President Trump signed, massive spending bills to avoid a government shutdown. There was a silver lining; both parties made concessions in areas each considers important. Republicans got a lot more to spend on defense and Democrats got all sorts of social spending. That kind of compromise once happened all the time but has been rare lately. Maybe this is a sign the gridlock is breaking. But if so, their cooperation still led to higher spending and more debt.

As long as this continues—as it almost certainly will, for a long time—the Fed will find it near-impossible to return to normal policy. The balance sheet will keep ballooning as they throw manufactured money at the problem, because it is all they know how to do and/or it’s all Congress will let them do.

Nor will there be any refuge overseas. The NIRP countries will remain stuck in their own traps, unable to raise rates and unable to collect enough tax revenue to cover the promises made to their citizens. It won’t be pretty, anywhere on the globe.

Luke Gromen of Forest for the Trees is one of my favorite macro thinkers. Like Louis Gave, he thinks the monetization plan will get more obvious in early 2020.

Those that believe that the Fed will begin undoing what it has done since September after the year-end “turn” are either going to be proven right or they are going to be proven wrong in Q1 2020. We strongly believe they will be proven wrong. If/when they are, the FFTT view that the Fed is “committed” to financing US deficits with its balance sheet may go from a fringe view to the mainstream.

Both parties in Congress are committed to more spending. No matter who is in the White House, they will encourage the Federal Reserve to engage in more quantitative easing so the deficit spending can continue and even grow.

As I have often noted, the next recession, whenever it happens, will bring a $2 trillion+ deficit, meaning a $40+ trillion dollar national debt by the end of the decade, at least $20 trillion of which will be on the Fed’s balance sheet. (My side bet is that in 2030 we will look back and see that I was an optimist.)

My 2020 forecast issue, which you’ll see after the holiday break, I’m planning to call “The Decade of Living Dangerously.” Sometime in the middle to late 2020s we will see a Great Reset that profoundly changes everything you know about money and investing.

Crisis isn’t simply coming. We are already in the early stages of it. I think we will look back at late 2019 as the beginning. This period will be rough but survivable if we prepare now. In fact, it will bring lots of exciting opportunities. More on that in coming letters.

Merry Christmas and the Happiest New Year

Perhaps I should say Feliz Navidad, as I will be spending Christmas in Puerto Rico with some of my children coming to visit. Not much chance for a white Christmas, but Shane and I really enjoy living in this tropical paradise.

There will be no letter next week. The first issue of January will be my annual forecast letter. This is the time of year when I think deeply about my goals for the future and reflect on how I responded to life’s challenges in the past. Perhaps it is just my age, but as I approach each new year, I become a great deal more reflective and appreciative of the time that I have to enjoy with family and friends.

One of the greatest gifts I receive is your attention and time to reading these hopefully thoughtful musings. One serious challenge of The Age of Transformation is the overwhelming amount of information demanding our attention. That you would give me part of your time is a greater honor than I can possibly imagine. My pledge to you in 2020 is to continue treating it with the respect you deserve.

And with that, I will hit the send button and wish you a truly Merry Christmas and the best of New Years. May you spend it with friends and have the most prosperous year ever!

Your ever hopeful analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All