Three Things We’re Thinking About Today

- Optimism surrounding the government’s economic agenda has resulted in a more favorable investment climate in Brazil. The Brazilian market outperformed its emerging market (EM) counterparts with a 14% gain over the fourth quarter 2019 and 27% increase for the year, both in US dollar terms. While the country’s economic recovery has been slower than expected, government and central bank efforts are improving the country’s longer-term growth potential. Inflation has remained under control, allowing the central bank to ease rates to record lows to stimulate the economy. We believe social security reform is key to stimulating investment and credit, which should help improve economic activity and significantly reduce Brazil’s fiscal deficit. A major privatization plan has also been announced, and tax and other structural reforms should improve the ease of doing business.

- Trade and slowing growth fears have largely overshadowed China’s initiatives to strengthen and diversify its economy. The government’s focus on economic restructuring and long-term sustainable growth has led to an acceleration in the implementation of structural reforms and widespread industry consolidation, as well as the development of local supply chains in the technology space to replace US sources. China will be a frontrunner in the fifth-generation wireless technology arena (5G) and is expected to have some 600 million 5G subscribers by 2025, or about 40% of the forecasted 1.6 billion subscribers globally.1 Together with artificial intelligence (AI) and robotics, this should help drive growth in China’s new economy as it strives to become less reliant on the United States. In our view, China will emerge from this challenging period stronger and more self-reliant, with multiple pillars of economic support.

-

Kuwait is undergoing a multi-year effort to introduce fiscal reforms, increase investment and diversify away from oil dependence. In December, index provider MSCI stated that Kuwait met all the necessary requirements for reclassification to EM status and will be added to the MSCI Emerging Markets Index in May 2020 with an estimated weight of 0.69%. With substantial reserves, low levels of debt and a stable banking sector, we think Kuwait stands out among its peers. Add to this a budget breakeven oil price of just US$49 a barrel for 2019—the lowest by some margin in the region—and a AA2 credit rating, we believe Kuwait could be considered an attractive investment destination in the Middle East. Despite trading at a premium to its EM peers, valuations in Kuwait remain reasonable, in our view.

Outlook

Much market noise and conflicting signals dominated 2019. While some of these uncertainties may persist in the near term, we believe it is essential to stay the course. The markets are just beginning to realize opportunities from technology disruption and the transition of businesses away from traditional models. We believe the investment scope in the emerging world is wide and promising for investors who can overlook near-term volatility and invest for the longer term.

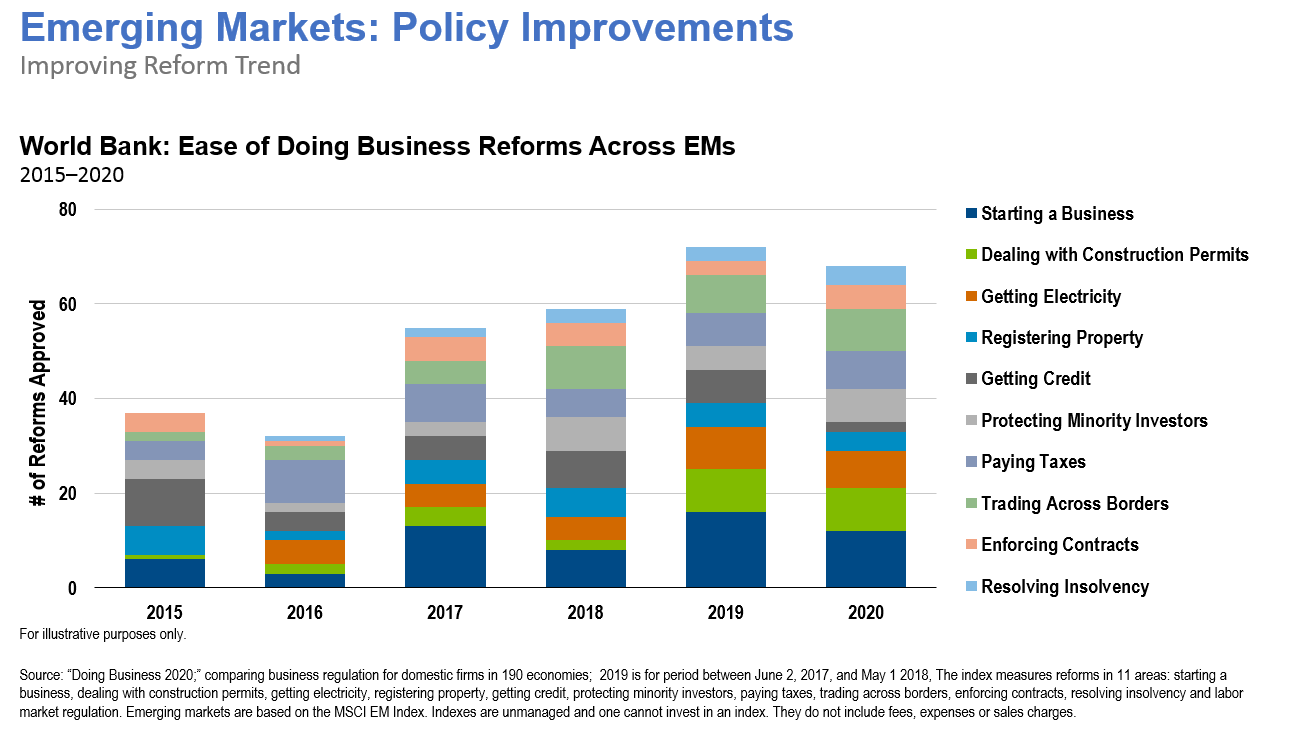

The International Monetary Fund forecasts EM growth will accelerate in 2020 and remain more than double that of developed markets.3 Improving fiscal, economic and monetary policies and a renewed focus on structural reforms in many EMs has been gaining traction. The EM landscape continues to transform. EM economies are more diversified now—with domestic consumption and technology offering new drivers of growth—and are growing less reliant on low-cost manufacturing and commodities.

Although US-China trade tensions have de-escalated in the short term on news of a partial trade deal and both countries scaling back tariffs, we expect the broader economic conflict to remain for some time. The impact from the trade conflict has not been limited to China. A comprehensive agreement therefore remains in the best interests of both sides. US President Donald Trump’s administration will be acutely aware of this heading into an election year in 2020.

Emerging Markets Key Trends and Developments

EM equities advanced over the fourth quarter of 2019 and pulled ahead of developed market stocks. Global monetary easing and the imminent signing of a partial US-China trade deal cheered investors, even as political tensions rose in parts of the emerging world. The MSCI Emerging Markets Index returned 11.9%, while the MSCI World Index returned 8.7%, both in US dollars.4

The Most Important Moves in Emerging Markets in the Fourth Quarter of 2019

Asian stocks climbed, with markets in Taiwan, China and South Korea outperforming. China and the United States reached consensus on a “phase one” trade deal, including the suspension of new tariffs and scaling back of certain duties. Improved global trade sentiment helped lift trade-sensitive indexes in Taiwan and South Korea. Meanwhile, Thailand’s stock market edged down amid a weaker outlook for the domestic economy.

Latin American equities advanced. Brazil’s stock market rallied as the central bank raised its economic growth forecasts and trimmed its key interest rate to a record low. We expect lower interest rates in Brazil to drive a reallocation of assets from cash to equities as investors seek better returns. In Mexico, stocks finished the quarter higher supported by gains in December as the central bank loosened monetary policy and a US-Mexico-Canada trade pact drew nearer to completion.

In the Europe, Middle East and Africa region, Russian equities delivered sturdy returns. The Bank of Russia’s interest-rate cuts and a rebound in crude oil prices buoyed the market. Strong retail sales and real wage growth further supported sentiment. South Africa’s market rose as firmer gold prices lifted materials stocks. A stronger rand also boosted equity returns. Equity markets in the UAE, Turkey, Qatar and Saudi Arabia, however, lagged.

Scroll over the map to view comments on the countries indicated and our sentiment.

Green = positive, Red = negative, Blue = neutral

The graphic reflects the views of Franklin Templeton Emerging Markets Equity regarding each region and are updated on a quarterly basis. All viewpoints reflect solely the views and opinions of Franklin Templeton Emerging Markets Equity. Not representative of an actual account or portfolio.

Regional Outlook As of December 31, 2019+-

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The views expressed are those of the investment manager(s) and the comments, opinions and analyses are rendered as of the publication date and may change without notice.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security.

Past performance does not guarantee future results.

Products, services and information may not be available in all jurisdictions and are offered outside the US by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

1. Source: GSMA Intelligence. As of October 2019. There is no assurance that any forecast, estimate or projection will be realized.

2. Moody’s Definition of AA Credit Rating: Obligations rated AA are judged to be of high quality and are subject to very low credit risk.

3. Source: International Monetary Fund World Economic Outlook database, October 2019. There is no assurance that any estimate, forecast or projection will be realized.

4. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments