While there are a number of uncertainties in the global economy today, many investors may not realize the depth and breadth of potential opportunities emerging markets still offer—on both the equity and fixed income side. Franklin Templeton Multi-Asset Solutions’ Subash Pillai outlines the team’s approach to risk management when it comes to emerging market investing, noting that not all countries in this category should be viewed through the same lens.

Many investors tend to treat all emerging market economies the same, but we think this is a mistake. Emerging markets represent a broad and diverse mix of economies—with different cultures, demographics, political regimes and economic drivers. And, the potential investment opportunities are likewise diverse, as are the risk profiles.

With an opportunity set that has been expanding on both the equity and fixed income side, we see emerging markets as an important building block for a global investment portfolio.

In a prior commentary, I discussed the appeal our team sees in emerging markets, particularly in an environment where interest rates are negative in a number of developed economies. For yield-seeking investors in particular, it has become more difficult to fulfill income needs.

What many economists and academics would typically consider a “risk-free” rate of return—the three-month US Treasury bill—is currently yielding less than 2%, which barely covers inflation. As a result, many investors have recognized the need to take on more risk in order to generate capital growth in excess of inflation.

We believe emerging markets offer attractive risk-adjusted investment opportunities, with income potential via dividend yields on the equity side as well as “coupon” or interest rate payments on the fixed income side, in addition to capital growth potential.

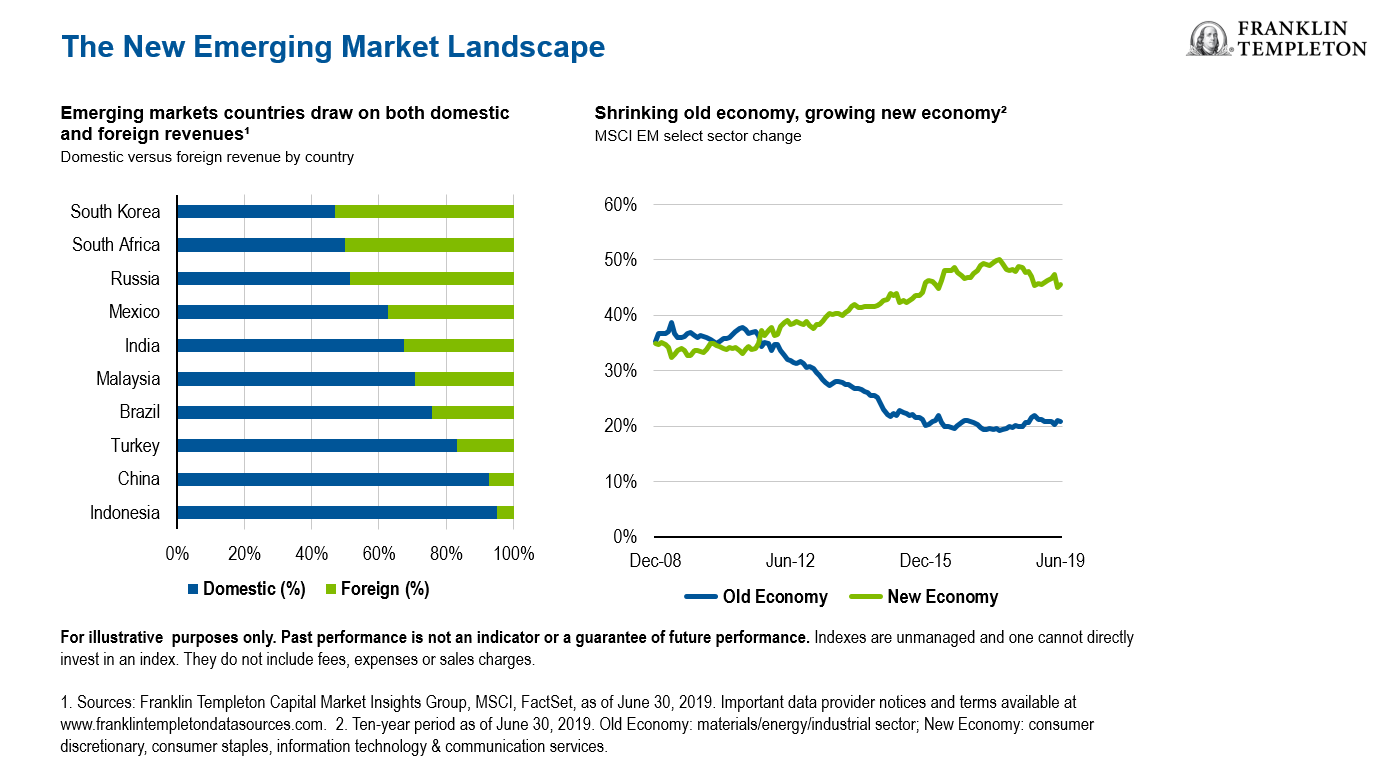

The New Emerging Market Landscape

As our team has reiterated many times, emerging markets have been transforming. Commodity exports and/or manufacturing of low-value goods are no longer the primary sources of economic growth for many of these economies—an “old economy” model. Today, many countries classified as emerging markets are leaders in high-tech, consumer goods and value-added services—a “new economy” model.

In addition, emerging market countries today draw on both domestic and foreign revenues. Many investors may be surprised to learn both China and Brazil’s economies are primarily domestic in orientation, for example. Thus, foreign headwinds may not have as large of an impact as they have in the past.

On the fixed income side, many emerging markets offer attractive yields that are in excess of those available in developed markets. And on the equity side, emerging markets offer a potential source of growth, with competitive valuations. One valuation metric, the forward price-earnings ratio, stands at 16.85 in developed markets versus 12.21 in emerging markets, so we think emerging markets offer a good value opportunity.1

Risk Management in Practice

We are excited about the potential opportunities emerging markets offer, but of course, investing in them is not without risk. Our experience over several decades tells us that an active allocation approach—applying top-down as well as bottom-up perspectives to decide the weightings of asset classes across a portfolio—may help illuminate possible risks in aggregate and help investors make decisions around their expectations.

Taking a dynamic approach allows us to maintain a long-term view while remaining on the ball about macroeconomic changes—dialing up or down our exposure across asset classes as we deem appropriate based on factors such as economic and inflation forecasts, valuation measures and historical risk premia.

As such, risk management is an integral part of our strategy.

Tactical Asset Allocation and Risk Management

Our stock research starts with a proprietary, rigorous and bottom-up selection process to develop a portfolio of high-conviction stocks. Both quantitative and qualitative analysis drives our asset allocation mix, with local insights, combined with global perspectives, driving our investment views.

Our macro views on the fixed income side involve the use of proprietary interest rate and currency models, as well as econometric and analytical techniques to evaluate potential interest rate and currency misalignments in the market. The team applies these quantitative assessments to the macro profiles of each country to identify longer-term value opportunities. Rather than rely on a single model in its analysis, the group analyzes the results from each tool, seeking to understand why the models may provide different outcomes. The results are an important input in the analysis of countries, which drives the investment process.

Then, we assess risk within our fixed income and equity portfolios. We implement portfolio-wide hedges when necessary and conduct ongoing monitoring of volatility, large risk exposures, tracking error of a portfolio versus a benchmark and any other potential “tail-risk” outcomes—events that could cause an investment to move more than three standard deviations beyond its current price.

Current Convictions

We have seen improved fundamentals in many emerging markets countries versus decades past; several countries learned the lessons from past crises and improved their resiliencies to external shocks. Past crises have taught emerging market countries to minimize external borrowing and focus on domestic markets, resulting in higher average credit quality for local currency issuances. Within fixed income, we currently prefer local currency bonds as they have tended to be more liquid than hard currency bonds during periods of risk aversion, as the domestic investor bases often step in to buy, even as foreign investors are fleeing.

On the fixed income side, we favor short-dates Mexican local currency bonds. We continue to monitor the policy agenda of the government, but believe institutional strength should preserve much of the fiscal advances the country has made over the past several years. So far, central bank independence has been maintained and the government passed a reasonable fiscal budget for 2020.

Mexico’s central bank has been easing to shore up the economy, which has been moderating due to both external and domestic factors (including disappointing oil production). We anticipate additional easing ahead. There certainly are some uncertainties, including public security concerns that have put pressure on the business climate and undercut government credibility, in addition to political and trade-related issues. But risk-adjusted yields in Mexican local currency bonds remain attractive, in our view, with the front end of the curve (one-year maturity) yielding around 6.8% (as of December 31, 2019).

Meanwhile, we see growing penetration of e-commerce and digital ecosystems in several emerging markets, with greater and faster adoption of new technologies (China and India, for example). We also see strengthening consumer markets and rising affluence driving numerous investment opportunities.

And lastly, while there’s still work to be done, we think improvements in corporate governance in emerging markets have been encouraging, providing a structural tailwind for investors.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Investment Adventures in Emerging Markets blog.

For timely investing tidbits, follow us on Twitter @FTI_Emerging and on LinkedIn.

Important Legal Information

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security.

Past performance is not an indicator or guarantee of future results.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds adjust to a rise in interest rates, the share price may decline. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

1. Source: MSCI, as of January 31, 2020. Emerging markets represented by the MSCI Emerging Markets Index, which captures large- and mid-cap representation across 26 emerging market countries. Developed markets represented by the MSCI World Index, which captures large- and mid-cap representation across 23 developed markets countries. Indexes are unmanaged and one cannot directly invest in an index. They do not include fees, expenses or sales charges. Past performance is not an indicator of future results. The price-earnings (P/E) ratio is a valuation metric that measures a company’s share price relative to its earnings. Forward P/E measures earnings forecasted for the next 12 months. There is no assurance that any estimate, forecast or projection will be realized.

© Franklin Templeton

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments