Macro Factors and Their Impact on Monetary Policy, the Economy, and Financial Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGlobal Economy Tipping Toward Recession

As discussed in the January issue of Macro Tides entitled ‘Markets Are Priced for Perfection, Not Disappointment’, coming into 2020 expectations for an acceleration of growth in the global economy and in the U.S. were high. “The U.S. stock market ended 2019 with a record run based on a Phase One trade deal with China, institutional Fear Of Missing Out (FOMO), projections by the Federal Reserve that interest rates will not change in 2020, and expectations the U.S. and global economy will strengthen in 2020. This expectation is critical since S&P 500 earnings were basically flat in 2019, so the entire gain in the S&P 500 in 2019 was due to a 30% expansion in its Price Earnings ratio.” I thought expectations for a quick pickup in growth in the first quarter were too optimistic, and explained why in the February issue entitled ‘Global Economy Stabilizing But Signs of a Rebound Are Weak.’ “The balance of recent data for the global economy and the U.S. indicate that both have stabilized, so the widespread slowing in growth in 2019 has been arrested. However, indications that a true acceleration is taking hold are not yet present.” I noted that the IMF had once again downgraded its forecast for global GDP for 2020 and 2021. It was the sixth straight reduction, even though the IMF expected global GDP to post a modest rebound from 2.9% to 3.3% in 2020. Despite the modest improvement, the IMF acknowledged that "there are now tentative signs that global growth may be stabilizing, though at subdued levels", and admitted that "few signs of turning points are yet visible in global macroeconomic data."

I also noted that global trade had contracted in 2019 for the first time since the financial crisis and for only the second time since 1990. Although the trade deal between the U.S. and China removed the risk of a further escalation, a 25% tariff on $250 billion in Chinese imports and a 7.5% tariff on another $120 billion of imports remained in place. The Congressional Budget Office has estimated that the existing tariffs would lower the level of real GDP by 0.5 percent in 2020, raise consumer prices by 0.4 percent, and continue to weigh on profit margins of the U.S. companies involved.

The expectations for a speedy recovery in the first quarter were predicated on a rebound in manufacturing and business investment. However, a Deloitte CFO survey of 147 CFO’s of companies with at least $3 billion in annual sales in Canada, Mexico, and the United States found that the percent of CFO’s planning to increase hiring had dropped from 63% in early 2019 to 54%, and only 49% expected to increase business investment in 2020 compared to 73% in 2019. This suggested that after an extended period of slowing growth, the majority of businesses would adopt a ‘Show Me’ attitude before deciding to further increase business spending. The reluctance to increase business investment had also been confirmed by the dramatic slowing in Commercial and Industrial loans during 2019.

Although there were good reasons to question whether GDP growth would accelerate in the first quarter, there were also good reasons why I expected the rate of growth to improve before mid year.

The service sector comprises more than 85% of the U.S. economy and it remained resilient, despite the recession in manufacturing in 2019. Consumer confidence, although down from a record high in 2018, was still high and consistent with consumers making trips to the shopping mall and window shopping on the internet. The most important factor was that financial conditions had eased significantly since November 2018, and had further improved since September 2019, after the Federal Reserve lowered the federal funds rate three times, Treasury yields dropped, the Dollar fell, and the stock market soared in the fourth quarter. I thought financial conditions would provide the economy a lift 6 to 9 months after the improvement in financial conditions began last September. This suggested that the easing in financial conditions would begin to support growth in the second quarter and beyond. In my view the anticipation of this coming support had stretched the valuation of the S&P 500 to an extreme and led investors to mistake signs of stabilization for actual improvement.

As noted in the January Macro Tides, the S&P 500 had spent very little time trading above a Forward Price / Earnings ratio of 17.0 since 2002. “The S&P 500 has only traded at a multiple above 17 in 21 out of 918 weeks (2.3% of the time) since 2002, with 9 of those 21 weeks falling at the end of 2017 and the first 4 weeks in January 2018. That stretch was followed by a two week intra-day correction of -11.8% that lowered the multiple from above 18.0 to 16.0. The S&P 500’s Forward P/E has been above 17.0 for the past 9 weeks and as of January 21 was 18.6, so the U.S. market continues to be priced for perfection and not disappointment.”

As discussed in the January Macro Tides, data from China and the European Union also indicated that the first quarter of 2020 was likely to remain soft. Fathom Consulting specializes in global financial and market research and produces an Economic Sentiment Indicator (ESI) that does a good job of tracking GDP in the major economies. Fathom tracks GDP on a quarterly basis so an increase of 0.2% translates to 0.8% annually. The ESI for the EU had yet to turn up so a rebound didn’t look imminent. Bank of America estimated GDP growth in the EU will be 1.0% in 2020 which would not represent much improvement from 2019. The rebound in global growth wasn’t going to receive much of a lift from growth in the European Union in the first quarter.

Fathom Consulting has also developed its China Momentum Indicator (CMI) which is designed to provide a more in-depth view of China's economic growth and is not dependent on ‘official’ data. My assessment was that China’s rebound might not kick in until the second half of 2020. “Since peaking in late 2017 Fathom’s CMI has been trending lower and is suggesting GDP growth is closer to 4.1% than China’s official rate of 6.0%. More importantly, the CMI offers no evidence that China’s economy is about to strengthen. This conclusion is further supported by the weak growth in the China Credit Impulse. The rebound since the fourth quarter of 2018 looks anemic when compared to prior surges in credit. While the Phase 1 trade deal should be a positive for growth in China, the impact is not going to materialize in the first quarter of 2020 and may not really come into play until the second half of 2020.”

The analysis of the U.S. and global economy provided in the January and February Macro Tides indicated that the U.S. and global economy had stabilized at the end of 2019 and was poised to improve by mid 2020, after an extended period of slowing due to the trade war with China. The outbreak of the coronavirus (COVID-19) materialized as the global economy was thus vulnerable to an unexpected shock and has delivered a strong headwind that will at best push the expected improvement from mid-year into the second half of 2020. At worst, COVID-19 may deliver a knockout punch that tips the global economy toward a recession as Japan and the EU contract, China’s growth dives toward 0%, and the U.S. flirts with recession.

In the January 27 Weekly Technical Review entitled ‘Coronavirus – Much Ado About Nothing?’ I detailed why the cornavirus was far more likely to spread than the SARS virus in 2003. “Those who contracted the SARS version of coronavirus were not infectious until after they exhibited symptoms. This made it possible to quarantine those exposed to SARS and isolate those with the SARS virus quickly and before they infected other people. In contrast, the current version of coronavirus is infectious before symptoms appear, meaning it can be transmitted to many people before the initial person can be quarantined. It is believed that the incubation period, during which a person has the disease but no identifiable symptoms, ranges from between one and 14 days. A person may not know they have the coronavirus, but can spread it to dozens of other people who would then be capable to infect many others before any of them know they are sick. This is a huge difference since it makes it infinitely more difficult to contain this version of coronavirus as compared to SARS.” The difference in the infectious transmission between SARS and coronavirus was ignored as strategists who focused instead on how much the S&P 500 rallied after SARS appeared in February 2003. However, the rally developed after the S&P 500 had declined by 45% from its peak in March 2000, and had more to do with rate cuts by the Fed and a second tax cut by President Bush than SARS.

The disconnect between the likelihood that the cornavirus was going to continue to spread and investors high level of complacency was addressed in the February 17 WTR entitled ‘How Deep Is the Valley?’ “The risk that the valley is much deeper than investors realize is a significant. If the experts are correct and COVID-19 cripples China’s economy and spreads as some have forecast, investors may be confronted with an unpleasant collision with reality. Fed rate cuts and Chinese stimulus may look more like a placebo than an actual cure for what is making the global economy sick. If the number of infections and deaths continues to grow beyond 4 weeks and the disruption to supply lines becomes more pronounced, the S&P 500 could quickly fall to 3070 – 3150, while the Nasdaq 100 tumbles to 8175 – 8445 by the end of first quarter.” Since peaking on February 19, the S&P 500 has suffered its largest decline from a high in history falling from 3393 to 2954 on February 28 a decline of -12.9% in seven trading days.

China has been the epicenter of the epidemic and investors assumed that the coronvirus would follow the same pattern as SARS. Retail sales plunged in the four months after the SARS outbreak began in Hong Kong, but recovered all that was lost and more within 4 months. Strategists and investors expected that the coronavirus would repeat this V-shaped bottom, since China would implement a large stimulus program and the Peoples Bank of China was already injecting a huge amount of liquidity into the Chinese banking system.

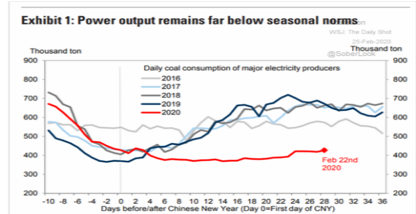

Economic activity was expected to quickly rebound after businesses were authorized to reopen on February 10, after being closed for a week beyond the end of the Lunar New Year celebration. Various measures of China’s economy indicate that activity remains well below what has occurred after the end of recent Lunar New Year celebrations. Twenty-eight days after the New Year ended, power output remains about 40% below where it was in 2017, 2018, and 2019. Steel demand was still down by 50% 3 weeks after the New Year, which certainly indicates that manufacturing activity remains depressed. Coal consumption at major power companies was about 40% lower from a year earlier and home sales were one-quarter of the seasonal norm. Traffic congestion in Beijing and Shanghai is down by more than a third. Vehicle sales in China cratered 92% in the first 16 days of February, according to the China Passenger Car Association.

Any estimate of GDP for China in the first quarter and beyond is merely a guess since no one knows how long China’s economy will be hobbled or how severely. Pantheon Economics believes the Chinese economy could contract at an annual rate of more than -8.0% in Q1, but rebound strongly making up most of what is lost in Q1 in the second and third quarters. If COVID-19 behaves as other flu type viruses and fades as temperatures rise, the rebound in China may develop but is more likely to kick into gear in late in the second quarter or in Q3.

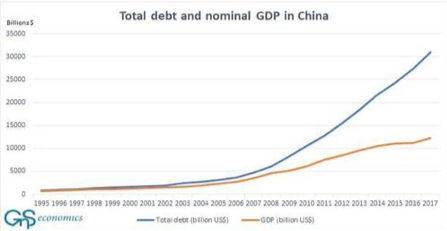

Even if this more optimistic outcome plays out, the slowdown in China’s economy will worsen a number of other problems that have been building for years. China’s debt to GDP soared after the financial crisis rising from 160% of GDP in 2008 to 310% in 2019. A surge in corporate debt during this period was a main contributor to the overall increase in debt. Any extended period of slowing will put more pressure on many private companies to service their debts and there may be a sharp increase in the number of bankruptcies, unless the government acts. An increase in bankruptcies has the potential to further disrupt supplies chains in China and production outside of China that receive parts. The increase in corporate debt and potential increase in bankruptcies could result in problems for small and medium sized banks in China. In recent years there has been a significant increase in the amount of nonperforming loans. The biggest banks will always be insulated since China will provide them whatever liquidity and support they need. Policy makers in China will respond to this economic crisis the same way they responded after the financial crisis – they will allow banks and local governments to issue more debt and will instruct banks to roll over most of the loans to companies to minimize bankruptcies. The net result is the China’s debt to GDP will approach 350% by 2022. Despite another surge in debt, economic growth won’t accelerate as much, since each new dollar of debt has been generating less GDP growth since 2008. Slowly but surely China is sowing the seeds of its own demise, just as every other advanced economy has been doing for decades by increasing debt to GDP levels.

Japan increased its Consumption Tax to 10% from 8% on October 1. No surprise then that consumption tanked in the fourth quarter with GDP contracting at an annualized rate of -6.30%. Japan increased the consumption tax on April1, 2014, which caused a plunge in demand in the second quarter of 2014 and a steeper decline in GDP than in the fourth quarter of 2019. In the first quarter of 2014 GDP jumped as Japanese consumers rushed to front run the tax increase which enabled GDP to rise strongly. The real shock in the third quarter of 2019 was that consumption didn’t soar as consumers failed to spend gobs of money before the tax increase took effect on October 1. In the third quarter GDP was only up 0.4% annualized and lower than growth in the first and second quarter. There is a good chance Japan will enter a recession in the first quarter as it deals with the COVID-19. Japan is facing two immense hurdles. Japan’s population peaked in 2010 so GDP growth will be structurally slower in coming decades, and Japan already has the largest public debt of any country in the world at 223% of GDP. In contrast, China’s government debt as a percent of GDP was 59.5% in 2019 according to Statista.

The Eurozone ended 2019 on a weak note with GDP growing by a scant 0.1% and an annual rate of 0.4%, and could easily slip into contraction in the first quarter. In recent weeks the Citi Economic Surprise Index has plunged as many data points came in below estimates like Retail Sales which were up 1.3% versus 2.3%. As GDP growth slowed throughout 2019, European banks tightened lending standards based on a number of factors: Economic outlook, Credit standards as applied to individual firms or industry, and the banks risk parameters. All of these reasons will intensify as the global economy slows in the first half of 2020 and the Eurozone flirts with recession. The tendency to tighten lending standards further in the face of economic uncertainty will negate any efforts by the ECB to ease monetary policy. The net result is there may be less liquidity available to businesses and consumers as the need for liquidity increases despite the ECB’s efforts. Lending standards won’t ease until banks are convinced the Eurozone economy is improving, which will mute the initial phase of recovery and probably delay it until the second half of 2020.

In the U.S. consumer spending has remained healthy and enabled the U.S. economy to absorb a manufacturing recession in 2019. This was possible since manufacturing comprises just 11% of GDP compared to 70% for consumption and 85% of GDP for services. Consumer spending has been sustained by wage growth of 3.0% and good job creation that has sustained consumer confidence at a high level. That is going to change in coming months since there is a high correlation between changes in the S&P 500 and consumer confidence. The S&P 500 has just experienced the largest decline from a high in history and the cause for the decline isn’t going away and consumers will be reminded of this fact every day in coming weeks. One of the antidotes for COVID-19 is asking consumers to avoid contact with large groups of people as well as wash their hands. As consumers change their behavior, less people will go to movies, restaurants, sporting events, and anywhere that includes coming into contact with others. This change in behavior will depress economic activity. To gauge this impact it will be of value to monitor attendance at outdoor events, movie attendance, etc., since it will indicate whether Americans are in fact changing their behavior and by how much. As it becomes apparent that consumers are responding to the threat by sheltering more, estimates for U.S. GDP will be lowered as will estimates for corporate earnings.

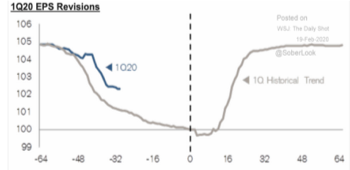

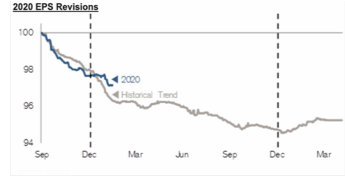

In the course of the normal year estimates for S&P 500 earnings start the year at a high level and then are gradually lowered. Part of this is due to guidance from companies that play the game of guiding estimates down so they can ‘beat’ the lowered estimates by a few pennies. It is remarkable that revisions have been smaller than normal for the first quarter and 2020 as a whole, even after news of the coronavirus began making headlines in late January. This underscores how narrow minded and bullish most strategists were as they focused on the potential of rate cuts by the Fed, stimulus from China, and the belief that the U.S. would remain strong since job growth was healthy and consumer spending was so resilient. There was also the concentration of money in the 5 biggest stocks, which I discussed in the February 10 Weekly Technical Review entitled ‘The Last Stocks Standing’. “As the S&P 500 was making a new high on February 6, 227 stocks in the S&P 500 were actually down year to date. The mega cap stocks (Microsoft, Apple, Amazon, Facebook, and Alphabet Class A&C) comprised 18.1% of the S&P 500 as of February 7 and have enabled the S&P 500 to make a new high. As long as these 5 stocks continue to attract money from momentum investors, the S&P 500 can make marginal new highs and help the overall market hold up. The S&P 500 Equal Weight Index is democratic since each company is treated the same and each has the same weighting of 0.2% as the other 499 companies. Apple and Microsoft, which make up almost 10% of the regular S&P 500, are no more important than Gap Inc which has a weighting of 0.0139%. The Fav Five contributes 18.1% to the daily change in the S&P 500 compared to the bottom 300 companies which only add 16.8%. The concentration of money in the Fav Five and complacency they’ve inspired has reached the goofy stage. When the turn lower comes, it could be violent as traders all try to exit at the same time.”

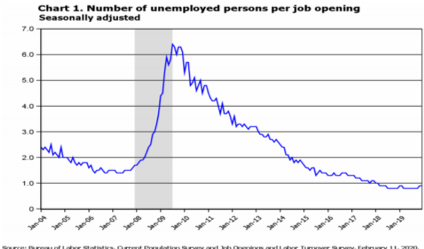

At the end of each month the Bureau of Labor Statistics conducts its Job Openings and Labor Turnover Survey (JOLTS) survey. This comprehensive survey estimates the number of job openings, hires, and layoffs for the total nonfarm labor market and is broken done by industry and four geographic regions. Since January 2018 the number of job openings exceeded the number of unemployed workers, which is why the ratio of unemployed persons per job opening was below 1.0. In December 2019 the number of job openings fell sharply (-364,000) and finished 2019 -14.9% below its level at the end of 2018. This is why the ratio of job openings to the number of unemployed workers has begun to curl higher even though it is still below 1.0.

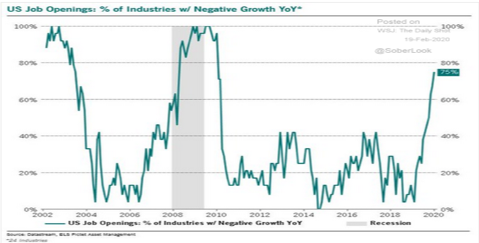

When the decline of -364,000 in openings was first reported my initial response was that the data was skewed, probably concentrated in a small number of industries, and would be revised upward next month. It may indeed be revised higher for January but the decline in job openings was quite widespread with 75% of industries reducing the number of their job openings. The trajectory of the increase in the percent of industries curbing their openings is dramatic and suggests the labor market experienced a sea change at the end of 2019. The concern regarding the impact of COVID-19 on the domestic economy will surely convince many employers to put a hold on job openings and any additional hiring. There has been a high correlation between job openings and employment, with changes in job openings leading employment growth by three to six months. The decline in openings will lead to a slowdown in job growth soon and potentially a contraction if economic growth slows materially in the next few months. This could lead to an increase in unemployment claims and eventually the unemployment rate.

The U.S. consumer has been invincible for years and economists and stock market strategists have assumed consumer spending will always buttress growth. If the stalwart consumer begins to spend less, estimates for GDP growth and earnings for 2020 may be given a haircut, and lead to another selling squall in the stock market. In 2019 earnings for the S&P 500 companies was $165.00 and were expected to rise to $180.00 by many firms. If 2020 earnings estimates are lowered to $165.00, basically unchanged from 2019, and the Forward P/E falls to 14 from the elevated level of 18 in January, the S&P 500 could drop to 2310, and 2475 if given a Forward P/E of 15. The black trend line connecting the March 2009 low, with the October 2011 bottom, and the February 2016 low comes in near 2500. A decline to this trend line wouldn’t violate the context of the 2009 bull market, and would represent a great buying opportunity.

The number of infections and deaths from COVID-19 is expected to spread in the next few weeks around the world and gain a foothold in the U.S. Although the stock market will rally if the Federal Reserve lowers the federal funds rate, the rally may be measured in hours rather than days, since people aren’t going to go out to dinner, movies, sporting events just because the FOMC cut rates. The notion that a vaccine can be developed to curb the current pandemic is fantasy. At best a vaccine may be in place and mass produced to help during the flu season in 2021. The best hope for improvement will occur if COVID-19 behaves as the annual flu does and fades as temperatures rise with the coming of spring. The risk is that COVID-19 explodes into a global pandemic in the next few weeks with millions of people becoming infected and tens of thousands of people succumbing. If this scourge is avoided and the number of people infected with COVID-19 peaks and begins to trend lower during April, the stock market can record a low possibly by the end of March. A strong rally would then ensue in response to Central Bank rate cuts, fiscal stimulus programs in China and potentially in the Eurozone, and the unleashing of pent up global demand. The S&P 500 could be expected to recover at least 61.8% of the decline and could rally into late summer.

Federal Reserve

The yield curve has inverted with the 10-year Treasury yield falling below the 3-month Treasury bill yield. When the yield curve inverted in May 2019 I thought it was due to the plunge in global bond yields that caused $17 trillion of bonds to sport a yield below zero percent. The decline in global bond yields had pulled the 10-year Treasury yield down so that it fell below the 3-month Treasury bill yield, and therefore shouldn’t be accepted as a legitimate warning of an impending recession. This inversion is different since economic growth will be impacted and the risk of recession is therefore elevated. At least one and probably two of the three rate reductions in 2019 were not necessary and were basically wasted since the economy really didn’t need them. The FOMC now has fewer cuts to utilize as they confront this threat to the economy.

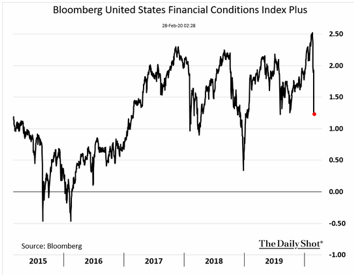

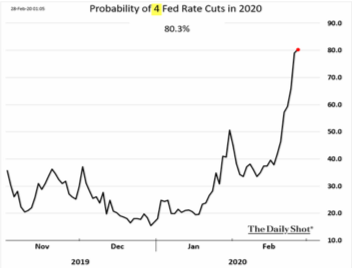

One of the factors that impacts financial conditions is the stock market along with Treasury yields, the value of the Dollar, credit spreads, and a number of other financial instruments. The 12.9% plunge in the S&P 500 has thus tightened financial conditions and is another reason why the FOMC will decide to lower the federal funds rate. In response to the big decline in the stock market, and plummeting Treasury yields, the federal funds rate market is pricing in not one or two rate cuts in 2020, but an 80.3% probability of four rate cuts. The FOMC typically follows market rates, so with expectations so high for action, the FOMC will feel compelled to lower the funds rate when they meet on March 18, irrespective of its efficacy in helping the economy meaningfully. It may help calm financial markets at least temporarily. The question will be whether the FOMC decides to lower the funds rate by 0.25% or 0.50%. If COVID-19 continues to spread and leads people to change their behavior, there is a risk than any rally in the stock market that follows a rate reduction will be seen as an opportunity to sell and be followed by a washout that probably creates at least a short term trading low.

Bernie Sanders

President Trump has attributed some of the big drop in the stock market to the fact that Bernie Sanders has been doing well in the Democratic primaries. While the rise of Bernie may be a small contributing factor, it’s a reach to attribute much of the decline to him. Most Wall Streeters believe an election pitting President Trump against Bernie Sanders would be won by President Trump. Las Vegas odds makers don’t think Bernie has much of a chance. A person who bets $175 on Trump to win will get back $100, so Trump is considered to be the overwhelming favorite. A $100 bet on Bernie will win $175. If Wall Street thinks Bernie won’t win and Las Vegas is priced for a decisive win by President Trump, Bernie Sanders good showing in the primaries would be expected to help the stock market, since President Trump is considered good for stocks. I think to completely dismiss Bernie’s chances though may be mistake and the race could prove much closer than Wall Street or Las Vegas expects. I will discuss this in more detail if Bernie continues to do well on Super Tuesday on March 3, when more than one-third of Democratic presidential primary votes will be decided.

Jim Welsh

@JimWelshMacro

[email protected]

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits