Our Emerging Markets Equity team examines the impact of the spread of coronavirus across emerging market economies during the month of February.

Three Things We’re Thinking About Today

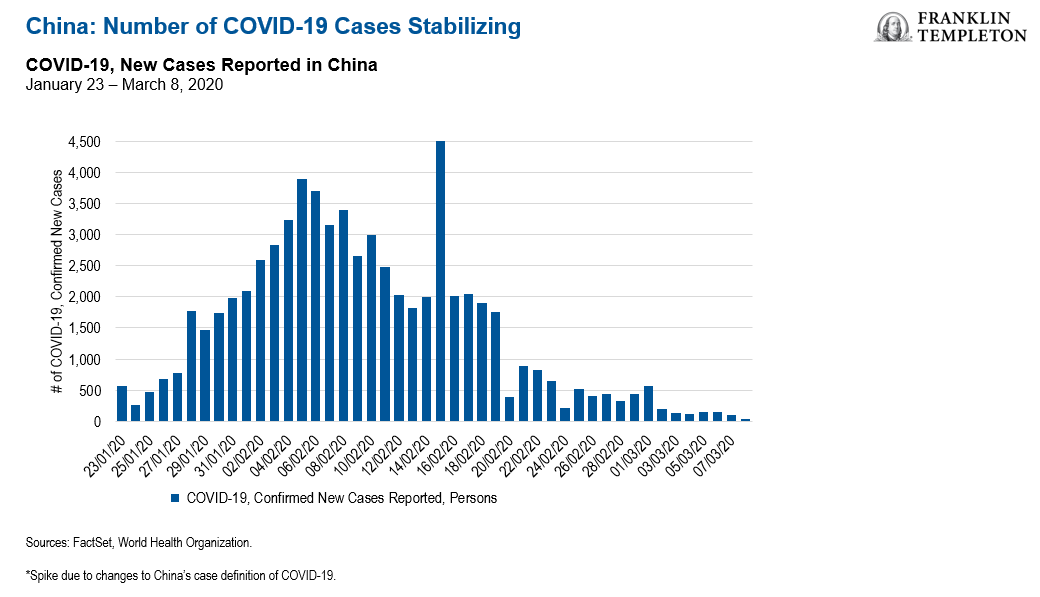

- The Covid-19 coronavirus led the narrative in February, as a spike in new cases outside of China heightened global uncertainty. While new cases in China, Hong Kong and Singapore started to taper, the spread of Covid-19 across Europe and the United States saw financial markets in developed markets drop considerably late in the month. Expectations of weaker-than-expected global energy and metals demand growth (especially from China) also led commodity prices to decline in February. Although this will adversely impact net exporters such as Russia, net importers such as India stand to benefit, in our estimation. Chinese equity markets, however, were resilient in February, as the Chinese authorities’ aggressive steps to contain the spread of Covid-19 started to yield positive results. Supportive action from policymakers including monetary easing, fiscal measures and additional liquidity also helped ease investor concerns. While first-quarter 2020 economic growth is expected to be severely impacted, we could see growth in the short-term continue to be affected as a resumption in Chinese production, and demand may not necessarily translate into a full recovery in exports.

-

South Korea saw a sharp rise in new cases of Covid-19 in February, taking its total to the highest globally outside of China. In addition to China, South Korea is a key supplier in the global supply chain. While large-scale production suspensions were not reported, some production lines were halted for safety reasons. Supply disruptions from China also had an impact. The tourism and retail sectors have, however, been more severely affected. In late February, the Bank of Korea disappointed investors by leaving its benchmark interest rate unchanged at 1.25%, choosing instead to undertake targeted support such as increasing the special lending facility for small companies that were impacted by the outbreak. High household debt levels and real estate inflation remained key concerns. Gross domestic product (GDP) growth estimates for 2020 were trimmed to 2.0% from 2.3% amid increased uncertainty resulting from the virus outbreak. The government is expected to announce a supplementary budget in March to help businesses impacted by the outbreak. We believe that there is significant pent-up demand, which could lead to a swift recovery once the virus has been contained.

-

Thailand was one of the weakest markets in February as Covid-19 and a rise in political uncertainty compounded impact from the country’s worst drought in 40 years, along with budget delays. The government cut its 2020 GDP growth forecast to 1.5-2.5% from 2.7-3.7% as a decline in tourists (especially from China) impacted the tourist-reliant economy, and a strong baht weighed on exports. In addition to new investment measures and tax benefits, the government announced plans to introduce an economic stimulus package covering tourism, consumption and investment in the near term. The Bank of Thailand also cut its benchmark interest rate to a record low of 1.0% in February amid efforts to stimulate the domestic economy. Over the longer term, we are of the opinion that key beneficiaries of Thailand’s economic recovery include exporters, including tourism exports (e.g. airports and hotels) and health care exports (e.g. hospitals a large exposure to medical tourism) as well as consumer staples (e.g. convenience store operators, retailers). Major domestic banks also appear attractively valued to us.

Outlook

The global spread of the virus and interdependence between economies as a result of interlinked supply chains and tourism means that the outbreak cannot be considered an issue localized to China or even Asia. We have seen developed and emerging markets (EM) fall in tandem.

While we have seen a fall in daily new cases in earlier-impacted countries such as China, large outbreaks of Covid-19 in countries such as South Korea, Italy and Iran continue to push up the global number of cases. Government policy should remain supportive as policy makers take actions to support impacted segments of the economy. However, the scale and duration of global demand destruction as a result of policy measures to contain the virus remains unknown.

The resilience and geographical divergence of EMs should not be overlooked. Structural themes remain unchanged, with information technology and consumers playing key roles. While we have seen weak consumer sentiment impacting discretionary purchases and travel, e-commerce, internet and software companies are benefiting from an increase in online activities. In addition, a recovery is likely in semiconductors because demand and supply has been delayed but not denied, and technology evolution continues. However, we do expect a slower recovery in consumer discretionary expenditure. We are also looking for companies that could benefit from any permanent behavioral changes in society as technology is likely to be more strongly embraced. We think companies that are excessively leveraged are best avoided.

Over the long term, history has shown us that markets will stabilize and recover. Valuation and sustainable earnings remain key.

Emerging Markets Key Trends and Developments

Global stock markets declined in February as the widening Covid-19 outbreak heightened world economic growth concerns and hurt investors’ risk appetite. EM equities fell, but fared better than developed market stocks. Oil prices retreated on a softer outlook for demand. EM currencies were mostly weaker against the US dollar. The MSCI Emerging Markets Index declined 5.3%, while the MSCI World Index fell 8.4%, both in US dollars.1

The Most Important Moves in Emerging Markets in February 2020

- A surge in Covid-19 infections outside China, where the outbreak began, pressured Asian equities and prompted the region’s policymakers to introduce monetary and fiscal stimulus. Stock markets in Thailand, Indonesia and South Korea were amongst the weakest performers. Thailand confronted a list of economic and political uncertainties, including the virus’ potential impact on its tourism industry. South Korea reported the second-highest number of cases worldwide. Conversely, China’s stock market rose as the outbreak showed signs of easing in the country. The authorities’ interest-rate cuts and fiscal support, coupled with market expectations for more stimulus, also lifted equities.

- Ongoing fears that the outbreak could impact trade and commodity prices weighed on Latin American markets and currencies in February. The spread of Covid-19 to the continent also raised concerns about its potential spread regionally. Equity prices in Brazil declined the most in the region as depreciation in the Brazilian real and weak economic activity data compounded fears over the outbreak in the country. Lower metal prices and concerns over Chinese demand weighed on the export-driven economies of Chile and Peru. Political uncertainty ahead of the constitutional referendum also led investors to adopt a more cautious stance in Chile. The Mexican market also fell in February but continued to perform better than its regional peers. The Mexican central bank cut its benchmark interest rate by 0.25%, to its lowest level in more than two years.

- Markets in the Europe, Middle East and Africa region lost ground over the month as a significant Covid-19 outbreak in Italy spread across the continent. Turkey, Russia and South Africa were among the weakest performers, ending the month with double-digit declines. A sharp decline in oil prices and devaluation of the Russian ruble weighed on Russian equities. The Central Bank of Russia cut its key interest rate by 0.25% to 6.0% and signaled potential rate cuts later in the year amid lower inflation and risk of a global economic slowdown. South Africa slipped into a technical recession in the final quarter of 2019, exerting pressure on the rand. Finance Minister Tito Mboweni’s 2020/21 budget, which included a larger-than-expected cut in expenditure, however, was well-received by investors in late-February. At the other end of the spectrum, Egypt, the United Arab Emirates and Qatar performed relatively better than their regional peers.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

1. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

More Mutual Funds Topics >