Consistent with misapprehensions expressed during other recent market crises, there has been a chorus of alarmist speculation about the actions and state of risk-parity strategies during the current crash. We felt it would be helpful to revisit the concept of risk parity and take a snapshot of how a typical global risk parity strategy might have been expected to behave this year.

As a quick refresher, risk parity is a global asset allocation strategy that emphasizes preparedness over prediction. The idea is to prioritize DIVERSITY and BALANCE:

- Diversity is about holding markets that are fundamentally designed to flourish in different market environments, and growth opportunities around the world

- Balance is about ensuring that markets with different risk characteristics are able to contribute equally to the portfolio

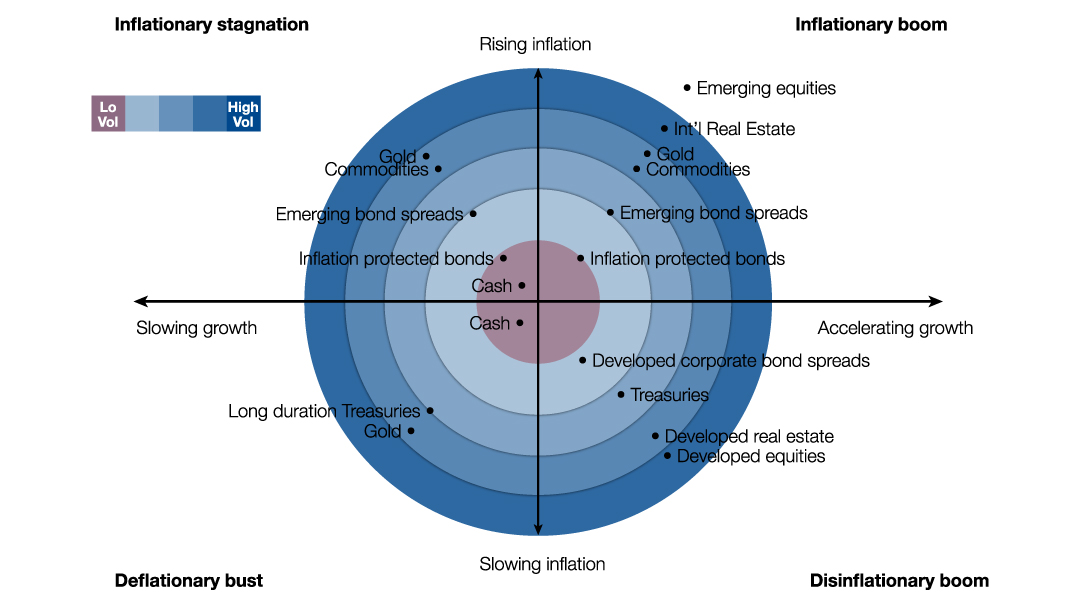

As an asset allocation model, risk parity strategies focus on market exposures with long-term expected positive returns: global stocks, bonds, and commodities. The primary drivers of returns to these markets are unexpected changes to expectations about growth and inflation. Different asset classes would be expected to respond in predictable ways to shifts in these dynamics.

Figure 1. Asset class expected responses to inflation and growth regimes.

Source: ReSolve Asset Management. For illustrative purposes only.

Critically, when constructing portfolios for risk parity the emphasis is on preparation rather than prediction. The strategy is designed to express the view that it is almost impossible to accurately and consistently estimate the future state of markets and the economy. The difficulty in foresight means that we are equally likely to rely on stocks, bonds and/or commodities for returns in the future. From a risk parity standpoint, major global asset classes all have the same expected return when adjusted for their respective risks.

Extreme diversification makes it common for risk parity strategies to exhibit naturally low levels of volatility. To achieve higher return targets, investors may use leverage to increase their exposure to the entire portfolio. Among the most popular risk parity funds, it is most common to scale portfolios to target an 8 percent to 10 percent annualized standard deviation.

Simulating A Risk Parity Strategy

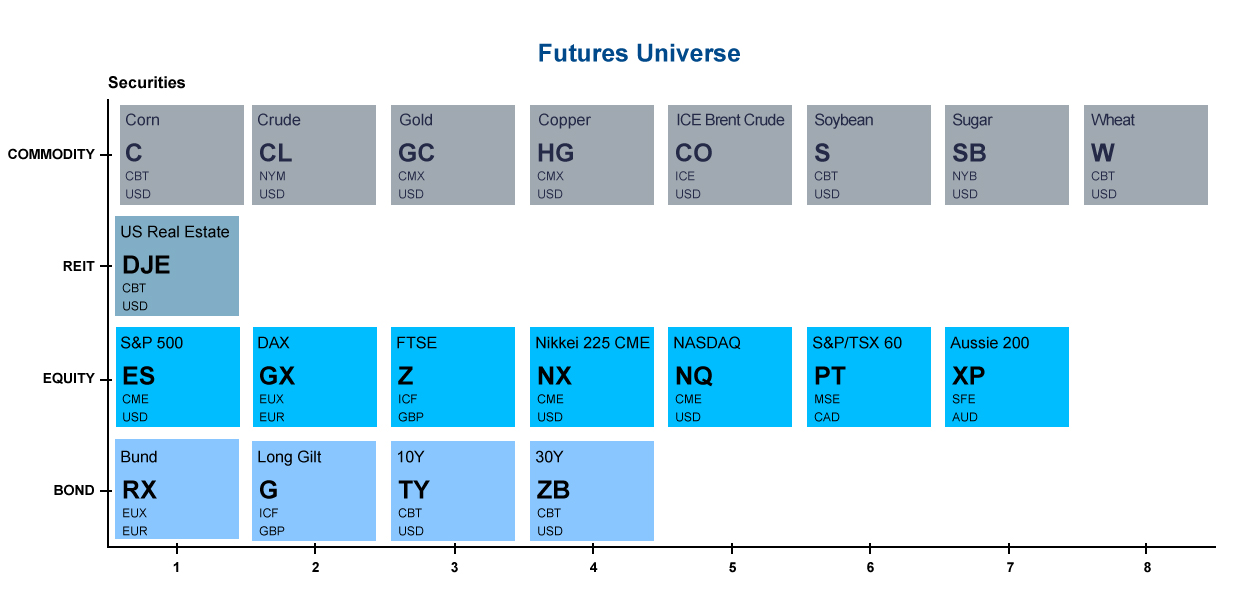

For illustrative purposes we simulated a global risk parity strategy with an investment universe consisting of the global markets we trade in our Adaptive Asset Allocation futures mandates ex currency futures.

Figure 2. Investment universe

Source: ReSolve Asset Management. For illustrative purposes only.

There are many ways to form risk parity portfolios emphasizing diversity and balance that are equally legitimate. And there are many ways to specify the strategy in terms of how slowly the portfolio would be expected to adapt to changes in market relationships (correlations) and risks.

We employed an ensemble strategy combining a variety of portfolio formation methods with a spectrum of lookback horizons to measure risk and correlations. The final simulation was simply an average of the optimal daily weights produced from the ensemble.

We set a target portfolio volatility of 10 percent annualized (approximately 0.6% per day standard deviation) based on the past month’s estimated daily returns. We restricted leverage to 3x cash value and assumed execution at the close one day after weights were generated.

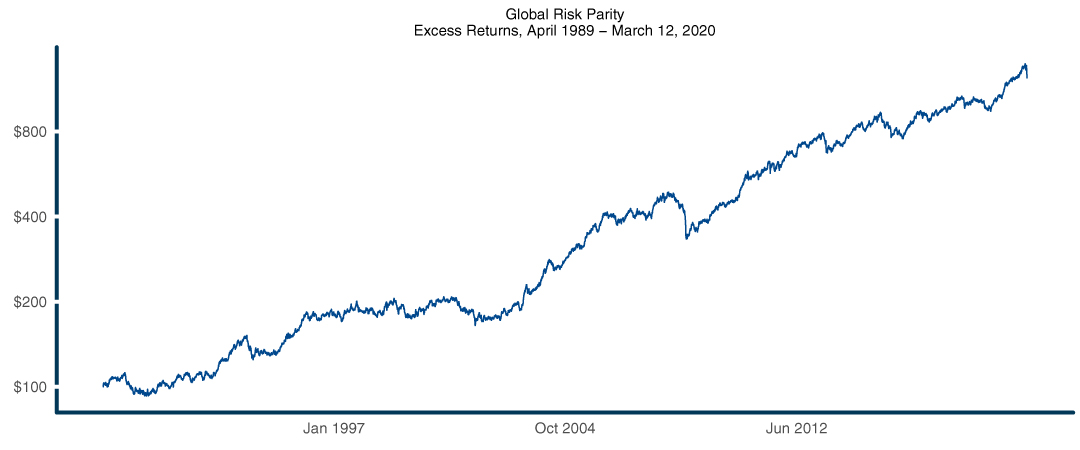

Figure 3. Wealth trajectory of excess returns (in excess of cash collateral) for risk parity strategy, April 12, 1989 through March 12, 2020.

Source: ReSolve Asset Management. Data from CSI Data. FOR ILLUSTRATIVE PURPOSES ONLY.

Source: ReSolve Asset Management. Data from CSI Data. FOR ILLUSTRATIVE PURPOSES ONLY.

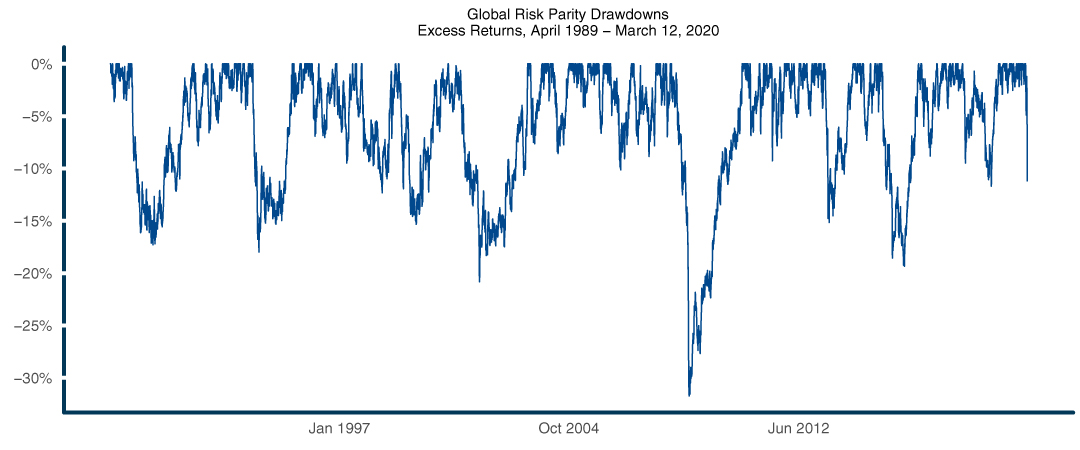

Figure 4. Drawdowns from all-time-high value of wealth trajectory of excess returns, April 12, 1989 through March 12, 2020

Source: ReSolve Asset Management. Data from CSI Data. FOR ILLUSTRATIVE PURPOSES ONLY.

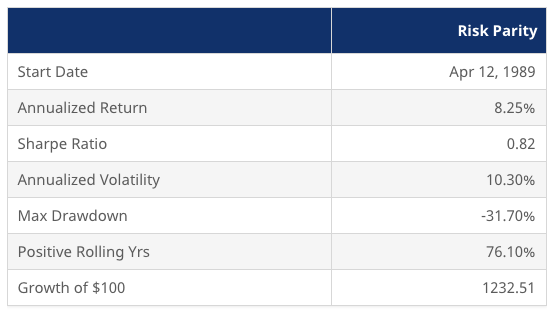

The risk parity strategy produced 8.25 percent per year in compound excess return since 1990 at a realized annualized volatility of 10.3 percent, which translates to a Sharpe ratio of 0.82. The cash yield on T-bills over the same period was 2 percent, and the strategy utilized about 15 percent of margin on average, so the total return including cash yield would have been over 9 percent per year.

The strategy endured a 31.7 percent maximum peak-to-trough loss during the 2007-2009 Great Financial Crisis as it took several attempts before policymakers provided a response that restored balance across global asset classes. This is approximately in-line with the maximum drawdown experienced by a global 60/40 stock and bond fund in the same period.

Risk Parity in 2020

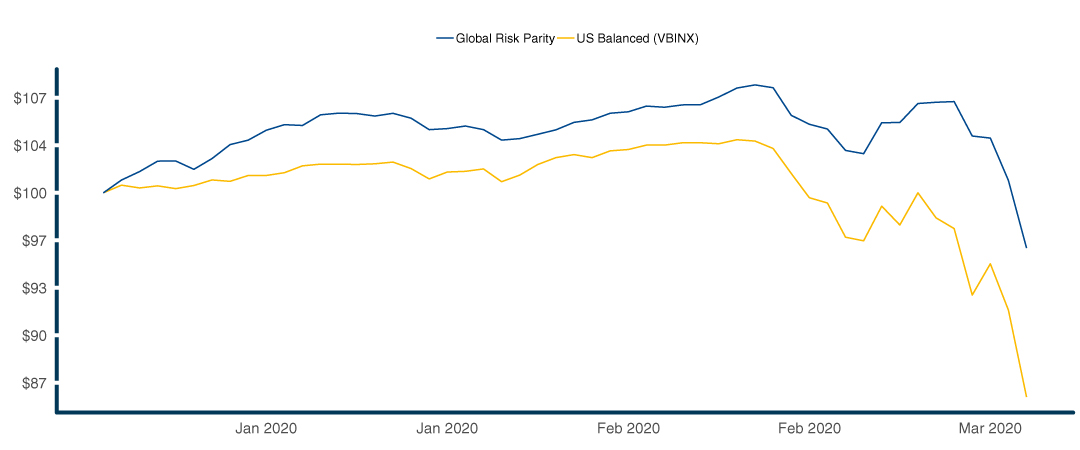

Turning to the recent crisis period, Figure 5 describes the performance of the risk parity strategy in calendar 2020.

Figure 5. Wealth trajectory of excess returns (in excess of cash collateral) for risk parity strategy and US Balanced portfolio, January 1st through March 12th, 2020.

Source: ReSolve Asset Management. Data from CSI Data. FOR ILLUSTRATIVE PURPOSES ONLY.

While the risk parity strategy has suffered losses in the face of the current crisis, it fell by just 11.2 percent from peak to trough. This compares to a 17.1 percent loss over the same period for the Vanguard Balanced Fund (VBINX). Moreover, the risk parity strategy is down just 3.9 percent on the year, compared to 13.85 percent for the balanced fund.

Conclusions

Many popular investment commentators have derided risk parity strategies in the current crash. The nature of their comments belies a fundamental misunderstanding of the nature of the strategy.

Risk parity is simply about diversity and balance. Diversity across economic regimes and balance across markets with different risk character. This balance is specifically designed to produce resilient returns over the long-term, regardless of economic environment.

In observing the performance of a representative risk parity strategy over the current period, we can only conclude that the approach is delivering on its promise exactly. We see no evidence that the strategy has experienced a dislocation or outlier risk event whatsoever. As expected, it is doing a more effective job than traditional portfolios in navigating an environment that is customarily hostile to traditional 60/40 balanced portfolios.

We continue to view global risk parity strategies as an attractive core holding for long-term investors.

© ReSolve Asset Management

Read more commentaries by ReSolve Asset Management