As coronavirus-related market volatility expands into municipal bonds, the Franklin Municipal Bond Department explains how they are navigating an increasingly challenging muni-market environment. They also share reasons why they believe a longstanding preference for high-quality municipal bonds supports their efforts to turn volatility into opportunity.

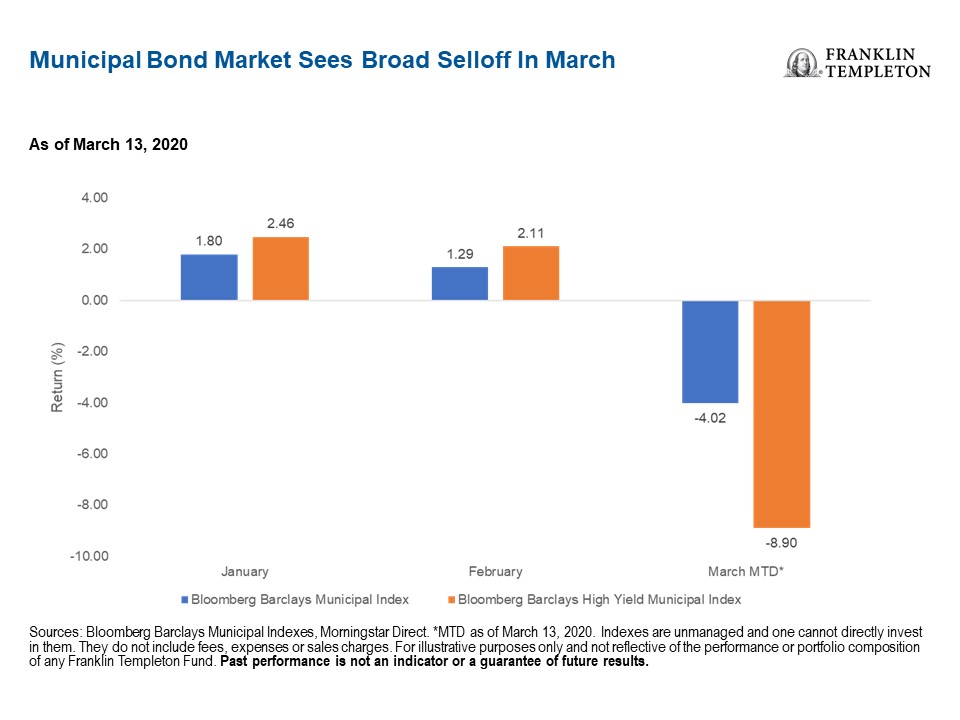

As volatility due to the global coronavirus outbreak picked up across financial markets in late February and into early March, the municipal bond market seemed relatively impervious at first. Then, during the second week of March, the muni market experienced one of its worst single-day price declines over the last decade.1

In our view, it’s premature to predict the full impact of the coronavirus outbreak on society and the US and global economies until the impacts of the COVID-19 pandemic are behind us. However, as the global market turmoil has carried over into munis—a unique corner of the US fixed income market—we wanted to highlight some of the key factors that have rapidly combined to create a much more volatile investment environment, one that we believe our strategies are relatively well-positioned to navigate.

In the United States, the recent selloff in municipals has felt similar to the global financial crisis just over a decade ago, with US Treasuries seemingly presenting the only safe haven in the minds of many investors.

Although uncertainty related to the coronavirus outbreak has been the main reason for muni-market volatility, we have seen a number of other contributing factors as well.

For example, the oil shock that began to hit corporate bond markets in late February and has since gained steam, has started to play a more meaningful role in the municipal market. Another key factor contributing to the recent declines is the fact that the municipal market has recently transitioned to net redemptions after experiencing record cashflows in 2019 and the first two months of 2020. The entire municipal market has sold off, but this may be one reason why high yield has been hit hardest, a risk we highlighted in detail in a previous article in January.

After returning 4.62% for the year-to-date (YTD) through February, the Bloomberg Barclays High Yield Index returned -8.67% during the week of March 9, leaving YTD returns at -4.68% as of 3/13/20.2

Implications for Municipal Investors

Although we believe certain credits and sectors are more likely to be negatively impacted by these factors than others, the recent selloff has been indiscriminate in nature, hitting broad swaths of the municipal market and creating attractive opportunities for some tax-sensitive investors.

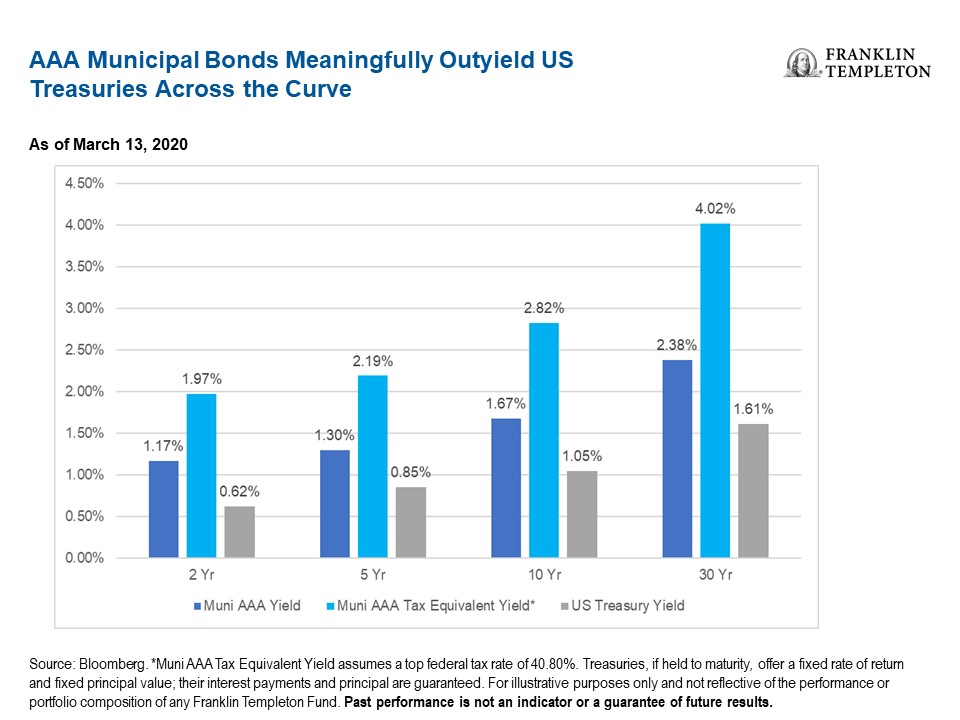

We entered this downturn coming off a strong economy, and we think many state and local governments, as well as most municipal issuers, are fairly well-positioned heading into this crisis. After the recent selloff, even the highest-rated segment of the municipal bond market (AAA) far outyields US Treasuries across the yield curve, and short-term AAA munis are actually outyielding long-term Treasuries in some cases, as the chart below shows.3 Depending on an investor’s tax situation, the yield pick-up provided by municipal bonds versus Treasuries becomes incrementally more compelling.

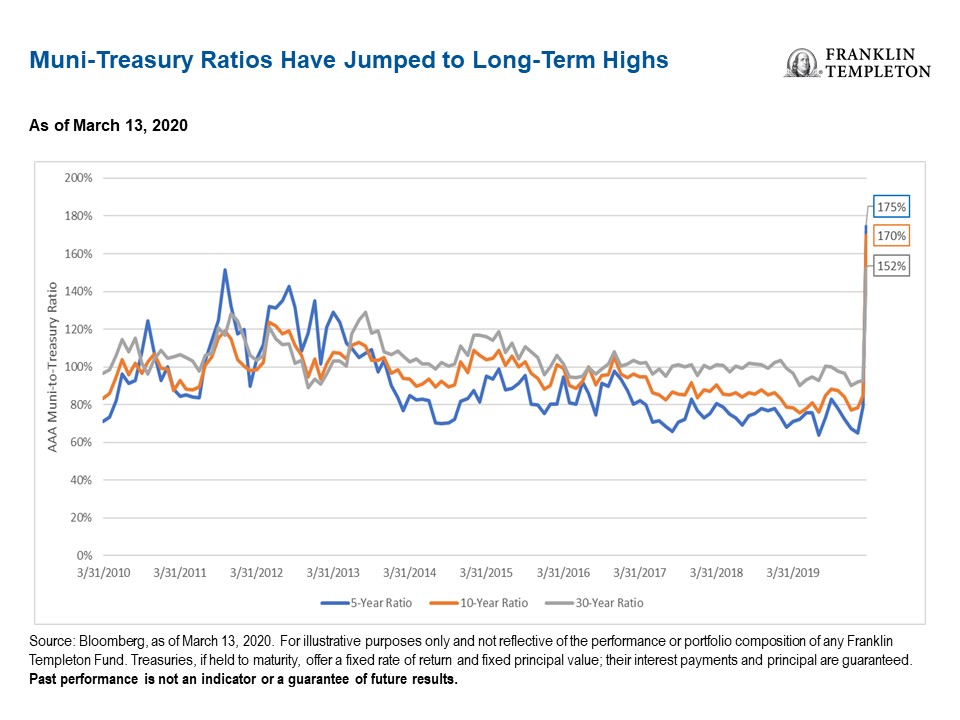

A related measure of relative value to consider is the Municipal-to-Treasury ratio.4 Muni yields are typically lower than those of Treasuries, as their tax-exempt benefits are priced in to some extent; however, as a ratio approaches and/or exceeds 100%, investors are theoretically able to capture the income tax benefit of municipal bonds at attractive valuations.

Given the magnitude of recent market moves, Muni/Treasury ratios have quickly shot up towards historical highs across the curve. Again, it’s important to note that these charts only reflect yields for AAA-rated municipals and that yield potential is even higher when we consider the broader opportunity set.

Franklin’s Municipal Approach

As the market has started to show signs of distress amid extreme volatility, credit research will be critical for those looking to capitalize on opportunities created by the recent selloff. Existing portfolio composition will also determine one’s ability to be nimble amid a rapidly changing environment, as we believe liquidity dynamics could be very challenging for those with levered positions and significant exposure to non-rated securities, especially if investor outflows persist.

For a number of reasons, we believe our approach to municipal investing is particularly well-suited for the volatile market environment. We have focused on purchasing high-quality bonds over the last several years, even in our high-yield portfolios, as quality spreads have been narrow. We have also maintained exposure to pre-refunded bonds over the past several years. Pre-refunded bonds are the most liquid high-quality bonds in the market, and roughly 11.8% of our investment-grade fund assets are pre-refunded.5

Across these investment-grade funds, over 80% of our bonds are rated AAA, AA or A.6 The preference for quality is even apparent in our national high yield fund, which has an average credit quality of A and holds 15% in pre-refunded securities.7 Our portfolios have low amounts of non-rated securities and do not use leverage.

Taken together, we believe these characteristics provide favorable liquidity dynamics across our municipal platform, allowing our portfolio managers to move quickly as indiscriminate selling often creates price dislocations for select credits and issuers. With respect to portfolio positioning, we will look to enhance book yields (and thus income distribution levels) in these market conditions, which often allow us to increase income potential without materially changing a portfolio’s credit quality or duration profile. Capitalizing on these opportunities is much easier in portfolios with strong liquidity, especially as those with greater liquidity risks become forced sellers in order to meet redemptions.

Our seasoned team of analysts and portfolio managers have navigated very difficult times before, and we are using that knowledge to navigate through this panic. While we recognize that volatility is here to stay given the significant level of uncertainty that will continue to weigh on financial markets, we are confident in our ability to provide relative downside protection for tax-sensitive, income-oriented investors.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. Asset types mentioned herein are used solely for illustrative purposes, and any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not an indication of the trading intent of any Franklin Templeton managed portfolio. These opinions may not be relied upon as investment advice or as an offer for any particular security.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Source: Bloomberg Barclays Municipal Indexes, as of March 13, 2020. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

2. Source: Morningstar Direct. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

3. Source: Bloomberg, as of March 13, 2020. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results. Treasuries, if held to maturity, offer a fixed rate of return and fixed principal value; their interest payments and principal are guaranteed.

4. The muni/Treasury ratio is a popular relative value measure, dividing the yield of AAA municipal bonds vs. Treasury yields across the curve.

5. As of February 29, 2020, pre-refunded bonds represented approximately 11.8% of assets across 27 investment-grade funds. Holdings subject to change.

6. As of February 29, 2020, bonds rated AAA, AA or A represented over 80% of assets across 27 investment-grade funds. Holdings subject to change.

7. As of February 29, 2020, Franklin High Yield Tax-Free Income Fund held an average credit quality of A and held 15% in pre-refunded securities. Holdings subject to change.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments