summary

- Elevators and Staircases

- Coronabonds Reopen Europe’s Divide

- Paycheck Protection Pandemonium

Before “normal” was redefined by COVID-19, I spent a fair amount of time traveling to give presentations. (So much, in fact, that my wife used to joke that I should change my address to the airport, because that is where I seemed to live for much of the year.) I enjoy meeting people and listening to what they have to say. I often learn more from their insights than I do from official economic reports. And it is rewarding to help a few of them understand what is going on a little bit better.

Like many of you, I have been confined to my quarters by the pandemic. And I am finding that as much as we frequent flyers complain about aspects of life on the road, I miss it. I miss being on the move and meeting people in person. We’re doing our best to soldier on with webinars and teleconferencing, and we hope these commentaries are keeping you abreast of a rapidly changing environment.

Among the things I do not miss about traveling are broken conveyors. If an elevator or escalator is out of service (not at all uncommon), I must carry my rollaboard up the steps. My bag weighs quite a bit during weeklong trips, and the ascent can be challenging.

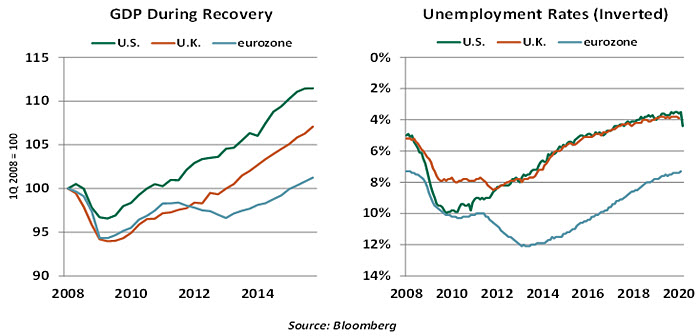

I was thinking of that metaphor as I contemplated the global economic outlook this past weekend. Things have been happening with such speed that it has been hard to forecast with any confidence at all. But one centering principal is likely to govern what’s ahead: economic activity typically descends by elevator, and recovers on the stairs.

The charts below show the progression of growth and unemployment during the recently concluded business cycle.

Across countries, declines in economic fortune are sharp, and recoveries gradual. These patterns exist because businesses are often quick to retreat and slower to re-engage. Because they set payrolls to match their expectations, the labor market also recovers gradually. And because the labor market drives income and consumption, gross domestic product (GDP) can take some time to return to its former levels after a downturn.

Policy measures attempt to change the shape of these trajectories. Direct government spending can replace flagging private demand during recessions. Monetary measures can make credit cheaper and easier to access. The key to bending the slope of the recovery curve is implementing policies that are properly designed and properly scaled. The economic paths different regions follow are a function of their structures and the steps they take to support activity.

“It may take much longer than expected for economic activity to get back to normal.”

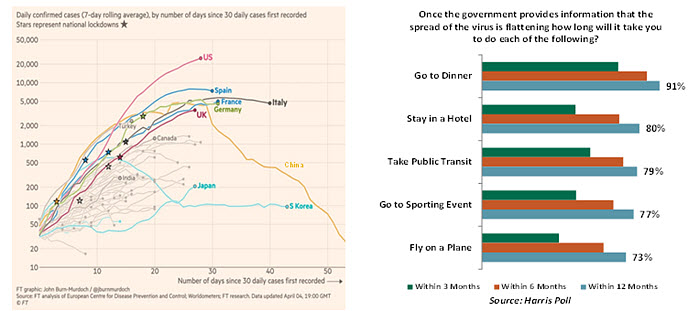

The current economic situation is complicated by another curve, the one that captures the advance of the pandemic. While confirmed cases are peaking in Western Europe, they are still rising in the United States, the United Kingdom and Japan. And as we discussed last week in the context of India, cases are just now taking root in some of the world’s biggest emerging markets.

According to the figures it shares, China is on the other side of the contagion curve and is reopening its factories. The challenge it will face in the months ahead is that export demand is likely to be severely curtailed, meaning that much of its industrial output could sit in inventory until the West begins to recover.

The normalization of commerce depends critically on two sets of decision makers. The first are public health officials, who have implemented increasingly restrictive social distancing measures. They, too, are quick to become conservative and slow to relax. Some areas have quoted April 30 as a decision day, but during the past two months, we have persistently underestimated the ability of the coronavirus to spread. Some places may spend the whole summer awaiting an all-clear.

And when that signal is given, the question becomes how quickly people will get back to their daily business. As shown by the survey above, people may remain hesitant about certain activities long after clearance is given. And because some households will be dealing with lingering economic damage from the early months of the crisis, they may find it difficult to afford things like trips and meals out.

Furthermore, until a broad range of countries has been reopened for business, some global supply chains will not be operable. Lingering restrictions on the movement of raw material, people, and parts will make it difficult for production to resume.

At the outset of the outbreak, some of us thought the impact would be confined to China, and to its manufacturing sector. That ended up being a colossal miscalculation. The medical and economic consequences of the pandemic have consistently exceeded our expectations. The recession we recently entered could be deeper and more lasting that anyone suspected.

“The medical and economic consequences of the pandemic have consistently exceeded expectations.”

After a slow start, policy makers have quickened their pace in providing a range of economic support. Fiscal programs of well in excess of 10% of GDP have been implemented in many countries, and central banks around the world are coordinating to use their balance sheets and printing presses to arrest the decline. But the size—and more importantly, the speed—of the response may still not match the challenge presented by the coronavirus. As astonishing as it may sound, much more stimulus may be needed.

Journalists have tried to characterize the pattern of future economic growth with a symbol. At first, this was a “V,” indicating a brief interruption followed by a rapid recovery. Subsequently, the letter “U” was proposed, indicating a slightly longer time at the bottom but a powerful recovery thereafter. Most likely, though, the quarters ahead will follow the pattern seen after 2009: a checkmark, with a gently-sloped ascent.

That would leave the global economy in the same position I am often in the airport. Trying to ascend, while carrying heavy baggage.

Testing Bonds

At a time when the global economy is bracing for an unprecedented economic crisis, the members of the eurozone common currency region are once again divided over the issue of sharing debt burdens. “Coronabonds” are at the center of current disagreements.

Spain, Italy and France are among the nine nations backing a common debt instrument called coronabonds, for which all 19 members of the currency region would be jointly liable. The aim is to secure stable long-term financing for the policies required to counter the damages caused by the pandemic. The idea was first pitched by Italy during the global financial crisis, with France and Italy favoring the idea during the eurozone’s sovereign debt crisis a few years later. At the time, they were referred to as “eurobonds.”

The prospect has reopened some old fissures in the 19-member eurozone. Repeating the debate over eurobonds, fiscally prudent northern states including Germany, the Netherlands, Finland and Austria have been staunch opponents of the idea, harboring concerns of pooling their liabilities with those of southern countries known for fragile public finances.

Eurozone policymakers have relied on a mix of fiscal and monetary policy to combat the perils of the outbreak, but those measures won’t be nearly enough to address a crisis of this magnitude. Some nations, mostly in the north, have the financial means to fight the crisis by providing generous assistance to their businesses and unemployed residents. Unfortunately, some of the nations facing the worst outbreaks, such as Italy and Spain, are also the most indebted.

Through coronabonds, more-challenged eurozone nations hope to obtain cheaper access to funds for recovery. But issuing these bonds could raise complexities. For starters, which European institution would issue them, and how it would pay for them? The eurozone lacks a treasury with a federal budget; it is a monetary union, not a fiscal one. Additionally, establishing coronabonds would require a change to the European Union treaties since a “no-bailout” clause prevents countries from rescuing each other. The process could take months.

Coronabonds also won’t solve the problem of the heavy debt faced by fiscally and structurally weaker nations. The Italian government might pay a lower interest rate on the debt financed by coronabonds, but the rest of its debt would remain unsustainable.

Those opposing the new bonds prefer the region’s crisis fund, the European Stability Mechanism (ESM). It already has €410 billion, or 3.4% of eurozone gross domestic product (GDP), in lending capacity. Funds made available through the ESM could amount to up to 2% of any member country’s GDP, a rule that can be adjusted in an emergency.

However, coronabond advocates are not in favor of ESM support, as it would likely come with strings attached in the form of Greek-style austerity and structural reforms. Since this crisis is emanating from a pandemic beyond any country’s control, European officials have hinted at an easier stance toward the terms surrounding the bonds.

“This could be an existential moment for the eurozone.”

Europe faces a tough but familiar choice. The circumstances of today’s pandemic are different than those of the 2012 sovereign debt crisis, but the divisions over a common debt instrument are the same. In the long run, the best way forward will be to build both a fiscal and a political union, but that will be no small undertaking. Until then, the bloc must find a practical fix to existential problems. Failure to support those states in dire need will hurt the European project, already under attack by anti-EU parties across the continent. In many ways, this could be an existential moment for the eurozone.

Funding Frenzy

Last Friday, April 3, the U.S. Small Business Administration (SBA) launched the Paycheck Protection Program (PPP). This component of the CARES Act offers a new type of small business loan that can be forgiven if used for payroll expenses.

PPP loans are available to businesses with fewer than 500 employees and are guaranteed by the SBA. Terms are friendly for borrowers, with no fees, a 1% interest rate, no payments for six months and no collateral required. Eight weeks of costs including rent, utilities and payrolls can be eventually forgiven. Employment is the program’s focus: 75% of the forgiven amount must apply to payrolls, and employers must maintain headcount or quickly rehire.

These terms have proven popular. The SBA reported more than 17,000 loans worth over $5.4 billion were issued on PPP’s first day, with the total shooting up to $66 billion the following business day. It is evident that the $349 billion PPP funding from Congress may be exhausted far ahead of its June 30 application deadline, leading to calls this week for additional incremental financing for the program.

The SBA relies on banks to issue business loans that the SBA guarantees. And this is where complications arose. Just one week passed between the signing of the CARES Act and PPP’s launch. Government programs are typically designed and communicated over a span of months, not days. PPP is a large program, in high demand, implemented by thousands of independent banks. Some stumbles were to be anticipated. Banks reported unclear and sometimes conflicting guidance on underwriting requirements for PPP loans.

To ensure stability, the U.S. Federal Reserve announced its intention to purchase PPP loans. This is a novel way to bring liquidity into the lending market. The Fed will fund PPP loans with newly created money, which will not return if the loans are forgiven.

“Judging by demand, the PPP experiment is a success.”

Like all provisions of the CARES Act, PPP is temporary and meant to support business through a brief disruption. But the timeline of eight weeks until businesses return normal staffing may be too optimistic. The surge in initial unemployment claims has been discouraging, and no one would welcome an echo when PPP expires. And the money must reach small businesses before they reach the point of closure, which makes speed of the essence.

Given its high demand, we expect to see PPP’s funding expanded. If it is executed successfully, we may mark it as our first new entry in the playbook for future crisis responses.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust