Rarely has market performance and sentiment changed so quickly than what has been observed in the first quarter of 2020. The start of the year was promising, with the S&P 500 climbing above 5% through the middle of February. This performance came on the heels of very strong equity returns in 2019, in which the market gained more than 30% despite a lack of underlying earnings growth. However, the onset of the coronavirus has introduced a completely novel variable to both society and financial markets.

While there is little doubt the economy will struggle in the near term, the big question, and one that only time will answer, is whether the current disruption to our lives and the economy will be sharp but short, or sharp and elongated? Any prediction here is fraught with unknowns. On the one hand a high degree of economic damage has been discounted into equity markets and most economists are now calling for an economic contraction between 20% and 25% in the second quarter of 2020. The fiscal and monetary policy reaction is unprecedented and highly accommodative as the government seeks to build a bridge to the other side of this crisis. What we don’t know is the tail length of the virus and the shape of the recovery. Will the virus be contained quickly with a relatively quick return to normal life or will the virus itself and the aftereffects linger?

Another big story is oil. If it weren’t for the coronavirus, crude oil prices would be the story of 2020. Part of the decline relates to demand destruction brought on by the coronavirus, but Saudi Arabia’s actions to protect market share in its spat with Russia has been an added factor behind crude prices falling to levels not seen since 2003. While lower oil prices are positive for consumers and transportation companies, they are highly destabilizing to other parts of the economy. Energy companies quickly come to mind, but a fair chunk of the industrial economy is tied to oil equipment and services, and a strong ripple can also be seen in credit markets, where billions of dollars of energy debt are owned. The risk of financial contagion creates an “unknown,” and memories of 2008 are unsettling to financial markets.

The last big story of the year is the speed with which all of this happened. The 34% peak-to-trough decline from market highs has been truly breathtaking, and according to BofA Global Research marks the fastest time to a 30% or greater market correction in history. To put it in a more recent context, we looked at the VIX measure of market volatility, which typically spikes during market corrections. In the Great Financial Crisis, the VIX took about 100 days to rise from 20, the start of elevated volatility, to 80, its peak. In 2020 a similar rise took only 15 days! Much of this can be explained by overly bullish positioning heading into this correction, but the combination of quantitative investment strategies and leverage cannot be overlooked.

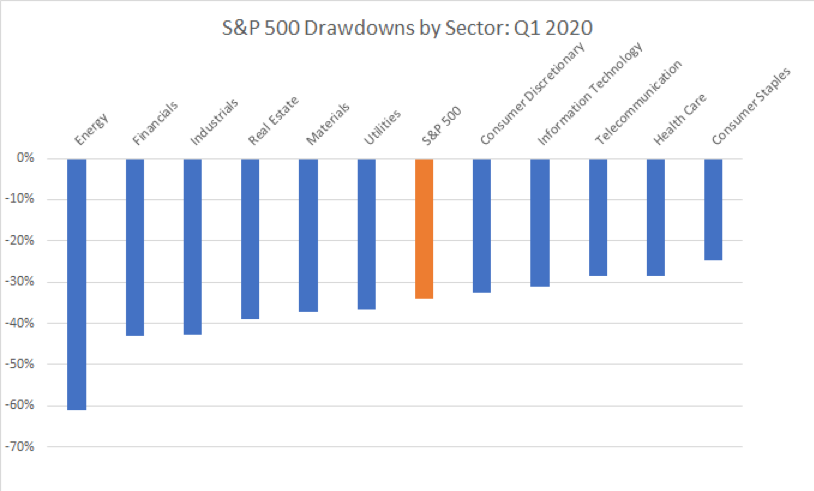

The impact of all of this is a nearly 34% correction in the S&P 500 from peak to trough. While pain has been felt across the entire market, it has not been uniform. In fact, from our perch, we think the market has been rather rational in sorting out those industry sectors and business models that are most at risk relative to those that are more durable and insulated. For example, the most pain has been felt in energy, which makes sense given the dual challenges of a global demand shock and the aforementioned price war. On the other end of the spectrum, consumer staples and health care have held up the best. Given that the vast majority of the country is currently sheltering-in-place, increased demand for consumer staples makes perfect sense. Health care has held up due to a mix of defensiveness, particularly in pharmaceuticals, and a strongly held belief that the decline in elective procedures is transitory. Telecommunications and information technology were the next strongest sectors, and we suspect remote work and increased demand for data center processing are the key supports behind both.

Source: Bloomberg

One area where we are willing to make a prediction – no matter the shape of the recession – strong companies will come out stronger and weak companies will come out weaker. This is the underlying hypothesis to portfolio changes that we have recently initiated. This is no bottom call. Rather it reflects our view that the market correction has put a good number of market-leading companies on sale at what could be generationally low prices. We have actively sold companies that have high leverage, are potentially exposed to dilutive capital raises and government bailouts, and face higher risk of experiencing an L-shaped recovery in their business relative to the shape of the economic recovery. In their stead we have purchased leading companies that are likely to accelerate their market share gains, have measurable moats around their business, are well capitalized, and are more likely to experience U- or even V-shaped recoveries relative to the overall economy. On average, the companies we recently purchased pay a 2.6% dividend and trade at an average of just 11.5x normalized earnings. Whether the normalized earnings estimates are two, three, or four years out will depend on the overall recovery, but these multiples on market-leading companies provide very attractive entry points that cannot be ignored.

On the fixed income side, the financial meltdown caused a dramatic widening of spreads in both investment grade and high yield bonds, though they did not surpass their 2008 peaks. High yield spreads swelled to over 10%, which may be good news according to a blog post by Barclays. In the piece, they point out that anytime spreads have widened this dramatically the high yield bond market has returned 36% on average over the ensuing 12 months, 25% per year over the ensuing 24 months and 20% per year for the subsequent three year period. If history repeats itself this time, one would conclude that the corporate bond market has probably passed the point of maximum pain and should be poised for a significant recovery.

One final note. There was significant insider buying of stocks during the worst part of the first quarter meltdown. This is usually a good sign indicating that corporate insiders believe their company’s stocks are oversold and represent real value. We know the next few months are likely to be volatile, but we also know that strong companies vital to the economy will come out ahead as things return to normal, however slowly. We can now buy such companies at significant discounts to where they were trading before the crisis.

Please let us know if you have questions. Meanwhile, stay healthy.

Sincerely,

John Osterweis, Larry Cordisco

Past performance is no guarantee of future results. Index performance is not indicative of fund performance. To obtain fund performance call (866) 236-0050 or visit osterweis.com.

This commentary contains the current opinions of the author as of the date above, which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

The Chicago Board Options Exchange (CBOE) Volatility Index, or VIX, is a real-time market index that represents the market's expectation of 30-day forward-looking volatility.

The corporate earnings cited are trailing 12-month earnings per share after extraordinary items.

Price-to-Earnings (P/E) ratio is the ratio of the stock price to the trailing 12 months diluted earnings per share (EPS).

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance. One cannot invest directly in an index.

Earnings growth is not a measure of the Fund’s future performance.

Holdings and sector allocations may change at any time due to ongoing portfolio management. References to specific investments should not be construed as a recommendation to buy or sell the securities by the Osterweis Fund or Osterweis Capital Management.

[44787]

© Osterweis Capital Management

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management