summary

- Small Businesses Cast A Large Shadowargumen

- Oil’s Not Well

- Reopening? Haste Makes Waste

We love tales of successful entrepreneurship. We admire tech titans who start by cobbling together computers in a parent’s garage, researchers who spend years perfecting and then producing revolutionary medical therapies, and small people with big ideas who overcome serial failure to produce an overriding success. Their creativity, drive and dedication serve as an example for others to follow.

But small businesses are not only a source of inspiration. Small businesses are the growth drivers of modern economies. They are a vital source of innovation and employment, and they are fixtures within their communities. Unfortunately, small businesses have been placed at significant risk by the coronavirus. Governments around the world are racing to support them before they fail.

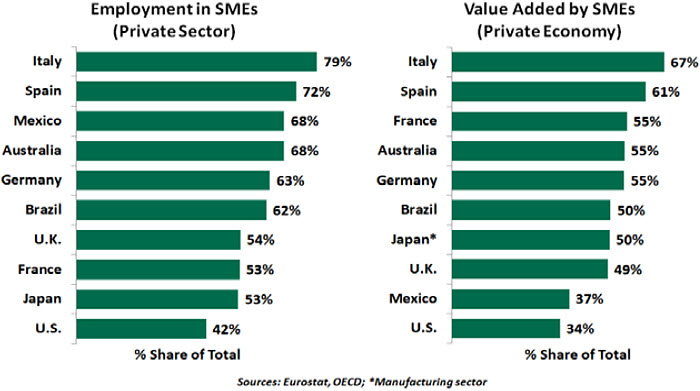

The definition of small-and-medium-sized enterprise (SME) has some local variation. The European Union (EU) defines a medium-size company as one with up to 250 workers, while the U.S. Small Business Administration (SBA) typically supports businesses of up to 500. According to the World Bank, SMEs account for the majority of businesses globally, representing over 90% of all firms and over 50% of employment worldwide.

In high income, Organization for Economic Cooperation and Development (OECD) countries, SMEs account for the vast majority of companies (99% of all firms), about 70% of employment and more than half of value added. SMEs in emerging markets (EMs) represent a little less than half of total employment and about one-third of gross domestic product (GDP). If one accounts for the large informal sector in countries like India, their importance is likely to be even greater than is reflected in formal statistics.

Entrepreneurship has long been vital to global economic policy. It represents a path to prosperity for those willing to work hard and serves as a source of constant economic renewal. An OECD survey shows that SMEs participate significantly in a range of innovative work: For example, SMEs account for about 20% of patents in biotechnology-related fields in Europe.

Recognizing the importance of the small business sector, countries around the world have established agencies to aid them. The U.S. SBA was created in 1953 to guarantee loans to SMEs. SMEs have been a focal point in shaping the EU’s enterprise policy. And China has worked hard over the past few years to diversify away from large state-owned enterprises and encourage the formation of more fledgling firms.

“COVID-19 has dealt a severe blow to SMEs, the backbone of the world economy.”

But with over half of the world population now under some form of lockdown, smaller businesses are bearing the brunt of reductions in global demand. According to a survey of over 1,500 small firms in the United States, 51% of owners said they will be able to continue operations for less than three months in the current economic environment. A February survey of China’s SMEs revealed that only one-third had enough cash to cover fixed expenses for a month. At a European level, about 90% of SMEs have experienced business losses of at least 50%.

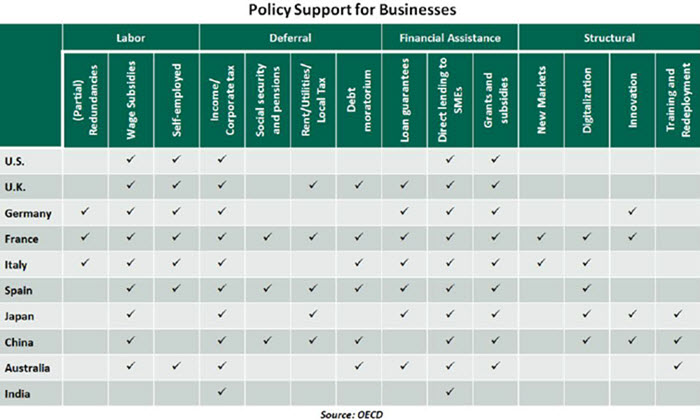

Policymakers across the world are making unprecedented efforts to help SMEs stay in business and sustain their employment. Those measures include temporary tax relief, direct financial support, loan subsidies and moratoriums on debt repayments. Some prominent examples are:

- The U.S. SBA’s new Paycheck Protection Program will forgive loans if they are used to maintain payrolls. Its initial $349 billion of funding was consumed within two weeks, and this week’s fresh tranche of $310 billion will meet high demand when it is released.

- Among European nations, France took the lead on SME funding, with French banks offering more state-backed loans than other countries in Europe. The Italian Banking Association agreed to a large-scale moratorium on debt repayments, including mortgages and repayments of small loans and revolving credit lines for businesses. The U.K. announced cash grants of £10,000 for eligible small businesses and up to £25,000 for SMEs in retail, hospitality and leisure; a 100% business tax holiday has been established for the next 12 months.

-

The Reserve Bank of Australia has established a term funding facility of at least $50 billion for the banking system, including credit support to small- and medium-sized businesses.

- Asian economies including South Korea and Singapore are offering flexibility for repayments of existing loans. India increased the threshold for starting insolvency proceedings against SMEs in default by a factor of 100.

“Governments must do “whatever it takes” to maintain a vibrant small business community.”

Even though many small firms might manage their way through this crisis without permanent scars, the hurdles are only going to increase in the aftermath of the Great Lockdown. Access to credit has always been a challenge in this sector; the crisis could do damage to the banks and investment pools that have traditionally arranged financing for younger companies. International capital has grown as a resource, but advancing protectionism could restrict inbound investment. In one recent example, India amended its foreign direct investment rules to halt the acquisition of Indian businesses by neighboring countries, with an eye on China. Australia and the European Union are considering similar moves.

Though the current support measures might help alleviate some pain, they are likely to fall short of providing relief to all who have been affected by this unprecedented crisis. Widespread bankruptcies are a potential byproduct of prolonged virus containment measures. Considering the World Bank’s estimate that 600 million jobs will be needed in the next decade to absorb the growing global workforce, governments will have to ensure SMEs not only survive but are ready to thrive when growth resumes. Substantial assistance is on offer to SMEs, but it is also vital to ensure that the support schemes are easily accessible and topped up where necessary.

Every business leader can share war stories of times when they faced difficult circumstances, only to survive and emerge even stronger. Today’s circumstances, though, may fall beyond the capacity of even the most intrepid entrepreneurs to adapt and overcome. Policy will need to raise the odds that small businesses survive; for their sake, and for ours.

Losing Energy

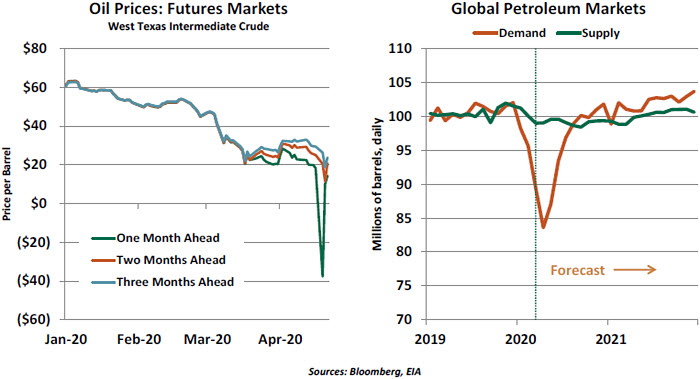

If these were normal times, the biggest story in the global economy would be the collapse in oil prices. Crude has been in retreat for six weeks; conditions reached a strange nadir this week when some spot and futures prices for a barrel of oil went below zero. That extreme resulted from technical factors in the energy markets. But fundamentally, there is a glut of petroleum accumulating, and it may take a long time for it to dissipate.

About 70% of fuel derived from oil is used for transportation: road, rail, sea and air. When COVID-19 first emerged, factory shutdowns in China interrupted supply chains and left rail cars and tankers idle. As the virus spread to other countries, social distancing measures led to tens of thousands of cancelled flights, a steep decline in car traffic, and further impairment of shipping. Restrictions on movement are still spreading and strengthening, and will likely take some time to relax. In all, petroleum demand has collapsed by about 20% from former levels.

On the supply side, global oil production has remained strong. Failure to agree on output restrictions led to a damaging battle between Saudi Arabia and Russia. The oil market was almost literally being flooded with crude, to the point where storage began to reach capacity in some places. If the intent of the Saudis was to punish overproducers, or to do damage to competitors, the effort has been a success.

In a landmark arrangement, the United States joined an agreement with the Organization of Petroleum Exporting Countries (OPEC) and Russia in a plan to reduce production. (The prospect of the U.S. collaborating with OPEC to reduce oil supply would have been anathema twenty years ago.) The new guidelines went into effect this week, but will not be nearly enough to bring prices back to their levels of early this year.

Prices are too low to support new development, so companies that supply equipment and engineering expertise will see their business dwindle. Existing wells are being closed off at a rapid pace, because the cost of extraction is far above the prevailing market price. This has been especially harsh for U.S. and Canadian producers. Some smaller energy companies have borrowed substantial sums through bond markets; some analysts are expecting default rates on those issues to approach 20% by the end of this year.

“Supply controls will not offset a substantial collapse in the demand for oil.”

The American shale industry has appealed for federal relief, noting the strategic importance of energy independence. But other industries are at the head of the line. There are also those who note that some oil producers (and the investors who finance them) inherently take risks that the public should not have to backstop.

In the U.S., energy-producing states are going to see an extra measure of unemployment and additional declines in tax revenue. On a broader scale, energy-producing countries will feel a pinch if oil prices remain low. For countries that are heavily dependent on petroleum proceeds, significant holes will appear in their national budgets. Some will fill these holes by drawing down their financial reserves; those without reserves will struggle to sustain public spending and social stability.

In normal times, cheap fuel would be a boon to consumers and importers. But because driving and flying have been so severely curtailed, the benefit to households will be limited. If there is any consolation at all, it is that air quality in many parts of the world has improved, at least temporarily.

Many forecasters are still predicting oil prices to return to the $50 range in the next year or so. That outlook is predicated on the assumption that economic conditions will normalize at a reasonable pace, which is not at all certain. The global energy industry, and the communities that depend on it, are facing a very difficult interval ahead.

Argumentum Ad Absurdum

Tradeoffs are central to economics: Debt vs. savings, free markets vs. regulations, risks vs. rewards. We relish spirited debate around these balancing acts. Keep us talking long enough, and we may argue both sides of an issue. But sometimes, a clear answer emerges.

We think this applies to the debate over the post-quarantine recovery. A reader of the situation may conclude that communities are fighting with epidemiologists over when to lift economic restrictions. If only those meddling doctors would stand down, some say the economy would bounce back. We disagree.

A return to robust economic activity requires a populace that feels safe to leave their homes, go to businesses, earn income and spend it. Rushing a return to business-as-usual too soon could lead to a second wave of infections, which could be even more commercially and psychologically harmful than the current outbreak. And reopening businesses does not guarantee a return to business-as-usual, amid lingering public concern that crowded areas may be unsafe for some time to come.

“Health and income are both vital needs, but you can’t have one without the other.”

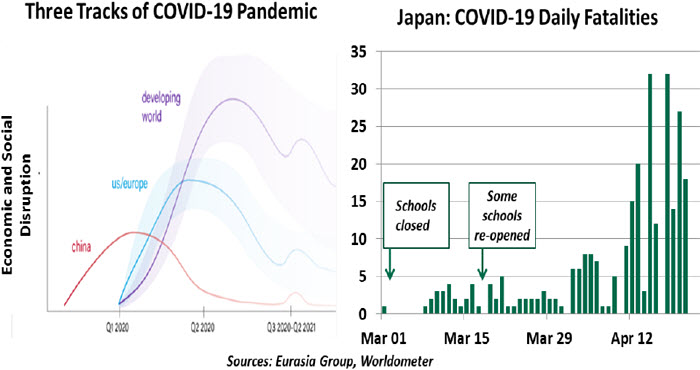

The desire to reopen is understandable. Our incomes are down, our jobs and businesses are at risk, and frankly, we’re bored. Quarantine measures reduce the spread of infections, but paradoxically, fewer infections can make us think the risk was overstated. Officials in Japan and Singapore found themselves fighting a second wave of infections after initial restrictions mitigated the risk and were then relaxed. We also take heed from the 1918-1920 influenza pandemic: regions that practiced aggressive social distancing saw less severe outbreaks and greater economic activity when the disease subsided.

Today’s Great Lockdown is a circumstance we have no choice but to accept. This is a public health crisis, and health experts must determine the appropriate timing and pace of resuming activity. In the long run, following their instructions will likely lead to the best economic outcomes..

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust