As headlines revolve around the impact of the coronavirus and the costs of government spending packages to keep the economy afloat, the state of Social Security is one thing we can find at least some assurance in, says Gail Buckner, our personal retirement and financial planning strategist. She takes a look at the latest Social Security Trustees’ Report, released on April 22.

If you’re like most other Americans, you have a retirement plan that is not affected by what happens on Wall Street/in the financial markets.

It’s called “Social Security.”

Social Security was one of several federal programs created in response to the Great Depression, which started in 1929 and lasted a decade. By 1933 the nation’s unemployment rate had hit 25%. One out of four working Americans had lost their job. There were literally Americans dying on the streets of our cities because they could not afford food or a place to sleep. Many of them were our most vulnerable citizens—the elderly.

That year, under newly elected President Franklin Roosevelt, Congress passed the first “New Deal,” a package of short-term economic programs which, among other things, included work assistance programs and financial aid. It also put an end to the gold standard and introduced prohibition. Two years later, a second wave of New Deal legislation was signed into law creating the Securities and Exchange Commission (SEC), the Federal Housing Administration (FHA), the Social Security Administration and other programs. Despite this, in 1937 the economy collapsed into recession.

It was not federal programs or federal aid, but war that brought the United States out of the dark days of the 1930s. When President Roosevelt decided America would help Western Europe fight back Hitler’s Germany, millions of able-bodied men were suddenly employed—by the US military. By 1943, America’s unemployment rate was down to 2%.

What Is Social Security?

If you strip away the misconceptions and the drama that often surround the program, Social Security is an annuity—an account that is guaranteed to pay you a certain amount of money each month. You can buy an annuity from an insurance company, but it would not even approximate the benefits that Social Security offers. Although it began as a retirement income program, over the years Congress has greatly expanded the benefits that Social Security provides.

For instance, if a worker becomes disabled and is unable to work, she/he can receive a benefit at any age. So can family members such as spouses, minor children and dependent parents. When you die, close family members who survive you—such as your spouse and children—receive a benefit. Importantly, unlike the pensions so many people remember from the “good ol’ days,” you don’t lose your Social Security if you change jobs; your account is tied to your work history, not a particular employer.

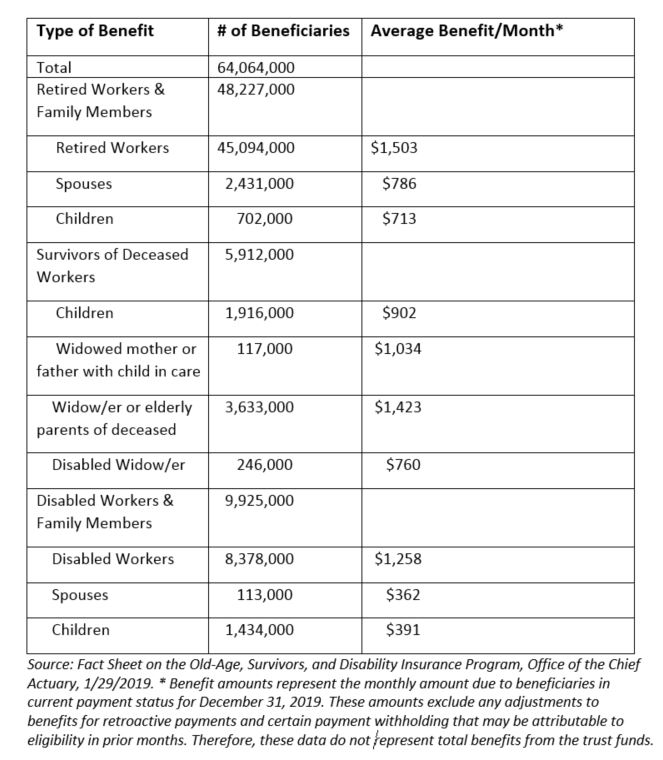

In December of 2019, Social Security paid out more than $88 million (monthly rate) to over 64 million people. Here’s a breakdown:

Show Me the Money

Both you and your employer contribute to your Social Security account. Each pay period, 6.2% comes out of your paycheck—half the Social Security tax rate of 12.4%.1 Your employer adds another 6.2% and sends the total to the US Treasury, which credits the two Social Security “trust funds.” (One fund pays “retirement” benefits, the other pays “disability” benefits.) At the end of last year, these two funds held a combined $2.895 trillion.

Contrary to pervasive rumors, the government cannot “borrow” money from either of the Social Security trust funds. This misconception probably arises from the fact that Congress mandated that excess cash in the trust funds had to be: 1) invested so that it earned a profit, and 2) invested in absolutely safe securities. Thus, excess cash is invested in special US Treasury bonds that are only issued to the two trust funds and which pay a market rate of interest. In fact, the interest paid by the federal government on these bonds is a significant contributor to Social Security’s financial health, amounting to nearly $81 billion in 2019!2

Setting the Record Straight

Another widespread “myth-understanding” is that Social Security is “going broke.” The causes are supposedly the aforementioned “borrowing” of Social Security funds to pay for other federal spending and wasteful spending by the Social Security Administration itself.

Let’s look at the facts.

Overall, the federal government’s budget is more than $4 trillion a year. The biggest portion of that goes to Social Security beneficiaries.

However, the money that Social Security sends to retirees, surviving spouses and children, the disabled and others entitled to a benefit is based on money that these individuals—and their employers—contributed. It also includes interest on the Treasury bonds in the two Social Security trust funds as well as income tax that higher-income retirees pay on their Social Security benefits. In other words, Social Security benefits are not paid out of general federal income tax funds or other sources of money the federal government receives.

In addition, the administrative cost of running the Social Security is also borne by those who benefit. A portion of the payroll tax that American workers and their employers pay covers the expense of running the Social Security Department, which is one of the leanest in the federal government. Administering the program represents roughly one percent of its total annual cost.

The Long-Term Outlook

By law, every year the Social Security trustees have to report on the 75-year outlook for the program’s finances. The latest report came out on April 22, 2020. (It does not take into account the high unemployment rate caused by the COVID-19 pandemic, because it is too early to accurately compute this.)

Here are a few of the things that Social Security experts are expected to predict—for each of the next 75 years (!)—in order to create this report:

- How much in benefits the program will be required to pay out?

- What will be collected in the form of payroll tax and interest on the trust fund bonds?

- How fast will the economy grow?

- What will the birth rate be?

- What will the unemployment rate be?

- How long will people live?

- How will average earnings grow?

As Yogi Berra once said, “It’s hard to make predictions. Especially about the future!”

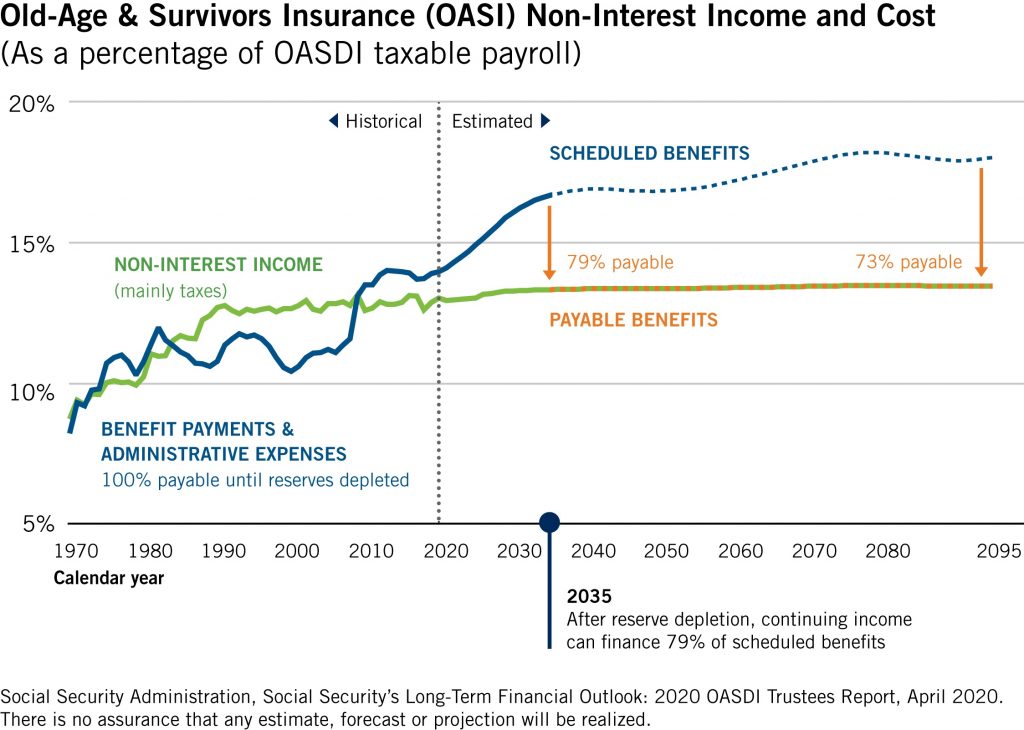

The full report runs more than 100 pages. The chart below sums up the part most Americans are interested in:

Translation: The green line shows past and projected income in the form of payroll tax paid by workers and their employers. The blue line represents the cost of running the Social Security program, which includes benefits already paid or owed 75 years in the future.

The dotted blue line indicates that by 2035 Social Security will only be able to pay 79% of the benefits it will owe. The main reason is demographic: since around 2000 there has been a substantial increase in the number of individuals retiring. Many Baby Boomers did not have large families, so there aren’t as many workers coming up behind them and contributing to the program.

We’ll be fine for the next 15 years because the excess money in the trust funds can make up the difference. But that’s projected to be used up by 2035. At that point, unless something is done, the only source of money Social Security will have is the payroll tax paid by current workers and their employers. That will only be sufficient to cover 79% of the benefits that will be owed.

Deeeeeeeep breath.

- This is not a surprise. Congress has known about this for more than a decade.

- This is not Social Security’s “fault.”

- We’ve been here before: President Reagan had to tackle this in his first term.

- We have 15 years to address this. Reagan had two years.

- It would not take much to fix the situation. Pennies on the dollar.

- How? We ever so slightly raise the Social Security tax. It’s been done before.

Doing the Math

The current Social Security tax rate is 12.4%. Employees and employers each pay half of that: 6.2%. According to this year’s Trustees report, if each party paid a little more: about one and a half cents more for every dollar you earn or $16 per $1,000 you make (up to this year’s maximum of $137,700), everyone would receive the benefit they’ve earned for the next 75 years.

The longer we delay, the bigger the fix.

This information is intended for US residents only.

1. Beginning in 1966, Congress authorized an additional Medicare hospital insurance (HI) tax. Today, employers and employees each contribute 1.45%. An additional Medicare tax is paid by individuals with income earned income above $200,000 or above $250,000, if married.

2. Source: 2020 OASDI Trustees Report, www.sssa.gov/OACT/TR/2020/II_B_cyoper.html

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments