summary

- Has China Been Cured?

- Auto Sector Skids

- Mexico’s Fiscal Past Clouds Its Future

The coronavirus has exacted a significant toll on economic activity around the world. Many indicators appear to have fallen off a cliff, as stay-at-home guidance depresses commerce. We may not see a bottoming in the data for several months.

Fortunately, growth in coronavirus cases has slowed in many places, allowing the contemplation of reopening. From the country of Germany to the U.S. state of Georgia, public health officials have granted additional freedom of movement, albeit with some lingering restrictions. The outcomes of these experiments will serve as useful guides for other jurisdictions seeking to restore economic activity.

Interestingly, few are paying much attention to the lessons offered by China’s experience. China was the first country to confront the coronavirus, and the first to reopen after the contagion had been arrested. The country claims to be almost fully recovered, but doubts surround China’s medical and economic accounting. In the aftermath of the pandemic, China may never get back to business as usual.

The origins of the coronavirus are the subject of some controversy. Western scientists think it originated late last year, in a market in southeastern China. Some governments are now pressing the Chinese for explanations and reparations.

After initially suppressing information about the outbreak, China moved with speed and force to limit the spread of the virus. Wuhan, a city of 11 million, was locked down; strict limitations on movement were enforced elsewhere in the country. These measures, however draconian, apparently arrested contagion.

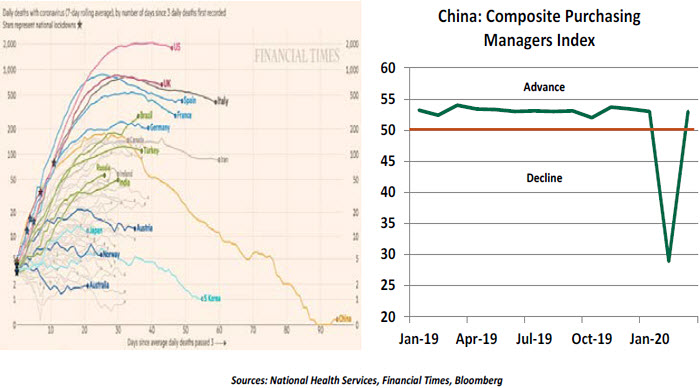

According to Chinese accounts, new cases have fallen to only a handful each day. Although China’s population is more than four times larger than the U.S., only 4,600 Chinese are reported to have died from the disease, less than one-tenth the toll in the United States.

“There are questions surrounding China’s medical and economic information.”

External observers have expressed doubts about China’s patient counts. During the height of the infection in Wuhan, case reports fluctuated wildly, as different definitions were used to categorize the sick. To be fair, proper accounting for the coronavirus has been challenged by asymptomatic carriers and limited testing. But China’s official tally has remained muted, despite reports of new outbreaks in various parts of the country. Western analysts sense a systematic undercount, born of a desire to suppress information about the outbreak. This renders Chinese data useless for scientists trying to model the course of the pandemic, a critical tool for guiding public health policy.

As part of the quarantine efforts, China suspended production at many of the nation’s factories, extending the holiday period following the Lunar New Year. After a decline during the month of February, a key measure of economic activity (the Purchasing Managers Index, or PMI) rebounded quickly to its pre-COVID-19 level. Sudden recoveries from such depressed levels have never been seen in other countries; interestingly, the Chinese version is calculated by its government, whereas PMIs elsewhere are assembled by an international research firm.

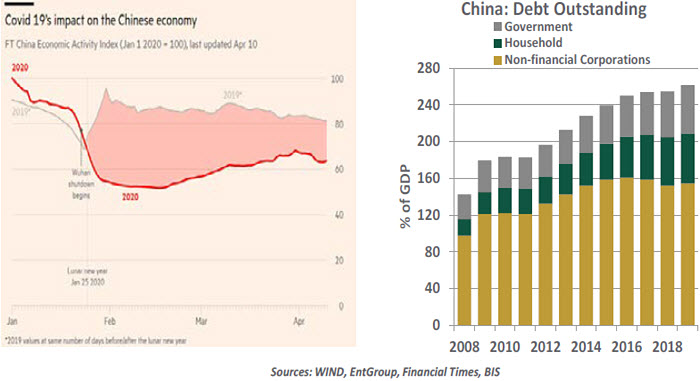

China did record a substantial drop in gross domestic product (GDP) during the first quarter. Chinese officials have asserted that a full recovery will soon be at hand. But measures covering traffic, power usage and other quantities illustrate a more gradual process of returning to work. Safety is certainly one reason, but another might be the deeply damaged demand for Chinese output. China’s consumers have been through a challenging interval, and with Western countries falling into a deep recession, export demand could be limited.

China’s government has implemented a broad range of supports to help the economy. China has passed out spending vouchers to many of its citizens and has enhanced the support available for the unemployed. (These steps are comparable to those taken in other countries.) It has also initiated new infrastructure programs. The People’s Bank of China has lowered rates and taken steps to promote additional lending in the economy.

A challenge for policy makers is that China has become a heavily indebted country over the past decade. The financial health of some Chinese firms has come under question; loan default rates are rising. Just three years ago, Chinese leaders announced their intent to slow the growth of credit to improve the health of the economy; now, they have been forced to go back to their old ways.

On a larger scale, loans China made to other countries under its Belt and Road Initiative are under stress; borrowers are asking for forbearance and relief. It isn’t easy being a creditor at a time like this, especially when the magnitudes are so large and the situations are so public. Out of suspicion of China’s motivations, a handful of countries have started limiting inbound Chinese investment. China’s desire to be seen as a helping hand to emerging economies is encountering obstacles.

“The coronavirus may result in lasting damage to China’s economy.”

China may also be facing longer-term economic consequences in the aftermath of COVID-19. Its two-year-old trade battle with the United States had already prompted companies to consider reorienting their supply chains to limit reliance on China. As firms and nations seek to reduce the risk of interruptions, recent events may only serve to accelerate that trend

The situation surrounding medical supplies adds an element of national economic security to the mix. China makes well over half of the world’s medical masks, and gave itself priority over export clients during the worst weeks of the outbreak. In response to an intense global demand for testing kits, China delivered products that were shown to be unreliable. China has had issues with quality control in the past, but the stakes are magnified when matters of health are involved.

It would be a remarkable and positive outcome if China has truly conquered the coronavirus. But the economic afflictions confronting China will not be cured so easily.

Nowhere To Go

Like most consumer spending, auto sales have fallen precipitously. While many U.S. state quarantine orders deemed car dealerships to be essential businesses (especially for repairs), those same quarantine orders are keeping people off the roads and limiting their interest and ability to go car shopping. This has had a profound impact at all levels of the industry.

Industry analysts at Cox Automotive expect U.S. automotive sales volume fell to 7.5 million annualized units in April, which would be a record low for sales data dating back to 1976. The slump would exceed the last monthly trough of 9.6 million seen in January 2009. Sales figures worldwide are following a trend similar to the U.S., with a massive drop in April and a hope for a return to business in May. Sluggish American auto retailers may consider themselves fortunate compared to their peers in India, some of whom likely witnessed a month of zero sales.

While dramatic, this is not unexpected. Sharp increases in unemployment around the world are curtailing purchases of many things; the bigger the ticket, the softer the demand. At dealerships, touching a car previously driven by strangers and negotiating payment face-to-face are of no appeal to consumers worried about contagion. As a result, dealer inventories are high.

Aside from supply accumulation and working through disruptions to supply chains, global manufacturers faced the challenge of stopping COVID-19’s spread among their workers. Most factories reacted by announcing temporary closures. The U.S. is seeking to restart its auto industry, but supply chains are interwoven with Canada and Mexico. Getting back online will require clearance from a range of public health officials.

While the auto sector appears to not need the broad support offered in 2008, several nations are supporting factory retooling to supplement production of medical equipment.

For now, many potential shoppers are repairing the vehicles they already have, instead of committing to a payment on a new car. As economic conditions improve and old cars deteriorate, shoppers will gradually return to dealer lots. We have seen bursts of sales in the years following recent slumps; manufacturers and dealers may face a poor year in 2020, but they will be poised for a recovery thereafter.

Vehicle demand has fallen not merely at dealerships, but also in our daily lives. As most workplaces are temporarily closed, the need to commute has dropped precipitously. Essential workers are still traveling to their jobs, perhaps finding some solace in light traffic and low fuel prices. However, most commuters are either working from home or sitting out layoffs. Shopping trips are minimized, and social events have been cancelled. While daydreaming about a new car may fill some of our endless days at home, a new car buyer would have nowhere to drive.

“Car buyers will return once their employment stabilizes.”

Ordinarily, families would be looking forward to summer getaways, often traveling by car. As of today, summer holidays for many families around the world remain uncertain. Tourists with itineraries including theme parks, sporting events or concerts are changing their plans. While historical sites, national and state parks, hotels and restaurants are starting to reopen, will consumers be ready to go back into social situations? And will those who have become unemployed, even temporarily, be able to afford any trips at all this year? There may be no peak in peak driving season this year.

As quarantines subside, auto demand may find some tailwinds. Airborne transmission of COVID-19 may make some commuters choose to drive instead of riding public transportation. A trend toward home offices could prompt more people to move to larger homes in residential areas that are more car-dependent. And low interest rates will continue to support vehicle affordability.

The automotive industry is cyclical, and there is no question the cycle has turned. Manufacturers, dealers and motorists eagerly await the day that they can get back in gear.

¡Abre El Bolso!

Worldwide government spending has taken off, to soften the blow from COVID-19. But one major emerging market is opting to buck the trend. In Mexico, the spread of the virus has led to a shutdown of most the economy. However, Mexican President Andrés Manuel Lopez Obrador has stayed with his preferred policies of austerity, refusing to increase spending to counteract the pandemic.

Mexico is experiencing severe economic damage. A large of number of workers (officially about 350,000) lost jobs between mid-March and early April as businesses struggled amid a slump in economic activity. Including the economy’s large informal sectors like street vendors and unregistered businesses, the job losses are likely much larger. And stress in the automotive sector, as discussed above, resonates in Mexico. The auto industry accounts for about a fifth of the country’s manufacturing, employs over 970,000 people and is key to the North American supply chain.

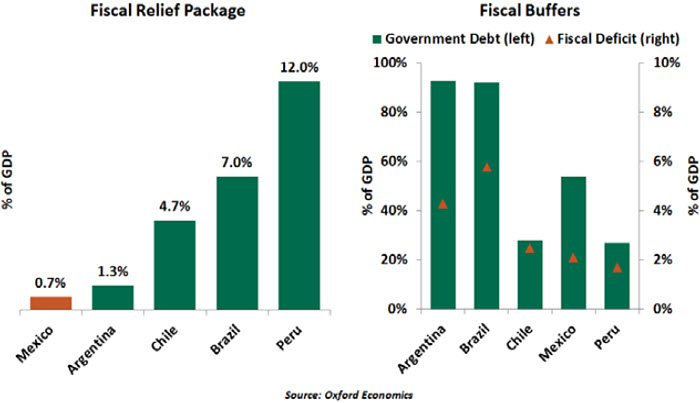

Despite this damage, Mexico’s policy responses have been the smallest in the region. Fiscal stimulus has amounted to just 0.7% of gross domestic product (GDP); this compares to Brazil’s 7% and Peru’s 12%. Banxico, the Mexican central bank, has offered only a modest 0.50% policy rate cut, despite ample room for more.

“Fiscal inaction will exacerbate the recession.”

The government has rejected calls for additional relief. Mexico’s history includes a debt crisis, a currency crash and a bank bailout; Lopez Obrador won election on a promise of fiscal discipline. He remains skeptical of credit programs and has avoided taking on debt for a major stimulus, despite the country having more fiscal space than its regional peers. Public sector austerity, along with tumbling oil prices, will create sizable economic losses. The Mexican peso has reached record lows, and credit rating agencies have downgraded Mexican debt.

Normally, investors welcome thoughtful policy debates and commitments to fiscal prudence, but these aren’t normal times. As Mexico faces serious health and economic emergencies, it must take steps to stabilize conditions. Trying to avoid the troubles of the past might lead to a mistake in the present.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust