Safety Net or Stimulus

Membership required

Membership is now required to use this feature. To learn more:

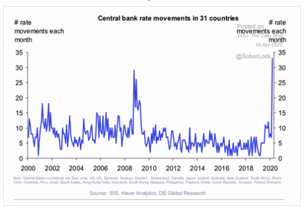

View Membership BenefitsIn response to the COVID-19 pandemic governments imposed shelter in place rules for their citizens and issued orders to close all but essential business in their country. The collective impact resulted in an unprecedented global plunge in economic activity that threatens the existence of many small and medium size businesses and a surge in joblessness in a matter of weeks as tens of millions of workers lost their job. In the U.S. more than 30 million workers have already filed for unemployment insurance and millions more are in the pipeline. In responding to this economic calamity central banks slashed interest rates at a faster pace than they did in battling the financial crisis in 2008, which is noteworthy since global policy interest rates were far lower in 2020 than in 2008.

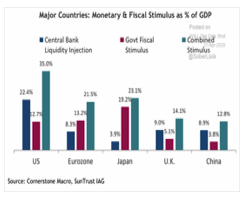

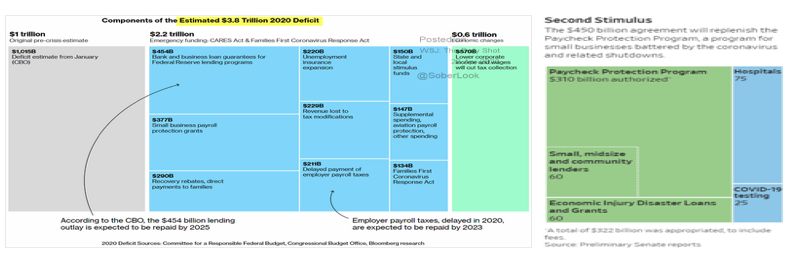

As financial markets became dysfunctional and illiquid, central banks also injected an enormous amount of the liquidity to stabilize financial markets so the health crisis didn’t become a financial crisis. The Federal Reserve has been the most aggressive central bank, while Japan has led the way with a large dose of fiscal stimulus. The U.S. has the largest combined response when monetary and fiscal spending is combined and this chart doesn’t include the U.S.’s second Payroll Protection Program of $450 billion.

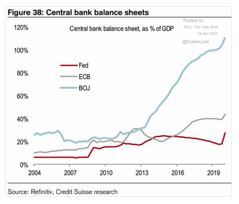

Since 2013 the Bank of Japan has left the ECB and the Fed in the rear view mirror as it has continued to buy Japanese government bonds, commercial paper, and Exchange Traded Funds (ETFs) including those owning stocks. The BOJ’s balance sheet is larger than 100% of Japan’s GDP while the ECB’s will approach 50%. If the Fed’s balance sheet reaches $10 trillion by the end of 2020 it will approach 40% of GDP. For many economists this development is a big surprise but something I expected. This is a quote from the June 2018 issue of Macro Tides and the February 2019 Macro Tides. “During the next recession, the Fed’s balance sheet could easily balloon to $10 trillion or more, as it attempts to prevent an outright deflationary debt collapse.”

The Federal Reserve began to normalize its balance sheet (think shrinking) in October 2017 through the end of August 2019. The Federal Reserve began to gradually expand its balance sheet from a low of $3.71 trillion on September 2, 2019. In the past 2 months the Federal Reserve has expanded its balance sheet from $4.17 trillion on February 17 to $6.57 trillion on April 20. To provide some prospective during the height of its third Quantitative Easing program the Fed was buying $120 billion of Treasury bonds a month. The Fed is now buying $70 billion a day!

The Federal Reserve has also made it possible for the Treasury to leverage the funds it has received from Congress by roughly 8 to 1, which is an extraordinary expansion in the Fed’s role of being the lender of last resort. This will allow the Treasury to extend more credit to small businesses through the Main Street Lending Program, Payroll Protection Program, and every other creative but necessary ‘Facility’ the Fed and Treasury Department needed to put a finger in the economic dyke.

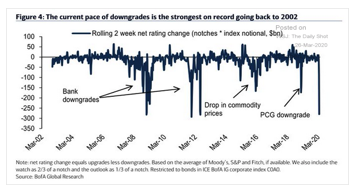

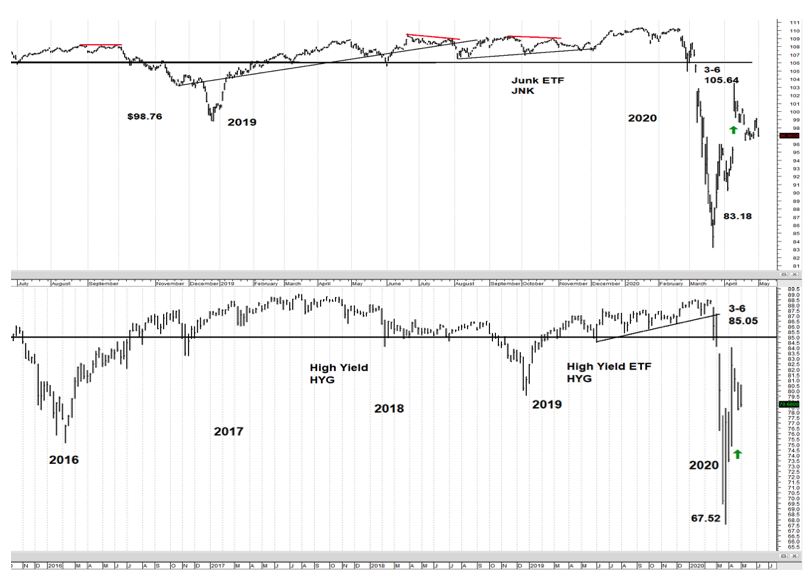

In the November 2019 Macro Tides I discussed how vulnerable corporate debt in the U.S. would be in the next recession. “In the U.S. corporate debt as a percent of GDP is at its highest level in history at 47%, and has generated a slew of articles expressing concern since a peak in corporate debt levels has preceded each of the last three recessions in the U.S. This is a legitimate concern that will be unmasked in the next recession.” The prime vulnerability within the corporate bond market is that an inordinate amount of debt was rated BBB just one level above junk. With 3 times as much debt rated BBB (the lowest rung of investment grade corporate debt) versus BB, any economic slowdown was likely to result in a surge in downgrades that would force some pension funds to sell. I covered this risk in the July 1, 2019 Weekly Technical Review. “During the next recession, a wave of downgrades to less than investment grade could prove problematic for the corporate bond market. Many pension funds have limits on how much high yield or junk bonds they can own. A wave of downgrades could trigger a wave of liquidations that could swamp investors who own the high yield ETF (HYG) or the junk bond ETF (JNK). A close below $106.00 would indicate trouble was coming. When JNK closed below $106 in November it quickly dropped to under $98.00. In the oil price collapse in 2016, JNK plunged to under $94.00 after it closed below $106.00.”

This is exactly what occurred in February and March when an avalanche of rating agency downgrades hammered the corporate bond market and especially BBB rated corporate bonds. The amount of downgrades in March was the most since 2002, even exceeding the spike in 2009. The monthly amount of downgrades during the financial crisis persisted and only time will tell if the total amount of downgrades during this crisis eventually exceeds the financial crisis. As the chart (below) shows the Junk bond ETF (JNK) plunged after it closed at $105.64 and below $106.00 on March 6.

In a March 23 You Tube video entitled ‘Debt Bomb - Corporate Bond Market’ I reviewed the charts showing the increase in downgrades and the plunge in the High Yield ETF (HYG), which had lost more than 20% in less than 3 weeks. My conclusion was that the Federal Reserve was going to step in and stabilize the corporate bond market as noted at the 3:05 mark in the video.

https://www.youtube.com/watch?v=y6Y4jvg_TIY&feature=youtu.be

On April 9 the Federal Reserve announced two more facilities to further stabilize the financial markets. The first rescue was directed at the corporate bond market, even though the Federal Reserve Act of 1913 precludes the purchase of corporate bonds by the Fed. The Fed circumvented the rule by not buying corporate bonds directly but through Exchange Traded Funds that own corporate bonds. The green arrows on the charts for JNK and HYG show the impact of the Fed’s intervention (above). You can also see how much these markets have sagged after the knee jerk reaction to the Fed’s announcement as investors reassess whether the Fed will be able to offset all of the bankruptcies and refunding troubles that are likely to emerge until the economy is back on its feet. Another factor could be the flood of corporate bond issuance that occurred after the Fed’s intervention allowed companies to roll over or float new debt to fortify their balance sheets. Delta Air Lines, Gap, and Carnival Cruise Lines were able to access the corporate bond market, which is something they would not have been able to do prior to the Fed’s intervention. The long term viability of Gap and Carnival Cruise Lines is debatable. The Fed’s Primary and Secondary Corporate Market Facility provided $750 billion of liquidity and has restored stability to the corporate bond market.

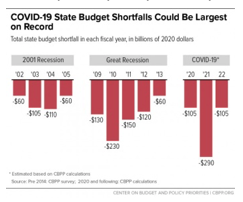

In its April 9 announcement the Federal Reserve also launched the Municipal Liquidity Facility to stabilize the municipal bond market which faces its own set of challenges in coming months. State budget shortfalls could exceed $500 billion this year, an amount that easily swamps the $283 billion in lost revenue that states experienced in the aftermath of the Great Recession. While the federal government can run deficits in the trillions of dollars, 48 states have laws or constitutional amendments requiring balanced budgets. States will be forced to issue municipal bonds to cover the budget shortfall, when the current fiscal year ends on June 30, and more bonds for their fiscal 2021 year. The Fed’s the Municipal Liquidity Facility will provide $500 billion to keep the municipal bond market functioning. Despite this life line state and local governments are going to be hard pressed to maintain the same level of services they were providing as recently as January 2020. If the recovery proves as labored as I expect, municipalities will be forced to cut back on services and lay off workers since tax receipts won’t be able to fund all the services municipalities provide communities. In the wake of the financial crisis states cut 170,000 jobs by 2013 and only added 38,000 jobs in the next five years. This proved one of the headwinds that caused the recovery from the financial crisis to be so lethargic despite extraordinary monetary and fiscal stimulus.

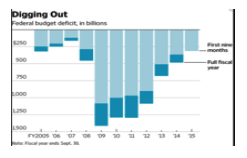

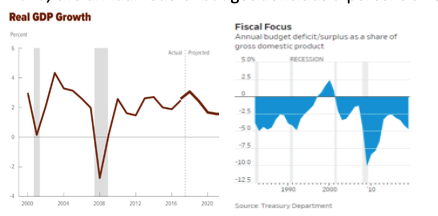

The Federal budget deficit is estimated to reach $3.8 trillion when the fiscal year ends on September 30, 2020, and could easily exceed $4.0 trillion since this chart doesn’t include the U.S.’s second Payroll Protection Program of $450 billion. Even before COVID-19 the deficit was projected to exceed $1 trillion.

The total amount of money Congress has authorized dwarfs the size as a percent of GDP of the TARP program in 2009 by a factor of 2.5 times. The other and just as important difference is the speed with which Congress has responded compared to the financial crisis in 2008. In some respects this is understandable since a Pandemic is much easier to identify than the financial crisis, which gathered steam over time before exploding into view after Lehman Brothers failed in September 2008. In 2007-2008 Congress didn’t take aggressive action until more than 420 days after the initial signs of trouble compared to 120 days after China reported the first death on January 11, 2020.

The first stage of the financial crisis actually began in August 2007 as I discussed on September 27, 2007, which I likened to a seismic event and explained why home prices might fall by more than 30%. “Throughout the Pacific Ocean there are sounding buoys to determine if a 100 foot tsunami traveling 500 miles per hour, or a 2 foot wading wave has developed after a large earthquake. The disruption that swept through credit markets worldwide in August was equivalent to an 8.4 magnitude earthquake. While seismologists know if a tsunami was created within a couple of hours, we won’t know for a number of months the full economic impact. But the displacements that took place leave no doubt that a significant seismic event occurred. In just seven days, T-bill yields plunged from 4.9% to 2.5%. In a month, the $2.2 trillion commercial paper market has contracted by more than 15%. Even as the ECB pushed well over $250 billion of liquidity into their banking system, the 90-day LIBOR rate jumped from 5.36% to 5.73%. In August, the issuance of junk bonds dropped by 93%, as the appetite for risk disappeared. This caused the spread between Treasury bonds and junk bonds to surge from 2.6% in June to 4.6% in less than six weeks.

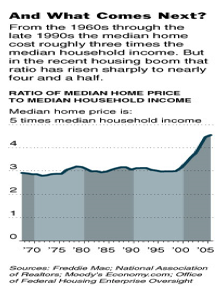

In August, the number of foreclosures surged 115% from last year, and increased a whopping 36% from July. With almost 2 million adjustable rate mortgages resetting in the next two years, the number of foreclosures will continue to soar. The imbalance between supply and demand in the housing market is likely to take far longer to stabilize than most people realize. Between 1968 and 2000, the ratio of the median home price to median household income fluctuated in a narrow range between 2.8 and 3.2. During this 32 year period, increases in home prices were supported by a rise in household income. This relationship provided underlying support for home prices, even when recessions developed in 1970, 1974, 1981, 1990 and 200l. However, between 2000 and 2006, the ratio rose from its long term average of 3 to 4.5.

This means median home prices have the potential to fall 33% should the ratio fall back to its long term average. In a recent analysis by Moody’s of home values, mortgage rates, tax rates and incomes going back to 1968, home values appeared 20% too high. Adding validity to this estimate, Federal Reserve Governor Frederic Mishkin recently estimated that housing prices could decline 20% in coming years. It is important to remember that these estimates are based on median home prices. In California and along the east coast, average home prices are two to three times the level of national median home prices. If national median home prices sink by 20% in coming years, home prices on both coasts could fall by 30% or more. The total value of housing in the U.S. is $20 trillion. A 20% drop in home values would slash $4 trillion from homeowners’ wealth, and maybe more if prices drop more on the coasts.”

The speed and size of the Facility Programs launched by the Federal Reserve and Congress in 2020 has led investors to believe that these programs represent a huge Stimulus. This has enabled the stock market to mount a strong rebound from the March 23 low. Since the majority of investors have been repeatedly told that markets are a discounting mechanism, they believe the stock market is confirming their PERCEPTION that the actions by the Fed and Congress will lead to a strong economic recovery in the second half of 2020. This seems like a bit of circular logic that will persist until it is contradicted by economic data that indicates it is too optimistic. This disappointment may be possible even if a second wave of infection is avoided. The reopening of the economy will progress slowly and be dependent on consumer’s willingness to go out and spend despite the risks. There is a good chance that many people will be more hesitant than investors currently expect, which will make the recovery in coming months slower and more labored.

The Federal Reserve and Congress have responded with speed and size for a good reason. The economy was on the cusp of a depression. In the first quarter GDP surprisingly fell -4.8%, even though the largest states didn’t issue stay at home orders until after mid March or when Q1 was more than 80% complete. (California March 19, New York March 22, Texas April 2, Florida April 3, and Illinois March 21.) The decline in Q1 was by far the largest drop since the fourth quarter of 2008 but will look small after GDP in the second quarter falls by more than -25% according to most estimates. The Congressional Budget Office estimated that Q1 GDP would fall by -3.5%, followed by a plunge of -39.6% in Q2, and a rebound of +23.5% in Q3 and +10.5% in the fourth quarter. For the year the CBO estimates that GDP will fall by -5.6% for the year as a whole, which would be more than twice as deep as the -2.5% contraction in 2008 due to the financial crisis. Investors have been willing to overlook the huge drop in GDP in the second quarter believing the response by the Fed and Congress will result in a strong second half. Investors who believe the stock market anticipates or discounts the future think the amazing rebound in the S&P 500 is telling them the recovery may take hold sooner and prove stronger. It is always interesting that the consensus is willing to have so much faith in the stock market, even though it failed to ‘tell’ them about the housing crisis in 2007 or COVID-19 in 2020.

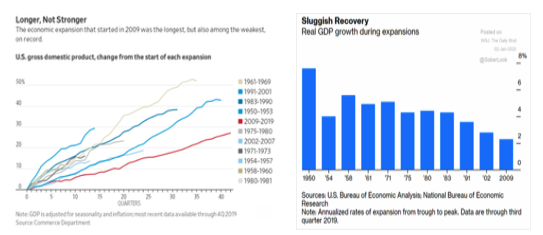

There are a myriad of reasons why the rebound won’t live up to expectations. Although the economic expansion after the 2008 financial crisis was the longest expansion in the history of the U.S., it was also the weakest since World War II in terms of average annual GDP. When average GDP growth is broken down by each expansion it becomes clear that each expansion since 1958 has experienced less annual GDP growth, especially during the last 3 recoveries. This trend suggests that there are some macro forces at work that increase the likelihood that the next recovery will be even weaker than the expansion after the financial crisis despite its record length.

The depth and shock of the contraction after the financial crisis led to unemployment soaring to 10.0% and a big increase in consumer savings which reduced consumption, as I discussed in the January 2009 Macro Tides. “With home prices not likely to rebound anytime in the next few years, many Americans are being smacked with a very unpleasant thought – “Oh, my gosh, we’re going to have to start saving!” What’s good for the soul is not necessarily good for the economy. For the first time since the Federal Reserve began tracking it in 1952, household debt fell in the third quarter of 2008. And, not surprisingly, the savings rate has started to climb. If the savings rate increases from 2% to near 8% over the next 3 years, annual GDP will be 1.25% weaker, than when we were a country of happy spendthrifts.” The Personal savings rate jumped from 3.1% in November 2007 to 8.8% in February 2019, which is another reason why the recovery after the financial crisis was weaker than prior expansions. State and local governments were forced to reduce services and employment and state spending. An increase in the personal savings rate (it was 13.0% in Q1 as personal consumption plunged), and reduced spending by state and local governments will also weigh on the coming recovery from the COVID-19 induced recession.

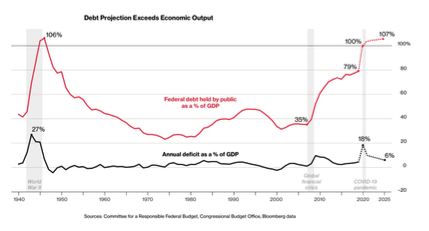

The expansion after the financial crisis was the weakest since World War II but it wasn’t for the lack of trying by policy makers. The Federal Reserve held short term interest rates at 0.12% for 7 years and pushed long term rates down as it increased its balance sheet from $900 billion in 2007 to $4.5 trillion in 2015 through its Quantitative Easing programs. Fiscal stimulus was huge in the wake of the financial crisis. The Federal government ran an annual deficit for four consecutive years of more than $1 trillion, which amounted to more than 6% of GDP compared to an average of 2.9% from 1969 to 2019. The amount of Federal Debt held by the Public (which excludes the debt in the Social Security program) soared from 35% in 2007 to 79% of GDP in 2019. Despite all the heavy lifting by the Fed and Congress the post financial crisis was weak.

All the jobs created in the past 10 years have been wiped out in less than 6 weeks. Coming into 2020 the unemployment rate was the lowest in 50 years and months later may exceed 24.9%, the peak in 1933 during the Depression. Consumer spending is 70% of GDP and the majority of consumers have been traumatized by how much their lives have changed, even if they didn’t lose their job. Just about every aspect of Americans daily life has been altered to some extent and the cause of this upending event is not going away anytime soon. The sobering realization that life as we knew it is not coming back for many months hasn’t completely sunk in for most people in the U.S. and around the world. The decline in the number of COVID-19 cases and deaths in the U.S. is good news, but shouldn’t be misconstrued with time running out in the fourth quarter and the home team holding a comfortable lead. Gilead Science’s drug Remdesivir is an incremental step forward but it is not a home run. The Phase 3 trial reduced the incidence of death from 11% to 8% and shortened the hospital stay of patients from 15 days to 11 days. Less time in the hospital lowers the burden on the health care system and any reduction in mortality is a much better outcome. In terms of facilitating a safer and quick reopening of the economy Remdesivir offers no benefit.

Recent polls show that a majority of Americans are more worried about reopening the economy too soon and will be reluctant to stop sheltering in place. A CBS News poll released on April 23 found that 63% of respondents were more worried about opening the economy too quickly compared to 37% wanting to open the economy. Anxiety about COVID-19 was apparent as 48% said they wouldn’t return to public places until the outbreak is over, with another 39% saying they might if they were more confident that virus was under control. When asked specifically about going out to a restaurant or bar, flying on an airplane, or going to a sporting event or concert, the vast majority were not comfortable. The views expressed were in spite of the financial hardship 36% were already experiencing and another 41% expecting the shutdown of the economy to negatively impact them in just a few weeks.

The majority of businesses don’t expect the demand for their goods or services to return quickly with 69.4% thinking it will take at least 6 to 9 months. If correct the majority of businesses won’t have a need to bring back all of their employees and they won’t. This suggests the unemployment rate will come down slowly after an initial fall and could still be above 12% by the end of 2020 and higher than the peak in 2010.

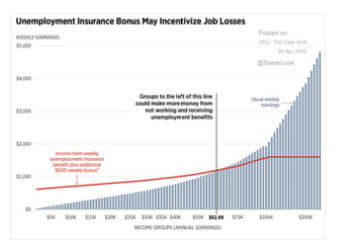

As businesses open up in coming weeks many will find some of their employees unwilling to return to work for two good reasons. Unless an employer is providing enough protection to prevent an employee from getting infected, employees will be reluctant to go back to work. The second reason is that many currently unemployed workers are making more money not working than they would if they returned to work. According to the National Employment Law Project states’ unemployment benefits replace about 45% of laid-off workers’ wages. In February median income for all workers was $66,538 ($33.27 an hour), so the median unemployment insurance payment would replace $29,942 or $575 a week. However, a more than half of unemployed workers earn far less than $33.27 an hour, which is why Congress tacked on the $600 a week bonus payment, so the average worker would have at least 100% of their prior weekly income replaced. The other reason is that the decades’ old technology many states use for their unemployment systems aren’t capable to calculate each workers lost wages and only make up the difference. Irrespective of the reason the $600 a week Congress authorized has the unintended consequence of being a disincentive to return to work, and some employees earning less than $15.00 an hour will milk the system unless those checks stop.

The Congressional Budget Office is nonpartisan and it has analyzed the impact of a national $15.00 minimum wage. In July 2019 the CBO reported that an increase in the minimum wage to $15 an hour by 2025 would increase the pay of at least 17 million people, but also put 1.3 million Americans out of work. The problem with a federal mandated minimum wage is that it ignores the wide disparity in the cost of living in different regions of the country. It is far more expensive to live in a major urban city than in rural cities. The Labor Department has data that calculates the cost of living throughout the country which would allow the minimum wage to be indexed. It may prove beneficial to have a minimum wage of $18.00 an hour in New York and $12.00 an hour in Biloxi Mississippi, so small businesses aren’t put out of business. Democrats have been pushing for a $15.00 an hour minimum wage and this crisis has provided the opportunity to get workers earning less than $15.00 an hour a taste of a better life.

As noted in the March 16 Weekly Technical Review and April Macro Tides many small businesses weren’t profitable even while the economy was doing well. “A 2019 report by the JPMorgan Chase Institute looked at 1.4 million small businesses and found 29% of the businesses in a typical community were unprofitable, and 47% had less than two weeks of cash liquidity.” Even with the infusion of cash from the Payroll Protection Program some small business owners are simply going to throw in the towel given the economic outlook for the remainder of 2020. If they were unable to be profitable before the recession, they know profitability will be nearly impossible if sales are 10% to 30% less in coming months after they reopen. I have no idea whether 5%, 10%, or more of small businesses never reopen, despite the availability of funding, but I’m certain that it won’t be zero percent.

The Federal Reserve has provided an unprecedented level of liquidity to stabilize every financial market and expanded its balance sheet in conjunction with a historical increase in spending by Congress. Investors have viewed these actions as being a huge economic stimulus, especially when compared to 2009 in response to the financial crisis. On the surface it is easy to come to this conclusion but common sense indicates that the current response resembles a safety net much more than actual stimulus. When the Federal Reserve was doing QE2 in 2011 and QE3 from the end of 2012 through October 2014, GDP growth was hovering above and below 2.0%. In an environment of 2% growth the Fed’s QE programs certainly constituted stimulus when applied on top of that growth.

Even as the GDP was growing around 2% after 2010, the annual federal budget deficit as a percent of GDP was the largest in history, other than during World War II. In effect the deficit as a percent of GDP was larger than the actual growth rate in GDP, and clearly represented a heavy dose of stimulus. The actions of the Federal Reserve and Congress in the past two months have provided a safety net that appears to have prevented another Depression. The removal of an extraordinarily negative outcome by injecting a safety net under the economy is not the same as the true stimulus provided after 2010. Once the health crisis is better contained in coming months, I expect Congress will pass another deficit expanding spending program that will represent stimulus with the Federal Reserve doing Whatever It Takes. Investors may come to realize that a safety net is not the same as stimulus, and the rally from the low on March 23 was predicated on a misperception. The best stimulus package possible is a vaccine.

Choosing Between the Lesser of Two Bad Options

Choosing Between the Lesser of Two Bad Options

The U.S. must weigh between two choices neither of which is positive, and thus we find the country between the proverbial rock and a hard place. The longer the economy is effectively shut down more economic damage will accrue, including the risk from the increase in long term debt (Debt projection chart pg.7), underfunding in programs like Medicare, Social Security, and public pension funds. As the U.S. economy is reopened in the next two months, the U.S. doesn’t have the testing capacity to perform widespread testing and the capacity to provide results within 24 hours. The value of more testing diminishes if it takes 2 or 3 days to get the results, since the delay allows the potential infected person to infect others. In order to prevent hot spots from developing, the U.S. must have the ability to perform timely and effective contact tracing, after an infected person has been identified. Some areas of the country may be able to do some contact tracing but many areas do not, although progress will be made in coming months. If the economy is opened up without the ability to perform widespread testing and effective contact tracing, the number of infections and deaths will rise. The choice between economic demise or more suffering is a no win situation.

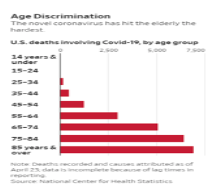

We MUST attempt to reopen the economy and we MUST do anything and everything necessary to limit the spread of infections, acting as if a vaccine won’t be available for at least 18 months. The dispersion of deaths from COVID-19 within age groups provides guidance. Clearly those under the age of 45 are far less vulnerable and should be allowed to go back to work. Workers older than 45 who are not diabetic, overweight, or suffer hypertension should also be allowed to go back to work if social distancing can be achieved in their work place. A study published in the Journal of the American Medical Association on April 22 analyzed the clinical outcomes of 5,700 patients hospitalized because of COVID-19 in the New York area. The median age of the 5,700 patients was 63 and with males representing 60.3% in the study. The study found that 94% of the patients had a chronic health problem, and 88% had two or more (comorbidity). The three most prevalent conditions were hypertension (56.6%), obesity (41.7%), severe obesity 19.0%, and diabetes (33.8%). According to the CDC 45% of adults in America have hypertension and only 24% of them have it under control. The National Center for Health Statistics reports that from 2000 through 2018 the incidence of severe obesity increased from 4.7% to 9.2%, and 42.4% of Americans were obese in 2018. According to the Diabetes Research Institute 10.5% of the U.S. population has diabetes. Those hospitalized in New York exceeded the national average in almost every category: hypertension 56.6% vs. 45%, obesity 41.7% vs. 42.4%, severe obesity 19.0% vs. 9.2%, diabetes 33.8% vs. 10.5%. These results suggests that workers who are even under of the age of 55, but have hypertension, overweight, severely overweight, or are diabetic would ideally work remotely or must abide by strict social distancing rules, since COVID-19 targets any health weakness no matter ones age.

Employers should be required to create a work space environment that makes Social Distancing easy, provide a surgical face mask, take employees temperature, and be able to perform testing if any employee exhibits symptoms. Conversely, those above age 65 who are diabetic, overweight, or suffer hypertension should avoid public spaces and be religious about social distancing and wearing a surgical face mask. Although wearing a face mask only lowers the spread of viral infections marginally, various studies have shown they have value. The medical grade N95 is far better than homemade masks made of cotton or cloth, but something is better than nothing. There will be no sporting events and large gatherings until a vaccine is widely available.

The outcome of reopening the economy will largely be dependent on how individuals behave and the one thing we can be certain of is this. Most people will do a good job but a few will do whatever they want. Hopefully, very few of those folks turn out to be super spreaders. A poll published by Gallop found that in the prior week the percent of people saying they wore a mask outdoors jumped from 38% to 62% which is encouraging. The table shows where the support is coming from.

However, the protests intended to pressure governors to open their state economy are not an encouraging sign. Most of the protestors aren’t wearing a mask or practicing social distancing since it is their constitutional right. It is their right it endanger their health, but since upwards of 30% of those infected with COVID-19 are asymptomatic their ‘choice’ also puts others at risk. The Constitution does not explicitly protect any individual’s right to put others at risk. The more important issue may be the additional divisiveness the reopening of the economy incites and the increased risk of violence. This issue will certainly increase the polarization within the U.S. and the US versus Them mentality between Americans that is already high.

Infections and deaths are going to increase after they hit a trough in the next few weeks, but an outbreak like New York is unlikely. Instead, COVID-19 is likely simmer at a lower level of infections, even as the number of deaths continues to climb at a much slower pace accompanied by spurts of random hot spots. This is the cost of reopening the economy versus keeping the economy shutdown, and there is no ‘right’ answer. This is a war and in every war there are casualties old and young alike.

Promise of a Vaccine

This started as a health crisis and won’t end until the health crisis is over. The first case of severe acute respiratory syndrome (SARS) was reported in 2002. SARS is a form of coronavirus and there is still no vaccine. Middle East respiratory syndrome (Mers) appeared in 2012 and is a different form of coronavirus and there is no vaccine yet. Allen Cheng, professor of infectious diseases epidemiology at Monash University in Australia, explains why it takes so long to develop a vaccine. “Making a vaccine isn’t a simple process – first there needs to be a ‘candidate’ vaccine, with an appropriate manufacturing quality. This is then tested in animals to see if it seems to work. Then there need to be tests in humans to see that it elicits an immune system response, and to define the dose, then it needs to be tested in proper trials to see if it actually protects against infection and doesn’t cause side effects. Then it needs to be approved by regulators, and manufactured at scale, purchased by governments and deployed. This would usually take 10 years at a minimum. Even if everything goes perfectly, I would expect this would at least take a few years.”

Despite this history there has never been so much money, technology, and global coordination so focused on developing therapies and eventually a vaccine to defeat COVID-19. If ever there was a time for history to be rewritten it is now. At a minimum there will be a solution or a group of partial solutions that will allow a return to normalcy but it will take time.

China

U.S. investors have been happy to embrace the narrative that says China was the first country into the COVID-19 shutdown and will point the way out, and the timing of when the U.S. can expect to recover. China is happy to appear superior in the way they handled COVID-19 and the fruits of their skills. No surprise then that the ‘official’ data for manufacturing and non-manufacturing shows that China is doing just fine and that the outbreak was merely a blip.

Unfortunately, other non ‘official’ data paint a less rosy picture. San Francisco-based SpaceKnow monitors and analyzes more than 5,000 industrial locations in China via satellite. As of April 20 its latest readings show activity slowed sharply amid efforts to contain the pandemic, and in many places stayed that way. For example, about 40% of the locations SpaceKnow tracks appear to have shut down. "The narrative is that China forced everyone to go back to work. The truth is they are not.”

The service sector within China has grown appreciably since 2003 and now represents 54% of GDP. After the SARS outbreak in 2003 and 2004 consumer confidence slumped and took a long time to recover. The COVID-19 outbreak exacted a much bigger toll on China’s economy and likely the psyche of the Chinese consumer. This is confirmed by the willingness of Chinese consumers to go out to restaurants and spend on luxuries, based on a recent survey by Morgan Stanley. China’s recovery suggests U.S. investors may be overly optimistic about the prospects for the U.S. economy based on ‘official’ Chinese data.

European Union

On April 29 the European Commission reported that its Economic Sentiment Indicator, a combined measure of business and consumer confidence, "crashed" to 67.0 from 94.2, the largest drop in a single month since the series began in 1985. Only once has sentiment been weaker, and that was in March 2009, when the scale of the economic damage caused by the global financial crisis was becoming clear. The European Central Bank (ECB) estimates the EU economy could shrink as much as 12% this year as a result of lockdowns to contain the coronavirus, and might fail to regain the previous level of GDP until the end of 2022. The ECB has responded aggressively and is expanding its balance sheet through its purchase of sovereign bonds and other financial assets, and has waived its self-imposed restriction on the amount of bonds it can buy from each member state in its Pandemic Emergency Purchase Program (PEPP).

The biggest challenge facing the EU is its inability to agree on offering a “European COVID-19 Investment Recovery Bond” that would provide monetary assistance to those countries hardest hit by the Pandemic without adding to any country’s debt to GDP ratio. This would help Italy which has been hit very hard by the pandemic and has a debt to GDP ratio of 135% more than double the European Commission’s rule of 60%. France’s debt to GDP ratio is just over 100%, which may be one reason it also supports the Recovery Bond concept. Based on electricity usage in France, Italy, and Spain, all three were operating at less than 80% of the level of activity in early March before the shutdowns were enacted. Germany and the Netherlands are opposed to the Recovery Bond since they believe it would open the door for European Bonds that would ultimately fall disproportionately on those countries that have been fiscally responsible. Germany’s debt to GDP ratio is 59.8% and the Netherlands is at 52.4%, comfortably below 60%, as mandated by the EU's Stability and Growth Pact. This issue has the potential to drive another wedge between the EU, Italy and France whose public support for the EU was waned. Since 2007 the percent of those who have a favorable opinion of the EU in Italy has fallen from 78% to 58% and to 51% from 62% in France. The viability of the EU could be called into question in coming years, if things continue to deteriorate and Italy or France threaten to exit, which would undermine the Euro currency. Should the Euro experience a large decline due to a divorce by Italy from the EU, the Dollar would strengthen noticeably since the Euro comprises 57.6% of the Dollar Index.

Jim Welsh

@JimWelshMacro

Related links:

file:///C:/Users/Owner/Downloads/jama_richardson_2020_oi_200043.pdf

https://jamanetwork.com/journals/jama/fullarticle/2765184

https://www.discovermagazine.com/health/why-wear-face-masks-in-public-heres-what-the-research-shows

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits