This month, we are watching economic data catch up to the difficult circumstances. We could see in our daily lives that the economy was approaching a standstill; now, we can begin to understand the extent of the economic impairment.

With smart behavior and some good fortune, we can put the worst of COVID-19 behind us. Many states are setting cautious paths to resuming economic activity. But the virus has not been defeated, and so a full return to normal activity will not happen until a vaccine or reliable course of treatment is proven. Until then, restrictions on movement will linger, precluding a “V-shaped” recovery.

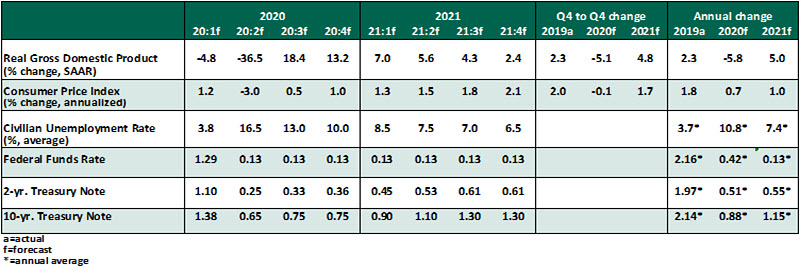

We expect the second quarter will see the worst outcomes. We are expecting successful return-to-work waves to restore a modicum of activity as we move through the summer, regaining a good measure of the lost ground. But progress will be slower from there. A second wave of infections is not our base case, but is the leading downside risk.

Influences on the Forecast

- Employment losses are beyond precedent. After seven weeks of initial jobless claims exceeding three million, the April unemployment rate of 14.7% was expected but still difficult to digest. The loss of six million workers from the labor force suggests this high reading is still an understatement of unemployment. Stimulus measures that supplement unemployment insurance and extend grants to businesses are important to help both workers and employers weather the storm. Hiring will resume as the worst of the virus passes, but at a more gradual pace than reductions occurred.

- The economy entered a contraction in the first quarter, with real gross domestic product (GDP) declining by 4.8% on an annualized basis. January and February were business as usual, but the beginning of the slowdown in March was sufficient to turn the whole quarter negative. On this basis, with April in lockdown and a cautious return to activity in May and June, we expect a massive output decline in the second quarter. Growth will resume at a decent clip in the third quarter, but from a low base. We don’t expect the U.S. economy to recover all of the output lost until well into 2022.