Lives and Livelihoods - May 2020

SUMMARY

- Lives and Livelihoods

After weeks in lockdown, many major economies are easing restrictions to reboot economic activity. Unfortunately, they are faced with a difficult tradeoff between lives and livelihoods. A slow reopening will limit a renewed viral outbreak, but will also prolong the stress on workers and firms.

The economic impact of COVID-19 has started to fully materialize, with major countries experiencing contractions in the first quarter. The second quarter is likely to be far worse. Economic activity is expected to recover in the second half of the year, but will be graded by four curves. Policymakers will continue to deploy additional support measures, but the room for further large scale stimulus is diminishing.

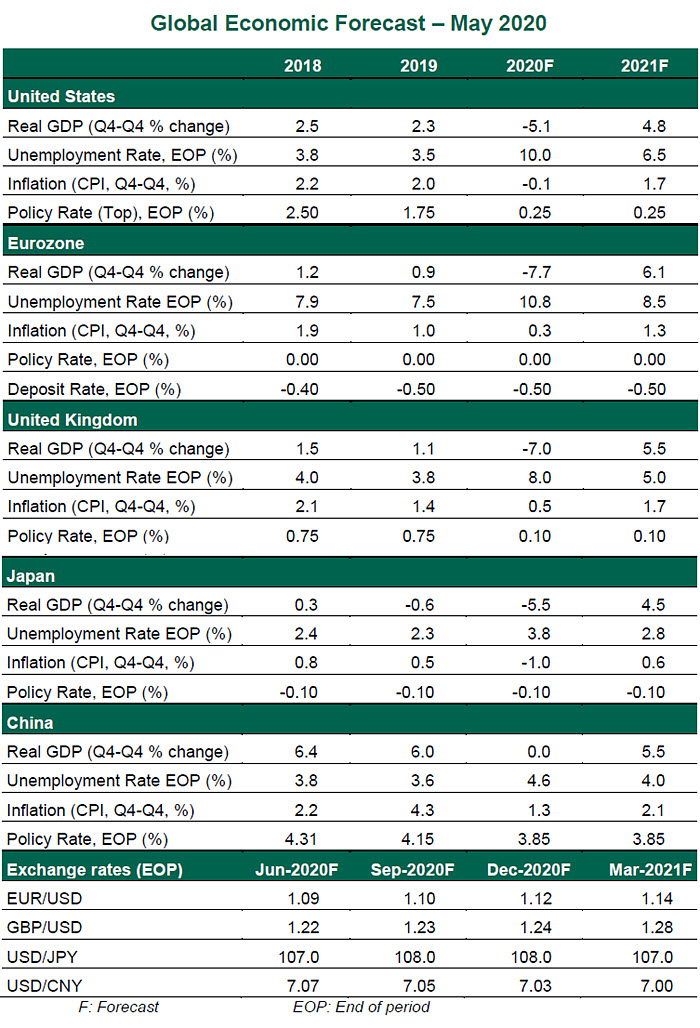

Following are our views on how major world economies will fare this year and next.

United States

- The “Great Lockdown” has hit the U.S. economy hard. Real gross domestic product (GDP) contracted by 4.8% on an annualized basis in the first quarter, as lockdowns took effect in March. The U.S. economy is likely to register a record contraction in the second quarter. Although we expect the recovery to begin in the third quarter, we don’t expect GDP to return to its late-2019 level until 2022. A second wave of virus spread is a major downside risk.

- Both the U.S. Federal Reserve and Congress have taken substantial steps to underpin the economy and the financial markets, but more fiscal and monetary measures may be needed. Fed Chair Powell reaffirmed his commitment to do “whatever it takes” to ensure a robust economic recovery and pledged to keep interest rates at their lower bound until that recovery has been achieved. The Fed has also underscored the need for additional spending and not just lending.

Eurozone

- Despite the announcement of a phased reopening across the eurozone, data releases have painted a gloomy picture of economic activity. First-quarter results varied by country, but all members of the common currency area suffered contractions and all are braced for a brutal second quarter. Unemployment is expected to peak at levels higher than those seen during the 2013 crisis. The economic situation in vulnerable countries, like Italy, is a major concern.

- The European Central Bank (ECB) continues to underpin the eurozone economy with a massive asset purchase program. Last month, it expanded banks’ access to ultra-cheap liquidity. A German court ruling threatens the ECB’s flexibility, but we expect the ECB to press ahead. Last week, the Pandemic Crisis Support program was approved. Germany and France have announced their backing for a €500 billion recovery fund to be disbursed in the form of grants, but this is only a small step forward considering the scope of the challenge the eurozone economy faces.