SUMMARY

- A Valedictory For This Year’s Graduates

- Europe Still Needs to Do More

- How The Other Half Lives

To the college class of 2020:

I was looking forward to seeing all of you and your families at the football stadium for commencement. I wrote this really inspiring speech, and I was anticipating multiple rounds of applause. I was going to encourage you to follow your dreams, get up one more time than you fall, and remember that you are part of a broader society that needs your engagement. And then: to the buffet!

Instead of that grand setting, I have been reduced to offering my remarks via video conference. Please remember to put your microphones on mute, press #6 to reach an operator, and enter the applause emoji in the comments box whenever you feel moved to do so. Afterwards, I invite all of you to go to your own refrigerators and help yourself to some snacks.

Graduates, it is terribly unfortunate that you are not able to enjoy the pomp and pageantry that normally attends such a significant achievement. You’ve all worked very hard to get to this point…well, with the exception of the last two months, when you were looking at Instagram photos instead of your online lectures. You have earned the right to rejoice: with friends at the campus bar (no need for fake ID anymore!) and in more formal settings with faculty and family. Unfortunately, COVID-19 has intervened.

The pandemic has not only interrupted your senior year celebrations, it has created one of the most challenging job markets in decades. I know some of you are still struggling to find employment; others have had offers deferred or rescinded. Those able to start work will likely be doing so from your parent’s homes, as factories and offices aren’t ready to receive you yet. Orientation will be… disorienting.

“The pandemic is producing some hard times for colleges and graduates.”

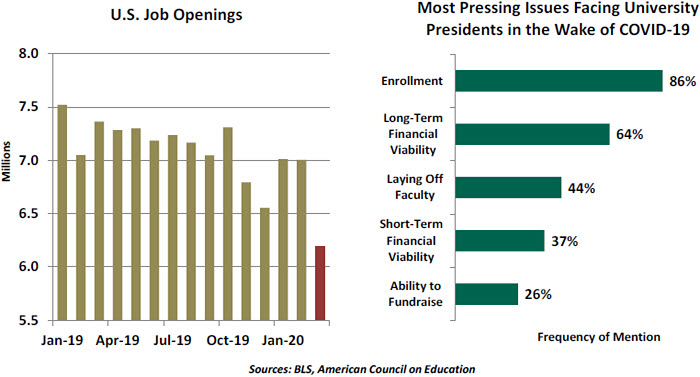

The colleges you are leaving are also dealing with a challenging new reality. Social distancing may make it difficult for students to return to campus in the fall; some schools have already announced remote learning will continue through the end of the calendar year. It’s not clear whether students will be willing to go as deeply into debt if they can’t interface with the faculty at close range.

Institutions of higher learning were already struggling with declining enrollment, the result of the demographic gap between millennials and the generation that followed them. Foreign students, who often pay full tuition, have been re-thinking their applications to U.S. universities amid rising international tensions. The coronavirus has led to extended border closings and may lead more talented foreigners to stay home.

And that’s not all. You know that meal plan you bought? The one that you rarely use because you frequently sleep until 2 p.m.? The university makes a lot of money on those. It makes a lot of money on the bookstore that you won’t be visiting and on the campus hotel where your parents won’t be staying because you’re not there. And then there’s the money that won’t be earned on football and basketball tickets. (Sorry, swimmers. We love you, but you don’t generate revenue.) Many universities have hospitals that profit from elective procedures, but not from emergency care. COVID-19 has put those on hold for the time being.

A number of private schools have endowments, which should help tide them over during difficult financial intervals. But endowments often include allocations to riskier assets that have underperformed recently. And donations typically dwindle during recessions.

Fortunately, the intellectual development that all of you have experienced should put you in a position to figure out this new environment, for yourselves and for the rest of us. Paradigm changes like this are unsettling, but often pave the way for inspiring change that uplifts our economy and our society. Through your ingenuity, the value of education will be on full display. And that should allow your alma maters to continue attracting young minds that want, one day, to be just like you.

Now, go out there and fix this recession! Rah, rah, sis-boom-bah! The webinar is now over—pass the guacamole.

A Union Divided

What is the European Union (EU)? It is an alliance of 27 member states that have decided to pool some of their sovereignty in limited areas. It is not a complete union, as it has no structure for fiscal oversight, making the region vulnerable to economic shocks. This time is no different.

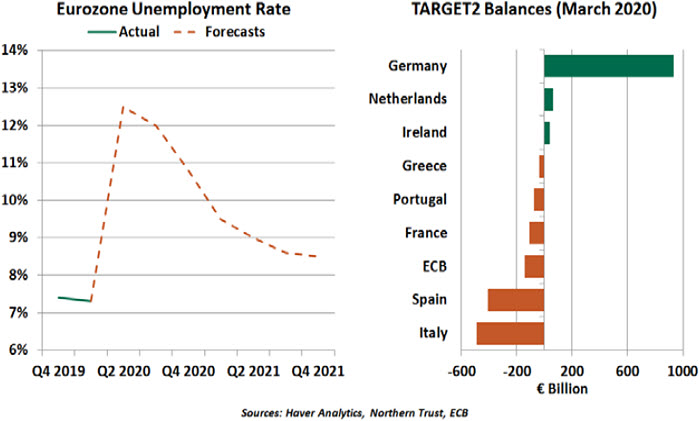

2020 is likely to be the worst on record in the economic history of modern Europe. The impact will be worst for those least capable to bear it. The European Commission (EC) expects both the Spanish and Italian economies to contract by over 9%, while German output is predicted to decline 6.5% this year.

Several European governments are making efforts to return to economic normalcy, relaxing curbs on public movement, schools and restaurants. But as we wrote recently, the recovery is going to be uneven. Many businesses won’t be able to operate at full capacity for months, implying a long period of elevated unemployment. Over 30 million workers have been furloughed in the four biggest EU member states.

Some countries look particularly ill-equipped to arrest the spreading malaise. For years, Greece was seen as the problem child of the European family. It will soon have company. Italy’s economy was already fragile, with unsustainable debt and low productivity. Its pain will now be compounded by the urgent need for fiscal measures to fight the COVID-19 shock. Concerns surrounding Italy’s solvency have driven up its borrowing costs, and are once again fueling speculation about the collapse of the euro.

“Italy is becoming Europe’s next problem child.”

Italy’s central bank also has a substantial deficit of about €500 billion with its eurozone counterparts through the TARGET2 payment system. Contagion may spread to Germany, as its balance of TARGET2 credits in the European Central Bank’s (ECB) payments system is rising towards €1 trillion. The German central bank, in the recent past, had issued a warning that it could witness heavy losses if a major member exits the eurozone and defaults on its debt to the ECB system.

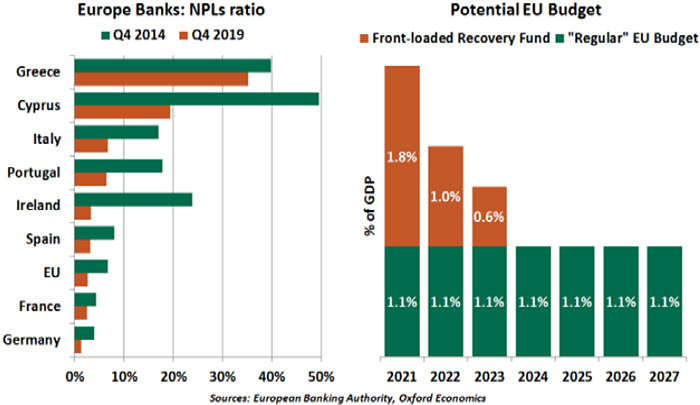

Europe’s banking sector faces renewed stress. More than half of all non-performing loans (NPLs) in the corporate sector were in construction, manufacturing, retail, accommodation and transport. These are the sectors that have been hit badly by measures taken to combat the pandemic and represent a key risk for a sizeable portion of the eurozone’s bank loan books.

Italy stands near the fragile end of the region’s banking spectrum. After an agonizing restructuring of balance sheets in the aftermath of past recessions, Italian banks are now bracing for a new wave of corporate defaults. The country’s NPL ratio is the third-highest in the region, after Greece and Cyprus. Recently, a major Italian bank set aside €900 million in loan loss provisions.

Brexit is not done. Westminster is stubbornly refusing to extend the Brexit timeline and negotiations between the EU and the U.K. have stalled again over various issues including fishing rights and business competition regulations. The odds of a “no trade deal” Brexit are rising, but that outcome would likely hurt Britain more than the EU.

The ECB is working hard to prevent a health crisis from becoming an economic one, but its actions are under legal scrutiny. Although a recent ruling by a German court threatens the ECB’s flexibility, it is likely to press ahead with its programs. The fiscal response has been uneven, owing to limited room for additional government spending in some countries and unresolved differences over the proper scope and size of a coordinated recovery package.

Under normal circumstances, the bloc’s rules put restrictions on how much support governments can offer to corporations; those limits have been loosened by the EC. Governments are providing aid in the form of guarantees and wage supplements to businesses at risk of bankruptcy, but the room for massive direct spending in several countries is quite low. The Italian government is doing whatever it can. The government has offered up to €740 billion in loan and investment guarantees to Italian businesses, but the rollout of the much-needed support has been slow given Italy’s stifling bureaucracy and the default risks the banks face. Only a fraction of the 300,000 firms seeking emergency benefits have received them.

“Europe needs much more stimulus if it is to avoid permanent economic damage.”

Germany and France announced their support this week for a €500 billion “recovery fund” to be financed by an issuance of joint debt. Fiscally conservative states like the Netherlands, Austria and some Nordic countries have yet to approve. The size of the proposed fund is modest: it represents a much lower fraction of GDP than the fiscal packages of other countries, and it is only one-third of the €1.5 trillion initially requested by countries like Italy and Spain. Even if approved, it will not be much immediate help. The fund will likely be part of the next EU multiannual budget in 2021 and could come with strings attached, like required economic reforms. More will be needed to protect the bloc’s workers and firms if there is to be a swift economic recovery.

Approval of the European Stability Mechanism’s Pandemic Crisis Support and progress on the recovery fund send a signal that Europe’s leaders are willing to work together in fighting this unprecedented crisis. That said, it is only a small step forward. The European project needs concrete foundations of a fiscal union (including financial risk-sharing), without which the bloc members will continue to face an existential crisis every time a catastrophe arrives at their doorsteps. If together they can reap economic benefits, it follows that they must sometimes share potential detriments. After all, a problem shared is a problem halved.

Well-Being Becomes Ill-Being

Last week, the U.S. Federal Reserve released its annual Report on the Economic Well-Being of U.S. Households. Most of the publication relies on a survey conducted in October 2019, and it’s fair to say circumstances have changed since then. We applaud the Fed for conducting a supplemental survey in the first week of April 2020 to gauge some of the initial effects of the COVID-19 crisis.

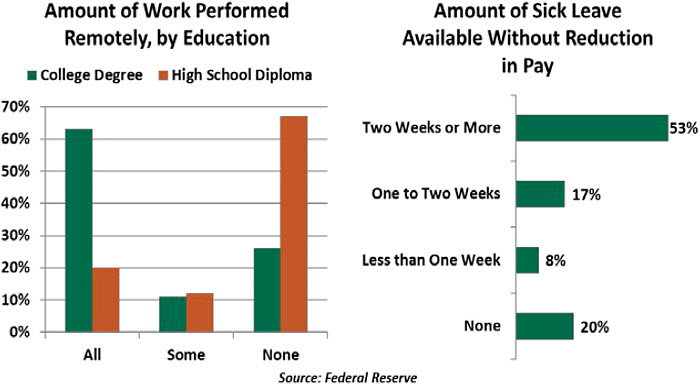

As feared, the survey shows that job losses were widespread, with 20% of panelists reporting a change from working to unemployed or furloughed from February to March. The worst effects were felt by the lowest earners, as 39% of people earning below $40,000 reported a job loss.

On the other end of the spectrum, better-educated workers have been more likely to keep working. Crucially, they often take roles that allow remote work. Seventy-four percent of workers with a bachelor’s degree or higher can perform some or all of their work from home, in contrast to only 32% of workers with a high school diploma. Income inequality will grow as higher earners keep earning and lower workers are left searching.

“Many households have a much worse financial outlook today than they did in 2019.”

Many of those who lost jobs remain optimistic. Nine out of 10 respondents who lost a job said their employer indicated that they would be re-hired, but most were given no specific timeline for returning. As the costs of job loss compound, from lost wages to skill atrophy, we hope these expectations are fulfilled. Sixty-four percent of those who reported a job loss or reduced hours expected to be able to pay all their bills in full in April; as the survey was taken before the enhanced unemployment and one-time payments of the CARES Act were implemented, an even higher share may remain solvent.

Those called back to work will face some health risks; unfortunately, 20% of workers reported no available paid sick leave. And some workers will have difficulty returning: 21% of those with reduced work hours reported that they did so voluntarily to care for children or family.

The economic picture of the crisis is becoming clearer. We can already see the worst effects are falling upon those least able to bear the burden of economic uncertainty. Future policy responses will need to aim at leveling the playing field.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

© Northern Trust

Read more commentaries by Northern Trust