After the shock of COVID-19, when will the global economy return to a sense of normalcy? Franklin Templeton Fixed Income CIO Sonal Desai examines some key economic activity indicators in the wake of the pandemic. She shares data on recent changes in US consumer behavior which seem to signal people are eager to go back to normal life.

What is foremost on my mind, and in my heart, is the pain that our country is suffering these days and the pain that our African American communities, colleagues and friends are experiencing and have been experiencing for too long. It’s a time for all of us to reflect deeply on the work we need to do to set our country on a better path, starting with everything that we can directly control, in our workplace and in our daily lives.

The economic crisis stemming from COVID-19, likely to be one of the worst of the past 100 years, has disproportionately hit the most vulnerable segments of society. It has exacerbated the inequality and economic difficulties that also underlie the latest protests and unrest. We are now entering a crucial potential turning point in the economic crisis. We still have over three weeks to go to the end of what will be one of the worst quarters in US economic history, and we will have to wait till the end of July to get the US Bureau of Economic Analysis’ (BEA) first estimate of the contraction. We currently expect it might be even worse than our previous estimate of a near-30% decline in gross domestic product in the second quarter (detailed in our US Macro Outlook, “Now Let’s Bend the Economic Growth Curve,” from April 2020).

However, parts of the US economy have started to reopen. Different states are moving at very different speeds: Georgia allowed hair salons, gyms, dine-in restaurants and theaters to reopen already at the end of April—with social distancing and other safety precautions. Texas took similar steps at the beginning of May. Other states like New York, New Jersey and parts of California are still mostly closed, following a much slower timetable.

Allowing businesses to reopen is a necessary but not sufficient condition for economic activity to come back to life. The crucial question all along has been whether consumers would feel comfortable coming back to restaurants, shopping malls and offices once the restrictions were loosened. This will determine how quickly (in some cases whether) businesses can claw their way back to profitability, and how quickly workers will be rehired. Any forecast of the economic recovery ahead relies on assumptions on whether and to what extent people’s behavior will change: Will we feel comfortable flying again in a fully booked airplane? Will we be willing to dine in a restaurant that is half full? Three-quarters full?

To get a sense of how the recovery is shaping up, Franklin Templeton Fixed Income has built a High-Frequency Activity Tracker, using data from Google Mobility and from Homebase. These data are beginning to yield a number of interesting insights:

-

People are shopping more—in person.

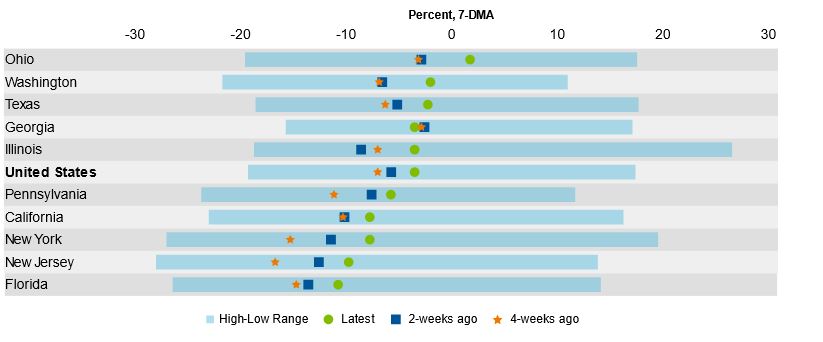

- The length of time people spend shopping at grocery stores and pharmacies has increased markedly over the past four weeks, and in states like Ohio, Washington, Texas, Georgia and Illinois it’s back to (or almost back to) normal. Even in states like Pennsylvania, New York and New Jersey, where it’s still about 10% below baseline, the improvement over the past four weeks has been substantial. (There has been some retracement in some states compared to two weeks ago, perhaps due to the recent wave of social unrest).

- Retail and recreation shows a much wider differentiation across states. In New York and New Jersey, it is still 40% below norm—an improvement from -50% levels seen four weeks ago, but still extremely weak. In Ohio, Texas and Georgia it is already back to about 10-15% below norm.

Google Mobility: Grocery and Pharmacy – length of stay relative to baseline (0 is baseline)

Google Mobility: Retail and Recreation – length of stay relative to baseline (0 is baseline)

Source: Franklin Templeton Fixed Income Research, Google Mobility. As of June 2, 2020. Baseline is taken as the median value from the five-week period from January 3–February 6, 2020. High-low range is for the period between March 15–latest data available.

-

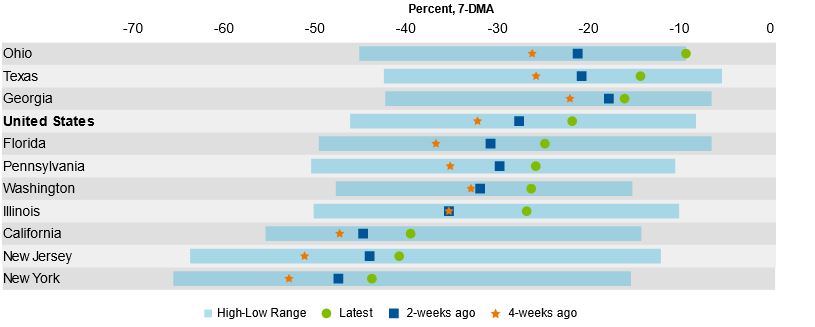

Transport is coming back to life. Use of transit systems has picked up substantially from the lows seen during the heights of the country-wide lockdowns, with states like Ohio, Texas and Georgia showing marked improvement. The retracement over the last two weeks (barring Texas and Florida) was likely due to the effect of the Memorial Day long weekend at the end of May and not necessarily COVID-related. New York and New Jersey, notwithstanding some improvement, are still over 50% below norm, and Washington, California and Florida are also lagging behind.

Google Mobility: Transit Stations – length of stay relative to baseline (0 is baseline)

Source: Franklin Templeton Fixed Income Research, Google Mobility. As of June 2, 2020. Baseline is taken as the median value from the five-week period from January 3–February 6, 2020. High-low range is for the period between March 15–latest data available.

-

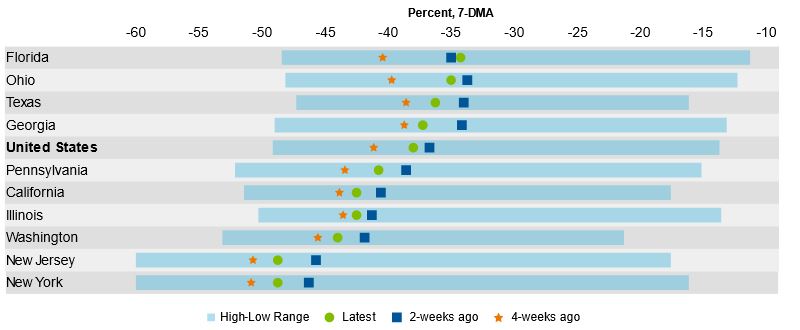

People are starting to go back to their workplaces. Here the improvement is more limited, and most states are still almost 35-45% below baseline, with New York and New Jersey still down over 45%. The United States as a whole is roughly 40% below baseline, a 10-point improvement from its lows. However, as with transit systems, the decline over the past two weeks was likely due to the long weekend at the end of May.

Google Mobility: Workplaces – length of stay relative to baseline (0 is baseline)

Source: Franklin Templeton Fixed Income Research, Google Mobility. As of June 2, 2020. Baseline is taken as the median value from the five-week period from January 3–February 6, 2020. High-Low range is for the period between March 15–latest data available.

-

Eating out is in again. Four weeks ago, most restaurants across the country were off-limits, with reservations on the OpenTable system down 100% from a year earlier. The bright spot was Texas, and even there, reservations were 85% lower than a year earlier. The latest data (as of June 1) show a much more encouraging picture: reservations are “only” 55-65% lower than a year ago in Oklahoma, Texas, Alabama, South Carolina, Arizona, Kansas, Indiana; 70-80% below in Kentucky, Utah, Colorado, Oregon, Tennessee, New Mexico; in Rhode Island they are only 10% lower; New York, the Washington DC area, Michigan and Illinois are still close to 100% down and California is 90% down.

Source: Franklin Templeton Fixed Income Research, OpenTable. As of June 1, 2020. Year-over-year percentage changes using seven-day moving average.

-

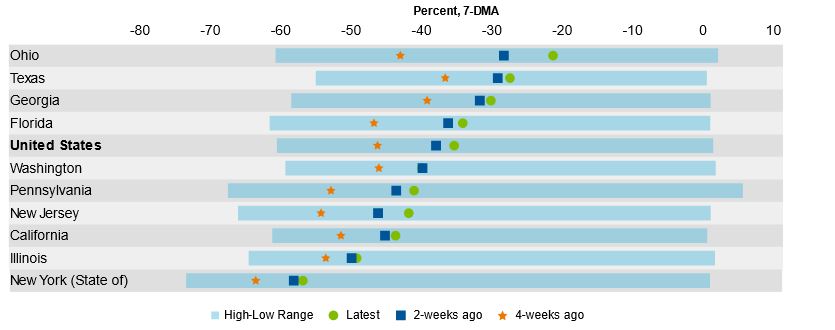

Hourly employees are beginning to benefit. Homebase data show that the employment of hourly workers has improved significantly in Florida and Ohio, and to some extent in Texas and Georgia. Less encouraging is that most states have seen little or no improvement over the past couple of weeks (with the exception of Ohio).

Google Mobility: Employment of hourly workers relative to baseline (0 is baseline)

Source: Franklin Templeton Fixed Income Research, Homebase. As of May 29, 2020. Baseline is taken as the median value from the four-week period from January 4–January 31, 2020. High-low range is for the period between March 15–latest available data.

Overall, I see these data as encouraging. We cannot assume they are the beginning of a new trend, of course. This will be an evolving picture; a lot will depend on whether the trend in infections continues to abate, or if we see a resurgence; it will depend on the restrictions that states will impose on different business activities and the pace at which these restrictions will be relaxed. All these factors will impact the logistics of business directly, but will also contribute to shaping people’s attitudes and behaviors. We will need to monitor the situation closely, leveraging a wider range of data.

For now, however, these data seem to signal that people are eager to go back to a normal life. They want the right safeguards in place, but if they feel that reasonable precautions are being implemented, they will not continue to hunker down in fear. This could help the recovery pick up some much-needed momentum during the summer and early fall, before a feared resurgence of contagion in October-November. In the meanwhile, policymakers will have some breathing room to compare the results of different strategies across US states and across countries and determine whether a possible renewed rise in infections can and should be countered with more targeted measures.

The encouraging message in the data so far is that if you open it, they will come.

If we have the courage and strength to address the fundamental causes of the current unrest, the healing process that will follow can still be accompanied and supported by a healthy recovery in economic activity and living standards.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments