As emerging markets cope with the COVID-19 epidemic, Franklin Templeton’s Emerging Markets Equity team considers three new realities they see in the emerging markets today. This second post in a three-part series examines how emerging markets have diversified their economies.

In our first post in this series, we explored how emerging markets have learned from past crises to strengthen their economies and become more resilient. Part of this resilience comes from a shift in the growth drivers for many countries, which have diversified into services, technology and domestic consumption.

New Reality #2: Emerging market economies have diversified, with consumption and technology providing secular growth drivers.

Compared with 30 years ago, emerging market economies are quite different.

While some emerging economies certainly have challenged fundamentals that perhaps skew overall perceptions during crisis periods, we believe fundamentals in emerging markets remain in good shape as a whole.

Emerging economies have been through a transformation. While many investors once considered emerging markets as tied to commodity ups and downs, the asset class has become much more diversified. Today, rising domestic consumption and technology are greater drivers of economic growth for many emerging countries than commodity exports.

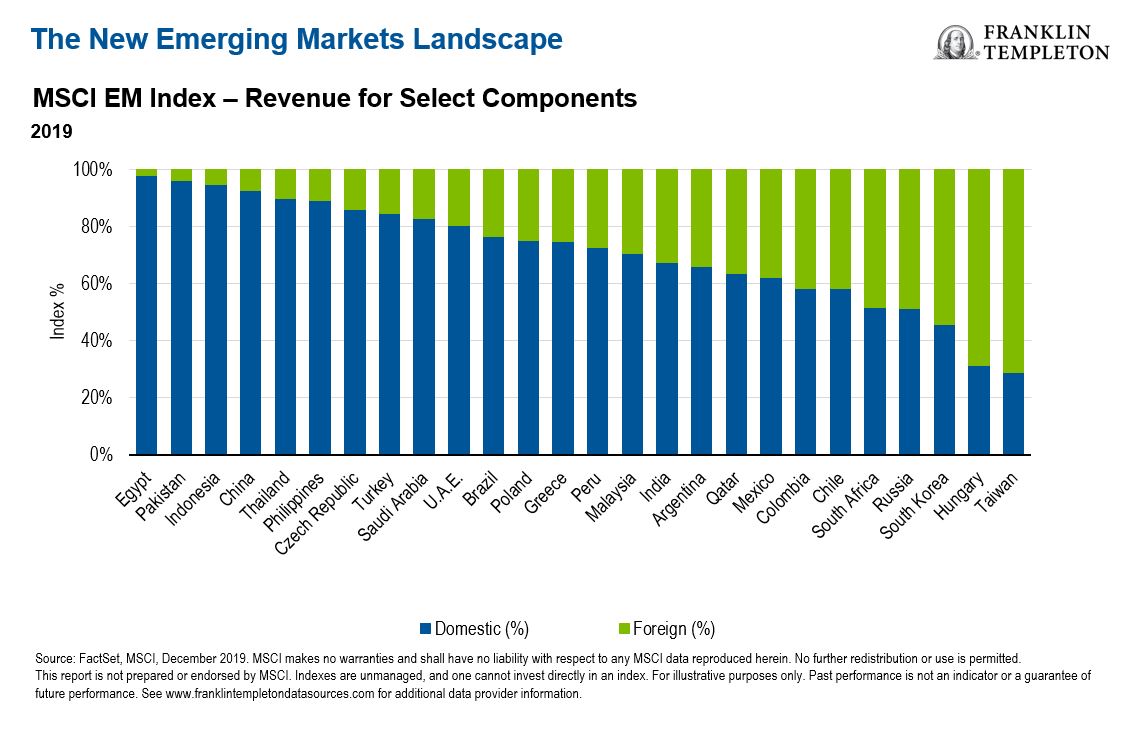

Economic Diversification

In the past, emerging market economies were broadly reliant on cheap exports of natural resources to developed markets. Today they benefit from both internal and external growth drivers.

Many emerging markets are primarily domestically driven, including large economies such as China and Brazil. A significant portion of exports are also intra-emerging market trades, versus exporting to developed markets.

The Single Commodity Focus Has Shifted to the Emerging Market Consumer

The emerging market story has shifted from a commodity play to one centered around domestic growth drivers and consumption. For example, China has been re-balancing its economy; domestic consumption is now the key driver of economic growth, representing 76% of gross domestic product in 2018, up from 44% a decade ago.1

Consumption has played a significant role in propelling emerging economies. We see a trend of penetration, the increased consumption of goods and services, as well as premiumization, which represents the rising demand for higher-quality goods and services amid a growing middle class. While COVID-19 could dampen discretionary spending in the short term, the secular factors such as favorable demographics, rising income and urbanization remain very much intact.

In our view, emerging economies could also eventually come out of the current crisis stronger as new technologies are adopted during the crisis and remain vital after.

In times of crisis, businesses tend to adapt accordingly, and embrace technology much more quickly. This is what we have witnessed in recent months, with many businesses moving from offline to online. Education is a good example of that; schools have embraced the use of online technologies to provide a learning platform for students. E-commerce, internet and software companies are also benefiting from an increase in online activities. Acceleration in internet usage and penetration will continue driving growth in cloud and other network architecture, increasing demand for servers and other memory intensive devices.

Franklin Templeton Emerging Markets Equity, May 12, 2020.

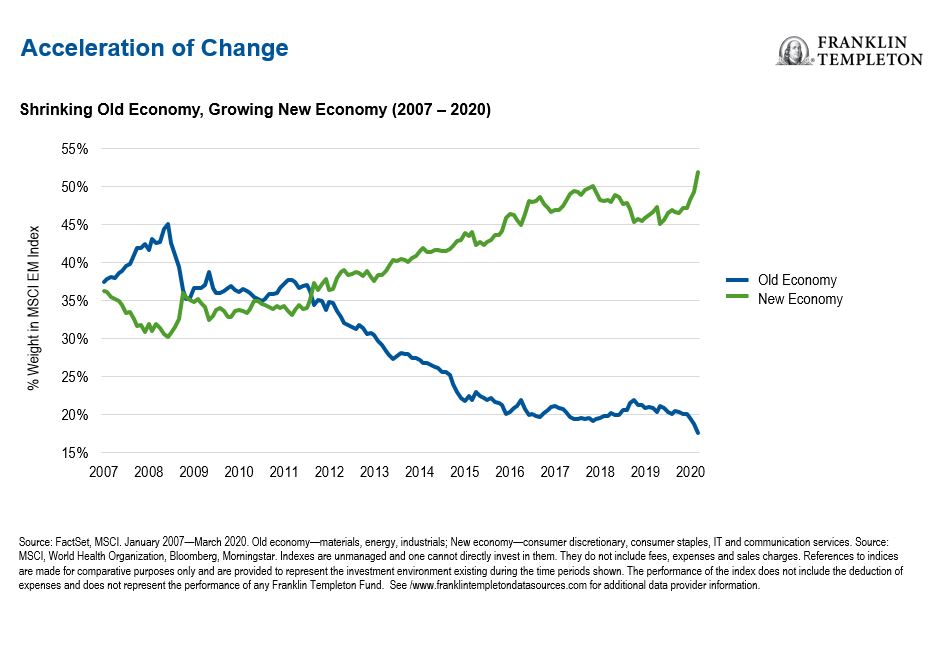

The chart below illustrates how “new economy” stocks—which include consumer staples, discretionary, information technology and communications—have a greater percentage weighting within the MSCI Emerging Markets Index than “old economy” stocks—which include industrials, materials and energy.

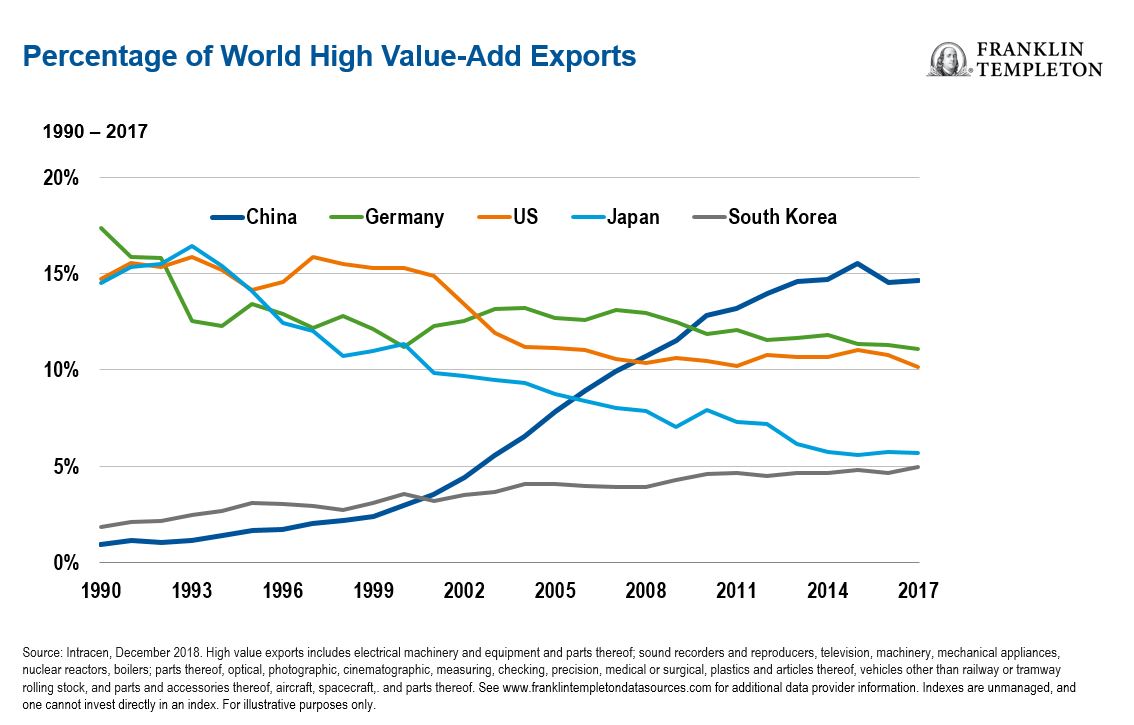

Moving Up the Value Chain

The continued technological development we see is an additional domestic-growth driver, and indeed a global growth driver. We’ve seen evidence of the emerging-market share of global high value-add exports has risen dramatically since the start of the 21st century, with China and South Korea as leading examples.

Emerging markets, which initially found economic success in producing low-value goods, have now set their sights further up the value chain. Many emerging markets today are established players and integral to global supply chains, given competitive labor costs and continued investments in research and development. Samsung Electronics, which evolved into the world’s largest memory chip maker, is just one example.

In our view, the coronavirus pandemic will likely change the way businesses consider supply chain logistics going forward. We think emerging economies could benefit from greater supply chain diversification.

A lot of consumers and corporates will have to ask themselves to what greater degree will they be willing to pay a premium for security of supply of key goods. And, that means companies will be looking to diversify their supply chains, not just looking at where it’s the cheapest, where they can ensure security of supply.

Manraj Sekhon, Franklin Templeton Emerging Markets Equity, April 23, 2020.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity.

1. National Bureau of Statistics China, August 2019.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments