Dislocations resulting from the pandemic shine a light on environmental, social and governance (ESG) issues, which can be used as an additional tool to identify leading companies from the laggards, according to Franklin Templeton’s Global Head of ESG, Julie Moret. She explains why she believes the pandemic has propelled “S” issues to the forefront, and how this environment could cultivate a fertile backdrop for active management.

We’re still in the early stages of understanding the longer-term impact the COVID-19 pandemic will have on the real economy. That said, the immediate impact on people’s lives and the dislocation of markets is evident.

While the crisis has no doubt emphasized how critical balance sheet resilience is now for companies and their longer-term viability, it has also accelerated a number of environmental, social and governance (ESG) themes which existed before the crisis. Many investors and executives argue that now is the time to “build back better” and create a more sustainable corporate world.

Against this backdrop, we see three near-term implications for investors which we believe will be sustained over the longer term.

Wider Stakeholder-Oriented Models and Focus on Stewardship—A Luxury or Necessity?

The crisis has both intensified and highlighted a range of societal issues, such as growing inequality and the fragility of customers and employees, especially in certain segments of the economy which have been left with little protection. It has also underscored the interconnectedness of people, the planet and profit.

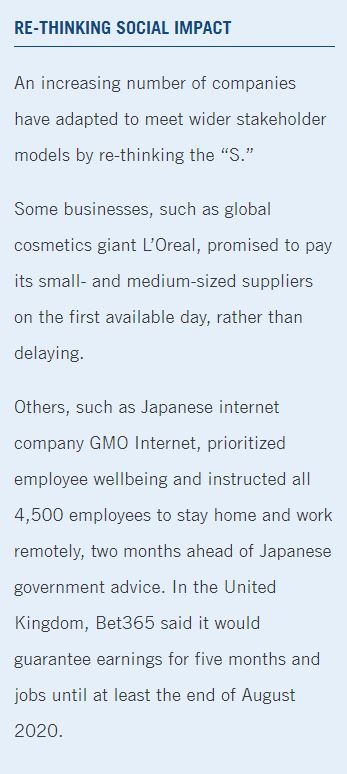

These drivers will increasingly require us to reframe what a well-managed business looks like. It reflects the increased pressure all companies face to manage a wider group of stakeholders beyond just shareholders. What we’re advocating are the ingredients that go into capturing quality and incorporate wider attributes. The crisis shines a light on the growing relevancy to corporates of wider stakeholder-oriented models, which provide equitable returns not just to shareholders but to employees, customers and suppliers, as well as the effective management of environmental externalities. All these considerations ultimately earn a company’s social license.

This infers a focus on stewardship and active engagement by investors. As investors, we are responsible stewards of our clients’ capital, which is to say we look after the assets our clients have entrusted us, with a view of returning them in a better condition than which we acquired them in the first place. ESG information provides an assessment on how companies are managing these issues. As such, it becomes a tool not only to further differentiate between well-run businesses versus the laggards, but also identify companies that are making a positive societal impact.

We’ve been advocating this for quite some time—companies need to consider wider stakeholder models in a changing world. We are mindful that businesses today are facing significant cost pressures in regard to allocating capital towards the welfare of staff, customers and suppliers.

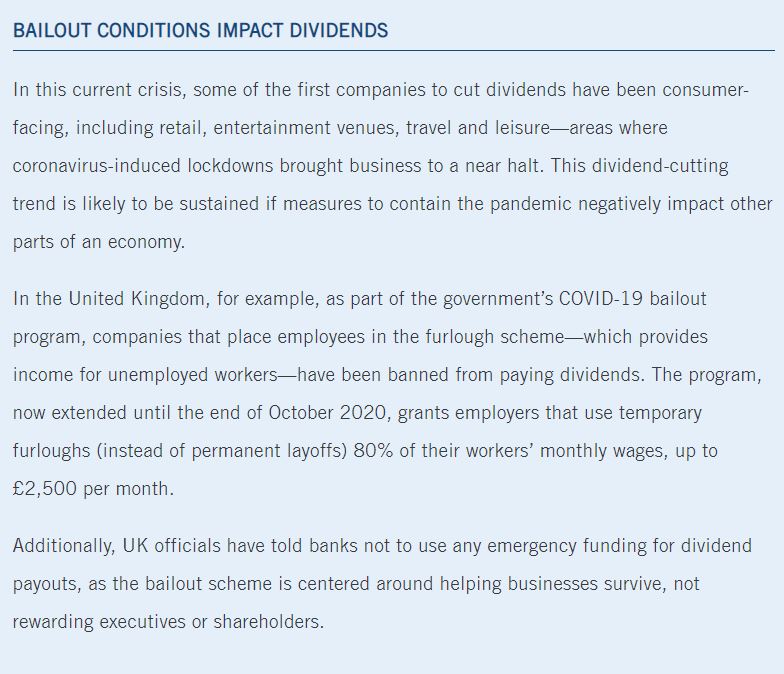

The conversations we’ve had with companies during this uncertain period have revolved around the strength of balance sheets, cash flow sufficiency and liquidity—all of which we use to assess whether a business can continue to operate over the long term. Our messaging has focused on exercising prudence and caution with a view that management should review the appropriateness of dividend and buyback programs, examining whether these policies could weaken the operational viability of the business in the face of the near-term pressures we outline above.

Human Capital Matters

The coronavirus pandemic has put human capital under the spotlight—issues such as employee contracts and rights have come to the forefront as investors and civil society scrutinize how businesses act during the crisis, including the way they treat their workers.

The crisis has exposed the fragility of independent contractors within the gig economy and those on zero-hour contracts in sectors heavily affected by the crisis, such as entertainment and leisure. Many of these workers have been left with little protection, both financial and health-wise. Post COVID-19, it is reasonable to expect sustained pressure on companies to improve labor rights and pay, which represents higher costs for companies and implies the levels of free cash flow distribution back to shareholders are unlikely to revert back to pre-COVID-19 levels, at least in the near term.

Corporate culture has also reached a turning point. We sense a shift in perception where virtual meetings and flexible working hours become more acceptable as business leaders consider how to create an environment conducive to employee needs. We’ve observed creative solutions some companies have made during the current crisis, including use of new technologies, including telecommunications.

“S” Won’t Eclipse the “E”

Sustained growth in client demand for environmentally focused capabilities, along with political and regulatory momentum in a number of countries, will likely ensure environmental matters aren’t eclipsed by the near-team focus on the societal issues.

In fact, a study we sponsored earlier this year revealed that environmental issues remain top of mind for investors.1 When asked to rank ESG factors, nearly half of the respondents in the survey (46%) said they believe environmental factors are the most important, with just 34% citing governance, and the remaining 20% for social issues.

The growing relevancy of environmental issues linked to climate change, natural resource scarcity and efficiency is undoubtedly driving greater interest in ESG products and solutions. Regulatory pressures are also accelerating these themes. Encouragingly, the study’s findings show that advisers are responding to the increased demand for ESG-focused strategies from clients, which should help deepen the industry’s knowledge and innovation in this space.

The crisis has underscored our conviction that companies which take environmental and social issues into consideration, and have good standards of corporate governance, will likely be more resilient businesses and better at navigating periods of shocks. We remain convinced that the time invested in understanding and integrating ESG issues into the investment process, in addition to our corporate engagement, makes us better-informed investors.

This information is intended for US residents only.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date (or specific date in some cases) and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments