For most US governors, June typically brings political fireworks when state legislatures hammer out final budgets for the next fiscal year. Our municipal bond team provides an overview of its recent COVID-19 credit research, explaining why some states face mounting credit pressures from high fixed costs and shallow emergency reserves, whereas other states with more diversified economies and strong financial management should fare better post COVID-19.

View the full paper. An excerpt follows.

In the wake of the COVID-19 pandemic, US governors have grabbed the media spotlight. After issuing lockdown procedures and more recently guidelines on re-opening businesses, public awareness of the role governors play in state economies has risen sharply. Evaluating the willingness of governors to make tough financial decisions is a key factor in our municipal bond team’s credit research, which gauges bond risks. Whereas some buyers of state-issued bonds might not blink if bond yields are tempting enough, our COVID-19 credit analysis helps ensure we are appropriately compensated for risks in states where governors may have chronically shortchanged budgets and degraded financial resiliency.

With regard to credit risks, it’s important to state upfront that despite the COVID-19 recession, states aren’t heading toward bankruptcy. Under current federal law, states can’t file for bankruptcy—granting authorization would require new legislation at the federal level. That said, we think mounting credit pressures could mean ratings reductions for some states if more federal funding doesn’t materialize from the US Congress this summer. Some states were ill-prepared to weather a normal cyclical downturn, let alone the dramatic economic shock of COVID-19.

A downgrade could increase borrowing costs for states already weighed down by pension liabilities and meager rainy-day reserves. To a degree, this year’s muni market performance already reflects the variability of credit pressures among states.

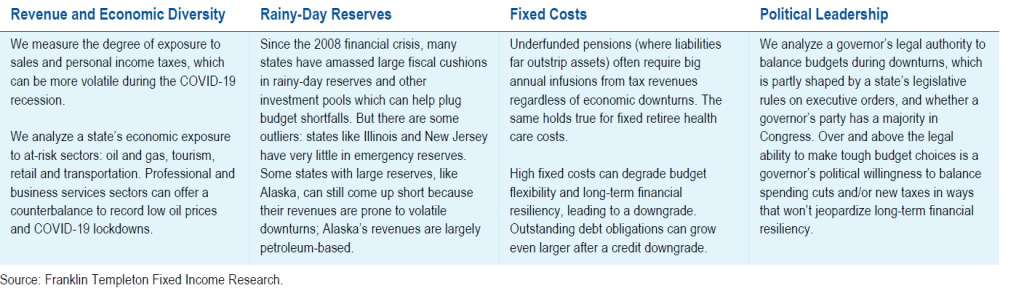

To gauge the credit pressures from COVID-19 (and record low oil prices) that are bearing down on state budgets, our team analyzes four key components that can impact a state’s financial and economic resiliency. Our research combines quantitative metrics—for example, the diversity of tax revenues, exposure to at-risk sectors like tourism and the size of “rainy day” reserves—and qualitative measures that consider the strength of a governor’s ability to implement hard choices like spending cuts or new taxes.

Our COVID-19 credit analysis tells us states like New Jersey face relatively high credit pressures compared with states like North Carolina and Texas, which enjoy higher financial resiliency and

economic diversity. Even states like New York—which came into this crisis with far more financial resiliency than states like Illinois—now face tough budget choices. With tax receipts already down 12.4% and state unemployment over 11% and climbing, New York Governor Andrew Cuomo’s enacted budget proposes US$10.1 billion in budget cuts, largely to public schools and state Medicaid health care—two of the largest budget items in most states.1

It’s important to note here that fresh unemployment data and revised state budgets are ongoing and coming fast. State governors and legislative offices are busy analyzing new economic projections and releasing revised estimates of revenue shortfalls. The credit views presented here are as of the published date and are subject to change, especially if more federal funding to states is approved this summer.

Revenue and Economic Diversity

As a whole, state governments rely on personal income and sales taxes for most of their tax revenues (with some notable exceptions). With US unemployment now at 14.7%—the highest since the 1930s Great Depression—and most retail shops and restaurants still closed or slowly getting back to normal, tax revenues have slumped dramatically and blown a hole through state budgets. Case in point: California Governor Gavin Newsom released a COVID-19 budget analysis showing a US$54.3 billion

shortfall through the summer of 2021, rendering his recent January budget proposal inoperative. To fix this deficit, Newsom thinks everything needs to be on the table—spending cuts, higher taxes and a plea for more federal help.

Understanding the composition of a state’s tax revenues is a key component of our credit-pressure analysis. For starters, not all states rely as heavily on sales and personal income taxes as states like New York and California do. Texas and Nevada, for example, don’t have personal income taxes. That doesn’t mean, however, that they’re in the free and clear from the COVID-19 recession. Nevada’s outsized exposure to tourism and gambling in Las Vegas and Lake Tahoe has hit sales tax revenues relatively hard.

On the other hand, sales taxes in Texas have fared somewhat better given its more diverse economy and looser shelter-in-place restrictions compared to states like New York. Other states get by with fewer sales and income taxes by relying more on “severance” taxes that come from the extraction of natural resources like oil, gas, coal, timber and fish. But here too, this doesn’t immunize state budgets from shortfalls. Given record-low oil prices, Alaska’s petroleum-based revenues have dropped significantly this year. Despite its large backup reserves and less reliance on income and sales taxes compared to states like California, Alaska’s credit was downgraded in early May.

As Alaska illustrates, tax diversity is inextricably linked with a state’s overall economic diversity, which forms another component of our credit-pressure analysis. Because New York City and its boroughs have been the epicenter of US-based COVID-19 infections, New York State is projecting sharp declines in sales and income tax revenues due to shelter-in-place restrictions. That said, New York City is also an international hub for financial services companies and a growing cadre of information and technology firms. These businesses largely remain up and running with more employees working from home.

Technology and professional services sectors provide diversity in Texas, which some investors mistakenly view solely as an oil and gas economy. Metropolitan areas like Austin, San Antonio and Houston have seen strong growth outside the energy sector over the past two decades, offering welcome economic resiliency from a credit risk perspective.

Federal Help and Rainy-Day Reserves

Unlike the federal government, US governors can’t print money, and a majority are obliged to balance their budgets annually by state law. Without more federal funds over and above the recent CARES Act, US governors are now signaling major cuts to key services, including public K-12 schools and colleges as well as social safety nets like Medicaid. To help fill their COVID-19 budget gaps, the National Governors Association has called for another US$500 billion in federal funding relief, and a consortium of governors including California’s Newsom recently suggested US$1 trillion. We are monitoring these proposals as they work their way through the US Congress.

Some states, however, are better equipped to weather the COVID-19 downturn than others. Over the recent 10-year economic expansion, many governors steadily grew their rainy-day reserves. Designed for unexpected shocks, states can tap these reserves to soften the need for severe and sudden

spending cuts or tax hikes to balance budgets. A vital budget resource to offset volatile tax revenues, our team tracks rainy-day reserves quite closely, as do bond rating agencies. For example, last year after California increased its rainy-day reserves to the largest in that state’s history—US$16.5 billion—Fitch upgraded California’s rating, citing its improved ability to manage future downturns.2

It’s worth mentioning here that many states maintain reserves outside their rainy-day funds, which can also offset budget shortfalls and bolster liquidity. Pennsylvania, for example, traditionally dips into the state treasurer’s investment pool to manage liquidity issues. The state estimates it has about US$1.5

billion available and has been borrowing through this mechanism this year. For states like Illinois with minimal reserves (rainy-day or otherwise) Congress offers the Municipal Liquidity Facility that provides loans to manage cash flow issues stemming from income taxes being pushed back to July this year.

High Fixed Costs

On the back of 10 years of steady economic growth, there remains a wide gap between states like South Dakota and Wyoming, which maintain relatively well-funded public pensions, and states like Illinois, where pension liabilities have mushroomed to outstrip assets and drive up annual fixed costs. This dilemma stems from a legacy of poor policy choices. By not consistently setting aside money for pension contributions, states like New Jersey, Kentucky, Connecticut and Illinois are shackled with relatively high pension costs. Add to that the costs from existing debt obligations and retiree health care, and total fixed costs can hamstring a governor’s budget flexibility during downturns.

For states like Illinois and New Jersey with almost no budgetary cushions from rainy-day reserves, high fixed costs substantially increase the difficulty of balancing budgets, in our view.

Political Leadership

Although much of our credit research is quantitative, qualitative measures of a governor’s leadership ability also play a role. Examples of strong leadership have been on full display during the COVID-19 pandemic. By balancing the need for public safety through shelter-in-place orders with the long-term viability of their state economies, Ohio governor Mike DeWine and New York’s Andrew Cuomo have enjoyed sky-high approval ratings from their constituents. The cruel nature of this COVID-19 recession is that during a time when the public is looking to social safety nets, it’s also the time when state tax revenues are shrinking dramatically. Legally obligated to balance state budgets, governors recognize some spending cuts are necessary—though the scope is shaped by the size of reserves, fixed costs and a state’s economic exposure to hard-hit sectors like tourism.

Ultimately, as credit analysts we’re looking for smart budget compromises that don’t jeopardize a state’s credit quality. Budget gimmicks that simply kick the can, like short-changing long-term pension obligations to avoid politically sensitive cuts, degrade long-term financial flexibility. As we explain in our five state summaries below, some governors face extraordinary balancing acts with little room for maneuvering.

Upcoming Budget Battles

As we move into peak budget season—most states’ fiscal years (but not all) end June 30th—we think sparks could fly when the budget rubber hits the COVID-19 road during June negotiations. Given the shock of COVID-19 and prospects of more help from the US Congress, these budget skirmishes are already making national headlines this year.

Although we think further muni bond market volatility is likely this year, we also recognize that many states entered this pandemic with replenished rainy-day reserves, helping governors balance their budgets for 2020 and fiscal year 2021. That said, individual states with higher fixed costs, lower reserves, and more exposure to COVID-19 infections could face ratings downgrades. Indeed, those expected scenarios are already playing out in the muni bond market, where states with lower financial flexibility, like New Jersey and Illinois, are underperforming Texas and California. As always, our muni team will be sifting through prodigious levels of noise this budget season, with an eye towards steering clear of unnecessary risks that aren’t properly compensated.

1. Source: Williams, Z. “Cuomo warns of $8.2 billion in cuts to localities.” City and State NY. April 26, 2020.

2. Source: “Citing Decisions to Save For a Rainy Day, Major Credit Agency Upgrades California’s Credit Rating” California Budget Office press release. August 16, 2019.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments