Pricing dislocations and adjustments between companies, industries, regions and asset classes due to the impact of COVID-19 offer opportunities for select hedged strategies, according to K2 Advisors. Brooks Ritchey and Robert Christian provide the team’s third quarter hedge-fund strategy outlook.

Strategy Highlights

Long/Short Equity–Europe

We believe Europe will benefit from an inflow of foreign capital as investors start to feel more comfortable with the risks inherent to the region. In our opinion, the upside of European managers’ long books remains elevated as persistently overlooked companies gain more traction.

Long/Short Credit

Recent dispersion in high-yield bonds could provide managers with a better environment in which to pick specific credits on both the long and short sides.

Macro Discretionary

Market focus has started to shift to the prospect of fiscal expansion, particularly in Europe, which may create directional and relative value trading opportunities for discretionary managers.

Macro Themes We Are Discussing

COVID-19: Will there be a second wave pandemic, or will economies reopen successfully?

As economies reopen and the rate of COVID-19 case growth slows, the logical next question is “will there be a second wave of infections?” While impossible to predict, the recent social distancing efforts may well last until a safe vaccine is found and/or the virus is otherwise eradicated. Companies involved with cashless payments, online product and service offerings, in-home entertainment, and other non-contact services may recover from the recent economic lockdown more quickly than traditional retail business models.

Will the recent growth in telecommuting continue post-COVID-19?

The pandemic forced millions of workers to work from home (or worse, lose their job). In addition, the fear of infection while attending public events may persist well beyond governments’ relaxing of social distancing rules and guidance. Many economists and strategists believe this will lead to a long-lasting cultural shift that will have a positive impact on some areas of an economy while enhancing business and government stresses in other areas.

Examples of companies that should benefit include:

- Those offering hardware and software that enhances home-based technology infrastructure

- Home maintenance and renovation retailers

- Food and package delivery services

- Online retailers

Conversely, areas that may see ongoing demand destruction include:

- Airlines and mass transit

- Commercial real estate

- On-site entertainment facilities (theaters, restaurants, casinos, sports and concert arenas, etc.)

Companies and cultures able to maintain growth while reducing expenses may see their equity and fixed income investments outperform those still reliant on traditional on-premises work environments.

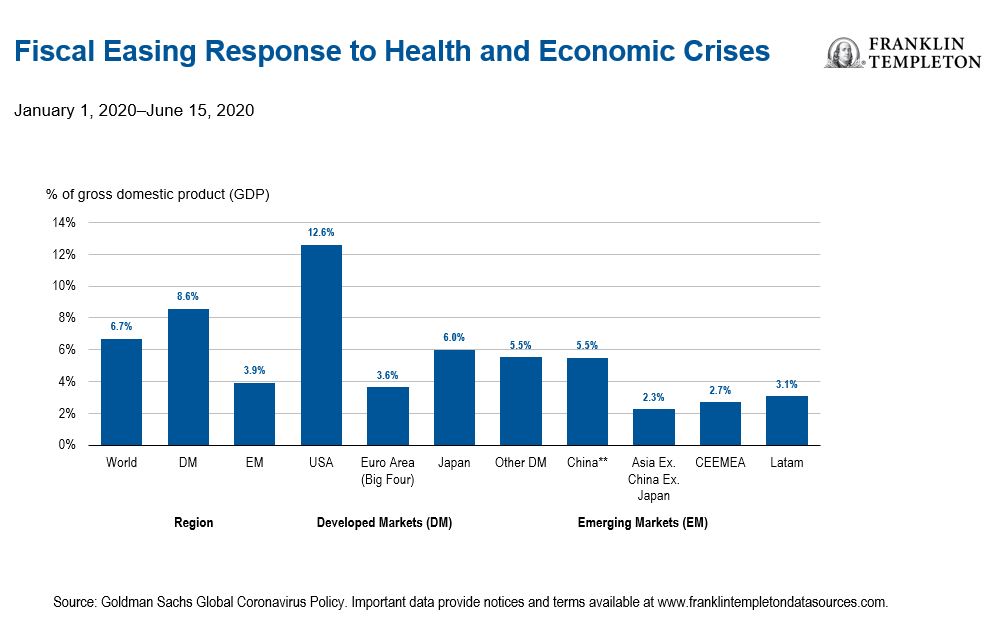

What market and economic impacts may arise due to the recent fiscal and monetary stimulus?

It is well-known that central banks around the world have offered much support through interest-rate cuts and quantitative easing. With many economies reopening, we have begun to see a stabilization in many growth indicators as the liquidity flows through the system. Should the health crisis continue to diminish alongside the return of consumer spending or the implementation of government infrastructure projects, there is a possibility that inflation comes in above the current low expectations.

Additionally, some of our managers are talking about the potential for the US dollar to weaken. This would be a potential tailwind for global commodity prices to move higher.

In this environment, one might expect the US yield curve to steepen, non-US equities to outperform domestic equities, and the dispersion of credit instrument returns to widen. We believe such a scenario would likely benefit long/short equity, macro/CTA, and long/short credit managers.

How might the upcoming US election and ongoing civil protests globally affect markets?

While equity and bond volatility will most likely not reach the levels seen in March, we believe the geopolitical uncertainties and slow economic recovery cycle will cause volatility to remain above average. Protests in Europe, Hong Kong and now the United States are indications of the frustrations felt by populations around the world. Laws and policies are being adjusted, moral codes are being re-written and inequities are being challenged.

The unhappiness of the populace alongside the strains of the health and economic crises may persist for a while. Specific to the United States, President Donald Trump’s recent policy decisions have caused his approval rating to drop. Some polls suggest that Democratic presidential candidate Joe Biden is leading in the race for the White House this November. While the market impact of a Biden victory is difficult to determine, the uncertainty between now and the election may well contribute to market volatility.

Will the geopolitical initiative from various countries to deglobalize prove sustainable?

Given the recent trade battles (United States/China) and economic bloc restructurings (Brexit), there seems to be a move by various countries to enhance their sovereign self-reliance. Government and business leaders speak of bringing production facilities and supply chains back from offshore locations to support local employment and avoid cross-border tariffs. This would entail a sizable shift in corporate capital expenditure plans and foreign exchange flows among the major economies of the world.

This shift in thinking may lead investors to rotate their investment flows away from those sectors that historically have benefited from lower-cost offshore labor or production facilities. Instead, the marginal investment assets may tilt toward companies and credits that are currently profitable in their local domicile.

Third-Quarter 2020 Outlook: Strategy Highlights

Discretionary Macro

The extraordinary policy measures taken so far to combat the health and economic crises related to COVID-19 may create attractive opportunities for nimble managers focused on macroeconomic developments. We think relative value opportunities may present themselves in macro asset classes like currencies, which can be driven by disparate policies and wide dispersion in economic conditions between countries before and after the policy implementation.

Long/Short Equity Generalist

COVID-19 has resulted in economic uncertainty, and coming out of the crisis, we do not anticipate a “one-size-fits-all” recovery. We expect share price dispersion across and within sectors while simultaneously accelerating the timeline of positive and negative long-term trends. Managers should be able to exploit the considerable uncertainty around the shape of the economic recovery.

Long/Short Credit

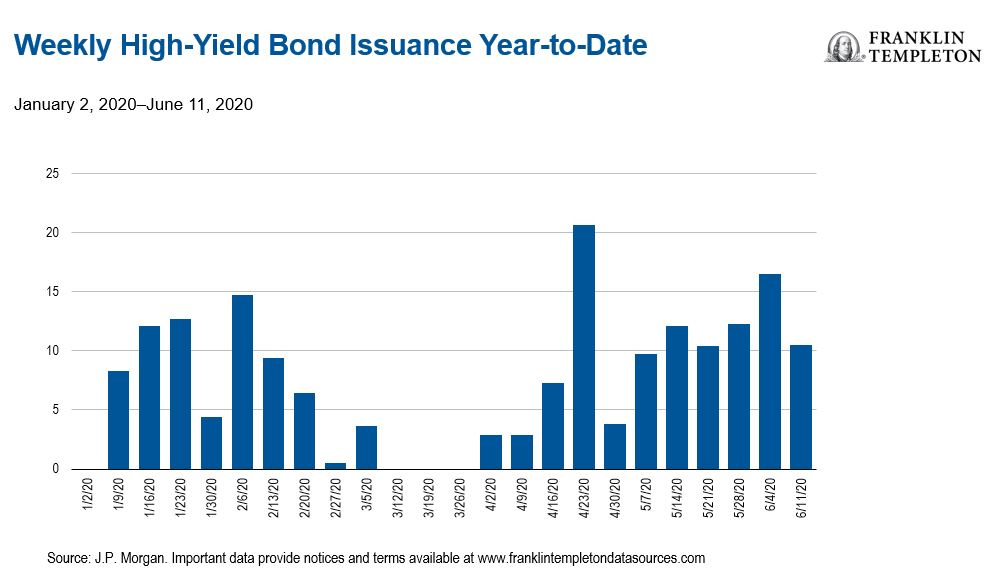

With credit markets gripped by extreme levels of volatility in March, new issuance in high yield froze. In response to the crisis, the US Federal Reserve introduced a number of emergency measures that effectively thawed key markets. Since then, the primary market has been extremely active, with issuers eagerly returning to capital markets. This level of activity can create opportunities for long/short credit managers in two respects.

First, managers can buy bonds directly from the company and sell them into the secondary market, often at a premium. Second, a flurry of activity often means the market is less discerning at the individual-deal level. Managers can apply a relative value approach, initiating a long position in one company against a short position in another company in the same industry, effectively isolating risk in the trade to the individual issuer.

What Are the Risks?

All investments involve risks, including possible loss or principal. Investments in alternative investment strategies and hedge funds (collectively, “Alternative Investments”) are complex and speculative investments, entail significant risk and should not be considered a complete investment program. Financial Derivative instruments are often used in alternative investment strategies and involve costs and can create economic leverage in the fund’s portfolio which may result in significant volatility and cause the fund to participate in losses (as well as gains) in an amount that significantly exceeds the fund’s initial investment. Depending on the product invested in, an investment in Alternative Investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. There can be no assurance that the investment strategies employed by K2 or the managers of the investment entities selected by K2 will be successful.

The identification of attractive investment opportunities is difficult and involves a significant degree of uncertainty. Returns generated from Alternative Investments may not adequately compensate investors for the business and financial risks assumed. An investment in Alternative Investments is subject to those market risks common to entities investing in all types of securities, including market volatility.

Also, certain trading techniques employed by Alternative Investments, such as leverage and hedging, may increase the adverse impact to which an investment portfolio may be subject.

Depending on the structure of the product invested, Alternative Investments may not be required to provide investors with periodic pricing or valuation and there may be a lack of transparency as to the underlying assets. Investing in Alternative Investments may also involve tax consequences and a prospective investor should consult with a tax advisor before investing. In addition to direct asset-based fees and expenses, certain Alternative Investments such as funds of hedge funds incur additional indirect fees, expenses and asset-based compensation of investment funds in which these Alternative Investments invest.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of date of publication and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

The information in this document is provided by K2 Advisors. K2 Advisors is a wholly owned subsidiary of K2 Advisors Holdings, LLC, which is a majority-owned subsidiary of Franklin Templeton Institutional, LLC, which, in turn, is a wholly owned subsidiary of Franklin Resources, Inc. (NYSE: BEN). K2 operates as an investment group of Franklin Templeton Alternative Strategies, a division of Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Investments are not FDIC insured; may lose value; and are not bank guaranteed.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments