The COVID-19 pandemic continues to impact economies across the globe as they emerge from lockdowns, including emerging markets. Our Emerging Markets Equity team provides an overview of developments over the past month, and takes a look at how the pandemic is driving a trend toward deglobalization as well as new innovations.

Three Things We’re Thinking About Today

- Geopolitical risk returned to the forefront as border tensions between China and India heightened, with the latter imposing economic measures including banning 50 Chinese apps and canceling government contracts with Chinese contractors. Although India has also renewed efforts to limit imports from China, we believe this would be challenging in view of India’s dependency on Chinese end-products as well as raw materials/machinery for its manufacturing supply chain. While geopolitical headlines relating to China have created noise and near-term uncertainty in recent years, they are unlikely to derail China from its path to recovery, in our view. The latest stimulus measures, including sizable fiscal spending, announced at the National Party Congress in late May, should provide positive catalysts to the domestic recovery in the nearer term. The government did not set an explicit growth target for China’s economy for 2020 due to the high level of uncertainty around the pandemic and global situation. However, it emphasized that employment as well as social measures (protecting basic livelihood) will be key priorities this year. This implies growth support and continued measured and targeted policy stimulus—with room for further stimulus if necessary—consistent with the trend Chinese policymakers have set thus far.

- The COVID-19 pandemic continues to add momentum to the discussion on deglobalization. This term has many potential meanings. It could simply refer to the re-shoring of certain strategic businesses, a reduced reliance on foreign supply chains, or the creation and/or support of national champions. However, some portray it to mean something more material. For instance, the collapse of international trade agreements and the organizations and associations that oversee them. So far, there is little evidence to suggest the latter is the case. Our view is that not all countries are keen to disrupt existing trade relationships. In fact, many continue to seek renewed trade deals, deepening their integration with others. Recent trade agreements include that between the European Union (EU) and Mercosur, while pending trade agreements include those between the United States and the United Kingdom. There are many positive examples across the globe of the benefits of trade and its ability to create wealth and opportunities for countries. Over the period 2009-2018, for instance, South Korean exports of goods and services rose by close to 60%, helping to fuel a nearly 30% rise in per-capita net income.1

Outlook

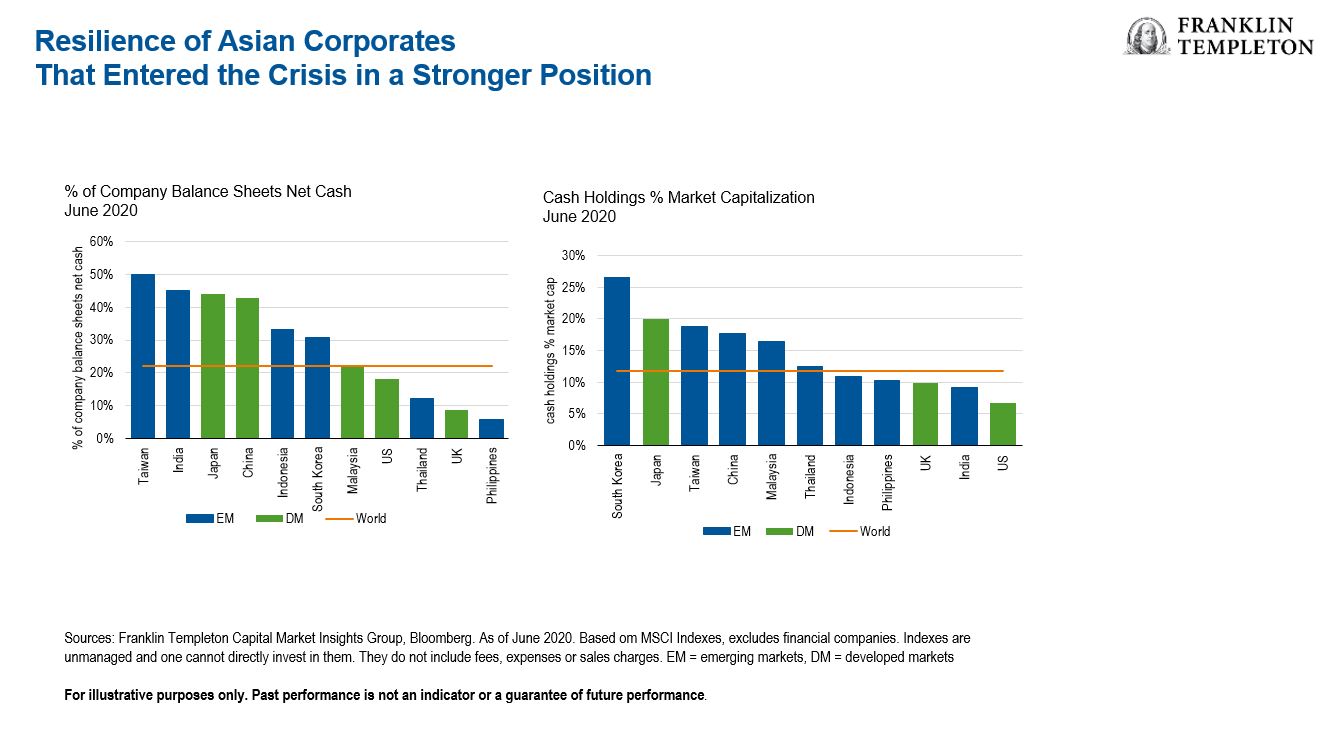

We believe that the COVID-19 pandemic has highlighted the strengths of the emerging world, including social systems, governance, and in many cases, health care. We have also seen solid progress in terms of reforms over the last decade, both from a fiscal and corporate point of view. As a result, we are seeing the financial strength of emerging economies and EM corporate balance sheets proving to be a source of resilience through the crisis. We expect this to continue to be the case, especially in Asia.

As an example, at the onset of COVID-19, when the scale of the crisis was yet to be fully known, many investors believed that EMs like China would require a significant amount of fiscal and monetary stimulus to get back on track. While we have seen some stimulus across EMs, the biggest source of stimulus, both fiscal and monetary, has in fact come from the developed world, And, it’s been at unprecedented levels which far exceed what we saw in the global financial crisis, raising the question of how that stimulus is going to be eventually recovered and paid for. We are of the opinion that is going to be a real hindrance and could lead to some headwinds for the developed world, at least for a while.

In addition, when placed alongside the developments in the corporate arena—where we have seen the notion of leapfrogging models and innovation come to the fore again in a range of industries including technology, consumerism as well as financials—this gives us a lot of optimism in these companies and some of these economies.

Emerging Markets Key Trends and Developments

EM equities rebounded in the second quarter, though they lagged developed market stocks. A gradual rollback of coronavirus-induced lockdowns around the world, better-than-expected economic indicators, optimism around potential COVID-19 treatments, and widespread economic stimulus outweighed fears of second-wave outbreaks and renewed US-China tensions. EM currencies were generally stronger against the US dollar. The MSCI Emerging Markets Index increased 18.2% during the quarter, while the MSCI World Index returned 19.5%, both in US dollars.2

The Most Important Moves in Emerging Markets in the Second Quarter of 2020

Asian equities were buoyant as all markets recorded strong gains in the quarter. Taiwan’s effective control of the pandemic lent support to its stock market, which witnessed a rally in technology heavyweights. In India, the start of lockdown relaxations lifted hopes for the economy’s recovery and drove equities higher, notwithstanding a flare-up in India-China border tensions. Stocks in South Korea rose as the authorities deployed monetary and fiscal stimulus to shore up the economy, while investors shrugged off military threats from North Korea. Chinese equities advanced on encouraging economic data, though the market trailed most of its regional peers. A resurgence in US-China frictions and a new coronavirus outbreak in Beijing checked investor sentiment.

Latin American markets joined the global rebound, with improving mobility trends offering support as governments continued to ease distancing measures. Argentina, Brazil and Chile led regional performances, while equity prices in Colombia, Peru and Mexico—despite recording double-digit gains—lagged their peers. Continued monetary easing drove sentiment in Brazil, as its central bank cut the key interest rate during the quarter by 1.5% to a record low of 2.25%. Improving political cooperation and better-than-expected economic activity data for April further supported sentiment. In Mexico, weak macroeconomic data and a sovereign credit rating downgrade shadowed the central bank’s monetary easing efforts. An additional stimulus package boosted sentiment in Chile, while a sovereign credit rating downgrade in Peru held back market returns there.

Markets in the Europe, Middle East and Africa region recorded a solid quarter with South Africa, the Czech Republic and Poland leading the pack. Qatar and Egypt, however, lagged their regional peers. South African equities rallied as investors chose to overlook sovereign credit downgrades and focus on the gradual lifting of lockdown measures, better-than-expected first-quarter gross domestic product (GDP) data and implementation of fiscal and monetary easing measures. Russia’s benchmark index, driven by strong appreciation in the ruble, higher oil prices and easing quarantine measures, also recorded double-digit returns over the three-month period. Voters passed a constitutional referendum that allows President Vladimir Putin to seek two additional terms, effectively remaining in power until 2036.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

1. Source: The World Bank.

2. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments